The Environment Agency's delayed release of updated flood risk data in January 2026 has created a critical valuation challenge: properties with documented flood resilience measures are commanding premiums of 7-15% in high-risk zones, yet standardized valuation methodologies remain inconsistent [5]. As climate projections extend to 2070 and surface water flooding becomes the UK's fastest-growing property risk, chartered surveyors face unprecedented pressure to quantify the financial value of flood barriers, elevated foundations, and resilient construction techniques. Understanding the Valuation Impacts of Flood Resilience Measures: RICS Adjustments for EA Flood Map Updates in 2026 has become essential for property professionals navigating this evolving landscape.

Key Takeaways

- 🏠 Properties with documented flood resilience measures command 7-15% valuation premiums in high-risk flood zones compared to unprotected equivalents

- 📊 EA flood map delays in 2026 require surveyors to use existing datasets while anticipating future climate change projections extending to 2070

- 💰 Insurance cost reductions of 30-50% directly impact property valuations, creating quantifiable financial benefits for resilient properties

- 📋 RICS Red Book valuations now require explicit consideration of flood resilience measures and their impact on marketability and insurance costs

- 🔄 Buyer negotiation tactics increasingly leverage flood risk assessments to secure price reductions or require resilience improvements as sale conditions

Understanding the 2026 Environment Agency Flood Map Updates

The Environment Agency's scheduled update for 2026 was intended to revolutionize how flood risk is assessed across England and Wales. The postponed release, announced on January 29, 2026, was designed to incorporate upper-end climate scenarios projecting flood risk through 2070 and beyond [5]. This delay has created significant challenges for property professionals who must continue relying on existing datasets while preparing for inevitable changes.

What Was Planned for the 2026 Updates

The Environment Agency's roadmap outlined several critical enhancements:

- Surface water flood risk modeling incorporating climate change projections

- Coastal erosion risk assessments with sea-level rise scenarios

- Updated river flood mapping reflecting changing precipitation patterns

- Integration of urban development impacts on flood pathways

- Enhanced granularity for property-level risk assessment

These updates align with the UK's Flood and Coastal Erosion Risk Management Strategy, which emphasizes building resilience into communities and infrastructure [7]. The strategy recognizes that traditional flood defenses alone cannot address the scale of future risk.

Impact of the Delay on Property Valuations

The postponement creates a valuation uncertainty gap where surveyors must balance current flood zone designations against anticipated future changes. Properties currently outside high-risk zones may face reclassification when updated maps eventually release, while some currently designated high-risk properties may benefit from improved modeling accuracy.

Key implications for valuers:

| Consideration | Current Challenge | Valuation Approach |

|---|---|---|

| Risk zone accuracy | Outdated baseline data | Apply precautionary adjustments |

| Climate projections | Unknown future classifications | Consider worst-case scenarios |

| Insurance availability | Based on current maps | Factor in potential premium increases |

| Marketability | Buyer uncertainty | Discount for perceived risk |

Chartered surveyors conducting RICS home surveys must now explicitly document flood risk considerations and explain limitations of current mapping data to clients.

RICS Red Book Standards for Flood Risk Valuation

The Royal Institution of Chartered Surveyors (RICS) provides comprehensive guidance through its Red Book valuation standards, which establish mandatory requirements for property valuations across the UK. When it comes to flood risk, RICS standards require valuers to consider all material factors affecting property value, including environmental risks and resilience measures.

Mandatory Considerations Under RICS Standards

RICS-registered valuers must investigate and report on:

✅ Location within Environment Agency flood zones (Zones 1, 2, or 3)

✅ Evidence of historical flooding or near-miss events

✅ Presence and effectiveness of flood defenses (community or property-level)

✅ Insurance availability and cost implications

✅ Planning restrictions related to flood risk

✅ Market perception and buyer demand in flood-prone areas

The Red Book valuation framework requires valuers to exercise professional judgment when quantifying risk impacts. This becomes particularly complex when evaluating properties with resilience measures, as there's no standardized methodology for calculating the value premium.

Valuation Methodology for Resilient Properties

When assessing the Valuation Impacts of Flood Resilience Measures: RICS Adjustments for EA Flood Map Updates in 2026, chartered surveyors employ several approaches:

1. Comparative Method with Resilience Adjustments

Compare similar properties with and without flood resilience measures, adjusting for:

- Construction cost of resilience features (typically £5,000-£50,000)

- Insurance premium differences (30-50% reduction potential)

- Marketability advantages in flood-risk areas

- Reduced maintenance and repair costs

2. Investment Method Considering Insurance Savings

Calculate the present value of future insurance cost savings:

- Annual insurance premium reduction: £500-£2,000

- Capitalization over property holding period

- Discount rate reflecting market conditions

- Risk of future premium increases without resilience

3. Residual Method for Development Properties

For new builds or major renovations incorporating resilience:

- Total development cost including resilience measures

- Enhanced market value due to flood certification

- Reduced insurance and maintenance costs

- Improved marketability and sales velocity

Professional surveyors conducting structural surveys must document all resilience features with photographs, specifications, and certification where available.

Quantifying Flood Resilience Measures in Property Valuations

The financial impact of flood resilience measures extends beyond construction costs to encompass insurance savings, marketability premiums, and reduced depreciation risk. Accurately quantifying these benefits requires understanding both the technical effectiveness of measures and market perception.

Types of Flood Resilience Measures and Their Value Impact

Different resilience strategies offer varying levels of protection and valuation impact:

Resistance Measures (Keeping Water Out)

-

Flood barriers and doors: £3,000-£8,000 installation

- Valuation premium: 3-5% in Flood Zone 3

- Insurance reduction: 20-30%

- Effectiveness: Up to 600mm flood depth

-

Non-return valves: £1,000-£3,000

- Valuation premium: 1-2%

- Insurance reduction: 10-15%

- Prevents sewage backflow

-

Sealed walls and floors: £5,000-£15,000

- Valuation premium: 2-4%

- Insurance reduction: 15-25%

- Protects building fabric

Resilience Measures (Minimizing Damage)

-

Elevated electrical systems: £2,000-£5,000

- Valuation premium: 2-3%

- Insurance reduction: 10-20%

- Reduces damage costs by 40-60%

-

Flood-resistant materials: £10,000-£30,000 (whole property)

- Valuation premium: 5-8%

- Insurance reduction: 25-40%

- Faster recovery, lower claims

-

Elevated foundations: £20,000-£80,000 (new build/major renovation)

- Valuation premium: 8-15%

- Insurance reduction: 40-50%

- Most effective long-term solution

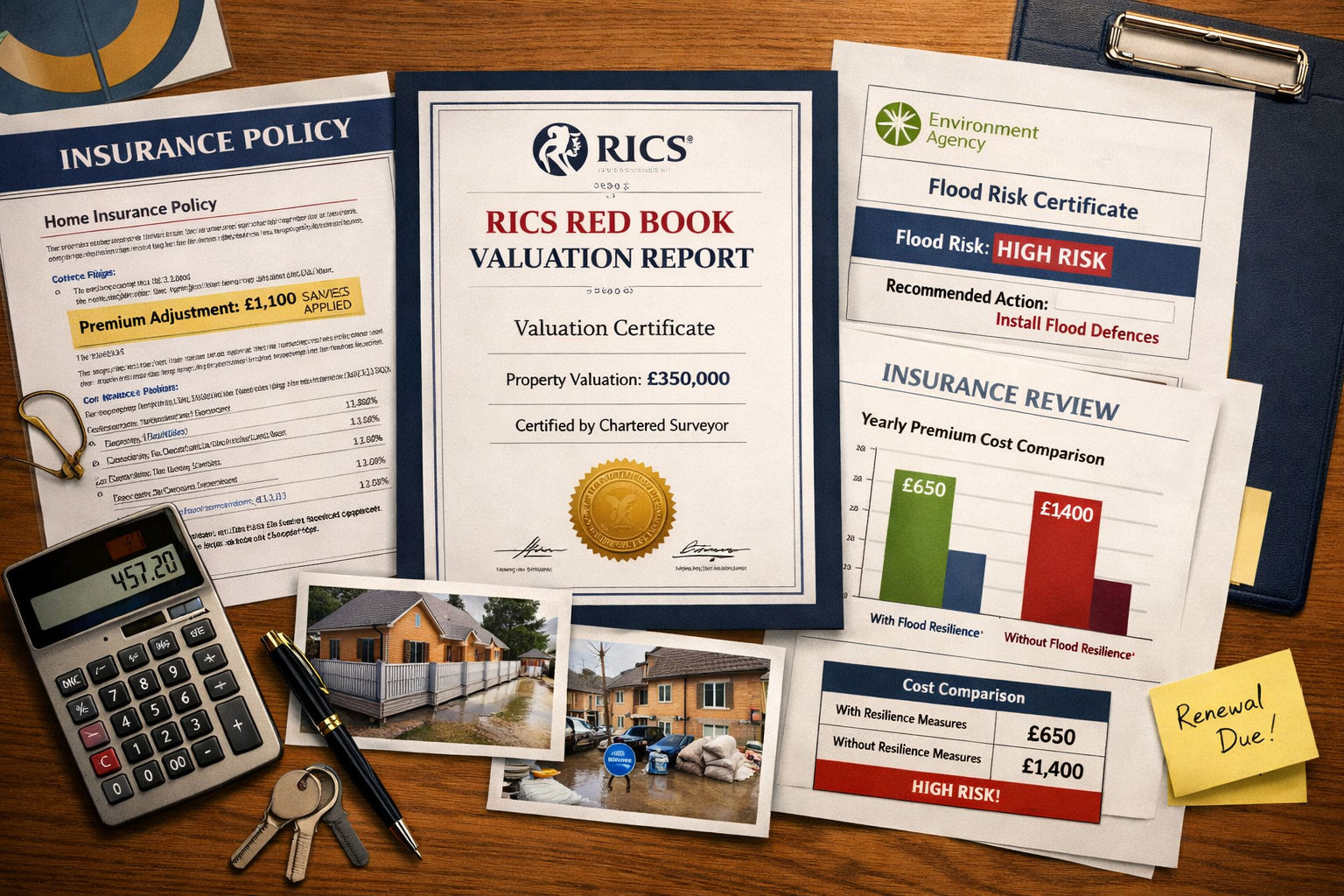

Insurance Cost Linkages and Valuation Premiums

The relationship between flood resilience and insurance costs creates direct, quantifiable value impacts that surveyors can incorporate into valuations. Properties in Flood Zone 3 without resilience measures may face:

- Annual premiums: £2,000-£5,000+

- High excess requirements: £2,500-£5,000

- Limited insurer options

- Potential uninsurability for repeat claims

With documented resilience measures:

- Annual premiums: £800-£2,500

- Standard excess: £250-£1,000

- Competitive insurer market

- Long-term insurability assurance

Calculating the valuation premium:

A property saving £2,000 annually on insurance over a 10-year holding period represents £20,000 in reduced costs. Using a 5% discount rate, the present value is approximately £15,400. This justifies a valuation premium roughly equivalent to the insurance savings plus the perceived marketability advantage.

When conducting RICS reinstatement cost valuations, surveyors must account for resilient construction specifications that may increase rebuild costs but reduce overall risk exposure.

Buyer Negotiation Tactics Leveraging Flood Risk Assessments

Sophisticated buyers and their advisors increasingly use flood risk assessments as powerful negotiation tools to secure price reductions or require sellers to implement resilience measures as conditions of sale. Understanding these tactics helps both buyers and sellers navigate transactions more effectively.

Pre-Purchase Flood Risk Due Diligence

Smart buyers commission comprehensive flood risk assessments before making offers:

Essential due diligence steps:

- Review Environment Agency flood maps for all risk types (river, surface water, coastal)

- Obtain historical flood data from local authorities and insurers

- Commission specialist flood risk assessments for properties in Zones 2 or 3

- Request insurance quotes before exchange to confirm availability and costs

- Inspect neighboring properties for evidence of flood damage or defenses

This information provides negotiating leverage when the seller hasn't disclosed flood risk adequately or when resilience measures are absent. Buyers can reasonably request:

- Price reductions equivalent to resilience measure installation costs (£10,000-£50,000)

- Seller-funded installation of basic flood defenses before completion

- Retention of funds in escrow pending resilience work completion

- Extended warranty coverage for flood-related damage

Negotiation Strategies Based on Resilience Status

Scenario 1: Property with No Resilience Measures in Flood Zone 3

Buyer position: Strong leverage for significant price reduction

- Request 10-15% price reduction to cover resilience installation

- Require seller to obtain Flood Performance Certificate

- Demand comprehensive flood insurance as completion condition

- Negotiate extended warranty for flood-related issues

Scenario 2: Property with Partial Resilience Measures

Buyer position: Moderate leverage for targeted improvements

- Identify gaps in resilience coverage (e.g., barriers but no elevated electrics)

- Request completion of resilience package or equivalent price reduction

- Verify certification and effectiveness of existing measures

- Negotiate insurance cost-sharing if premiums exceed expectations

Scenario 3: Property with Comprehensive Resilience Certification

Buyer position: Limited leverage but verification essential

- Verify all resilience measures are properly certified and maintained

- Confirm insurance benefits are transferable to new owner

- Request maintenance records and warranty documentation

- Negotiate modest discount if measures require updating or recertification

Buyers working with experienced surveyors for help to buy valuations should ensure flood risk is thoroughly assessed, as government-backed schemes may have specific requirements for flood-prone properties.

Future-Proofing Valuations: Climate Change Projections to 2070

The delayed EA flood map updates were intended to incorporate climate change projections extending to 2070, representing a fundamental shift in how flood risk is assessed over property lifecycles. While the data remains unavailable, surveyors must consider long-term climate impacts when valuing properties today.

Anticipated Changes in Flood Risk Mapping

Based on the Environment Agency's published strategy [7], future flood maps will likely reflect:

Precipitation Changes:

- 20-40% increase in winter rainfall intensity by 2070

- More frequent extreme weather events

- Increased surface water flooding in urban areas

- Overwhelmed drainage infrastructure in older developments

Sea-Level Rise:

- 0.5-1.2 meters rise by 2100 (depending on emissions scenarios)

- Expanded coastal flood zones affecting previously safe areas

- Increased tidal flood frequency

- Saltwater intrusion into groundwater

River Flow Changes:

- Higher peak flows during winter months

- Reduced summer flows affecting water quality

- Changed flood frequency from 1-in-100 year to 1-in-50 year events

- Erosion of riverbank properties

Incorporating Climate Scenarios into Current Valuations

Progressive surveyors are already incorporating climate considerations into valuations, even without official updated maps:

Precautionary valuation adjustments:

🌡️ Apply higher risk weighting to properties currently in Flood Zone 2 (medium risk)

🌡️ Consider properties within 500m of watercourses as potentially higher risk

🌡️ Factor in local topography and drainage patterns

🌡️ Assess proximity to combined sewer systems vulnerable to overflow

🌡️ Evaluate climate resilience of surrounding infrastructure

This approach aligns with international best practices. For example, New Jersey's 2026 REAL Rules require a Climate Adjusted Flood Elevation (CAFE) of FEMA's 100-year flood level plus 4 feet to account for sea-level rise [3]. While UK regulations haven't adopted similar mandatory adjustments, the principle of incorporating climate projections is gaining traction.

Investment Property Considerations

For investment properties and commercial valuations, climate risk assessment becomes even more critical:

- Rental yield impacts: Tenants increasingly avoid flood-risk properties

- Void period risks: Longer letting times in flood zones

- Maintenance cost escalation: Increased dampness and structural issues

- Exit strategy complications: Reduced buyer pool in future decades

- Financing challenges: Lenders becoming more risk-averse

Surveyors conducting probate valuations should consider whether flood risk will impact estate value realization timelines and achievable prices.

Practical Implementation: Case Studies and Examples

Case Study 1: Victorian Terrace in Flood Zone 3 with Comprehensive Resilience

Property: 3-bedroom Victorian terrace, Thames riverside location

Flood Zone: Zone 3 (high risk)

Resilience Measures: Flood barriers (£6,000), elevated electrics (£3,500), non-return valves (£2,000), flood-resistant plaster (£8,000)

Total Investment: £19,500

Valuation Impact:

- Comparable properties without resilience: £425,000

- Insurance cost difference: £1,800/year savings

- Marketability premium: 8%

- Adjusted valuation: £459,000

- Net value increase: £34,000 (175% return on resilience investment)

Case Study 2: New Build Development with Elevated Foundations

Property: 4-bedroom detached new build, coastal location

Flood Zone: Zone 2 (medium risk)

Resilience Measures: Elevated foundations (+600mm), integrated drainage system, flood-resistant construction throughout

Additional Construction Cost: £45,000

Valuation Impact:

- Standard comparable properties: £520,000

- Insurance cost difference: £2,200/year savings

- Enhanced marketability: 12%

- Adjusted valuation: £582,400

- Net value increase: £62,400 (139% return on resilience investment)

Case Study 3: Negotiation Outcome – Buyer-Secured Resilience Installation

Property: 2-bedroom cottage, river location

Original asking price: £315,000

Flood Zone: Zone 3 (no resilience measures)

Buyer's flood risk assessment: Identified £18,000 resilience requirement

Negotiation outcome:

- Initial offer: £285,000 (9.5% reduction)

- Seller counteroffer: £305,000 with £10,000 toward resilience measures

- Final agreement: £297,000 with seller installing flood barriers and non-return valves before completion

- Buyer achieved effective 5.7% discount plus guaranteed resilience measures

Professional Standards and Continuing Obligations

Chartered surveyors must maintain awareness of evolving flood risk standards and update their valuation methodologies accordingly. The Valuation Impacts of Flood Resilience Measures: RICS Adjustments for EA Flood Map Updates in 2026 represent an ongoing professional development requirement.

RICS Continuing Professional Development Requirements

RICS members must demonstrate competence in:

- Understanding current flood risk mapping and data sources [6]

- Applying appropriate valuation adjustments for environmental risks

- Recognizing and valuing flood resilience measures

- Advising clients on insurance implications

- Documenting assumptions and limitations in valuation reports

Regular training updates are essential as flood risk science evolves and new resilience technologies emerge.

Documentation and Reporting Best Practices

Comprehensive valuation reports addressing flood risk should include:

Mandatory sections:

- Flood Zone Designation: Current EA classification with map reference

- Historical Flood Events: Research into past flooding at property or vicinity

- Resilience Measures Inventory: Detailed description of all installed measures

- Insurance Assessment: Current availability, costs, and future outlook

- Valuation Adjustment Rationale: Clear explanation of premiums or discounts applied

- Limitations and Assumptions: Acknowledgment of data gaps (e.g., delayed EA updates)

- Recommendations: Suggested additional resilience measures if appropriate

This documentation protects both the surveyor and client by creating a transparent record of the valuation basis. For RICS registered valuers, maintaining these standards is essential for professional indemnity insurance coverage.

Conclusion: Navigating the New Flood Risk Valuation Landscape

The Valuation Impacts of Flood Resilience Measures: RICS Adjustments for EA Flood Map Updates in 2026 represent a fundamental shift in how property professionals assess and communicate flood risk. Despite the Environment Agency's delay in releasing updated mapping data, the direction of travel is clear: climate change is increasing flood risk across the UK, and properties with documented resilience measures command significant valuation premiums.

Key conclusions for property professionals:

💡 Flood resilience is now a material valuation factor, not an optional consideration

💡 Insurance cost linkages provide quantifiable justification for valuation premiums of 7-15%

💡 Buyer negotiation leverage is strongest for properties lacking resilience measures in high-risk zones

💡 Future-proofing valuations requires considering climate projections even without official updated maps

💡 Professional documentation and transparent methodology protect surveyors and inform clients

Actionable Next Steps

For Property Owners:

- Commission a flood risk assessment if your property is in Zones 2 or 3

- Investigate cost-effective resilience measures (start with barriers and elevated electrics)

- Obtain multiple insurance quotes to establish baseline costs

- Document all resilience investments with photographs and receipts

- Consider certification through Flood Protection Association schemes

For Buyers:

- Request flood risk information before making offers

- Commission independent flood assessments for at-risk properties

- Use lack of resilience measures as negotiation leverage

- Verify insurance availability and costs before exchange

- Budget for resilience improvements in purchase planning

For Surveyors and Valuers:

- Update valuation methodologies to explicitly address flood resilience

- Maintain current knowledge of EA mapping updates and climate projections

- Develop standardized approaches to quantifying resilience premiums

- Build relationships with flood risk specialists for complex cases

- Document assumptions and limitations transparently in reports

For Developers:

- Integrate flood resilience into design from project inception

- Budget for elevated foundations and resilient construction in flood-risk areas

- Market resilience features prominently to justify premium pricing

- Obtain third-party certification for resilience measures

- Consider climate projections to 2070 when selecting development sites

The property market is adapting to climate reality, and flood resilience is transitioning from niche concern to mainstream valuation factor. Professionals who master the Valuation Impacts of Flood Resilience Measures: RICS Adjustments for EA Flood Map Updates in 2026 will provide superior service to clients while protecting their own professional standards in an increasingly complex risk environment.

As the Environment Agency eventually releases its delayed mapping updates, expect further refinement of valuation methodologies and potentially significant reclassification of properties across risk zones. Staying ahead of these changes through continuous professional development and proactive risk assessment will distinguish leading practitioners in the years ahead.

References

[1] Fema Announces Policy Updates To Flood Risk Analysis And Mapping Standards – https://www.floods.org/whats-new/fema-announces-policy-updates-to-flood-risk-analysis-and-mapping-standards/

[2] Njdeps Real Rule Revisions Enter Final Phase What It Means For Coastal Development – https://riker.com/blog/environmental-law/njdeps-real-rule-revisions-enter-final-phase-what-it-means-for-coastal-development/

[3] Njdep 2026 Real Rules Set To Impact Construction Near Nj Coast – https://lanassociates.com/industry-insights/njdep-2026-real-rules-set-to-impact-construction-near-nj-coast/

[4] 2026 02 12 Fema Unveils Updated Flood Maps That Could Impact Insurance – https://ktrh.iheart.com/featured/houston-texas-news/content/2026-02-12-fema-unveils-updated-flood-maps-that-could-impact-insurance/

[5] Flood Risk Data Delay Slows Planning And Housing Delivery – https://www.unda.co.uk/news/flood-risk-data-delay-slows-planning-and-housing-delivery/

[6] Updates To National Flood And Coastal Erosion Risk Information – https://www.gov.uk/guidance/updates-to-national-flood-and-coastal-erosion-risk-information

[7] Fcerm Strategy Roadmap To 2026 Final – https://assets.publishing.service.gov.uk/media/629de862e90e07039c27b440/FCERM-Strategy-Roadmap-to-2026-FINAL.pdf

[8] Usace Publishes Policy Update For Inundation Maps And The National Inventory Of – https://www.usace.army.mil/Media/News-Releases/News-Release-Article-View/Article/2483323/usace-publishes-policy-update-for-inundation-maps-and-the-national-inventory-of/