While the UK property market shows signs of stabilisation in 2026, not all regions are experiencing equal recovery. Valuation Adjustments for East Anglia and South West Lagging Recovery: Bridging Affordability Gaps in Slower Markets has become a critical concern for surveyors, lenders, and property professionals navigating these underperforming regions. East Anglia currently stands as the only UK region experiencing declining values, while the South West continues to lag behind national trends despite modest price increases. Understanding how to adjust valuation frameworks for these affordability-constrained markets is essential for accurate property assessments in 2026.

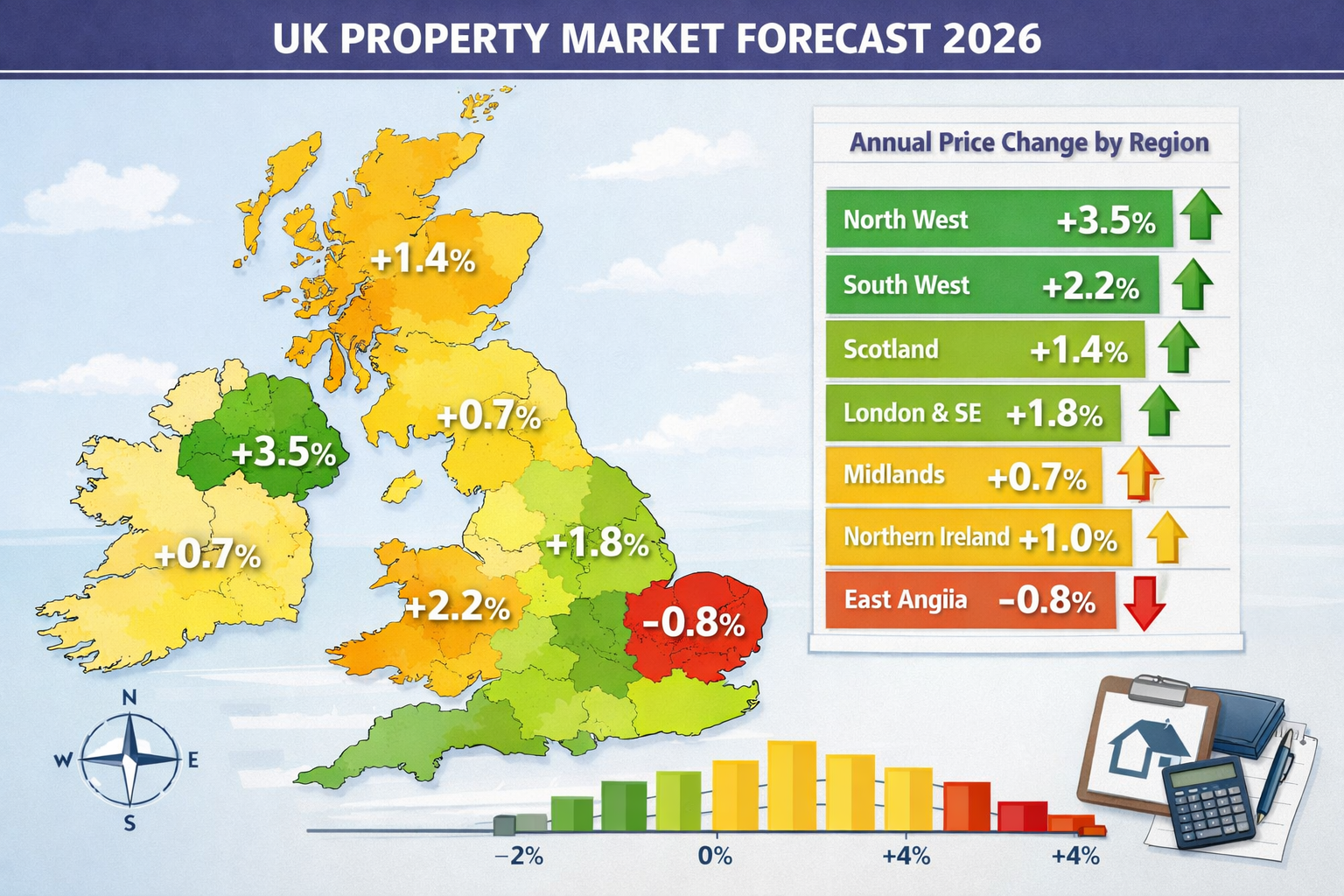

The stark regional divergence in property performance demands a nuanced approach to valuation methodology. With East Anglia recording -0.8% annual decline and the South West showing subdued growth of just +2.2%, compared to the North West's robust +3.5% appreciation, surveyors must recalibrate their comparative analysis techniques and risk assessments.[5] These slower markets present unique challenges that require specialized knowledge of local affordability constraints, supply dynamics, and buyer behaviour patterns.

Key Takeaways

- 📉 East Anglia is the only declining UK region at -0.8% annually, creating a 4.3 percentage point gap with top-performing areas

- 🏘️ Southern regions face structural affordability challenges with London (+0.7%) and South East (+0.1%) substantially underperforming national trends

- 📊 Supply imbalances drive regional divergence, with London stock up 16% and South East up 9% year-on-year, tempering price growth

- 💷 Price realism enforcement accelerated with 809,000 reductions across southern markets in 2025, signalling seller adaptation

- 🔄 Valuation adjustments must account for local constraints, including increased inventory, affordability pressures, and slower demand recovery

Understanding the Regional Performance Gap in 2026

The East Anglia Decline: A Unique Market Position

East Anglia's position as the only declining UK region in early 2026 represents a significant departure from national market trends. The -0.8% annual decline reflects deep-seated affordability constraints that have finally manifested as price corrections.[5] This performance creates substantial challenges for property valuations, as traditional comparable analysis methods may overstate current market values when relying on historical transaction data.

The region's decline isn't driven by lack of demand alone but rather by a fundamental mismatch between buyer purchasing power and asking prices. Wage growth in East Anglia has failed to keep pace with the property price inflation experienced during the 2020-2022 period, creating an affordability ceiling that now constrains market activity.

For surveyors conducting capital gains tax valuations or other retrospective assessments in East Anglia, understanding this decline trajectory is crucial for accurate historical value reconstruction.

South West's Modest Recovery Masks Underlying Pressures

The South West presents a more complex picture. While prices increased to £299,331 in August 2025 (+0.3% month-on-month, +2.2% year-on-year), this modest growth significantly lags the national recovery momentum.[3] More concerning for valuation professionals is the 7.2% year-on-year decline in prime market asking prices, which averaged £968,787 in early 2026.

This dual-speed market within the South West requires surveyors to carefully segment their analysis between:

- Standard residential markets showing marginal positive growth

- Prime and coastal properties experiencing continued price pressure

- Rural holdings with variable performance based on local amenity factors

The 10% increase in homes for sale compared with the prior year has created downward pressure on price growth despite easing borrowing costs and improving wage trends.[3] This supply-driven constraint fundamentally alters the valuation landscape for the region.

The North-South Divide Intensifies

The performance gap between northern and southern regions has widened substantially in 2026. The North West leads with +3.5% annual growth, while Scotland and Northern Ireland show strong upward trends.[1] This creates a 4.3 percentage point differential between the best and worst performing regions—the widest gap in recent years.

| Region | Annual Price Change | Key Driver | Valuation Impact |

|---|---|---|---|

| North West | +3.5% | Strong affordability, steady supply | Positive adjustments needed |

| Scotland | +2.8% | Improved buyer confidence | Moderate upward pressure |

| National Average | +1.5% | Stabilising conditions | Baseline comparisons |

| South West | +2.2% | Supply increase, affordability constraints | Downward pressure on prime |

| South East | +0.1% | High stock levels, affordability ceiling | Minimal growth adjustment |

| London | +0.7% | Oversupply, affordability barriers | Subdued recovery trajectory |

| East Anglia | -0.8% | Severe affordability constraints | Negative adjustments required |

This regional divergence demands that surveyors adjust their comparable selection criteria and apply appropriate geographic weighting when determining market values in slower-recovering areas.

Affordability Constraints Driving Valuation Adjustments for East Anglia and South West

Supply Imbalances Creating Downward Pressure

One of the most significant factors requiring valuation adjustments in southern regions is the dramatic increase in housing stock. London experienced a 16% year-on-year increase in available properties, while the South East saw a 9% rise in Q1 2026.[2] These supply increases stand in stark contrast to northern regions, which maintained relatively flat inventory levels.

The South West's 10% increase in homes for sale has directly contributed to tempering price growth despite improving macroeconomic conditions.[3] For valuation professionals, this supply dynamic requires careful consideration when:

- Selecting comparable properties from different time periods

- Adjusting for market conditions between contract and completion dates

- Assessing the likelihood of achieving asking prices

- Evaluating time-on-market expectations for Help to Buy valuations

Price Reduction Trends Signal Market Realism

The acceleration of price reductions provides concrete evidence of market adjustment. With 809,000 price reductions recorded across the South West and southern markets in 2025—7.8% higher than the prior year—sellers are actively adapting to affordability-driven conditions.[3] This trend has important implications for valuation methodology:

✅ Asking prices increasingly unreliable as initial valuation benchmarks

✅ Achieved sale prices provide more accurate market indicators

✅ Time-on-market adjustments become critical for comparable analysis

✅ Negotiation margins widen, requiring conservative valuation approaches

Surveyors conducting Right to Buy valuations in these regions must particularly account for the gap between initial asking prices and eventual achieved prices when determining fair market value.

Borrowing Cost Relief Provides Partial Support

Despite affordability challenges, declining borrowing costs offer some relief to buyer purchasing power. Mortgage rates are forecast to reach their lowest levels in three years during 2026, which should provide modest support to buyer confidence and transaction volumes.[4]

However, this positive factor alone cannot overcome the structural affordability constraints in East Anglia and the South West. The combination of:

- High absolute property prices relative to local wages

- Increased supply creating buyer choice

- Reduced urgency in post-pandemic market conditions

…means that improved borrowing terms translate to slower price recovery rather than renewed price inflation in these regions.

Wage-to-Price Ratios Remain Stretched

The fundamental affordability challenge stems from wage-to-price ratios that remain historically stretched in southern England. While wage growth has improved modestly in 2026, it has not kept pace with the property price inflation experienced during 2020-2022, particularly in previously high-performing areas like East Anglia and the South West.

This creates a ceiling effect on property values that surveyors must incorporate into their assessments. Properties priced above local affordability thresholds face extended marketing periods and increased likelihood of price reductions—factors that should inform valuation judgements.

Practical Valuation Frameworks for Slower Market Conditions

Adjusting Comparable Selection Criteria

When conducting valuations in East Anglia and the South West, comparable property selection requires more rigorous scrutiny than in stable or appreciating markets. Standard approaches may need modification:

Time Period Adjustments

In declining or flat markets, more recent comparables carry greater weight. Consider:

- Prioritising sales completed within the last 3 months over 6-month data

- Applying negative time adjustments when using older comparables in East Anglia

- Recognising that pre-2025 transactions may overstate current values

Supply Condition Adjustments

Properties sold during periods of lower inventory may have achieved higher prices:

- Research inventory levels at time of comparable sales

- Apply downward adjustments for comparables from lower-supply periods

- Consider seasonal supply variations in coastal South West markets

Motivation and Marketing Period Factors

Extended marketing periods signal weaker demand:

- Properties selling quickly may indicate under-pricing rather than strong market

- Extended time-on-market comparables better reflect current conditions

- Distinguish between motivated and unmotivated seller transactions

For professionals conducting Level 3 building surveys that include valuation components, these adjusted comparable criteria become essential for accurate market value assessments.

Geographic Micro-Market Analysis

The Valuation Adjustments for East Anglia and South West Lagging Recovery: Bridging Affordability Gaps in Slower Markets require recognition that performance varies significantly within these regions:

East Anglia Micro-Markets:

- 🏘️ Cambridge and university towns: Relatively resilient due to institutional demand

- 🌾 Rural Norfolk and Suffolk: More pronounced decline in agricultural areas

- 🏖️ Coastal communities: Variable performance based on second-home demand

South West Micro-Markets:

- 🏙️ Bristol and urban centres: Stronger performance than regional average

- 🏖️ Premium coastal locations: Significant prime market correction (-7.2%)

- 🏞️ Rural Devon and Cornwall: Mixed performance with affordability constraints

Surveyors should avoid region-wide generalisations and instead conduct detailed local market research for each specific location. What applies in Cambridge may not reflect conditions in rural Norfolk, despite both being within East Anglia.

Risk Assessment and Valuation Ranges

In slower markets with declining or minimal growth trajectories, valuation certainty decreases. Professional surveyors should consider:

Wider Valuation Ranges

Single-point valuations may not adequately reflect market uncertainty:

- Provide valuation ranges rather than single figures where appropriate

- Clearly communicate confidence levels in valuation conclusions

- Document market volatility factors affecting valuation certainty

Downside Risk Weighting

In declining markets like East Anglia:

- Weight comparables toward lower end of range

- Apply conservative adjustments for property-specific factors

- Consider worst-case scenarios in risk assessments for lenders

Market Condition Caveats

Transparent communication about market constraints:

- Explicitly reference regional underperformance in valuation reports

- Note supply-demand imbalances affecting marketability

- Highlight affordability constraints limiting buyer pool

These approaches align with RICS professional standards while providing clients with realistic assessments in challenging market conditions.

Incorporating Forward-Looking Indicators

While valuations reflect current market conditions, understanding trajectory and momentum helps inform professional judgement:

Expert Forecast Integration

Major forecasters including Knight Frank and Savills have downwardly revised their 2026 UK price projections, specifically citing high supply levels as a restraining factor—particularly relevant for southern regions.[4] These institutional views should inform surveyor expectations about near-term market direction.

Supply Pipeline Monitoring

Tracking new listings and inventory trends provides early warning:

- Continued inventory increases suggest ongoing price pressure

- Stabilising supply levels may indicate approaching market equilibrium

- Seasonal patterns should be factored into supply assessments

Transaction Volume Trends

Market activity levels signal buyer confidence:

- Increasing transaction volumes suggest improving market health

- Declining activity indicates continued buyer caution

- Compare current volumes to historical norms for context

For surveyors working on homebuyer surveys in these regions, incorporating these forward-looking factors helps clients understand not just current value but likely near-term market trajectory.

Regional-Specific Valuation Considerations

East Anglia: Valuing in a Declining Market

Conducting valuations in the only declining UK region presents unique challenges that require specific methodological adjustments:

Negative Time Adjustments

Unlike appreciating markets, East Anglia valuations may require:

- Downward adjustments when using comparables from 6-12 months prior

- Recognition that recent sales may already reflect declining trajectory

- Careful analysis of whether decline is accelerating or stabilising

Affordability Ceiling Analysis

Understanding local wage levels becomes critical:

- Research median household incomes for specific postcode areas

- Calculate affordability ratios for subject properties

- Recognise that properties exceeding 5x local income face limited demand

Exit Strategy Considerations

For investment or commercial property valuations:

- Assess liquidity and likely marketing periods

- Consider potential for further decline before sale

- Evaluate rental yields as alternative value indicator

Positive Factors to Monitor

Not all indicators are negative:

- Cambridge's technology sector provides employment support

- Infrastructure improvements (rail connections) may boost specific areas

- Declining borrowing costs should eventually provide demand support

South West: Navigating Dual-Speed Markets

The South West's modest overall growth masks significant internal variation, requiring careful market segmentation:

Prime vs. Standard Market Differentiation

The 7.2% decline in prime asking prices contrasts sharply with the 2.2% growth in standard markets.[3] Surveyors must:

- Clearly identify whether subject property falls within prime segment

- Apply different comparable criteria for prime vs. standard properties

- Recognise that prime market recovery may lag standard market

Coastal vs. Inland Dynamics

Second-home demand affects coastal areas differently:

- Coastal properties face higher supply levels from investor sales

- Inland properties benefit from local owner-occupier demand

- Holiday let potential adds complexity to valuation analysis

Supply Pressure Adjustments

The 10% increase in available homes requires:

- Downward adjustments for properties in oversupplied micro-markets

- Recognition that buyer negotiating power has increased

- Conservative marketing period assumptions

For professionals conducting building surveys in the South West, understanding these dual-speed dynamics ensures valuation components accurately reflect specific local conditions rather than regional averages.

London and South East Context

While not the primary focus, London (+0.7%) and South East (+0.1%) performance provides important context for understanding southern England's affordability challenges.[5]

Capital Market Influences

London's underperformance affects surrounding regions:

- Commuter belt areas in East Anglia affected by London weakness

- South East markets tied to London employment patterns

- International buyer sentiment impacts prime southern markets

Supply Overhang Effects

The 16% increase in London stock creates ripple effects:

- Buyers have increased choice across southern England

- Competition from London alternatives affects South East and East Anglia

- Supply discipline becomes critical for achieving asking prices

Professional Standards and Regulatory Considerations

RICS Red Book Compliance in Slower Markets

The RICS Valuation – Global Standards (Red Book) provides the framework for professional valuations, but application in slower markets requires particular attention:

Market Value Definition

The Red Book defines market value as "the estimated amount for which an asset should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion."

In declining or slow markets, this definition requires careful interpretation:

- ✅ "Proper marketing" may mean extended periods in slower markets

- ✅ "Willing buyer" assumes reasonable motivation, not distressed purchase

- ✅ "Knowledgeably" requires both parties understand market conditions

Assumptions and Special Assumptions

Transparency about market conditions:

- Clearly state assumptions about marketing period

- Note any special assumptions regarding market trajectory

- Document limitations in comparable evidence availability

Uncertainty and Material Uncertainty Declarations

When market conditions create significant valuation uncertainty:

- Consider whether material uncertainty declaration is appropriate

- Provide clear reasoning for valuation conclusions

- Document range of possible values where single point is difficult

Lender Requirements and Conservative Approaches

Mortgage lenders operating in East Anglia and the South West increasingly require conservative valuation approaches that account for regional underperformance:

Loan-to-Value Considerations

Declining or flat markets affect LTV risk assessment:

- Lower LTVs may be required in declining markets like East Anglia

- Lenders may apply regional risk adjustments to lending criteria

- Valuation methodology should align with lender risk appetite

Reinstatement Cost Assessments

For reinstatement cost valuations, market performance doesn't directly affect rebuild costs, but:

- Insurance valuations remain independent of market value

- Lenders require both market value and reinstatement cost

- Significant gaps between values may trigger additional scrutiny

Valuation Validity Periods

In volatile or declining markets:

- Shorter validity periods may be appropriate (60-90 days vs. standard 120 days)

- Lenders may require revaluations if completion delays occur

- Material market changes may necessitate updated valuations

Bridging the Affordability Gap: Market Solutions and Outlook

Government and Policy Interventions

Addressing the Valuation Adjustments for East Anglia and South West Lagging Recovery: Bridging Affordability Gaps in Slower Markets may require policy interventions:

Regional Affordability Programs

Targeted support for underperforming regions:

- Enhanced Help to Buy schemes for first-time buyers in slower markets

- Regional variations in stamp duty or transaction taxes

- Infrastructure investment to support economic growth and wages

Supply-Side Measures

While increased supply contributes to current pressure:

- Long-term housing supply remains inadequate nationally

- Planning reform could address affordability over time

- Social housing investment reduces pressure on private market

Market Self-Correction Mechanisms

Markets naturally adjust to affordability constraints through several mechanisms already evident in 2026:

Price Realism

The 809,000 price reductions in 2025 demonstrate seller adaptation.[3] Continued price discipline will:

- Gradually bring properties within affordability range

- Reduce inventory overhang as realistic pricing attracts buyers

- Restore transaction volumes to healthier levels

Wage Growth Catch-Up

If property prices remain flat while wages grow:

- Affordability ratios gradually improve without price declines

- Buyer purchasing power increases over time

- Market equilibrium can be restored through relative adjustment

Migration and Demand Shifts

Population movement may redistribute demand:

- Northern regions' stronger performance attracts migration

- Remote work enables relocation from expensive southern areas

- Demand rebalancing could support northern growth while easing southern pressure

2026-2027 Outlook for East Anglia and South West

Based on current trends and expert forecasts, the outlook for these slower markets includes:

Short-Term Expectations (2026)

- 📉 East Anglia likely to continue modest decline or flatten

- 📊 South West expected to show subdued growth below national average

- 💷 Affordability constraints to persist despite lower borrowing costs

- 🏘️ Supply levels to remain elevated, limiting price growth potential

Medium-Term Trajectory (2027-2028)

- 🔄 Gradual market stabilisation as prices align with affordability

- 📈 Potential for recovery acceleration if wage growth continues

- 🌍 International buyer return could support prime South West markets

- ⚖️ North-south gap may begin narrowing as northern growth moderates

Valuation Implications

Surveyors should:

- Maintain conservative approaches through 2026

- Monitor leading indicators for signs of market stabilisation

- Prepare for potential methodology adjustments as conditions evolve

- Continue rigorous comparable analysis with appropriate adjustments

Expert Perspective: "The regional divergence we're seeing in 2026 is primarily affordability-driven rather than demand-driven. Southern markets haven't lost their fundamental appeal—they've simply priced beyond local buyer capacity. As this rebalancing occurs, valuation professionals must maintain rigorous analytical standards while recognising that slower recovery doesn't mean permanent decline." — Market Analysis, RICS Survey January 2026[1]

Conclusion

Valuation Adjustments for East Anglia and South West Lagging Recovery: Bridging Affordability Gaps in Slower Markets represents one of the most significant challenges facing property professionals in 2026. With East Anglia experiencing the UK's only regional decline at -0.8% annually and the South West showing subdued growth of just +2.2%, surveyors must adapt their methodologies to accurately reflect these affordability-constrained market conditions.[5][3]

The fundamental drivers of underperformance—structural affordability constraints, elevated supply levels, and stretched wage-to-price ratios—require comprehensive adjustments to traditional valuation frameworks. From comparable selection criteria to risk assessment approaches, professional surveyors must apply more rigorous analytical standards when working in these slower markets.

Actionable Next Steps for Property Professionals

For Surveyors and Valuers:

- ✅ Review and update comparable databases to prioritise recent transactions from the last 3 months

- ✅ Implement micro-market analysis rather than relying on regional averages

- ✅ Apply conservative adjustments when using older comparables in declining markets

- ✅ Document market conditions thoroughly in valuation reports with clear caveats

- ✅ Monitor supply trends and inventory levels as leading indicators of market direction

For Buyers and Investors:

- 🔍 Commission thorough professional valuations from chartered surveyors experienced in slower markets

- 💡 Recognise opportunity in markets where affordability corrections create value

- 📊 Assess rental yields as alternative value indicators in flat price environments

- ⏱️ Prepare for extended marketing periods if purchasing for resale

- 🎯 Focus on micro-market fundamentals rather than regional generalisations

For Lenders and Financial Institutions:

- 🛡️ Apply appropriate regional risk adjustments to lending criteria

- 📋 Require detailed market condition commentary in valuation reports

- 🔄 Consider shorter valuation validity periods in volatile markets

- 💼 Engage experienced local surveyors familiar with regional dynamics

- 📈 Monitor portfolio exposure to underperforming regions

The path forward requires patience, analytical rigour, and realistic expectations. While East Anglia and the South West currently lag the national recovery, markets are self-correcting through price realism, improved affordability ratios, and natural demand rebalancing. Professional surveyors who adapt their methodologies to these slower market conditions will provide the most valuable guidance to clients navigating these challenging regional dynamics.

As borrowing costs continue to decline through 2026 and wage growth gradually improves affordability ratios, these regions should eventually stabilise and begin recovery—though the timeline remains uncertain. Until then, maintaining conservative valuation approaches while monitoring leading indicators will serve property professionals and their clients best in these affordability-constrained markets.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Uk Residential Property Market Update Spring 2026 – https://www.vailwilliams.com/uk-residential-property-market-update-spring-2026/

[3] South West Regional Market Report – https://www.fineandcountry.co.uk/insights/property-market-reports/south-west-regional-market-report

[4] The Property Market In 2026 Britains Top Experts On What You Can Expect And Its Good News All Round – https://www.countrylife.co.uk/property/the-property-market-in-2026-britains-top-experts-on-what-you-can-expect-and-its-good-news-all-round

[5] January 2026 Market Outlook Record Asking Prices Meet Stubborn Reality – https://www.shojin.co.uk/insights/january-2026-market-outlook-record-asking-prices-meet-stubborn-reality