Nearly one in five privately rented homes in England contains at least one Category 1 hazard under the Housing Health and Safety Rating System (HHSRS) — and from 2026, fire hazards sit squarely at the top of that enforcement agenda. The expansion of Awaab's Law into the private rented sector (PRS) means that fire hazard valuations under extended Awaab's Law, Level 3 building survey protocols for PRS compliance, and risk premium adjustments in 2026 are no longer optional considerations for landlords and surveyors. They are legal imperatives with direct financial consequences. [1][2]

This guide breaks down what surveyors, landlords, and investors must know: how fire hazards are now classified, what Level 3 survey protocols must capture, and how risk premiums are recalculated in the post-Awaab's PRS landscape.

Key Takeaways 🔑

- Fire hazards are now a prescribed category under Phase 2 of Awaab's Law (2026), requiring landlords to respond within strict statutory timeframes.

- Level 3 building surveys must now integrate EWS1-style fire assessments for PRS properties, covering cladding, compartmentalisation, and means of escape.

- Risk premium adjustments of 5–20% on property valuations are emerging as standard where unresolved fire defects are identified.

- Remediation cost schedules must be included in survey reports to support valuation deductions and insurance negotiations.

- Non-compliance exposes PRS landlords to enforcement action, civil penalties, and significant portfolio devaluation.

What Extended Awaab's Law Means for Fire Hazards in 2026

The Legislative Shift

Awaab's Law was born from tragedy — the death of two-year-old Awaab Ishak in 2020 due to prolonged exposure to damp and mould in a social housing property. Phase 1 of the law imposed strict repair timelines on social landlords. Phase 2, effective 2026, extends the prescribed hazard categories to include fire hazards, alongside electrical hazards, excess cold and heat, and structural collapse risks. [2][3]

Critically, the 2026 expansion also brings the private rented sector into scope. This is a seismic shift. Social landlords have had years to prepare compliance frameworks. Many PRS landlords — particularly small portfolio holders — are only now beginning to understand what this means for their properties and their balance sheets. [3]

What Counts as a Fire Hazard Under the Extended Framework?

Under the HHSRS, fire hazards are assessed by likelihood of occurrence and potential harm. The extended Awaab's Law framework integrates these into a prescribed response timeline, meaning:

| Hazard Severity | Required Response Timeline |

|---|---|

| Emergency (imminent risk) | 24 hours |

| Urgent (Category 1) | 7 days |

| Serious (Category 1, non-immediate) | 28 days |

| Category 2 (lower risk) | Reasonable period |

Fire-specific hazards now triggering these timelines include:

- Defective fire detection systems (missing or non-functional smoke/heat alarms)

- Compromised fire compartmentalisation (breached fire doors, unsealed penetrations)

- Combustible cladding or insulation (EWS1-relevant materials)

- Blocked or inadequate means of escape

- Faulty electrical installations contributing to ignition risk [4]

💬 "The integration of fire hazards into Awaab's prescribed list is not a procedural update — it is a fundamental rewriting of the risk calculus for every PRS landlord in England."

Level 3 Building Survey Protocols for PRS Fire Hazard Compliance

Why a Level 3 Survey Is Now the Baseline

A Level 2 HomeBuyer Report simply cannot capture the granular defect detail that fire hazard compliance now demands. For PRS properties — particularly those built before 2000 or containing converted flats — a Level 3 building survey is the minimum appropriate instruction. Understanding the key differences between Level 2 and Level 3 surveys is essential before commissioning any fire hazard assessment in 2026.

A Level 3 survey provides:

- Full structural inspection including roof voids, floor voids, and wall cavities

- Defect identification with causation analysis

- Remediation cost estimates (essential for risk premium calculations)

- Photographic evidence suitable for insurance and enforcement proceedings

- Condition ratings aligned with HHSRS scoring

For many surveyors, understanding what a surveyor checks during an inspection is now inseparable from understanding fire safety obligations under the extended law.

EWS1-Style Integration Into Routine Valuations

The External Wall System (EWS1) assessment was originally designed for high-rise buildings post-Grenfell. In 2026, its principles are being embedded into routine Level 3 survey protocols for any PRS property with external wall systems that could present a fire spread risk — including two-storey converted flats with timber-frame extensions, properties with EIFS (External Insulation Finishing Systems), and older stock with unknown cavity fill materials.

Surveyors conducting fire hazard valuations under extended Awaab's Law must now document:

- ✅ External wall construction type and material identification

- ✅ Fire door condition, certification, and self-closing mechanism function

- ✅ Compartmentalisation integrity (including ceiling voids in converted properties)

- ✅ Smoke and heat detection coverage and alarm interlink status

- ✅ Escape route width, obstruction risk, and signage compliance

- ✅ Electrical installation condition (EICR currency and findings)

- ✅ Evidence of previous fire damage or near-miss incidents

The Remediation Cost Schedule: A New Survey Deliverable

One of the most significant protocol changes in 2026 is the expectation that Level 3 survey reports for PRS properties include a remediation cost schedule for identified fire hazards. This serves three purposes:

- Valuation support: Provides the surveyor with a defensible basis for applying a risk premium deduction

- Insurance negotiation: Insurers increasingly require costed defect schedules before quoting PRS fire cover

- Compliance planning: Landlords can use the schedule to demonstrate a good-faith remediation programme to enforcement officers

For a comprehensive understanding of what a full structural survey report should contain, reviewing a full structural survey sample provides useful context on the expected depth of reporting.

Risk Premium Adjustments: How Fire Hazards Affect PRS Property Values

The Valuation Framework in 2026

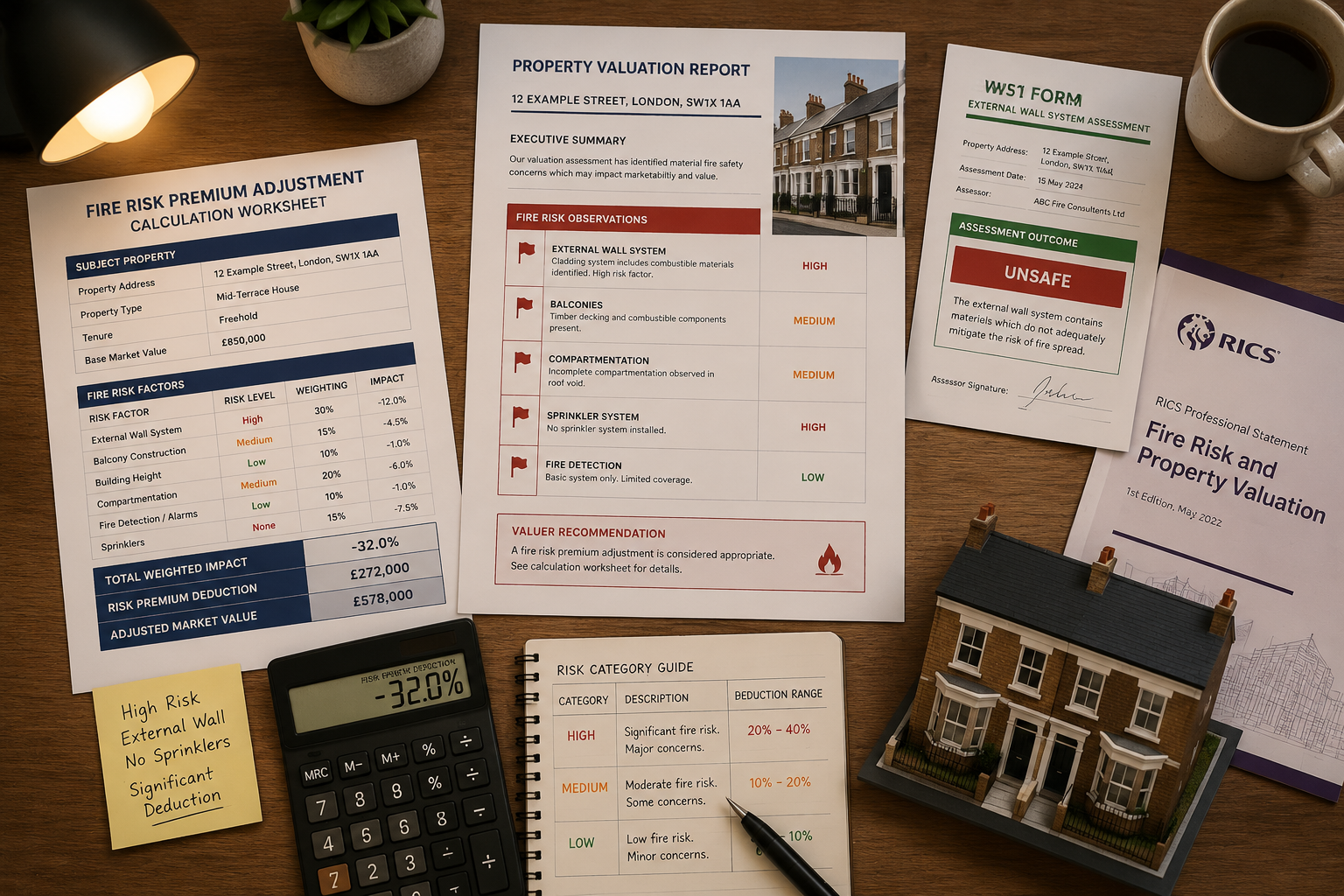

Fire hazard valuations under extended Awaab's Law — Level 3 building survey protocols for PRS compliance and risk premium adjustments in 2026 — are reshaping how RICS-registered valuers approach the private rented sector. The core question is no longer simply "what is this property worth?" but "what is this property worth given its fire compliance position?"

Risk premium adjustments are applied as percentage deductions from the Market Value or Market Rent of a property where unresolved fire hazards are identified. The emerging framework, informed by RICS guidance and lender requirements, suggests the following adjustment bands:

| Fire Hazard Category | Valuation Deduction Range | Rental Yield Impact |

|---|---|---|

| Minor (Category 2, low severity) | 0–3% | Negligible |

| Moderate (Category 1, remediation < £5,000) | 3–8% | -5 to -10% yield |

| Significant (Category 1, remediation £5k–£25k) | 8–15% | -10 to -20% yield |

| Severe (imminent risk, enforcement likely) | 15–25%+ | Property unlettable |

These deductions compound where multiple hazards coexist — a property with combustible cladding, a failed fire door, and an out-of-date EICR could face cumulative deductions exceeding 20% of market value.

How Surveyors Calculate Risk Premiums

The risk premium calculation methodology follows a three-stage process:

Stage 1 — Hazard Identification and Scoring

Using the HHSRS scoring methodology, each fire hazard is assigned a numerical score based on likelihood of harm and potential severity. Hazards scoring above 1,000 are Category 1; below 1,000 are Category 2.

Stage 2 — Remediation Cost Estimation

The surveyor estimates the full cost of bringing the property into compliance, including:

- Contractor costs for physical works

- Specialist assessments (e.g., fire engineer reports)

- Temporary decant costs where applicable

- Regulatory fees and certification costs

Stage 3 — Market Impact Assessment

The surveyor considers:

- Void risk: How long might the property be unlettable during remediation?

- Enforcement risk: What is the probability of local authority action?

- Insurance impact: Has the insurer been notified? Are premiums already elevated?

- Comparable evidence: Are similar compliant properties achieving a premium?

💬 "A fire hazard that costs £8,000 to remediate may cause a £40,000 valuation deduction once void risk, enforcement probability, and insurance loading are factored in. The remediation cost is only the starting point."

Insurance Implications for PRS Landlords

The insurance market has moved rapidly in response to Awaab's Law expansion. From 2026, many insurers are:

- Requiring EWS1 assessments for PRS properties over two storeys before quoting

- Excluding fire damage claims where known hazards were not disclosed at inception

- Loading premiums by 15–40% for properties with outstanding Category 1 fire hazards

- Voiding policies retrospectively where a landlord failed to remediate within statutory timeframes

This creates a direct link between Level 3 survey findings, Awaab's Law compliance status, and the insurability of a PRS investment. For landlords considering the value of professional survey input, the RICS reinstatement cost valuation process is increasingly intertwined with fire hazard assessment outcomes.

PRS Compliance: Practical Steps for Landlords and Investors

Building a Fire Compliance Audit Trail

Enforcement officers and courts will look for evidence that a landlord took proactive, documented steps to identify and address fire hazards. The compliance audit trail should include:

- Commissioned Level 3 survey with fire hazard section (dated and signed by RICS member)

- EWS1 assessment where external wall systems are present

- Current EICR (no older than 5 years for PRS)

- Gas Safety Certificate (annual)

- Fire risk assessment (for HMOs and buildings with common areas)

- Remediation schedule with contractor quotes and target completion dates

- Correspondence with local authority if enforcement action has been initiated

Landlords should also be aware of their obligations under dilapidations survey frameworks, particularly where fire hazard remediation works affect tenants' quiet enjoyment or require temporary relocation.

Portfolio-Level Risk Assessment for Investors

For investors holding multiple PRS properties, fire hazard valuations under extended Awaab's Law represent a portfolio-level risk event, not just a property-by-property compliance exercise. The recommended approach in 2026 is:

🔍 Step 1: Triage

Commission building surveys across the portfolio, prioritising pre-2000 stock, converted flats, and properties with known cladding or electrical concerns.

📊 Step 2: Risk Scoring

Aggregate HHSRS scores across the portfolio to identify concentration risk — where multiple properties share similar hazard profiles.

💰 Step 3: Valuation Restatement

Work with a RICS-registered valuer to restate portfolio values incorporating risk premium deductions. This is essential for accurate loan-to-value calculations and refinancing negotiations.

🔧 Step 4: Remediation Prioritisation

Sequence remediation works by hazard severity and enforcement risk, not simply by cost. A £2,000 fire door replacement that prevents enforcement action may deliver more portfolio value protection than a £15,000 cladding project on a lower-risk property.

📋 Step 5: Insurance Review

Notify insurers of survey findings and remediation plans. Proactive disclosure is significantly better than claims being declined post-incident.

Ensuring Your Surveyor Is Qualified for Fire Hazard Assessments

Not every surveyor has the competency to deliver the fire hazard assessment depth now required under extended Awaab's Law protocols. When commissioning a Level 3 survey for PRS compliance in 2026, verify that the surveyor:

- Holds RICS membership (MRICS or FRICS) — learn how to verify surveyor credentials in the UK

- Has specific experience with fire hazard assessments and HHSRS scoring

- Can demonstrate familiarity with EWS1 principles even if not a certified EWS1 assessor

- Provides reports that explicitly address Awaab's Law compliance requirements

- Carries appropriate professional indemnity insurance for fire hazard reporting

For complex or high-value PRS portfolios, a commercial building survey approach — with a multi-disciplinary team including structural engineers and fire engineers — may be appropriate. [2]

Conclusion: Acting Now Protects Both Tenants and Portfolios

The 2026 extension of Awaab's Law to fire hazards in the private rented sector is not a distant regulatory threat — it is an active compliance obligation with real financial teeth. Fire hazard valuations under extended Awaab's Law, Level 3 building survey protocols for PRS compliance, and risk premium adjustments in 2026 collectively define the new standard of care for responsible property ownership in England.

Actionable Next Steps ✅

- Commission a Level 3 building survey for every PRS property in your portfolio, with explicit fire hazard assessment scope — particularly pre-2000 stock and converted flats.

- Request a remediation cost schedule as part of the survey deliverable — this is now essential for valuation, insurance, and compliance planning.

- Engage a RICS-registered valuer to restate portfolio values with appropriate risk premium adjustments before your next refinancing or disposal.

- Review insurance policies immediately and disclose any known fire hazards to your insurer in writing.

- Build a documented compliance audit trail — enforcement officers will look for evidence of proactive action, not just completed works.

- Prioritise by hazard severity, not cost — Category 1 fire hazards with 24-hour or 7-day response requirements must be addressed first.

The landlords and investors who treat fire hazard compliance as a portfolio management opportunity — rather than a regulatory burden — will be best positioned to protect asset values, retain quality tenants, and avoid the enforcement consequences that are now firmly on the horizon.

References

[1] Awaabs Law Explained – https://firntec.com/blog/awaabs-law-explained

[2] Awaabs Law Extensions To Prs In 2026 Party Wall And Building Survey Protocols For New Hazard Categories – https://nottinghillsurveyors.com/blog/awaabs-law-extensions-to-prs-in-2026-party-wall-and-building-survey-protocols-for-new-hazard-categories

[3] Awaabs Law 2026 Social Landlords Housing Associations – https://www.villageheating.co.uk/awaabs-law-2026-social-landlords-housing-associations/

[4] Awaabs Law Technical Compliance Hvac Ventilation – https://www.arm-environments.com/resources/awaabs-law-technical-compliance-hvac-ventilation