The landscape for luxury property valuations has fundamentally shifted. Following the Autumn Budget announcement, properties valued above £2 million now face unprecedented scrutiny and taxation measures that will reshape how surveyors approach high-value assessments. With the new mansion tax set to impact over 100,000 households and strategic market behavior already emerging, professional surveyors must adapt their methodologies to navigate this complex new environment.

Understanding Post-Budget 2026 Valuation Challenges: Surveyor Strategies for High-Value Properties Over £2 Million has become essential for RICS-qualified professionals working in London's prime markets and across the South East. The stakes have never been higher, with property owners increasingly relying on expert valuations to minimize tax exposure while ensuring compliance with evolving regulations.

Key Takeaways

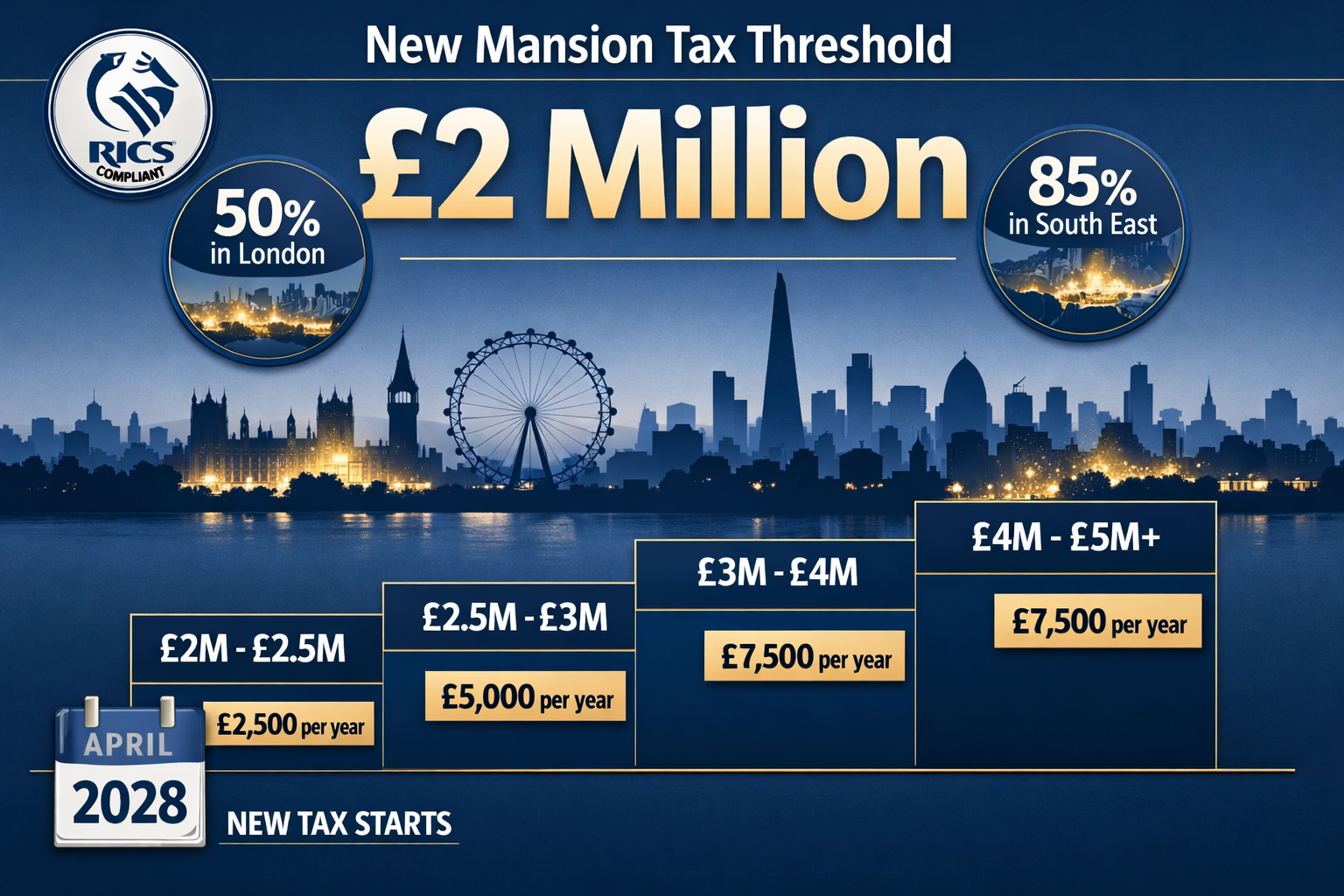

- 🏛️ New mansion tax threshold: Properties valued over £2 million face annual charges of £2,500-£7,500 starting April 2028, affecting 100,000+ households across the UK

- 📍 Geographic concentration: 50% of affected properties are in London, with 85% concentrated in the South East, creating regional valuation complexities

- ⏰ Critical deadline approaching: Property owners have until March 31, 2026, to request rateable value changes before new valuations take effect April 1, 2026

- 💼 Market behavior shifts: 83% of offers on properties near the £2 million threshold now come in below this mark, compared to 64% a year earlier

- 🔍 Enhanced scrutiny required: RICS-compliant adjustment techniques and robust comparable evidence are essential for defending valuations in disputes

Understanding the New Mansion Tax Framework and Its Impact on Valuations

The mansion tax represents the most significant change to high-value property taxation in over a decade. Properties in England valued above £2 million will face annual charges ranging from £2,500 to £7,500 depending on their assessed value, with implementation scheduled for April 2028.[1]

The £2 Million Threshold: A New Valuation Battleground

The government's decision to establish the threshold at precisely £2 million has created what industry experts call a "valuation cliff edge." This sharp demarcation point means that a property valued at £1,995,000 faces zero mansion tax liability, while one assessed at £2,005,000 triggers an immediate annual charge of at least £2,500.

Geographic Distribution of Affected Properties:

| Region | Percentage of £2M+ Properties | Estimated Households Affected |

|---|---|---|

| London | 50% | 50,000+ |

| South East (excl. London) | 35% | 35,000+ |

| Rest of England | 15% | 15,000+ |

This concentration in London and the South East creates unique challenges for chartered surveyors working in these regions, where market volatility and comparable evidence can vary dramatically between neighboring postcodes.

Market Behavioral Changes Already Evident

Strategic pricing behavior has emerged rapidly. In February 2026, 83% of offers on homes priced within 10% of £2 million came in below the threshold, compared to just 64% a year earlier.[1] This dramatic shift demonstrates how tax considerations are already influencing negotiation strategies and, consequently, the pressure on surveyors to justify valuations.

"We are sceptical about whether the revaluation needed for this mansion tax can be delivered cleanly and on time." – Paula Higgins, CEO, HomeOwners Alliance[1]

This industry skepticism highlights the infrastructure challenges facing the valuation profession. Surveyors must now balance accuracy with the reality that their assessments carry significantly higher financial consequences for property owners.

Additional Tax Burden Considerations

The mansion tax doesn't exist in isolation. Property owners and investors face compounding tax increases:

- Stamp duty surcharge increase: Rising from 3% to 5% for second homes and buy-to-let properties, with estimated costs potentially jumping from £12,266 to £24,781 by 2029[5]

- Property income tax rises: Increasing by 2% across all brackets from April 2027, reaching 22%, 42%, and 47% respectively[1]

- Projected house price increases: OBR forecasts of 2.1% in 2026, 2.8% in 2027, and 3% in both 2028 and 2029 will compound valuation-related costs[5]

These interconnected tax changes mean that professional surveyors must now consider the broader fiscal context when advising clients on high-value properties.

RICS-Compliant Valuation Techniques for Post-Budget 2026 Challenges

Navigating Post-Budget 2026 Valuation Challenges: Surveyor Strategies for High-Value Properties Over £2 Million requires enhanced technical proficiency and rigorous adherence to professional standards. The RICS Red Book provides the foundation, but surveyors must now apply these principles with heightened precision given the tax implications.

Enhanced Comparable Evidence Analysis

The traditional comparable method remains fundamental, but the threshold effect demands more sophisticated application:

Key Adjustments Required:

-

Time adjustments: With the April 2026 revaluation deadline approaching, surveyors must carefully adjust comparables for market movements, particularly given projected 2.1% annual growth[5]

-

Location micro-analysis: In concentrated markets like Kensington, Chelsea, and Fulham, street-by-street variations can mean the difference between falling above or below the threshold

-

Condition and specification adjustments: Period features, recent renovations, and energy efficiency improvements must be quantified with greater precision

-

Strategic pricing recognition: Surveyors must distinguish between genuine market value and strategically discounted asking prices designed to avoid the threshold

Valuation Methodology for Threshold Properties

For properties valued between £1.8 million and £2.2 million, a dual-methodology approach provides defensibility:

Primary Method: Comparable Evidence

- Minimum of 5-7 recent comparables (within 6 months)

- Detailed adjustment schedule with percentage impacts documented

- Geographic radius tightened to 0.5 miles in urban areas

- Transaction evidence preferred over asking prices

Secondary Method: Residual or Investment Approach

- Provides cross-check validation

- Particularly valuable for properties with development potential

- Demonstrates value from alternative perspective

This dual approach strengthens the surveyor's position when valuations are challenged, whether by property owners seeking lower assessments or tax authorities questioning valuations just below the threshold.

Documentation Standards for Dispute Resilience

Given the two-stage "Check and Challenge" process available to property owners,[4] surveyors must prepare documentation that withstands scrutiny:

✅ Comprehensive inspection records: Detailed notes, photographs, and measurements

✅ Comparable evidence schedules: Full addresses, transaction dates, adjusted values

✅ Adjustment rationale: Written justification for each percentage adjustment applied

✅ Market context analysis: Local market trends, supply-demand dynamics

✅ Professional qualification verification: Current RICS membership and relevant expertise

Understanding what a surveyor checks during inspections becomes even more critical when valuations may be subject to formal challenges.

Special Considerations for London Prime Markets

London's luxury property market presents unique valuation complexities that require specialized expertise:

Prime Central London Factors:

- International buyer demand fluctuations

- Freehold vs. leasehold value differentials

- Building-specific amenities (concierge, gym, security)

- Lateral space premiums in period conversions

- Garden and outdoor space value multipliers

Surveyors working in areas like Hammersmith, Chiswick, and Ealing must recognize that these submarkets often behave differently from broader London trends, particularly around threshold values.

Technology-Enhanced Valuation Approaches

Modern surveying tools provide additional accuracy and defensibility:

- Laser measurement systems: Eliminate measurement disputes

- Thermal imaging: Identify hidden defects affecting value

- Drone photography: Document property context and positioning

- GIS mapping tools: Analyze location premiums with precision

- Automated valuation models (AVMs): Cross-reference (but never replace) professional judgment

The integration of these technologies into comprehensive survey methodologies strengthens the evidential basis for valuations that may face challenges.

Expert Witness Strategies and Practical Tools for Valuation Disputes

As Post-Budget 2026 Valuation Challenges: Surveyor Strategies for High-Value Properties Over £2 Million intensify, surveyors increasingly find themselves in expert witness roles. The financial stakes—potentially thousands in annual tax liability—mean that disputed valuations will routinely progress through formal challenge processes.

The Two-Stage Challenge Process Explained

Understanding the procedural framework is essential for surveyors preparing defensible valuations:

Stage 1: Check (Factual Correction)

- Property owners can correct factual errors in their rateable value assessment

- Deadline: March 31, 2026, for current values[2]

- Focus: Physical characteristics, floor areas, property description

- Surveyor role: Provide accurate property data, correct measurements

Stage 2: Challenge (Valuation Dispute)

- Requires supporting evidence if Check doesn't resolve the issue[4]

- Formal submission to Valuation Office Agency (VOA)

- Surveyor role: Prepare comprehensive valuation report with comparable evidence

- Timeline: Can extend several months depending on complexity

After April 1, 2026, only future rateable values can be modified,[2] making the current window critical for property owners seeking adjustments.

Expert Witness Report Structure

When acting as an expert witness in valuation disputes, surveyors should structure reports to meet legal and professional standards:

Essential Report Components:

-

Executive Summary

- Property details and inspection date

- Valuation conclusion with clear statement

- Key factors supporting the valuation

-

Property Description

- Location analysis with map

- Physical characteristics and condition

- Accommodation schedule with measurements

- Photographs and floor plans

-

Market Analysis

- Local market trends and transaction volumes

- Supply-demand dynamics

- Price movements over relevant period

- Impact of budget changes on market behavior

-

Comparable Evidence

- Minimum 5-7 comparables in tabular format

- Adjustment schedule with percentage impacts

- Explanation of adjustments applied

- Maps showing comparable locations

-

Valuation Methodology

- Approach selected and justification

- Calculations and working

- Cross-check methodologies

- Sensitivity analysis around threshold

-

Professional Declaration

- RICS compliance statement

- Independence confirmation

- Qualifications and experience

- Understanding of expert witness duties

Case Study: Prime London Townhouse Valuation Dispute

Property: Four-bedroom Victorian townhouse, South East London

Initial VOA Assessment: £2,150,000

Owner's Contention: £1,950,000

Dispute Value: £200,000 (difference between tax liability and no liability)

Surveyor's Approach:

The appointed surveyor conducted a Level 3 building survey to identify all condition issues affecting value. Key findings included:

- Deferred maintenance estimated at £85,000

- Outdated mechanical systems requiring replacement

- Damp issues in basement level

- Period features in fair-to-poor condition

Comparable Analysis:

Seven recent transactions were identified within 0.3 miles, with adjusted values ranging from £1,875,000 to £2,025,000. After applying condition adjustments, the surveyor's professional opinion supported a value of £1,975,000.

Outcome: The VOA accepted the revised valuation during the Check stage, avoiding formal Challenge proceedings and saving the owner approximately £2,500 annually in mansion tax liability.

Practical Tools for Surveyors

Valuation Adjustment Calculator Template:

| Adjustment Factor | Comparable A | Comparable B | Comparable C |

|---|---|---|---|

| Sale Price | £2,100,000 | £1,950,000 | £2,050,000 |

| Time Adjustment (2.1% annual) | -1.75% | +3.50% | -0.88% |

| Location Premium | -2.00% | +1.50% | 0.00% |

| Size Differential | +3.50% | -2.00% | +1.50% |

| Condition | -4.00% | -1.00% | -3.00% |

| Adjusted Value | £2,019,750 | £2,000,475 | £1,999,225 |

This systematic approach demonstrates professional rigor and provides transparency for challenge proceedings.

Coordination with Other Professionals

High-value property disputes often require multi-disciplinary teams:

- Structural engineers: For properties with defects affecting value

- Party wall surveyors: When neighboring development impacts value (see our guide on finding qualified party wall surveyors)

- Tax advisors: To understand full fiscal implications

- Legal counsel: For formal challenge proceedings

- Specialized valuers: For unique property types or features

Understanding when to recommend additional expertise strengthens the surveyor's credibility and ensures comprehensive client service.

Regional Considerations Beyond London

While London dominates the £2 million+ market, significant concentrations exist in:

- Oxfordshire: Historic properties and country estates

- Berkshire: Commuter belt luxury homes

- Buckinghamshire: Period properties and modern developments

- Surrey towns like Guildford, Weybridge, and Leatherhead

Each region presents distinct market characteristics requiring local expertise and comparable evidence specific to the area.

Ethical Considerations and Professional Standards

Surveyors face ethical pressures when clients seek valuations below the £2 million threshold. Professional obligations require:

⚖️ Independence: Valuations must reflect genuine market value, not desired outcomes

⚖️ Objectivity: Personal relationships or fee arrangements cannot influence professional judgment

⚖️ Transparency: Assumptions, limitations, and uncertainties must be clearly stated

⚖️ Competence: Only accept instructions within areas of expertise and knowledge

The RICS Code of Conduct provides clear guidance, and surveyors should document their adherence to these principles in all valuation reports.

Conclusion

The post-Budget 2026 landscape for high-value property valuations has fundamentally transformed. With the mansion tax threshold established at £2 million and affecting over 100,000 households, surveyors face unprecedented responsibility in their assessments. The geographic concentration in London and the South East, combined with strategic market behavior already evident, means that valuation precision has never carried higher stakes.

Post-Budget 2026 Valuation Challenges: Surveyor Strategies for High-Value Properties Over £2 Million demand enhanced technical proficiency, rigorous RICS compliance, and comprehensive documentation standards. The critical March 31, 2026, deadline for rateable value challenges means property owners and their surveyors must act decisively.

Actionable Next Steps for Surveyors:

-

Update comparable databases with recent transactions, noting strategic pricing behavior around the £2 million threshold

-

Enhance documentation protocols to ensure all valuations can withstand Check and Challenge scrutiny

-

Invest in technology tools including laser measurement systems and thermal imaging to strengthen evidential basis

-

Develop expert witness capabilities through specialized training and report-writing practice

-

Build professional networks with structural engineers, tax advisors, and legal counsel for complex cases

-

Review regional market dynamics in key areas like London, Oxfordshire, and Berkshire to understand local valuation factors

-

Maintain RICS compliance through continuing professional development focused on high-value property valuation

For property owners with assets approaching or exceeding the £2 million threshold, engaging a qualified chartered surveyor with expertise in high-value properties is essential. Whether considering a comprehensive building survey or preparing for a valuation challenge, professional guidance can mean the difference between significant annual tax liability and legitimate tax efficiency.

The valuation profession stands at a pivotal moment. Those surveyors who adapt their methodologies, embrace enhanced standards, and develop dispute resolution expertise will not only serve their clients effectively but also strengthen the integrity of the high-value property market through this period of significant fiscal change.

References

[1] New Property Tax – https://hoa.org.uk/news/new-property-tax/

[2] Business Rates Revaluation 2026 – https://www.gov.uk/government/news/business-rates-revaluation-2026

[3] Revaluation 2026 Everything You Need To Know – https://valuationoffice.blog.gov.uk/2025/09/29/revaluation-2026-everything-you-need-to-know/

[4] Revaluation 2026 Everything You New To Know – https://valuationoffice.blog.gov.uk/2025/09/29/revaluation-2026-everything-you-new-to-know/

[5] Homebuyers and Investors Face Higher Costs After Budget Changes – https://eldridgeestates.co.uk/blog/homebuyers-and-investors-face-higher-costs-after-budget-changes/40029