The UK buy-to-let sector is experiencing a remarkable transformation in 2026, with property values climbing and institutional investors returning to the market with renewed confidence. As Buy-to-Let Valuation Surge 2026: Survey Strategies for Institutional Investors in a Recovering Market becomes the defining theme of this year's rental property landscape, professional landlords and institutional players must adopt sophisticated valuation methodologies to capitalize on regional growth opportunities while navigating significant regulatory changes.

With forecasts predicting a 22.2% average property value increase over the next five years and rental income expected to climb by 12% through 2030, the buy-to-let market presents compelling opportunities for investors who understand how to properly value assets in this recovering environment[1]. However, success requires more than optimism—it demands rigorous survey strategies, compliance-focused due diligence, and data-driven decision-making aligned with RICS standards.

Key Takeaways

- Regional markets are outperforming London, with Yorkshire, the North West, and Scotland projected to see gains of up to 28.8% over five years, requiring location-specific valuation approaches

- RICS-compliant valuation methods incorporating yield adjustments, comparable evidence, and regulatory compliance checks are essential for institutional investors in 2026

- Regulatory changes including Section 21 abolition (effective May 1, 2026) fundamentally impact property valuations and require updated risk assessment frameworks

- Rental growth of 12% nationally through 2030 creates opportunities for yield optimization, but regional variations demand granular market analysis

- Professional survey strategies must integrate new depreciation rules, energy efficiency requirements, and tenant protection legislation into valuation models

Understanding the Buy-to-Let Valuation Surge in 2026 📈

The current buy-to-let valuation surge represents a significant shift from the challenging conditions landlords faced in recent years. Multiple factors are converging to drive property values upward across the UK, creating a recovery that institutional investors are positioning to exploit.

Market Fundamentals Driving Growth

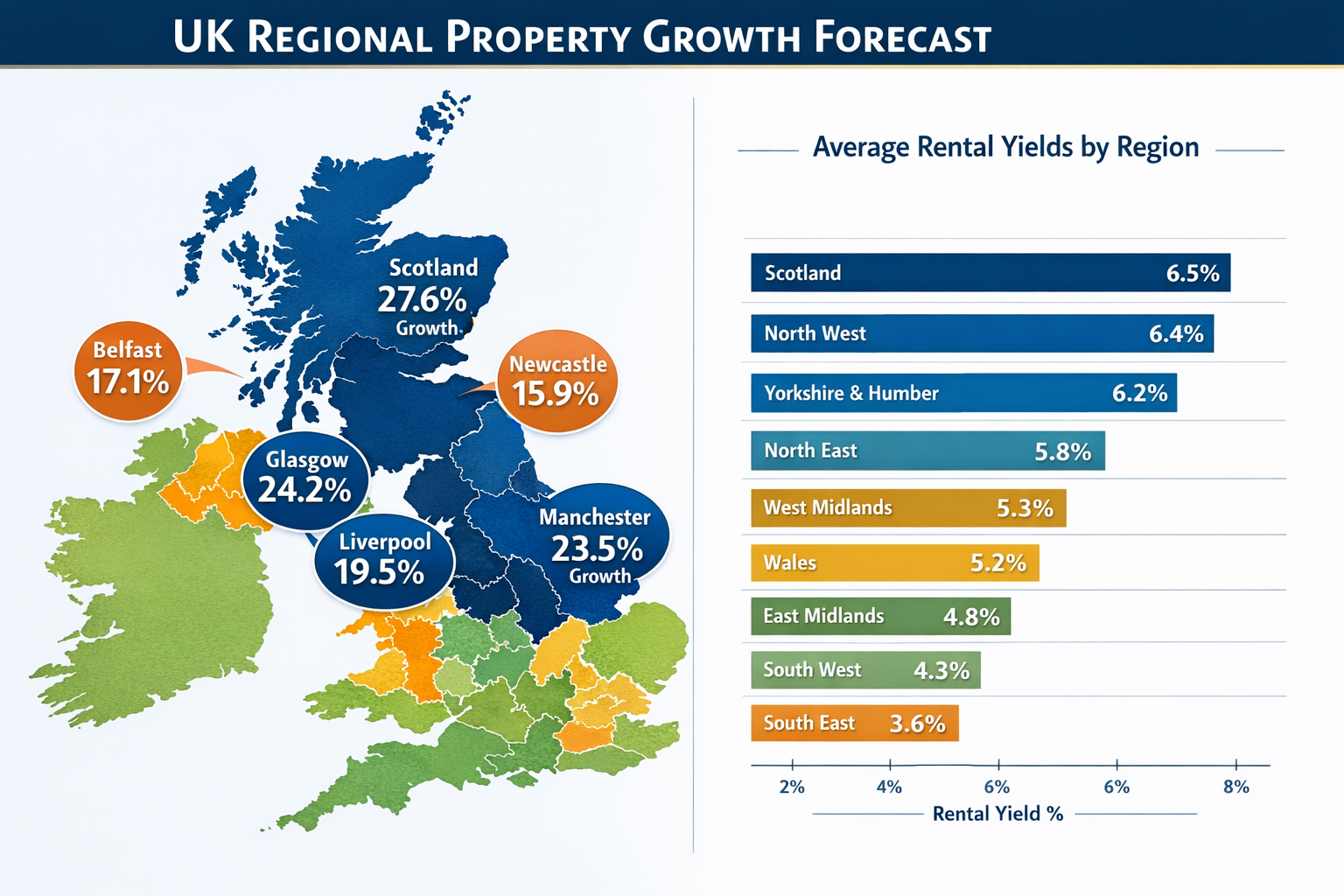

The foundation of the Buy-to-Let Valuation Surge 2026: Survey Strategies for Institutional Investors in a Recovering Market rests on several key economic indicators. Regional markets are leading the charge, with Yorkshire and The Humber and the North West anticipated to see +28.8% gains, while Scotland, Wales, and the North East follow closely at +27.6% over the five-year period[1].

Current performance data from Zoopla's latest index reveals the top five growth cities: Belfast (+7.8%), Liverpool (+3.3%), Glasgow (+2.6%), Newcastle (+2.4%), and Manchester (+2.4%)[1]. These figures demonstrate that value appreciation is concentrated outside traditional London-centric investment patterns, requiring institutional investors to recalibrate their geographic strategies.

Rental income projections add another dimension to valuation considerations. UK rents are expected to climb by 12% over the five-year period (2026–2030), with London's rental values projected to rise by 11.5%[1]. This balanced growth across the country means that yield calculations must account for regional rental inflation variations, which currently range from 3.3% in Scotland to 6.4% in Northern Ireland.

Lending Environment and Transaction Volume

The financial infrastructure supporting buy-to-let investment has stabilized considerably. Forecasts predict £11 billion in new buy-to-let purchase lending for 2026 alongside 1,202,000 property transactions[2]. This represents lender confidence in the sector's fundamentals, though it's important to note that lending conditions remain more stringent than pre-2016 levels.

Within the broader context of £300 billion gross mortgage lending expected across all sectors in 2026[2], buy-to-let represents a significant but selective segment. Institutional investors must understand that lenders are applying sophisticated stress testing and affordability calculations that directly impact property valuations and investment viability.

For professional landlords conducting comprehensive property surveys, these market fundamentals provide the backdrop against which individual property valuations must be assessed.

RICS-Compliant Valuation Methodologies for Institutional Investors

Institutional investors require valuation approaches that meet professional standards while accounting for the unique characteristics of the 2026 buy-to-let market. The Buy-to-Let Valuation Surge 2026: Survey Strategies for Institutional Investors in a Recovering Market demands adherence to RICS Red Book standards while incorporating market-specific adjustments.

The Investment Method: Yield-Based Valuation

The investment method remains the primary approach for buy-to-let property valuation, calculating market value based on rental income potential and appropriate yield rates. The formula is straightforward but requires sophisticated market knowledge:

Market Value = Net Annual Rental Income ÷ All Risks Yield (ARY)

However, determining the appropriate yield requires analysis of:

- Comparable evidence from recent sales of similar investment properties

- Location-specific yield compression or expansion trends

- Property condition and specification affecting tenant demand

- Lease terms and tenant quality influencing income security

- Regulatory compliance status impacting future costs

In 2026, institutional investors must adjust yields to reflect the new regulatory environment. Properties with strong energy efficiency ratings, modern specifications, and full compliance with evolving tenant protection legislation command lower yields (higher values) due to reduced risk profiles.

Comparable Evidence Analysis

The comparative method provides essential market validation for investment valuations. Professional surveyors analyze recent transactions of similar properties, adjusting for differences in:

| Adjustment Factor | Impact on Valuation | 2026 Considerations |

|---|---|---|

| Location | ±10-30% | Regional growth differentials significant |

| Property Size | ±5-15% per bedroom | HMO potential affects value |

| Condition | ±10-25% | Energy efficiency increasingly critical |

| Tenure | ±5-20% | Leasehold ground rent reforms impact |

| Rental Status | ±5-15% | Tenanted vs. vacant possession |

For institutional portfolios, chartered surveyors with regional expertise can provide granular comparable evidence that accounts for micro-market variations within broader growth regions.

Residual Valuation for Value-Add Opportunities

Many institutional investors pursue value-add strategies involving property improvement or conversion. The residual method calculates current value by working backward from projected end value:

Current Value = (End Value – Development Costs – Profit Margin) – Finance Costs

In the context of buy-to-let investments, this might involve:

- Converting single dwellings to Houses in Multiple Occupation (HMOs)

- Upgrading energy efficiency to achieve higher EPC ratings

- Refurbishing to command premium rents

- Reconfiguring layouts to optimize bedroom count

The residual method requires detailed cost estimation and realistic end value projections based on comparable evidence. Professional building surveys are essential to identify structural issues that could inflate development costs and undermine value-add assumptions.

Red Book Valuation Standards

All institutional valuations should comply with RICS Valuation – Global Standards (the Red Book). This ensures:

- Independence and objectivity in valuation conclusions

- Transparency in methodology and assumptions

- Competence through qualified RICS valuers

- Appropriate basis of value (typically Market Value)

- Clear reporting with assumptions and limitations stated

For investors requiring formal valuations for lending, financial reporting, or portfolio management purposes, engaging RICS-accredited surveyors for Red Book valuations provides the professional assurance that institutional stakeholders require.

Regional Market Analysis and Growth Projections

The Buy-to-Let Valuation Surge 2026: Survey Strategies for Institutional Investors in a Recovering Market is fundamentally a story of regional divergence. Institutional investors must adopt location-specific strategies that recognize the varying growth trajectories across the UK.

High-Growth Northern Regions

The North of England and Scotland represent the strongest growth prospects for the five-year period through 2030. Yorkshire and The Humber, along with the North West, are forecast to achieve 28.8% capital appreciation[1], driven by:

- Affordability relative to southern markets attracting first-time buyers and renters

- Economic regeneration in major cities like Manchester, Liverpool, and Leeds

- Infrastructure investment improving connectivity and employment prospects

- University populations creating consistent rental demand

- Lower entry prices enabling higher percentage returns

Scotland follows closely with 27.6% projected growth[1], supported by distinct market dynamics including different regulatory frameworks and strong rental demand in Edinburgh and Glasgow. Current rental inflation in Scotland stands at 3.3% year-on-year, with average rents of £1,012[2], suggesting room for rental growth as the market recovers.

Emerging City Hotspots

Specific cities are demonstrating exceptional current performance that validates their long-term growth potential:

Belfast leads with +7.8% annual growth[1], benefiting from limited supply, strong employment growth, and relative affordability. Liverpool (+3.3%) and Glasgow (+2.6%) follow, with Newcastle (+2.4%) and Manchester (+2.4%) rounding out the top five[1].

These cities share common characteristics:

- ✅ Strong rental yields (typically 5-7% gross)

- ✅ Diverse employment bases reducing economic vulnerability

- ✅ Established student populations providing rental demand stability

- ✅ Regeneration initiatives improving long-term prospects

- ✅ Transport connectivity to other major employment centers

Institutional investors developing portfolios in these locations should engage local chartered surveyors who understand neighborhood-level variations in tenant demand, rental values, and capital growth potential.

Regional Rental Dynamics

Rental growth projections vary significantly by region, requiring location-specific yield calculations. As of November 2025, rent inflation by nation shows:

- England: 4.4% year-on-year (average rent £1,422)

- Wales: 6.1% year-on-year (average rent £820)

- Northern Ireland: 6.4% year-on-year (average rent £871)

- Scotland: 3.3% year-on-year (average rent £1,012)[2]

These variations reflect different supply-demand dynamics and regulatory environments. Wales and Northern Ireland are experiencing the strongest rental inflation, suggesting potential for yield expansion, while England's higher absolute rental values provide greater nominal income despite slower percentage growth.

London Market Considerations

While regional markets lead growth projections, London remains significant for institutional investors due to market depth, liquidity, and international demand. London rental values are projected to rise by 11.5% over five years[1], slightly below the national average but from a higher base.

London's buy-to-let market presents distinct characteristics:

- Higher entry costs requiring larger capital deployment

- Lower gross yields (typically 3-5%) but stronger capital appreciation historically

- Greater regulatory scrutiny including selective licensing schemes

- Diverse micro-markets with significant value variations between boroughs

- International tenant demand providing resilience during domestic downturns

Investors targeting London should consider specialized local surveyors who understand the nuances of different boroughs and property types.

Regulatory Compliance and Risk Assessment in 2026

The regulatory landscape for buy-to-let property has transformed dramatically, with 2026 marking the implementation of several significant changes. The Buy-to-Let Valuation Surge 2026: Survey Strategies for Institutional Investors in a Recovering Market must be understood within this new compliance framework, as regulatory factors directly impact property valuations and investment returns.

Section 21 Abolition and Tenancy Changes

The most significant regulatory shift is the ending of Section 21 (no-fault evictions) on May 1, 2026 in England[2]. This fundamentally alters the landlord-tenant relationship by:

- Shifting most tenancies to periodic assured terms with no fixed end date

- Requiring specific grounds for possession rather than arbitrary eviction rights

- Extending notice periods and strengthening tenant security

- Increasing importance of tenant selection and property management

For valuation purposes, this change impacts:

Risk Assessment: Properties require more rigorous tenant vetting processes, potentially increasing void periods and management costs. Valuations should reflect higher operational expenses and reduced flexibility.

Exit Strategy Considerations: Institutional investors planning portfolio disposals must account for the complexity of achieving vacant possession, which may affect timing and achievable values.

Income Security: While tenant security improves rental income stability, it also increases the cost and difficulty of addressing problematic tenancies, requiring conservative void period assumptions in cash flow projections.

Rent Increase Restrictions

New regulations impose rent increase limits that directly affect yield calculations:

- Landlords can only raise rents once per year

- Minimum two months' notice required for rent increases

- Tenants can challenge above-market rises at tribunal[2]

These restrictions mean that institutional investors cannot assume automatic rental growth in line with market inflation. Valuation models must incorporate:

- Conservative rental growth assumptions (potentially below market inflation)

- Risk of tribunal challenges if market rents rise rapidly

- Strategic timing of rent reviews to maximize returns within constraints

Rental Bidding Restrictions

The implementation of rental bidding restrictions changes how properties are marketed:

- Landlords and agents must publish an asking rent

- Cannot invite or accept offers above the published rent[2]

This impacts valuation by:

- Eliminating the potential for rental "overbids" in high-demand areas

- Requiring more accurate initial rent pricing based on comparable evidence

- Potentially reducing peak rental values in competitive markets

Energy Efficiency Requirements

While not new in 2026, Minimum Energy Efficiency Standards (MEES) continue to evolve, with future tightening anticipated. Currently, properties must achieve at least an EPC rating of E to be legally let, but proposals for raising this to C or B by 2030 are under consideration.

Valuation implications include:

- Capital expenditure requirements for properties below minimum standards

- Obsolescence risk for poorly performing properties

- Premium values for properties with strong energy efficiency

- Rental demand concentration in higher-rated properties

Professional structural surveys should assess improvement costs and feasibility for properties requiring energy efficiency upgrades.

New Depreciation Rules for Private Landlords

For landlords operating through limited company structures, new depreciation rules allow:

- 80% of property value (excluding land) to be depreciated over 20 years

- New-build rates at approximately 3.5% annually[3]

This creates tax advantages for corporate ownership structures and affects after-tax return calculations. Institutional investors should incorporate these benefits into financial modeling, recognizing that:

- Depreciation provides non-cash tax deductions improving cash flow

- Older properties may have higher depreciation rates due to shorter remaining useful lives

- Land value apportionment requires professional valuation to support tax positions

Survey Strategies and Due Diligence for Institutional Portfolios

Institutional investors require comprehensive due diligence processes that go beyond individual property assessment to evaluate portfolio-level risks and opportunities. Effective Buy-to-Let Valuation Surge 2026: Survey Strategies for Institutional Investors in a Recovering Market approaches integrate multiple survey types and analytical frameworks.

Multi-Tier Survey Approach

Professional institutional investors typically employ a tiered survey strategy:

Tier 1: Desktop Analysis and Initial Screening

- Comparable evidence review

- Planning history checks

- Flood risk and environmental assessments

- Title and tenure verification

- EPC rating evaluation

Tier 2: RICS Level 2 Survey (HomeBuyer Report)

For standard properties in reasonable condition, a Level 2 survey provides:

- Visual inspection of accessible areas

- Identification of urgent defects

- Advice on necessary repairs

- Market valuation (if required)

Tier 3: RICS Level 3 Building Survey

For older properties, unusual construction, or those in poor condition, a comprehensive Level 3 building survey delivers:

- Detailed inspection of structure and fabric

- Analysis of defects and their causes

- Comprehensive repair cost estimates

- Long-term maintenance planning

Specialist Survey Requirements

Certain property types and conditions require specialist surveys beyond standard RICS levels:

Damp and Moisture Surveys

Essential for properties showing signs of water ingress, damp surveys use moisture meters and thermal imaging to identify:

- Rising damp from failed damp-proof courses

- Penetrating damp from roof or wall defects

- Condensation issues affecting habitability

Structural Engineer Reports

For properties with significant structural concerns, structural engineer reports provide:

- Professional assessment of structural integrity

- Design solutions for remedial works

- Cost estimates for structural repairs

- Building control compliance advice

Reinstatement Cost Assessments

For insurance purposes, reinstatement cost valuations ensure adequate building insurance coverage, particularly important for institutional portfolios with lender requirements.

Portfolio-Level Risk Assessment

Institutional investors must aggregate individual property surveys into portfolio-level risk frameworks that evaluate:

| Risk Category | Assessment Criteria | Mitigation Strategies |

|---|---|---|

| Regulatory Compliance | EPC ratings, licensing, safety certificates | Upgrade programs, compliance audits |

| Physical Condition | Structural integrity, maintenance backlog | Capital expenditure planning, preventive maintenance |

| Market Positioning | Rental demand, competitive positioning | Refurbishment, repositioning strategies |

| Tenant Risk | Arrears history, turnover rates | Enhanced vetting, property management |

| Geographic Concentration | Regional exposure, local market cycles | Diversification, market monitoring |

Technology-Enhanced Survey Methods

Modern institutional investors increasingly employ technology-enhanced survey approaches:

Drone Surveys

Drone surveys provide:

- Safe inspection of roofs and high-level features

- Photographic evidence of condition

- Thermal imaging for heat loss identification

- Cost-effective assessment of large portfolios

Digital Documentation

Professional surveyors now deliver:

- Interactive digital reports with embedded photographs

- Video walkthroughs of properties

- Cloud-based documentation for portfolio management

- Integration with property management software

Valuation Factor Integration

Comprehensive survey strategies must integrate findings into valuation adjustments that reflect:

Positive Factors (increasing value):

- ✅ Recent refurbishment to high standards

- ✅ Strong EPC ratings (A-C)

- ✅ Modern specifications meeting tenant expectations

- ✅ Excellent state of repair

- ✅ Desirable locations with strong rental demand

Negative Factors (decreasing value):

- ❌ Significant structural defects requiring remediation

- ❌ Poor energy efficiency (EPC D-G)

- ❌ Deferred maintenance backlog

- ❌ Non-compliant features (safety, licensing)

- ❌ Obsolete specifications reducing tenant appeal

Professional surveyors incorporate these factors into valuation factor analysis that provides transparent adjustment rationale supporting final value conclusions.

Financial Modeling and Yield Optimization

Beyond physical property assessment, institutional investors require sophisticated financial modeling that translates survey findings and market analysis into actionable investment decisions. The Buy-to-Let Valuation Surge 2026: Survey Strategies for Institutional Investors in a Recovering Market demands rigorous financial frameworks.

Gross vs. Net Yield Calculations

Understanding the distinction between gross and net yields is fundamental:

Gross Yield = (Annual Rental Income ÷ Property Value) × 100

This simple calculation provides initial screening but ignores operating costs. For example, a property purchased for £200,000 generating £12,000 annual rent delivers a 6% gross yield.

Net Yield = ((Annual Rental Income – Operating Costs) ÷ Property Value) × 100

Operating costs typically include:

- Property management fees (10-15% of rent)

- Maintenance and repairs (10-15% of rent)

- Insurance (£200-500 annually)

- Safety certificates and compliance (£200-400 annually)

- Void periods (typically 4-8 weeks annually)

- Letting fees (when re-letting)

The same £200,000 property might have operating costs of £3,600 (30% of rent), reducing net yield to 4.2%. This 1.8% difference significantly impacts investment returns and valuation conclusions.

Cash-on-Cash Return Analysis

For leveraged acquisitions, cash-on-cash return measures actual return on invested equity:

Cash-on-Cash Return = (Annual Net Cash Flow ÷ Total Cash Invested) × 100

This accounts for:

- Mortgage interest payments (not principal repayment)

- Actual rental income after voids and costs

- Initial cash investment (deposit, fees, refurbishment)

A property purchased for £200,000 with a 75% LTV mortgage (£150,000 loan at 5% interest) requires £50,000 equity plus approximately £5,000 in acquisition costs. If net rental income is £8,400 and mortgage interest is £7,500, annual net cash flow is £900, delivering a 1.6% cash-on-cash return.

This illustrates why capital appreciation is crucial in 2026's market—rental income alone may not deliver compelling returns on equity, but combined with projected 22.2% value growth over five years, total returns become attractive.

Total Return Projection

Institutional investors evaluate total return combining rental income and capital appreciation:

Total Return = Rental Yield + Capital Growth Rate

Using 2026 market projections:

- Net rental yield: 4.2%

- Annual capital growth (22.2% over 5 years): 4.4% annually

- Total return: 8.6% annually

This framework enables comparison with alternative investment classes and assessment of risk-adjusted returns.

Sensitivity Analysis

Professional financial modeling incorporates sensitivity analysis testing how returns vary with changing assumptions:

| Variable | Base Case | Optimistic | Pessimistic | Impact on Return |

|---|---|---|---|---|

| Rental Growth | 2.4% p.a. | 3.5% p.a. | 1.0% p.a. | ±1.5% total return |

| Capital Growth | 4.4% p.a. | 5.7% p.a. | 2.0% p.a. | ±2.4% total return |

| Void Periods | 6 weeks | 4 weeks | 10 weeks | ±0.8% total return |

| Maintenance Costs | 12% of rent | 8% of rent | 18% of rent | ±0.5% total return |

| Interest Rates | 5.0% | 4.0% | 6.5% | ±1.2% total return |

This analysis reveals that capital growth assumptions have the greatest impact on total returns, emphasizing the importance of accurate regional growth projections and location selection.

Practical Implementation for Institutional Investors

Translating survey strategies and valuation methodologies into operational investment processes requires structured implementation frameworks. Institutional investors pursuing the Buy-to-Let Valuation Surge 2026: Survey Strategies for Institutional Investors in a Recovering Market should adopt systematic approaches.

Acquisition Process Framework

A robust acquisition process typically follows these stages:

Stage 1: Market Selection (Weeks 1-2)

- Analyze regional growth projections and rental dynamics

- Identify target cities and neighborhoods

- Establish yield and return criteria

- Define property type preferences

Stage 2: Property Sourcing (Weeks 3-6)

- Engage local property agents and networks

- Review available opportunities against criteria

- Conduct desktop analysis and initial screening

- Shortlist properties for detailed assessment

Stage 3: Due Diligence (Weeks 7-10)

- Commission appropriate survey level based on property characteristics

- Review legal title and planning history

- Analyze rental comparables and yield projections

- Assess regulatory compliance status

- Estimate refurbishment costs if required

Stage 4: Valuation and Offer (Weeks 11-12)

- Integrate survey findings into valuation model

- Adjust for identified defects and opportunities

- Calculate maximum acquisition price based on return targets

- Submit offer and negotiate terms

Stage 5: Completion (Weeks 13-16)

- Finalize mortgage arrangements

- Complete legal conveyancing

- Arrange insurance and safety certificates

- Implement any immediate refurbishment

- Market property and secure tenants

Building a Regional Portfolio

Institutional investors should consider geographic diversification while maintaining operational efficiency:

Concentration Strategy: Focus on 2-3 high-growth regions to build scale and local expertise, enabling:

- Relationships with preferred surveyors and contractors

- In-depth market knowledge

- Efficient property management

- Economies of scale in maintenance

Diversification Strategy: Spread investments across 5-6 regions to reduce exposure to local market cycles, accepting:

- Higher management complexity

- Need for multiple service provider relationships

- Greater research requirements

- Reduced operational efficiency

Most institutional investors adopt a hybrid approach, concentrating 60-70% of portfolio value in 2-3 core regions while maintaining 30-40% in secondary markets for diversification.

Engaging Professional Surveyors

Selecting appropriate surveying professionals is critical. Institutional investors should:

Verify RICS Membership: Ensure surveyors hold appropriate RICS qualifications (MRICS or FRICS) and maintain professional indemnity insurance.

Assess Local Expertise: Prioritize surveyors with demonstrated experience in target regions and property types, such as chartered surveyors in specific locations.

Establish Panel Arrangements: For portfolio acquisitions, negotiate panel agreements providing:

- Consistent valuation standards

- Preferential pricing for volume

- Rapid turnaround times

- Standardized reporting formats

Request Sample Reports: Review previous survey reports to assess thoroughness, clarity, and alignment with institutional requirements.

Ongoing Portfolio Management

Post-acquisition, institutional investors require continuous monitoring and periodic revaluation:

Annual Portfolio Valuation: Commission desktop valuations annually to track performance against projections and identify underperforming assets.

Condition Surveys: Conduct periodic condition assessments (every 3-5 years) to identify maintenance requirements and prevent deterioration.

Regulatory Compliance Audits: Review portfolio compliance with evolving regulations, particularly energy efficiency standards and licensing requirements.

Market Repositioning: Identify opportunities to enhance value through refurbishment, reconfiguration, or change of use based on market evolution.

Conclusion

The Buy-to-Let Valuation Surge 2026: Survey Strategies for Institutional Investors in a Recovering Market represents a compelling opportunity for professional landlords and institutional investors who approach the market with rigorous methodology and comprehensive due diligence. With property values forecast to increase by 22.2% over five years and rental income projected to grow by 12% through 2030, the fundamentals support strategic investment in carefully selected regional markets.

However, success in this environment requires more than optimism about growth projections. Institutional investors must implement sophisticated valuation approaches that integrate RICS-compliant methodologies, comprehensive survey strategies, and detailed financial modeling. The regulatory landscape has transformed significantly, with Section 21 abolition, rent increase restrictions, and evolving energy efficiency requirements fundamentally changing risk profiles and operational considerations.

Key success factors for institutional investors in 2026 include:

🎯 Geographic Focus: Concentrate on high-growth northern regions and emerging city hotspots delivering superior returns compared to traditional London-centric strategies

🎯 Rigorous Due Diligence: Employ appropriate survey levels based on property characteristics, from Level 2 HomeBuyer Reports for standard properties to comprehensive Level 3 Building Surveys for complex assets

🎯 Regulatory Compliance: Integrate compliance requirements into valuation models, recognizing that regulatory-compliant properties command premium values and lower risk profiles

🎯 Professional Standards: Engage RICS-qualified surveyors with local expertise to provide Red Book valuations that meet institutional requirements and support lending arrangements

🎯 Financial Discipline: Focus on total return combining rental yield and capital appreciation, using sensitivity analysis to understand downside risks

Actionable Next Steps

For institutional investors seeking to capitalize on the buy-to-let valuation surge in 2026:

-

Conduct Regional Analysis: Review the growth projections for Yorkshire, the North West, Scotland, and Wales to identify specific cities and neighborhoods aligned with investment criteria

-

Establish Survey Protocols: Define appropriate survey levels for different property types and conditions, creating standardized due diligence processes that balance thoroughness with efficiency

-

Build Professional Networks: Identify and engage qualified chartered surveyors in target regions, establishing panel arrangements for portfolio acquisitions

-

Update Financial Models: Incorporate 2026 regulatory changes, depreciation benefits, and regional growth projections into investment return calculations

-

Develop Compliance Framework: Create systematic approaches to regulatory compliance covering energy efficiency, safety requirements, licensing, and tenant protection legislation

-

Commission Portfolio Reviews: For existing portfolios, engage professional surveyors to conduct comprehensive valuations that reflect current market conditions and identify optimization opportunities

The buy-to-let market in 2026 rewards investors who combine market knowledge with professional survey strategies and rigorous valuation methodologies. By adopting the approaches outlined in this guide, institutional investors can position themselves to capture value in a recovering market while managing the risks inherent in an evolving regulatory environment.

For professional survey services supporting institutional buy-to-let investment strategies, contact experienced chartered surveyors who understand the unique requirements of the 2026 market and can provide RICS-compliant valuations that support informed investment decisions.

References

[1] Why Buy To Let Is Still Worth It In 2026 – https://www.propertynotify.co.uk/investment/why-buy-to-let-is-still-worth-it-in-2026/

[2] Is Buy To Let Worth It 2026 In Uk – https://www.revolutionbrokers.co.uk/blog/is-buy-to-let-worth-it-2026-in-uk

[3] Guide To The New Private Landlord Status In 2026 For Buy To Let Investment – https://www.optimhome.com/en/blog/guide-to-the-new-private-landlord-status-in-2026-for-buy-to-let-investment