The RICS UK Residential Market Survey for February 2026 recorded its sharpest drop in buyer enquiries since late 2023 — a direct response to renewed inflation fears and the geopolitical shock that erupted in the final days of that month. For building surveyors completing valuations in this environment, the question is no longer whether macroeconomic conditions matter. It is how quickly and how precisely those conditions must be reflected in a professional opinion of value.

Macroeconomic uncertainty and Spring 2026 valuations: how building surveyors adjust for interest rate volatility and geopolitical risk is now one of the most pressing practical challenges in the UK property profession. Oil prices surged more than 50% from pre-conflict levels following the U.S.-Israeli military offensive launched on 28 February 2026, pushing crude above $100 per barrel for the first time in years [1]. March CPI in the U.S. jumped to an estimated 3.4% year-on-year, up sharply from 2.4% in February, driven almost entirely by energy costs [2]. Global bond markets fell 1.1% in Q1 2026 [4]. These are not abstract statistics — they feed directly into discount rates, comparable evidence reliability, and the assumptions that underpin every valuation report signed off this spring.

Key Takeaways 📌

- Oil price shock and CPI resurgence in early 2026 have materially altered the interest rate outlook, collapsing expectations of rate cuts and pushing the 10-year Treasury yield to 4.43% by late March [2].

- Building surveyors must apply explicit adjustments to yield assumptions, comparable weighting, and caveat language when macroeconomic indicators shift rapidly.

- Geopolitical risk premiums are no longer optional additions — they are a core component of credible valuation methodology in volatile markets.

- Regional divergence within the UK means a single national adjustment is insufficient; local market evidence must be weighted carefully against macro signals.

- RICS standards require surveyors to document the basis of any material uncertainty qualifications, making transparent methodology more important than ever.

The Macroeconomic Backdrop: What Happened and Why It Matters for Spring 2026 Valuations

A Geopolitical Shock That Rewrote the Rate Outlook

Before 28 February 2026, financial markets were broadly optimistic. Futures pricing implied two Federal Reserve rate cuts during the year, and UK base rate expectations tracked a similar downward path. That consensus evaporated within days.

The U.S.-Israeli military offensive triggered the effective closure of the Strait of Hormuz — the world's most critical oil chokepoint — sending shockwaves through global energy markets [1]. Crude oil broke above $100 per barrel. Gasoline in the U.S. climbed above $4 per gallon. Energy-driven inflation reversed what had been a steady disinflationary trend throughout 2025 [1].

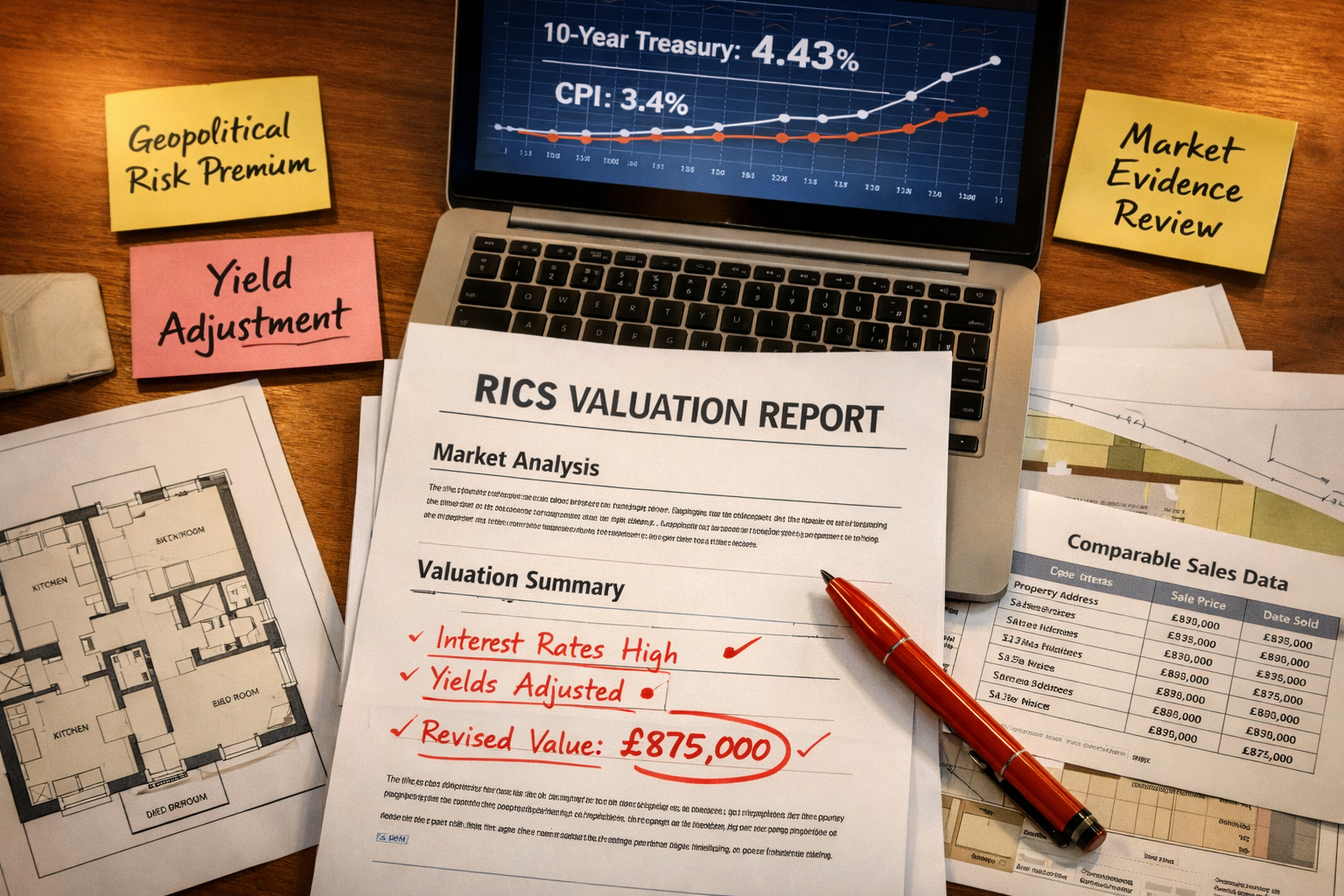

By month-end, CME FedWatch data showed meaningful probability of zero rate cuts in 2026. Seven of 19 FOMC participants indicated rates would remain unchanged through year-end [2]. The 10-year U.S. Treasury yield rose to 4.43% by 27 March 2026, up from 4.15% at February month-end, while the 2-year yield climbed 32 basis points across Q1 [2]. The S&P 500 returned -4.3% for the quarter, with growth stocks falling 9.8% [2].

💬 "Markets transitioned from a momentum-driven environment to one that is less predictable, more sensitive to geopolitical headlines, and more dependent on fundamentals like earnings quality and cash flow generation." [1]

What This Means for UK Property Markets

UK gilt yields moved in sympathy with U.S. Treasuries. Mortgage product pricing, which lenders had begun to ease through late 2025, stiffened again. The European Securities and Markets Authority's Spring 2026 Joint Committee update flagged elevated risks across real estate and financial markets, citing geopolitical instability and energy price volatility as primary drivers [3].

For building surveyors, this creates a direct methodological challenge. Valuations depend on:

- Comparable transaction evidence — which may now reflect a different rate environment than today's

- Yield assumptions — which must incorporate current market expectations, not last quarter's

- Buyer demand signals — which have weakened materially according to RICS survey data

- Caveat and qualification language — which must honestly reflect material uncertainty

Understanding what a chartered surveyor does in this environment goes well beyond physical inspection. It requires integrating macroeconomic intelligence into every professional opinion of value.

How Building Surveyors Adjust for Interest Rate Volatility and Geopolitical Risk: A Practical Framework

Step 1: Re-Dating Comparable Evidence

The most immediate practical problem in Spring 2026 is comparable evidence staleness. A transaction completed in November 2025 occurred in a world where two rate cuts were expected in 2026. That same property, if sold today, would trade in a materially different financing environment.

Surveyors should apply a structured approach to comparable weighting:

| Transaction Date | Macroeconomic Context | Weighting Adjustment |

|---|---|---|

| Pre-October 2025 | Low-rate optimism, pre-conflict | Reduce weighting significantly |

| October–January 2026 | Rate cut expectations intact | Moderate weighting |

| February–March 2026 | Conflict shock, rate repricing | High weighting (with caveats) |

| Post-March 2026 | New equilibrium forming | Primary evidence |

This is not a mechanical formula — it requires professional judgment. But surveyors who fail to acknowledge the shift in market conditions between late 2025 and Spring 2026 risk producing opinions that are already out of date on the day they are signed.

Step 2: Adjusting Yield Assumptions for Geopolitical Risk Premiums

For commercial and investment property valuations, the all-risks yield is the primary mechanism through which market sentiment is expressed. In a stable environment, yields compress when confidence is high and expand when uncertainty rises.

The BlackRock Geopolitical Risk Dashboard, updated in early 2026, shows geopolitical risk at elevated levels not seen since 2022, with Middle East conflict and energy supply disruption as the dominant drivers [5]. The World Economic Forum's Global Risks Report 2026 similarly identified geopolitical instability and energy price shocks as top-tier systemic risks [6].

Practical yield adjustment considerations for Spring 2026:

- 🔺 Add a geopolitical risk premium of 25–75 basis points above the pre-conflict benchmark yield, depending on asset class and location

- 🔺 Widen the yield range reported in the valuation to reflect genuine market uncertainty

- 🔺 For income-producing assets, stress-test the passing rent against a scenario where financing costs remain elevated for 12–24 months

- 🔺 For development appraisals, apply a higher discount rate and extend the assumed marketing period

For RICS valuations conducted in this environment, the methodology section of every report should explicitly state the basis for yield selection and reference current market evidence — not simply repeat the yield used in the previous instruction.

Step 3: Qualifying Reports with Material Uncertainty Language

RICS Valuation – Global Standards (the Red Book) provides for the use of a Material Uncertainty Clause when market conditions are such that less certainty can be attached to the opinion of value than would normally be the case. Spring 2026 meets that threshold for many asset classes.

A well-drafted material uncertainty qualification should:

- Identify the specific sources of uncertainty — in this case, interest rate volatility, energy price inflation, and geopolitical risk

- Quantify the range of values where possible, rather than stating a single figure with false precision

- Set a review date — given how rapidly conditions are changing, valuations from January 2026 may already require revisiting

- Avoid boilerplate language — generic clauses that do not reflect the specific market context undermine professional credibility

Surveyors completing RICS commercial building surveys alongside valuations should ensure that physical condition findings are also contextualised within the current market — a building requiring significant capital expenditure faces a very different financing environment today than it did six months ago.

Step 4: Applying Regional Divergence Analysis

One of the key risks in a volatile macroeconomic environment is treating the UK as a single market. In reality, Spring 2026 is producing significant regional divergence:

- Prime Central London — relatively insulated by international capital flows and cash buyers, but exposed to geopolitical risk through foreign buyer sentiment

- Commuter belt and outer London — more sensitive to mortgage rate movements; buyer affordability is directly impacted by gilt yield rises

- Northern and Midlands cities — mixed picture; some markets benefit from relative affordability, others face demand weakness from local employment sensitivity to energy costs

- Commercial property — logistics and industrial assets remain relatively resilient; retail and secondary office face compounding headwinds

Chartered surveyors in London must be especially careful not to apply a single London-wide adjustment. The gap between prime and secondary markets has widened materially in Q1 2026.

Macroeconomic Uncertainty and Spring 2026 Valuations: Sector-Specific Considerations

Residential Valuations: Mortgage Market Sensitivity

For residential surveyors, the most direct transmission mechanism from macroeconomic uncertainty to property values is through mortgage affordability. With rate cut expectations collapsed and lenders repricing products upward, the pool of qualifying buyers at any given price point has shrunk.

Key adjustments for residential valuations in Spring 2026:

- Recalibrate price per square foot benchmarks using only post-February 2026 agreed sales where available

- Apply greater scrutiny to asking price evidence — the gap between asking and achieved prices is widening in rate-sensitive markets

- Factor in extended marketing periods when assessing whether a property is genuinely marketable at the stated value

For buyers considering whether a survey is worth commissioning in this environment, the answer is unambiguous: hiring a residential surveyor could save thousands on a property purchase, particularly when market conditions mean that structural defects or overpricing risks are harder to detect without professional guidance.

A Level 3 building survey is particularly valuable in volatile markets — it provides the most comprehensive assessment of physical condition, which directly informs negotiating position when comparable evidence is thin or unreliable.

Commercial Valuations: Yield Compression Reversal

The commercial property sector entered 2026 with cautious optimism following a period of yield expansion in 2023–2024. That recovery narrative has been disrupted. Invesco's April 2026 tactical asset allocation commentary noted that real assets face renewed pressure from the combination of higher-for-longer rates and geopolitical risk premiums [7].

For commercial surveyors, the practical implications include:

- Office valuations — already under pressure from occupancy uncertainty; geopolitical risk adds a further layer of investor caution

- Retail — consumer spending sensitivity to energy costs compounds existing structural challenges

- Industrial and logistics — most resilient sector, but supply chain disruption from Middle East conflict may affect tenant covenant strength in import-dependent businesses

- Development sites — residual land values are highly sensitive to finance costs; a 50bps rise in the discount rate can reduce a residual value by 15–25% depending on scheme structure

New Build and Development Appraisals

Development appraisals are among the most sensitive valuation exercises in a volatile rate environment. The combination of rising build costs (energy-linked materials), higher finance costs, and weakened end-value evidence creates a compressing margin that requires explicit acknowledgment.

Surveyors advising on new build properties should ensure that clients understand the distinction between a developer's projected GDV (gross development value) — which may be based on pre-shock assumptions — and a current market opinion of value.

Best Practice Checklist for Surveyors Navigating Spring 2026 Conditions ✅

The following checklist consolidates the key methodological steps for surveyors working through macroeconomic uncertainty and Spring 2026 valuations:

- Re-date all comparable evidence — apply reduced weighting to pre-February 2026 transactions

- Document yield selection methodology explicitly, referencing current market evidence

- Apply a geopolitical risk premium where appropriate, with written justification

- Consider Material Uncertainty Clause for all valuations where market evidence is thin or rapidly changing

- Conduct regional divergence analysis — do not apply national averages to local markets

- Stress-test income assumptions against a higher-for-longer rate scenario

- Set a short review date on valuation reports — conditions may change materially within 60–90 days

- Communicate proactively with clients about the limitations of current market evidence

Conclusion: Actionable Next Steps for Building Surveyors in 2026

The convergence of geopolitical shock, energy price inflation, and collapsed rate cut expectations has created the most complex valuation environment since 2022. Macroeconomic uncertainty and Spring 2026 valuations: how building surveyors adjust for interest rate volatility and geopolitical risk is not a theoretical question — it demands practical, documented, and defensible methodological responses.

The surveyors who will serve their clients best in this environment are those who:

- Act quickly to update comparable evidence databases and yield benchmarks with post-February 2026 data

- Write clearly — qualification language must be specific, not generic

- Think regionally — national averages mask the divergence that matters most to individual clients

- Communicate proactively — clients making major financial decisions in this environment need to understand the limitations of any valuation, not just receive a number

For property buyers, sellers, and investors navigating Spring 2026, the value of a qualified, RICS-regulated surveyor has never been higher. Whether the need is for a comprehensive structural survey, a RICS valuation, or specialist commercial advice, working with professionals who understand how macroeconomic forces translate into property-level risk is the most important step any party can take right now.

The market will stabilise. But the surveyors who document their methodology rigorously during the instability will be the ones whose opinions of value stand up to scrutiny when it does.

References

[1] Q1 2026 Market Recap – https://trajanwealth.com/blog/q1-2026-market-recap/

[2] April 2026 Economic And Market Update Geopolitics At The Forefront – https://www.crestwoodadvisors.com/april-2026-economic-and-market-update-geopolitics-at-the-forefront/

[3] Jc 2026 06 Jc Update On Risks And Vulnerabilities Spring 2026 – https://www.esma.europa.eu/sites/default/files/2026-03/JC_2026_06_-_JC_Update_on_Risks_and_Vulnerabilities_Spring_2026.pdf

[4] Q2 2026 Quarterly Market Outlook Global – https://www.eastspring.com/docs/librariesprovider6/our-perspectives/market-outlook/2026/q2-2026-quarterly-market-outlook_global.pdf

[5] Geopolitical Risk Dashboard – https://www.blackrock.com/corporate/insights/blackrock-investment-institute/interactive-charts/geopolitical-risk-dashboard

[6] Wef Global Risks Report 2026 – https://reports.weforum.org/docs/WEF_Global_Risks_Report_2026.pdf

[7] Tactical Asset Allocation April 2026 For Financial Professionals – https://www.invesco.com/content/dam/invesco/us/en/documents/insights/tactical-asset-allocation-april-2026-for-financial-professionals.pdf