The RICS February 2026 survey reveals a striking market reversal: landlord instructions have plummeted to -27% while tenant demand remains remarkably stable, creating the most acute rental supply constraints in recent memory. This dramatic shift from the oversupply conditions of late 2025—when national vacancy rates peaked at 7.3%—signals a fundamental recalibration in how surveyors must approach rental property valuations. With rental growth projections of +20% expected in Q2 2026, the Private Rented Sector (PRS) faces a valuation sensitivity challenge unlike any seen in the past decade.

Understanding Rental Supply Shortage and Valuation Sensitivity: Assessing PRS Property Values Amid Tenant Demand Surge in 2026 has become essential for investors, landlords, and property professionals navigating this volatile transition. The confluence of collapsed construction activity, regulatory pressures reducing landlord participation, and sustained tenant demand creates a complex valuation environment where traditional metrics require substantial recalibration.

Key Takeaways

✅ Supply Constraint Reversal: Landlord instructions dropped to -27% in February 2026, reversing 2025's oversupply conditions and creating acute rental shortages despite previous high vacancy rates.

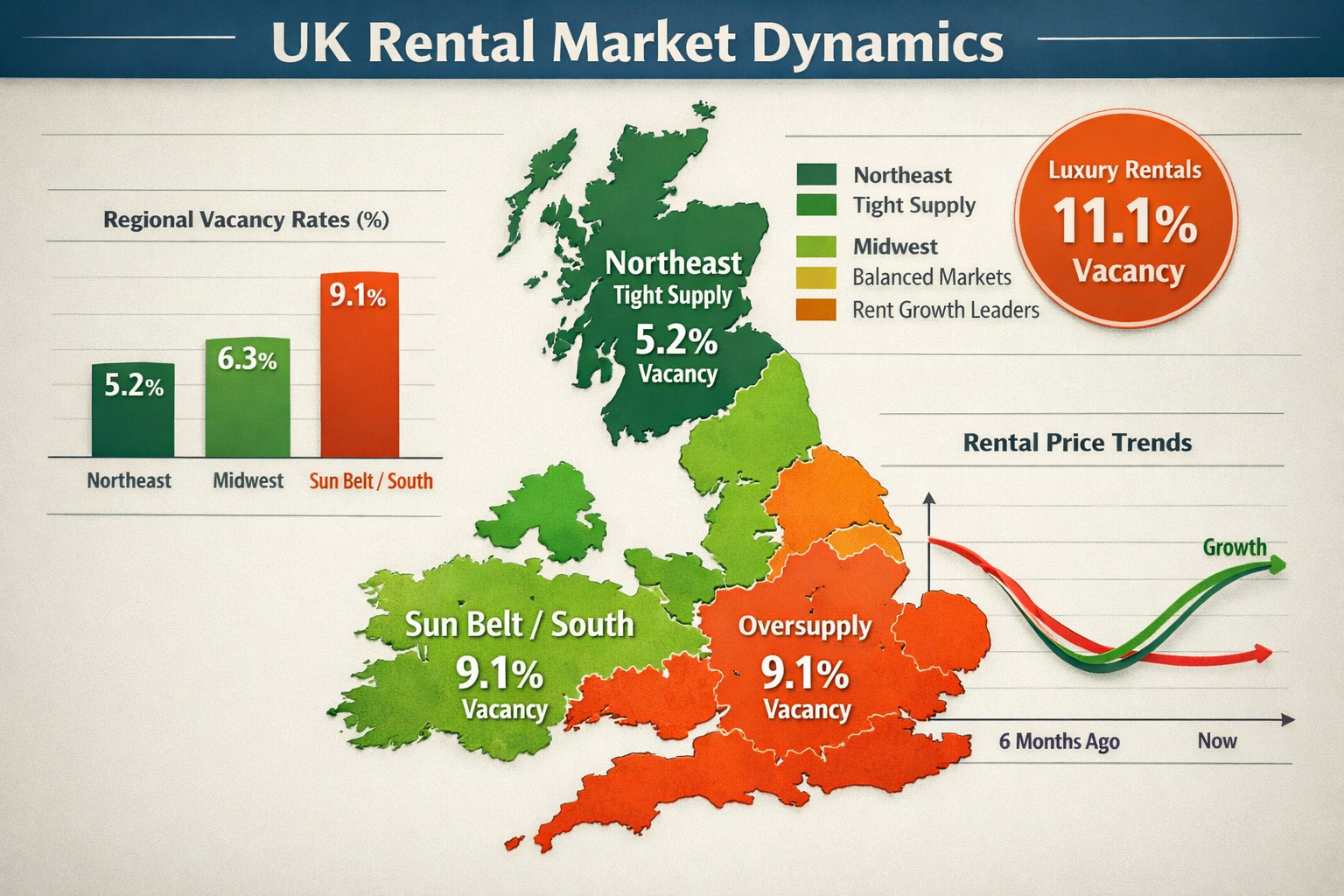

✅ Regional Valuation Divergence: Supply-constrained Northeast markets (5.2% vacancy) command premium valuations compared to oversupplied Sun Belt regions (9.1% vacancy), requiring location-specific assessment approaches.

✅ Rent Growth Acceleration: After six consecutive months of decline through January 2026, rental markets are projected to achieve +20% growth in Q2 2026 due to supply constraints.

✅ Luxury Segment Vulnerability: High-end properties face continued valuation pressure with vacancy rates reaching 11.1%, creating segmentation challenges in portfolio assessments.

✅ Investment Calculus Transformation: The shift from oversupply to shortage fundamentally alters PRS investment returns, requiring surveyors to adjust yield assumptions and risk premiums in valuation models.

Understanding the 2026 Rental Market Transition

From Oversupply to Acute Shortage

The rental market's transformation from late 2025 to early 2026 represents one of the most dramatic supply-demand shifts in recent property market history. National rental vacancy rates reached 7.3% in January 2026, the highest level in several years, driven by substantial new supply coming online while renter demand temporarily weakened [2]. The Census Bureau reported vacancy rates of 7.1% in Q3 2025, indicating the oversupply trend had been building throughout the year.

However, the RICS February 2026 survey data reveals this oversupply narrative has reversed with remarkable speed. Landlord instructions collapsing to -27% indicates a severe withdrawal of rental supply from the market, while tenant demand metrics remain stable or improving. This creates the conditions for the projected +20% rent growth in Q2 2026—a swing from six consecutive months of rent declines that saw the national median rent dip to $1,353 in January 2026 [2].

Several factors drive this supply constraint:

🏠 Regulatory Pressures: Increased compliance requirements and taxation changes have prompted landlords to exit the market

📉 Construction Collapse: Multifamily starts dropped more than 40% between 2023 and 2025, with minimal recovery expected due to high material costs and elevated interest rates [1]

💰 Financing Constraints: Higher borrowing costs make new PRS investment less attractive, reducing portfolio expansion

⚖️ Landlord Sentiment: Negative sentiment from the 2025 oversupply period creates hesitation to re-enter the market

For property surveyors conducting RICS registered valuations, this transition requires fundamental reassessment of comparable evidence, yield assumptions, and market sentiment factors that inform rental property valuations.

Regional Variation in Supply Dynamics

The rental supply shortage narrative in 2026 varies dramatically by region, creating significant valuation sensitivity challenges for surveyors assessing PRS portfolios. The Northeast maintains the tightest supply constraints with only 5.2% rental vacancy compared to the South's 9.1% vacancy rate [1]. This regional divergence creates substantially different valuation contexts.

Supply-Constrained Markets:

- Northeast Region: Chronic housing shortages and limited new construction create sustained pricing power

- New York City: Asking rents rose 4.8% from January through October 2025, defying national trends due to sky-high home prices and persistent rental housing shortage [3]

- Midwest Markets: Positioned as regional rent growth leaders for 2026 as these markets remain the most balanced [1]

Oversupplied Markets:

- Sun Belt Cities: Orlando, Austin, Miami, Nashville, and Phoenix face 4-5% increases in apartment stock in 2026-2027, requiring extended periods to return to supply-demand balance [1]

- Luxury Segment: High-end properties experiencing the most severe oversupply, with some luxury buildings reporting vacancy rates as high as 11.1% compared to national averages [2]

This regional variation means surveyors must apply location-specific adjustments when assessing Rental Supply Shortage and Valuation Sensitivity: Assessing PRS Property Values Amid Tenant Demand Surge in 2026. A standardized valuation approach fails to capture the material differences between constrained and oversupplied markets.

When conducting commercial property surveys, professionals must integrate regional supply pipeline data, demographic trends, and local regulatory environments into their valuation frameworks.

Valuation Methodology Adjustments for Supply-Constrained Markets

Recalibrating Comparable Evidence

Traditional comparable evidence analysis faces significant challenges in the 2026 rental market transition. Transactions and rental agreements from late 2025—when vacancy rates peaked at 7.3%—no longer provide reliable indicators for current valuations as supply constraints tighten. Surveyors must implement temporal adjustments to comparable evidence that reflect the rapid market shift.

Key Adjustments for Comparable Analysis:

📊 Time-Based Adjustments: Apply monthly adjustment factors to comparables from Q4 2025 and Q1 2026 to reflect accelerating rent growth trajectory

🎯 Supply Constraint Premium: Add location-specific premiums for properties in markets with sub-6% vacancy rates and declining landlord instructions

🏢 Segment-Specific Analysis: Separate luxury segment comparables (11.1% vacancy) from mid-market properties experiencing tighter supply conditions

📍 Micro-Location Weighting: Increase weighting for comparables in immediate vicinity as neighborhood-level supply variations become more pronounced

The challenge becomes particularly acute when assessing properties that last transacted during the oversupply period. A rental property valued in October 2025 using comparables from that period would significantly understate current market value if supply constraints have tightened substantially in the intervening months.

For surveyors conducting rent reviews, the comparable evidence recalibration directly impacts rental value assessments and arbitration outcomes. Landlords and tenants may have sharply divergent views on appropriate adjustments, requiring clear documentation of the methodology and market evidence supporting temporal adjustments.

Yield Compression and Investment Return Assumptions

The transition from oversupply to shortage fundamentally alters PRS investment returns and required yield assumptions in valuation models. When rental markets experience supply constraints and accelerating rent growth, investors accept lower initial yields in anticipation of capital appreciation and rental growth potential.

Yield Adjustment Framework:

| Market Condition | Typical Yield Range | 2026 Adjustment |

|---|---|---|

| Oversupplied Markets (>8% vacancy) | 5.5% – 6.5% | +50-75 basis points |

| Balanced Markets (5-7% vacancy) | 4.5% – 5.5% | Baseline |

| Constrained Markets (<5% vacancy) | 3.5% – 4.5% | -50-100 basis points |

| Prime Urban Locations | 3.0% – 4.0% | -75-125 basis points |

These yield adjustments reflect investor sentiment and market pricing observed in early 2026 as the supply shortage becomes apparent. Properties in constrained markets command premium valuations due to:

✨ Rental Growth Potential: Projected +20% Q2 2026 rent growth creates significant upside for income returns

🛡️ Downside Protection: Limited new supply pipeline reduces risk of future oversupply and rental decline

💼 Portfolio Diversification: Supply-constrained assets provide hedge against broader market volatility

🎯 Tenant Retention: Limited alternatives increase tenant retention rates and reduce void periods

When conducting RICS commercial building surveys, surveyors must document the yield assumptions applied and provide sensitivity analysis showing valuation impact of alternative yield scenarios. This transparency becomes essential when valuations inform lending decisions, portfolio acquisitions, or financial reporting requirements.

Incorporating Demand Sustainability Analysis

Assessing Rental Supply Shortage and Valuation Sensitivity: Assessing PRS Property Values Amid Tenant Demand Surge in 2026 requires rigorous analysis of demand sustainability. While supply constraints create immediate pricing power, valuations must consider whether tenant demand can support projected rent growth or if affordability constraints will limit rental increases.

Demand Sustainability Indicators:

📈 Employment Growth: Local job market strength and wage growth trends that support rent affordability

👥 Household Formation: Demographic trends indicating sustained renter household creation

🏠 Homeownership Barriers: Mortgage rate levels and home price-to-income ratios that keep potential buyers in rental market

💰 Affordability Metrics: Rent-to-income ratios and their trajectory relative to historical norms

The broader housing supply gap widened to 4.03 million homes in 2025, indicating new construction fell short of household formations despite multifamily oversupply in select metros [4]. This structural shortage supports long-term rental demand, though regional variations remain significant.

However, the deepening affordability crisis presents valuation risks. The number of homes renting for less than $600 declined by 2.5 million between 2014 and 2024—a 30% drop [5]. This indicates oversupply is concentrated in higher-priced units while affordable housing becomes scarcer, creating segmentation in demand sustainability.

For mid-market and affordable PRS properties, demand sustainability appears robust due to limited alternatives. For luxury segment properties already experiencing 11.1% vacancy rates, demand sustainability remains questionable even as overall market supply tightens.

Regional Market Analysis and Valuation Implications

Northeast and Midwest: Supply Constraint Leaders

The Northeast and Midwest regions present the strongest cases for positive valuation adjustments in 2026 due to sustained supply constraints and balanced market fundamentals. The Northeast's 5.2% rental vacancy rate [1] remains well below the national average, creating persistent pricing power for landlords and premium valuations for investors.

Northeast Market Characteristics:

🏙️ Chronic Undersupply: Limited developable land and restrictive zoning create structural supply constraints

📊 Stable Fundamentals: Diversified employment base and established renter demographics support demand

💼 Institutional Interest: Supply-constrained markets attract institutional capital seeking stable returns

🔒 Regulatory Stability: Mature regulatory environments create predictable operating conditions

New York City exemplifies the Northeast dynamic, with asking rents rising 4.8% from January through October 2025 despite national rent declines [3]. This pricing power reflects sky-high home prices that keep potential buyers in the rental market and persistent rental housing shortage that limits tenant alternatives.

The Midwest is positioned as the regional rent growth leader for 2026 as markets remain the most balanced [1]. Unlike Sun Belt markets facing extended absorption of oversupply, Midwest cities maintained disciplined construction activity that avoided the 2024-2025 oversupply conditions.

Valuation Implications for Northeast/Midwest Properties:

- Apply negative yield adjustments of 50-100 basis points reflecting supply constraint premium

- Incorporate rental growth assumptions of 3-5% annually for 2026-2028 period

- Reduce void period assumptions due to limited tenant alternatives

- Apply premium multiples to net operating income reflecting market positioning

For surveyors conducting comprehensive condition surveys in these regions, the physical condition and capital expenditure requirements take on heightened importance as supply constraints make quality properties increasingly valuable.

Sun Belt Markets: Extended Absorption Period

Sun Belt markets face fundamentally different valuation considerations due to substantial oversupply that will require extended absorption periods. Orlando, Austin, Miami, Nashville, and Phoenix will see 4-5% increases in apartment stock in 2026-2027 [1], creating continued downward pressure on rents and valuations despite the national supply shortage narrative.

Sun Belt Oversupply Dynamics:

📦 Pipeline Overhang: Substantial construction started in 2023-2024 continues to deliver in 2026-2027

📉 Vacancy Pressure: The South's 9.1% vacancy rate [1] indicates significant excess supply

⏳ Extended Timeline: 18-24 month absorption periods required to return to market equilibrium

🎯 Segment Concentration: Oversupply concentrated in luxury and Class A properties

The challenge for surveyors assessing PRS properties in Sun Belt markets involves distinguishing between temporary oversupply conditions and fundamental market weakness. Markets with strong employment growth and household formation may absorb excess supply relatively quickly, while markets facing demographic headwinds may experience prolonged weakness.

Valuation Approach for Oversupplied Sun Belt Markets:

- Conservative Rent Growth: Apply 0-2% annual rent growth assumptions for 2026-2027, with acceleration in 2028+

- Yield Premiums: Add 50-75 basis points to required yields reflecting absorption risk

- Extended Stabilization: Model 12-18 month lease-up periods for new acquisitions

- Segment Differentiation: Apply more conservative assumptions to luxury segment properties

Despite near-term challenges, Sun Belt markets retain long-term fundamentals including population growth, business-friendly environments, and relative affordability compared to coastal markets. Valuations should reflect both near-term absorption challenges and longer-term positioning.

When conducting dilapidations surveys in oversupplied markets, property condition becomes particularly important as landlords compete for tenants through property quality and amenities.

Luxury Segment: Persistent Valuation Challenges

The luxury rental segment faces unique valuation challenges in 2026 despite broader market supply constraints. High-end properties report vacancy rates as high as 11.1% compared to national averages [2], indicating oversupply concentrated in the premium segment even as mid-market properties experience tightening conditions.

Luxury Segment Dynamics:

💎 Demand Ceiling: Limited pool of tenants able to afford luxury rents creates natural demand constraint

🏗️ Supply Concentration: Development activity from 2022-2024 concentrated in luxury segment due to higher margins

📊 Affordability Sensitivity: Luxury tenants have greater flexibility to delay moves or purchase homes when conditions favor homeownership

🔄 Substitution Risk: High-end rentals compete with luxury home purchases, creating cross-market sensitivity

The number of homes renting for less than $600 declined by 2.5 million between 2014 and 2024 [5], while luxury supply expanded substantially. This inverse relationship—affordable housing shortage alongside luxury oversupply—creates segmentation that surveyors must carefully navigate.

Luxury Property Valuation Adjustments:

- Apply higher void assumptions (8-12% vs. 4-6% for mid-market)

- Incorporate concession costs (1-2 months free rent) in net operating income calculations

- Use higher capitalization rates (50-100 basis points above mid-market)

- Model conservative rent growth (0-2% annually) until oversupply absorbs

For investors considering luxury PRS acquisitions, the valuation sensitivity to market timing becomes acute. Properties acquired during peak oversupply conditions may offer significant value, while properties valued at 2023-2024 pricing levels may face write-downs as the oversupply persists.

Investment Calculus and Portfolio Strategy Implications

The Shifting PRS Investment Thesis

The transition from oversupply to shortage fundamentally transforms the PRS investment thesis and required returns. Investors who positioned portfolios based on 2025's oversupply conditions face material valuation adjustments, while those recognizing the emerging supply constraint early gain significant competitive advantage.

2025 Investment Environment:

- National vacancy rates: 7.3% [2]

- Rent trajectory: Six consecutive months of decline to $1,353 median [2]

- New supply: Substantial deliveries creating downward pricing pressure

- Investor sentiment: Cautious due to oversupply concerns

- Valuation approach: Conservative yields, limited growth assumptions

2026 Investment Environment:

- Landlord instructions: -27% indicating supply withdrawal

- Rent trajectory: Projected +20% growth in Q2 2026

- New supply: 40% decline in multifamily starts [1] limiting future competition

- Investor sentiment: Increasingly positive as supply constraints become apparent

- Valuation approach: Compressed yields, aggressive growth assumptions

This dramatic shift creates both opportunities and risks. Investors who acquire properties during the late 2025 oversupply period at distressed pricing may realize substantial valuation gains as supply constraints tighten. Conversely, investors who delay acquisition until mid-2026 may face significantly higher entry pricing that reduces long-term returns.

For surveyors conducting RICS help to buy valuations or investment portfolio assessments, documenting the market timing and comparable evidence becomes essential to justify valuation conclusions.

Portfolio Segmentation and Risk Management

Assessing Rental Supply Shortage and Valuation Sensitivity: Assessing PRS Property Values Amid Tenant Demand Surge in 2026 requires sophisticated portfolio segmentation that recognizes divergent market conditions across property types, locations, and tenant segments.

Portfolio Segmentation Framework:

| Segment | Valuation Trend | Risk Level | Strategy |

|---|---|---|---|

| Northeast Mid-Market | ⬆️ Strong Appreciation | Low | Hold/Acquire |

| Midwest Workforce Housing | ⬆️ Moderate Appreciation | Low-Medium | Acquire |

| Sun Belt Class A | ➡️ Flat/Declining | Medium-High | Selective/Avoid |

| Luxury Urban | ⬇️ Declining | High | Avoid/Divest |

| Affordable Housing | ⬆️⬆️ Strong Appreciation | Low | Acquire Aggressively |

This segmentation reflects the reality that "rental supply shortage" in 2026 does not apply uniformly across all property types and locations. The affordable housing shortage—with 2.5 million fewer units under $600 monthly rent [5]—creates particularly strong fundamentals for workforce housing investments.

Risk Management Considerations:

⚠️ Concentration Risk: Portfolios concentrated in oversupplied Sun Belt markets face continued valuation pressure

🎯 Segment Risk: Luxury-heavy portfolios vulnerable to extended absorption periods

📍 Geographic Risk: Single-market portfolios lack diversification to offset regional variations

⏰ Timing Risk: Acquisition timing significantly impacts entry pricing and long-term returns

For institutional investors managing large PRS portfolios, the valuation sensitivity to these segmentation factors creates material impact on reported net asset values and investment performance metrics. Quarterly revaluations must incorporate current market intelligence on supply-demand dynamics rather than relying on trailing comparable evidence.

Financing and Leverage Considerations

The valuation sensitivity in 2026's rental market transition has direct implications for financing and leverage strategies. Lenders conducting loan-to-value assessments must determine whether current valuations reflect sustainable market conditions or temporary supply-demand imbalances that may reverse.

Lender Valuation Approaches:

🏦 Conservative Scenario: Apply higher capitalization rates and conservative rent growth to protect against oversupply return

📊 Market Scenario: Use current market yields and consensus rent growth projections

🎯 Optimistic Scenario: Incorporate supply constraint premium and accelerated rent growth

Most lenders in early 2026 adopt conservative to market scenarios, creating potential valuation gaps between borrower expectations (often optimistic scenario) and lender assessments (conservative scenario). This gap affects maximum loan amounts and required equity contributions.

Leverage Strategy Implications:

- Supply-Constrained Markets: Higher leverage acceptable due to lower downside risk

- Oversupplied Markets: Reduced leverage appropriate given absorption uncertainty

- Luxury Segment: Significantly reduced leverage due to elevated vacancy risk

- Affordable Housing: Maximum leverage justified by strong fundamentals

For borrowers seeking acquisition or refinancing, engaging qualified surveyors to conduct Level 3 building surveys provides lenders with confidence in property condition and supports higher valuation conclusions.

Practical Valuation Guidance for Surveyors and Investors

Documentation and Methodology Transparency

Given the significant valuation sensitivity in 2026's transitioning rental market, documentation and methodology transparency become essential for defensible valuations. Surveyors must clearly articulate the assumptions, adjustments, and market evidence supporting valuation conclusions.

Essential Documentation Elements:

📋 Market Context: Detailed analysis of local supply-demand dynamics, vacancy trends, and construction pipeline

📊 Comparable Evidence: Comprehensive comparable analysis with explicit temporal and location adjustments

🎯 Yield Justification: Clear rationale for capitalization rates applied, including market evidence and risk factors

📈 Growth Assumptions: Documented basis for rent growth projections, including demand sustainability analysis

⚖️ Sensitivity Analysis: Valuation impact of alternative scenarios (conservative, base, optimistic)

This documentation serves multiple purposes: supporting valuation conclusions, providing transparency to clients and lenders, and creating defensibility if valuations are challenged. In rapidly changing markets, the methodology and assumptions often matter more than the specific valuation figure.

For surveyors conducting schedule of condition assessments, integrating property condition analysis with market valuation creates comprehensive reporting that serves client needs.

Scenario Planning and Valuation Ranges

Rather than single-point valuations, the 2026 market environment favors scenario-based approaches that present valuation ranges reflecting different potential market outcomes. This approach acknowledges uncertainty while providing decision-makers with framework for understanding valuation sensitivity.

Three-Scenario Framework:

Conservative Scenario:

- Supply constraints prove temporary as landlord instructions recover

- Rent growth achieves only 5-8% in 2026 vs. 20% projection

- Vacancy rates stabilize at 6-7% rather than declining substantially

- Valuation Impact: 10-15% below base case

Base Case Scenario:

- Supply constraints persist through 2026 as projected

- Rent growth achieves 15-20% in Q2-Q4 2026

- Vacancy rates decline to 5-6% by year-end

- Valuation Impact: Current market evidence

Optimistic Scenario:

- Supply constraints intensify beyond current projections

- Rent growth exceeds 20% as competition for tenants increases

- Vacancy rates decline below 5% in supply-constrained markets

- Valuation Impact: 10-20% above base case

This scenario framework allows investors and lenders to understand the valuation sensitivity to different market outcomes and make risk-adjusted decisions accordingly. Properties in supply-constrained Northeast markets have narrower scenario ranges (lower uncertainty) compared to oversupplied Sun Belt luxury properties (higher uncertainty).

Monitoring and Revaluation Triggers

Given the rapid market transition from oversupply to shortage, establishing monitoring frameworks and revaluation triggers becomes essential for portfolio management and financial reporting accuracy.

Key Monitoring Metrics:

📊 Vacancy Rates: Monthly tracking of property-level and market-level vacancy trends

💰 Rental Achievement: Actual rents achieved vs. projections, including concessions

📈 Landlord Instructions: Regional RICS survey data on new supply coming to market

🏗️ Construction Pipeline: Permits, starts, and completions in relevant markets

⏰ Absorption Rates: Speed at which new supply is absorbed by tenant demand

Revaluation Triggers:

- Vacancy rate changes exceeding ±200 basis points from valuation assumptions

- Rental achievement variance exceeding ±10% from projections

- Material change in local supply pipeline (major project announcements or cancellations)

- Significant economic developments affecting local employment and household formation

- Regulatory changes impacting landlord operating environment

For portfolios valued quarterly or annually, interim monitoring allows early identification of valuation trends and timely adjustments to investment strategies. Properties showing positive variance from valuation assumptions may warrant accelerated acquisition activity, while negative variance properties may require disposition consideration.

Conclusion

The rental market's dramatic transition from the 7.3% vacancy rates of early 2026 to acute supply shortages by February—evidenced by the -27% collapse in landlord instructions—creates unprecedented valuation sensitivity for PRS properties. Understanding Rental Supply Shortage and Valuation Sensitivity: Assessing PRS Property Values Amid Tenant Demand Surge in 2026 requires surveyors and investors to fundamentally recalibrate valuation methodologies, yield assumptions, and risk assessments.

The projected +20% rent growth in Q2 2026 represents a dramatic reversal from six consecutive months of rent declines, but this growth potential varies dramatically by region and property segment. Supply-constrained Northeast markets with 5.2% vacancy rates command premium valuations and compressed yields, while oversupplied Sun Belt markets facing 9.1% vacancy rates require conservative assumptions and extended absorption timelines. The luxury segment's persistent 11.1% vacancy rates create particular valuation challenges despite broader market tightening.

Key Action Steps for Property Professionals:

✅ Recalibrate Comparable Evidence: Apply temporal adjustments to late 2025 comparables that reflect the rapid supply-demand shift

✅ Implement Regional Differentiation: Abandon one-size-fits-all approaches in favor of location-specific valuation frameworks

✅ Document Methodology Rigorously: Provide transparent documentation of assumptions, adjustments, and sensitivity analysis

✅ Adopt Scenario-Based Valuations: Present valuation ranges reflecting conservative, base, and optimistic market outcomes

✅ Establish Monitoring Frameworks: Track key metrics and revaluation triggers to identify emerging trends early

✅ Segment Portfolio Analysis: Recognize divergent fundamentals across property types, locations, and tenant segments

For investors, the current market transition creates both significant opportunities and material risks. Properties acquired during the late 2025 oversupply period at distressed pricing may realize substantial appreciation as supply constraints tighten. However, properties in persistently oversupplied segments or locations may face continued valuation pressure despite the broader shortage narrative.

The structural housing supply gap of 4.03 million homes and the deepening affordability crisis—with 2.5 million fewer units under $600 monthly rent—support long-term rental demand fundamentals. Yet the 40% collapse in multifamily construction starts ensures supply constraints will persist well beyond 2026, creating sustained pricing power for well-positioned PRS properties.

Surveyors conducting valuations in this environment must balance optimism about supply constraints against realistic assessment of demand sustainability, regional variations, and segment-specific challenges. The valuation sensitivity to these factors makes methodology, documentation, and scenario analysis more important than ever for defensible, decision-useful valuations.

For professional guidance on rental property valuations, consider engaging RICS registered valuers who can provide comprehensive assessment incorporating current market intelligence and rigorous methodology appropriate for 2026's dynamic rental market conditions.

References

[1] multifamilydive – https://www.multifamilydive.com/news/rent-outlook-2026-multifamily-apartment/809477/

[2] Us Rental Market Vacancy Rates Reach Record High In 2026 – https://www.noradarealestate.com/blog/us-rental-market-vacancy-rates-reach-record-high-in-2026/

[3] Housing Market Predictions – https://www.zillow.com/learn/housing-market-predictions/

[4] Us Housing Supply Gap 2026 – https://www.realtor.com/research/us-housing-supply-gap-2026/

[5] Harvards 2026 Rental Housing Report Points To A Softer Market With A Deeper Affordability Crisis – https://www.novoco.com/notes-from-novogradac/harvards-2026-rental-housing-report-points-to-a-softer-market-with-a-deeper-affordability-crisis