The buy-to-let landscape has transformed dramatically. As rental markets recover in 2026, institutional investors face unprecedented scrutiny from lenders who now examine entire portfolios rather than individual properties. Surveying buy-to-let portfolios for institutional investors: 2026 risk assessments in recovering rental markets requires a forensic approach that balances regulatory compliance, yield optimization, and balance sheet resilience. With Awaab's Law reshaping landlord responsibilities and stress-testing protocols becoming more rigorous, professional landlords must adopt systematic stock condition surveys that identify yield-impacting defects before they derail portfolio growth.

The stakes have never been higher. A single underperforming property can now block financing for otherwise strong acquisitions, while aggregate leverage above 75% triggers intensive credit committee reviews.[1] This comprehensive guide details the protocols institutional investors need to navigate 2026's complex risk landscape.

Key Takeaways

- Portfolio-wide stress testing is now mandatory: Lenders assess aggregate rental income against stressed interest obligations across all properties, not individual metrics[1]

- Interest Coverage Ratios (ICR) between 125-145% are standard: Tax status and ownership structure determine minimum thresholds that must be met portfolio-wide[1]

- Awaab's Law compliance is non-negotiable: Stock condition surveys must identify hazards that could trigger regulatory breaches and tenant claims[4]

- Geographic and property-type concentration attracts scrutiny: Diversification is now a key underwriting criterion for institutional portfolios[1]

- Refinancing clustering poses hidden risks: Multiple loan maturities within 12 months can escalate credit reviews despite strong individual property performance[1]

Understanding Portfolio-Wide Risk Assessment in 2026

The Shift from Property-Level to Balance Sheet Analysis

Traditional buy-to-let underwriting focused on individual property metrics—rental yield, loan-to-value ratios, and single-asset cash flow. That era has ended. In 2026, lenders conducting surveying buy-to-let portfolios for institutional investors: 2026 risk assessments in recovering rental markets now examine entire balance sheets for portfolio landlords (defined as those with four or more mortgaged properties).[1]

This forensic approach compares aggregate rental income against aggregate stressed interest obligations portfolio-wide. The implications are profound:

- ✅ Strong properties cannot compensate for weak performers in aggregate calculations

- ✅ Overall borrowing capacity depends on portfolio-wide sustainability

- ✅ Maximum loan-to-value availability reflects total portfolio health

- ✅ Single property failures can prevent new acquisitions

For institutional investors, this means comprehensive building surveys must identify not just major defects but any factor that could reduce rental income or increase void periods across the portfolio.

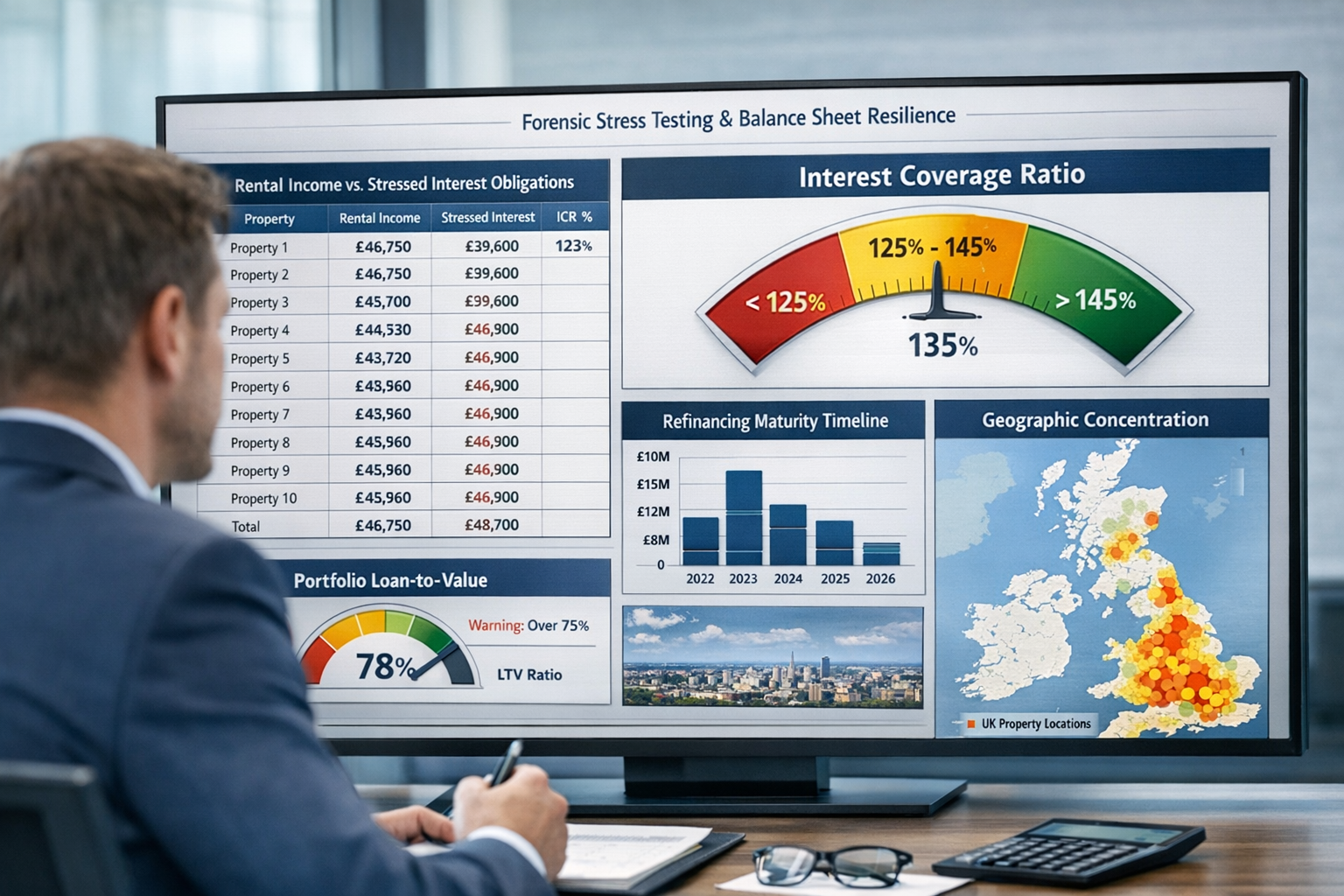

Interest Coverage Ratio Requirements Have Intensified

Interest Coverage Ratio (ICR) has become the primary affordability metric. Lenders typically require minimum thresholds between 125% and 145%, depending on borrower tax status and ownership structure.[1]

Here's how ICR works in practice:

| Monthly Rental Income | Stressed Interest Payment | ICR Calculation | Result |

|---|---|---|---|

| £1,500 | £1,100 | (1,500 ÷ 1,100) × 100 | 136% ✅ Pass |

| £1,200 | £1,000 | (1,200 ÷ 1,000) × 100 | 120% ❌ Fail |

| £1,800 | £1,200 | (1,800 ÷ 1,200) × 100 | 150% ✅ Strong Pass |

The "stressed interest payment" applies conservative affordability models shaped by 2022-2024 volatility. Despite Bank of England base rate stabilization, stress rates remain elevated relative to pre-2022 levels.[1]

"When lenders stress-test portfolios as a whole, if one weaker property fails the ICR test, it can prevent borrowing on otherwise strong new acquisitions."[2]

This reality makes stock condition surveys critical. Identifying defects that reduce rental income—damp issues, outdated heating systems, poor energy efficiency—allows investors to address problems before they compromise portfolio-wide ICR calculations.

Aggregate Leverage and Credit Committee Scrutiny

Highly leveraged portfolios, particularly those above 75% overall loan-to-value, attract deeper credit committee review even when individual properties meet ICR thresholds.[1] This represents a fundamental shift toward balance sheet resilience assessment.

Lenders now analyze:

- 📊 Total debt exposure across all mortgaged properties

- 📊 Liquidity buffers including personal income and retained profits

- 📊 Cash reserves to weather void periods or rate increases

- 📊 Refinancing clustering (multiple loans maturing within short timeframes)

In one documented case, a landlord with three loans maturing within 12 months was escalated for credit committee review despite the subject property meeting a 140% ICR at stressed rates.[1] The refinancing risk alone triggered enhanced scrutiny.

For institutional investors, this underscores the importance of RICS commercial building surveys that provide accurate valuations and condition assessments, enabling strategic refinancing schedules that avoid clustering.

Stock Condition Surveys: Protocols for Professional Landlords

Awaab's Law Compliance and Hazard Identification

The tragic death of two-year-old Awaab Ishak from prolonged exposure to mould has reshaped landlord obligations. Awaab's Law now mandates specific timeframes for investigating and remedying hazards in social housing, with private sector expectations rapidly aligning.

When conducting surveying buy-to-let portfolios for institutional investors: 2026 risk assessments in recovering rental markets, stock condition surveys must systematically identify:

- 🏠 Category 1 hazards under the Housing Health and Safety Rating System (HHSRS)

- 🏠 Damp and mould issues requiring immediate remediation

- 🏠 Ventilation deficiencies that could lead to condensation problems

- 🏠 Structural defects compromising tenant safety

- 🏠 Fire safety compliance including working smoke alarms and escape routes

Professional landlords should commission Level 2 surveys for standard properties and Level 3 building surveys for older or complex properties. These assessments provide the forensic detail needed to identify compliance risks before they escalate into regulatory breaches or tenant claims.

Yield-Impacting Defects: The Hidden Portfolio Killers

Beyond regulatory compliance, stock condition surveys must identify defects that directly impact rental yield and void periods. In 2026's recovering rental markets, tenant expectations have risen significantly. Properties now require more rigorous maintenance standards to attract and retain quality tenants.[4]

Critical yield-impacting defects include:

Energy Efficiency Issues

- Outdated boilers with high running costs

- Poor insulation reducing Energy Performance Certificate (EPC) ratings

- Single-glazed windows in an era of rising energy prices

- Lack of smart heating controls

Aesthetic and Functional Defects

- Dated kitchens and bathrooms reducing rental appeal

- Poor decoration deterring premium tenants

- Inadequate storage solutions

- Substandard flooring or carpets

Maintenance Backlogs

- Deferred repairs creating compounding problems

- Aging electrical systems requiring rewiring

- Roof repairs needed before leaks develop

- External decoration protecting structural integrity

Tenant vetting processes have become more rigorous in 2026, potentially increasing void periods and management costs.[4] Properties with visible defects or poor energy ratings face longer vacancy periods, directly reducing the rental income that determines ICR calculations.

Systematic Inspection Methodology

Professional stock condition surveys for institutional portfolios should follow a structured protocol:

Phase 1: Desktop Review

- Review existing RICS home survey reports

- Analyze historical maintenance records

- Check EPC ratings and improvement recommendations

- Verify compliance certificates (gas safety, electrical, etc.)

Phase 2: Physical Inspection

- Conduct room-by-room assessments using standardized checklists

- Use moisture meters, thermal imaging, and other diagnostic tools

- Photograph all defects with detailed annotations

- Test all systems (heating, electrical, plumbing)

Phase 3: Risk Categorization

- Category A (Urgent): Immediate safety hazards or compliance breaches

- Category B (Essential): Defects affecting rental income or causing deterioration

- Category C (Desirable): Improvements enhancing yield or reducing future costs

Phase 4: Financial Impact Analysis

- Estimate repair costs for each defect

- Calculate impact on rental income if unaddressed

- Project effect on portfolio-wide ICR calculations

- Prioritize interventions by return on investment

This systematic approach ensures institutional investors understand the true condition of their portfolios and can make informed decisions about capital allocation.

Navigating Lender Requirements and Stress Testing in 2026

The New Underwriting Landscape

Surveying buy-to-let portfolios for institutional investors: 2026 risk assessments in recovering rental markets must account for fundamentally changed lender expectations. Beyond ICR and LTV metrics, underwriters now assess:

Geographic Concentration Risk

Heavy exposure to one geographic area attracts enhanced scrutiny, especially where local rental markets are volatile. Lenders expect portfolios to demonstrate structural sustainability rather than rely solely on yield strength.[1]

For example, a portfolio concentrated in a single city facing economic challenges (factory closures, declining population) would face tougher underwriting than a geographically diversified portfolio. Stock condition surveys should note location-specific risks and recommend diversification strategies.

Property-Type Concentration

Similarly, portfolios dominated by one property type (e.g., all student housing or all HMOs) face additional scrutiny. Capitalization rates vary significantly by property type—multifamily Class A properties average 4.74%, while office properties range from 8.4% to 9.02%.[5]

Diversification across property types provides resilience against sector-specific downturns and demonstrates sophisticated portfolio management to underwriters.

Liquidity and Reserve Requirements

Lenders now review personal income, retained profits (for limited companies), and cash reserves to assess portfolio resilience.[3] This extends financial scrutiny beyond rental cash flow to overall financial capacity.

Institutional investors should maintain:

- 💰 Minimum 6 months' void coverage in accessible reserves

- 💰 Emergency repair fund equivalent to 10% of portfolio value

- 💰 Refinancing buffer for unexpected rate increases

- 💰 Documented income sources beyond rental yields

Stock condition surveys inform these reserve calculations by providing accurate repair cost projections and identifying properties likely to require capital expenditure.

Stress Rate Realities and Affordability Modeling

Despite Bank of England base rate stabilization, lenders continue applying conservative affordability models. Current mortgage rates for investment properties remain elevated at 6.6-7.5%,[5] significantly higher than pre-2022 levels.

Stress testing applies additional buffers to these rates, typically adding 1-2% to current mortgage rates when calculating affordability. This means:

- A property mortgaged at 6.8% might be stress-tested at 8.3%

- Monthly interest payments of £1,000 could become £1,200 in stress scenarios

- ICR requirements of 135% mean rental income must reach £1,620

For institutional investors using BRRRR strategies (Buy, Rehab, Rent, Refinance, Repeat), these elevated refinancing costs significantly reduce extracted equity.[5] Accurate property valuation and renovation budgeting become critical to strategy viability.

Commercial property surveyors can provide the detailed valuations and cost assessments needed to model refinancing scenarios accurately, ensuring investment strategies remain viable under 2026's stress-testing protocols.

Optimizing Portfolio Performance Through Strategic Surveying

Addressing Underperforming Assets Before They Block Growth

The harsh reality of portfolio-wide stress testing: a single underperforming property can block portfolio growth.[2] When aggregate ICR calculations fail due to one weak asset, institutional investors cannot access financing for otherwise strong new acquisitions.

This creates an imperative to identify and address underperforming assets proactively. Stock condition surveys provide the data needed to make strategic decisions:

Option 1: Strategic Disposal

Sell properties that consistently underperform and cannot be economically improved. Use proceeds to strengthen overall portfolio metrics and reduce aggregate leverage below 75% thresholds.

Option 2: Value-Add Refurbishment

Invest in improvements that increase rental income and improve ICR performance. Focus on high-ROI interventions like kitchen/bathroom upgrades, energy efficiency improvements, and aesthetic enhancements.

Option 3: Rent Optimization

Where properties are under-rented relative to market rates, implement strategic rent increases (within regulatory limits). Ensure properties justify higher rents through condition improvements identified in surveys.

Option 4: Refinancing Strategy

For properties with low LTV but poor cash flow, consider remortgaging to release equity while improving overall portfolio balance sheet metrics.

Rent review services can provide independent assessments of market rental values, supporting strategic decisions about rent optimization and property repositioning.

Building Resilience Through Preventive Maintenance

The most cost-effective portfolio strategy is preventing problems before they develop. Stock condition surveys should inform preventive maintenance schedules that:

- 🔧 Address minor defects before they become major repairs

- 🔧 Extend asset lifespans through systematic upkeep

- 🔧 Reduce void periods by maintaining rental appeal

- 🔧 Demonstrate professional management to lenders and tenants

A documented preventive maintenance program also strengthens lender confidence. Underwriters reviewing portfolio applications look favorably on systematic asset management that reduces future risk.

Leveraging Technology and Data Analytics

Modern portfolio management increasingly relies on technology platforms that track:

- Property condition scores across the portfolio

- Maintenance history and scheduled interventions

- Tenant satisfaction metrics and retention rates

- Financial performance against stress-tested projections

- Compliance status for all regulatory requirements

Integrating stock condition survey data into these platforms creates a comprehensive portfolio management system that supports both operational efficiency and lender confidence.

Regulatory Compliance and Future-Proofing Portfolios

Beyond Awaab's Law: Emerging Regulatory Trends

While Awaab's Law compliance is mandatory in 2026, institutional investors must anticipate emerging regulatory trends:

Energy Performance Standards

Minimum EPC ratings for rental properties continue rising. Properties rated below Band C may face rental restrictions or mandatory improvement requirements. Stock condition surveys should assess improvement pathways to meet future standards.

Decent Homes Standard Extension

Originally applied to social housing, decent homes standards increasingly influence private sector expectations. Surveys should assess compliance with these benchmarks even where not legally mandated.

Electrical Safety Regulations

Five-year electrical inspection certificates are now standard. Surveys should verify compliance and flag properties approaching inspection deadlines.

Fire Safety Requirements

Post-Grenfell fire safety regulations continue evolving. Multi-occupancy properties face particular scrutiny. Stock condition surveys must verify compliance with current standards and identify potential future requirements.

Documentation and Audit Trails

Professional portfolio management requires comprehensive documentation. Stock condition surveys should create audit trails that demonstrate:

- ✅ Regular systematic inspections across all properties

- ✅ Prompt response to identified hazards and defects

- ✅ Compliance with all regulatory requirements

- ✅ Tenant communication regarding repairs and improvements

- ✅ Financial planning for capital expenditure

This documentation protects institutional investors against tenant claims, regulatory enforcement, and lender scrutiny. It demonstrates the professional management standards that underwriters now expect.

The Role of Chartered Surveyors

Chartered surveyors bring professional expertise and regulatory knowledge that institutional investors require. Their involvement provides:

- Independent, objective property assessments

- RICS-compliant reporting standards

- Professional indemnity insurance coverage

- Expert witness capability if disputes arise

- Credibility with lenders and regulators

For significant portfolios, establishing ongoing relationships with chartered surveying practices ensures consistent standards and institutional knowledge about specific properties.

Practical Implementation: Building Your Survey Programme

Establishing Survey Frequency and Scope

Institutional portfolios require systematic survey programmes rather than ad-hoc inspections. Recommended frequencies:

Annual Reviews:

- Properties with known issues or recent tenant turnover

- High-value assets where condition directly impacts portfolio metrics

- Properties approaching refinancing dates

Biennial Reviews:

- Standard portfolio properties in good condition

- Properties with stable, long-term tenants

- Mid-range assets with no recent concerns

Quinquennial Reviews:

- Comprehensive Level 3 surveys for all properties

- Structural assessments and system evaluations

- Strategic planning for major capital expenditure

Trigger-Based Reviews:

- Before refinancing applications

- Following tenant departure (void inspections)

- After severe weather events

- When considering disposal or major refurbishment

Cost Management and Budgeting

Survey costs represent a small percentage of portfolio value but deliver significant risk mitigation. Typical costs:

- Level 2 Homebuyer Survey: £400-£800 per property

- Level 3 Building Survey: £600-£1,500 per property

- Specialist surveys (damp, structural, etc.): £300-£800 each

For a 20-property portfolio with biennial Level 2 surveys and quinquennial Level 3 surveys, annual survey costs might average £5,000-£8,000. This represents approximately 0.2-0.3% of a £2.5 million portfolio value—a modest investment for comprehensive risk management.

Understanding full structural survey costs helps institutional investors budget appropriately for comprehensive portfolio assessments.

Integrating Survey Findings into Portfolio Strategy

Stock condition surveys deliver maximum value when findings drive strategic decisions:

Quarterly Portfolio Reviews:

Analyze survey findings alongside financial performance data. Identify trends across the portfolio (common defect types, geographic patterns, property age correlations).

Capital Expenditure Planning:

Create multi-year capital expenditure budgets based on survey recommendations. Prioritize interventions by ICR impact and regulatory urgency.

Acquisition Criteria Refinement:

Use survey data from existing properties to refine criteria for new acquisitions. Avoid property types or locations that consistently underperform.

Lender Communication:

Share survey programmes and findings with lenders to demonstrate professional management. Proactive disclosure of issues and remediation plans builds confidence.

Tenant Relationship Management:

Use survey findings to prioritize tenant-facing improvements. Well-maintained properties reduce void periods and support rent optimization.

Conclusion

Surveying buy-to-let portfolios for institutional investors: 2026 risk assessments in recovering rental markets represents a fundamental shift from individual property focus to comprehensive balance sheet analysis. Portfolio-wide stress testing, elevated ICR requirements, and intensified regulatory scrutiny demand systematic stock condition surveys that identify both compliance risks and yield-impacting defects.

The stakes are clear: a single underperforming property can block portfolio growth, while aggregate leverage above 75% triggers intensive credit reviews. Geographic and property-type concentration attract additional scrutiny, and refinancing clustering poses hidden risks that can escalate applications to credit committees despite strong individual property performance.

Success in 2026's rental market recovery requires institutional investors to adopt forensic survey protocols that address Awaab's Law compliance, energy efficiency standards, and preventive maintenance. These surveys must integrate with broader portfolio management systems that track financial performance, regulatory compliance, and strategic positioning.

Actionable Next Steps

-

Audit Your Current Portfolio: Commission comprehensive stock condition surveys for all properties, prioritizing those approaching refinancing dates or with known performance issues.

-

Calculate Portfolio-Wide Metrics: Determine aggregate ICR, overall LTV, and refinancing clustering risks using current and stress-tested interest rates.

-

Develop Remediation Plans: Address Category A hazards immediately, create timelines for Category B defects, and budget for Category C improvements that enhance yield.

-

Establish Survey Schedules: Implement systematic annual, biennial, and quinquennial survey programmes with documented protocols and audit trails.

-

Engage Professional Support: Partner with chartered surveyors who understand institutional portfolio requirements and lender expectations.

-

Build Lender Relationships: Proactively communicate portfolio management strategies, survey findings, and remediation plans to demonstrate professional standards.

-

Monitor Regulatory Developments: Stay informed about emerging compliance requirements and adjust survey protocols to address future standards.

The recovering rental market of 2026 offers significant opportunities for institutional investors who approach portfolio management with professional rigor. Comprehensive surveying protocols provide the foundation for sustainable growth, regulatory compliance, and lender confidence in an environment where portfolio-wide resilience determines success.

References

[1] Portfolio Landlords And Stress Testing In 2026 How Underwriting Has Tightened – https://www.willowprivatefinance.co.uk/portfolio-landlords-and-stress-testing-in-2026-how-underwriting-has-tightened

[2] Buy To Let Mortgages – https://www.augustapp.com/blog/buy-to-let-mortgages

[3] Portfolio Landlords And Stress Testing In 2026 How Underwriting Has Tightening – https://www.willowprivatefinance.co.uk/portfolio-landlords-and-stress-testing-in-2026-how-underwriting-has-tightening

[4] Buy To Let Valuation Surge 2026 Survey Strategies For Institutional Investors In A Recovering Market – https://nottinghillsurveyors.com/blog/buy-to-let-valuation-surge-2026-survey-strategies-for-institutional-investors-in-a-recovering-market

[5] Building A Real Estate Investment Portfolio Your Complete Guide – https://www.amerisave.com/learn/building-a-real-estate-investment-portfolio-your-complete-guide