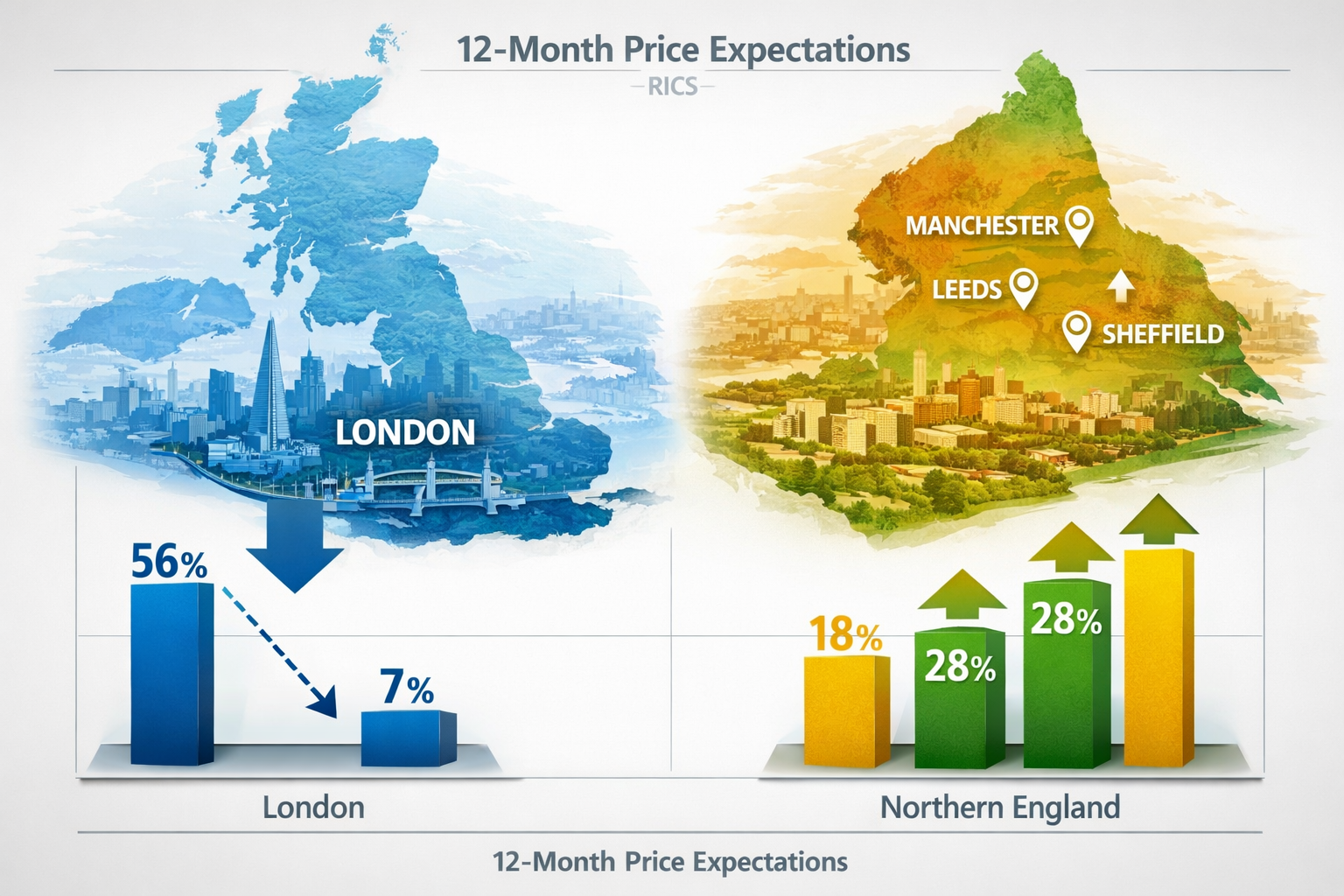

RICS data from February 2026 tells a striking story: London's 12-month house price expectations collapsed from +56% to just +7% — while Northern cities continue to post robust momentum figures. For building surveyors, buyers, and investors navigating the UK property market this spring, that gap is not just a headline. It is a strategic signal that demands a fundamentally different approach depending on which side of the divide a client stands on.

This article unpacks the Regional Price Divergence in Spring 2026: Building Survey Strategies for London Market Weakness vs Northern Recovery Opportunities — examining what the data means, how surveyors should adapt their methodologies, and what actionable steps buyers and investors can take right now.

Key Takeaways 📌

- London's price expectations have plummeted from +56% to +7% in 12 months, signalling a cooling market with elevated risk of overvaluation.

- Northern markets (Manchester, Leeds, Sheffield, Newcastle) are showing stronger price momentum and improved buyer confidence in Spring 2026.

- Building survey strategies must be regionally calibrated — the risks, defects, and valuation considerations differ significantly between London stock and Northern housing.

- Level 3 Building Surveys are increasingly essential in both markets, but for different reasons: London for legacy structural issues; Northern for older, rapidly transacting stock.

- Buyers and investors who skip surveys in fast-moving Northern markets risk costly surprises — speed should never replace due diligence.

Understanding the Regional Price Divergence in Spring 2026

The Data Behind the Divide

The numbers are hard to ignore. According to RICS sentiment surveys, London's net balance of surveyors expecting price rises over the next 12 months dropped dramatically — from a buoyant +56% to a fragile +7% [1]. That is not a gentle correction. That is a structural shift in market confidence.

Meanwhile, cities like Manchester, Leeds, Sheffield, and Newcastle have maintained positive price momentum through early 2026. Factors driving this include:

- Lower average house prices relative to earnings, making affordability comparatively stronger

- Infrastructure investment — HS2 legacy projects, Northern Powerhouse Rail planning, and regeneration zones

- Remote and hybrid working continuing to push demand away from London commuter zones

- Younger buyer demographics relocating northward in search of value

The broader macroeconomic backdrop matters too. Global disruption and divergence across markets in early 2026 have created an environment where domestic UK property is subject to sharper regional variation than at any point in the past decade [1]. The Office for Budget Responsibility's March 2026 Economic and Fiscal Outlook noted that household disposable income pressures remain uneven across UK regions, with London households facing higher mortgage-to-income ratios that are suppressing transaction volumes [2].

💬 "The UK housing market in Spring 2026 is not one market — it is at least two, and possibly four or five, depending on the metric you examine."

What "London Market Weakness" Actually Means

It is important to be precise here. London is not crashing — but it is underperforming relative to its own recent history and relative to Northern England. Key indicators of London weakness include:

| Indicator | London (Spring 2026) | Northern England (Spring 2026) |

|---|---|---|

| 12-month price expectation (RICS net balance) | +7% | +35% to +42% |

| Average days on market | Increasing | Stable or decreasing |

| Buyer enquiries | Declining | Rising |

| New instructions | Rising (supply pressure) | Moderate |

| Agreed sales per surveyor | Falling | Holding steady |

This combination of rising supply, falling demand, and compressed price expectations creates a buyer's market in London — but one with significant structural complexity beneath the surface.

Building Survey Strategies for the London Market Weakness

Why London Properties Demand More Rigorous Surveys Right Now

In a cooling market, defects that sellers might have obscured in a hot market become more visible — and more negotiable. This is precisely the moment when a thorough RICS Level 3 Building Survey becomes a buyer's most powerful tool.

London's housing stock presents a unique set of structural challenges:

- Victorian and Edwardian terraces with aging timber floors, original lead pipework, and single-skin rear extensions

- Converted flats in Georgian townhouses with complex shared structural elements and party wall considerations

- Post-war concrete construction with potential carbonation issues

- Basement conversions — increasingly common in prime London boroughs — with heightened damp and drainage risks

For buyers in areas like Chelsea, Hammersmith, Camden, or Battersea, the combination of high purchase prices and aging stock makes professional survey oversight non-negotiable. A comprehensive building survey in these areas can identify defects that, in a negotiation-friendly market, could reduce the purchase price by tens of thousands of pounds.

Choosing the Right Survey Level in London

Not every London property needs the same survey. Here is a practical framework:

Level 2 (HomeBuyer Report) — Suitable for:

- Modern flats built post-2000 in good condition

- Leasehold apartments in managed blocks with recent EWS1 certificates

- Properties where a mortgage valuation has already flagged no major concerns

Level 3 (Full Building Survey) — Essential for:

- Any property built before 1930

- Properties with visible signs of movement, damp, or structural alteration

- Basement conversions or significant extensions

- Any property over £750,000 where the financial stakes justify full scrutiny

For a detailed breakdown of survey types and their applications, the Level 2 vs Level 3 survey comparison guide offers clear, practical guidance.

Party Wall Considerations in London's Cooling Market

One area that often catches London buyers off guard is party wall complexity. In terraced and semi-detached London properties, any structural work — including the basement conversions and loft extensions that are common in the capital — triggers obligations under the Party Wall etc. Act 1996.

In a buyer's market, sellers are more likely to have undertaken recent works without proper notices. A building surveyor should always check for evidence of recent structural alterations and advise buyers accordingly. Understanding party wall surveyor roles and responsibilities is therefore directly relevant to any London property purchase in 2026.

Northern Recovery Opportunities: Survey Strategies for a Rising Market

The Northern Opportunity — and Its Hidden Risks

The Regional Price Divergence in Spring 2026: Building Survey Strategies for London Market Weakness vs Northern Recovery Opportunities is perhaps most urgently relevant in Northern England, where rising buyer confidence can create dangerous complacency around due diligence.

When markets move quickly, buyers feel pressure to act fast. Surveys get skipped. Offers go in without proper structural intelligence. This is a well-documented pattern — and it consistently leads to costly post-completion surprises.

Northern England's housing stock carries its own set of structural characteristics that demand careful survey attention:

- Back-to-back terraces and through terraces in cities like Leeds and Bradford — often with inadequate damp-proof courses and aging drainage

- Stone-built properties in Yorkshire and Lancashire — beautiful but prone to pointing failure and penetrating damp

- Former mining subsidence areas across County Durham, Nottinghamshire, and South Yorkshire — requiring specialist ground movement assessments

- Pre-1919 stock comprising a higher proportion of total housing than in many Southern regions

⚠️ Key risk: In rising markets, sellers have less incentive to reduce prices based on survey findings. This makes it even more critical to commission a survey before finalising an offer, not after.

Calibrating Survey Depth for Northern Properties

The complete guide to building surveyors makes clear that survey scope should always match property age, type, and condition — not market speed.

For Northern recovery markets, the recommended approach in Spring 2026 is:

- Always commission at minimum a Level 2 survey — even for properties that appear in good condition

- Upgrade to Level 3 for any pre-1945 property — which covers the majority of desirable Northern stock

- Request specialist damp and drainage reports where back-to-back or terrace configurations are involved

- Check for mining legacy — the Coal Authority's interactive map should be consulted before any purchase in former coalfield areas

- Review EPC ratings carefully — many Northern properties have low energy ratings that will require significant investment under future regulations

For buyers unsure whether to invest in a full survey, is a Level 3 survey worth it? provides a clear cost-benefit analysis that almost always points toward yes for older stock.

Regional Survey Intelligence: What Surveyors Need to Know

For chartered surveyors operating across both markets, Spring 2026 demands a genuinely bifurcated intelligence framework. The same survey checklist cannot serve a London Georgian conversion and a Yorkshire stone terrace equally well.

Key regional intelligence points for surveyors in 2026:

| Factor | London Focus | Northern Focus |

|---|---|---|

| Primary structural risk | Movement, subsidence, basement damp | Penetrating damp, pointing failure, subsidence (mining) |

| Most common defect type | Flat roof failures, party wall damage | Chimney stack deterioration, slate roof wear |

| Valuation pressure | Downward (use defects as negotiation leverage) | Upward (identify defects early to protect buyer) |

| Client priority | Price renegotiation intelligence | Risk identification before commitment |

| Typical survey type needed | Level 3 for most pre-war stock | Level 3 for pre-1945; Level 2 for post-war semis |

Strategic Recommendations for Buyers, Investors, and Surveyors in 2026

For Buyers in London

- Use the cooling market to your advantage — commission a thorough Level 3 building survey and use findings to negotiate price reductions

- Don't skip surveys on leasehold properties — service charge arrears, cladding issues, and structural defects in blocks remain a significant risk

- Check party wall history — ask sellers to provide party wall awards or notices from any recent works

- Factor in energy efficiency costs — London's older stock often requires significant EPC improvement investment

For Buyers and Investors in Northern Markets

- Act fast but survey first — in rising markets, speed is important but never more important than structural intelligence

- Prioritise mining subsidence checks in County Durham, South Yorkshire, and Nottinghamshire

- Budget for damp remediation — penetrating damp in stone-built properties is common and often more expensive to fix than it appears

- Consider commercial opportunities — Northern city centres offer strong commercial property fundamentals; a commercial building survey is essential before any investment commitment

For Chartered Surveyors

- Develop regional market intelligence briefs for clients — the divergence between London and Northern markets is now significant enough to warrant market-specific client communications

- Adjust comparable evidence frameworks — London comparables from 2024-2025 may overstate current values; Northern comparables may understate trajectory

- Invest in specialist training for mining subsidence assessment if operating in Northern markets

- Communicate survey findings in market context — a cracked lintel in a falling London market has different negotiation implications than the same defect in a rising Northern market

Conclusion: Navigating the Divide with Confidence

The Regional Price Divergence in Spring 2026: Building Survey Strategies for London Market Weakness vs Northern Recovery Opportunities is not a temporary blip. The structural factors driving this divide — affordability, infrastructure investment, demographic shifts, and macroeconomic pressure on London households [2] — suggest that regional variation will remain a defining feature of the UK property market for the foreseeable future [1].

For buyers, the message is clear: never let market conditions — whether falling or rising — become a reason to skip professional survey advice. The risks are simply too high, and the cost of a thorough building survey is trivial compared to the cost of an undiscovered defect.

For surveyors, this moment demands regional sophistication. Generic survey approaches will not serve clients well in a market this divided. The professionals who will thrive in 2026 are those who combine technical excellence with genuine regional market intelligence.

Actionable next steps:

- ✅ Commission a Level 3 Building Survey for any pre-war property, regardless of region

- ✅ Use the house survey checklist to prepare for your survey appointment

- ✅ Speak to a chartered surveyor who understands your specific regional market

- ✅ In London, use survey findings as a negotiation tool in a buyer's market

- ✅ In Northern markets, prioritise early survey commissioning before making a final offer

The divide is real. The opportunity is real. The risk of navigating it without professional guidance is also very real.

References

[1] Disruption And Divergence Markets In Early 2026 – https://www.im.natixis.com/en-latam/insights/macro-views/2026/disruption-and-divergence-markets-in-early-2026

[2] Economic And Fiscal Outlook March 2026 – https://obr.uk/efo/economic-and-fiscal-outlook-march-2026/