The UK rental market stands at a critical juncture in 2026, where declining rental inflation meets intensifying regulatory pressures on landlords. As average monthly rents reached £1,368—growing at just 4.0% annually, the slowest pace since May 2022[1]—property investors face a complex valuation landscape. Understanding Valuation Adjustments for 2026 Rental Market Shifts: Impact of Landlord Tax Pressures on UK Yields has become essential for surveyors, landlords, and investors navigating this transforming market.

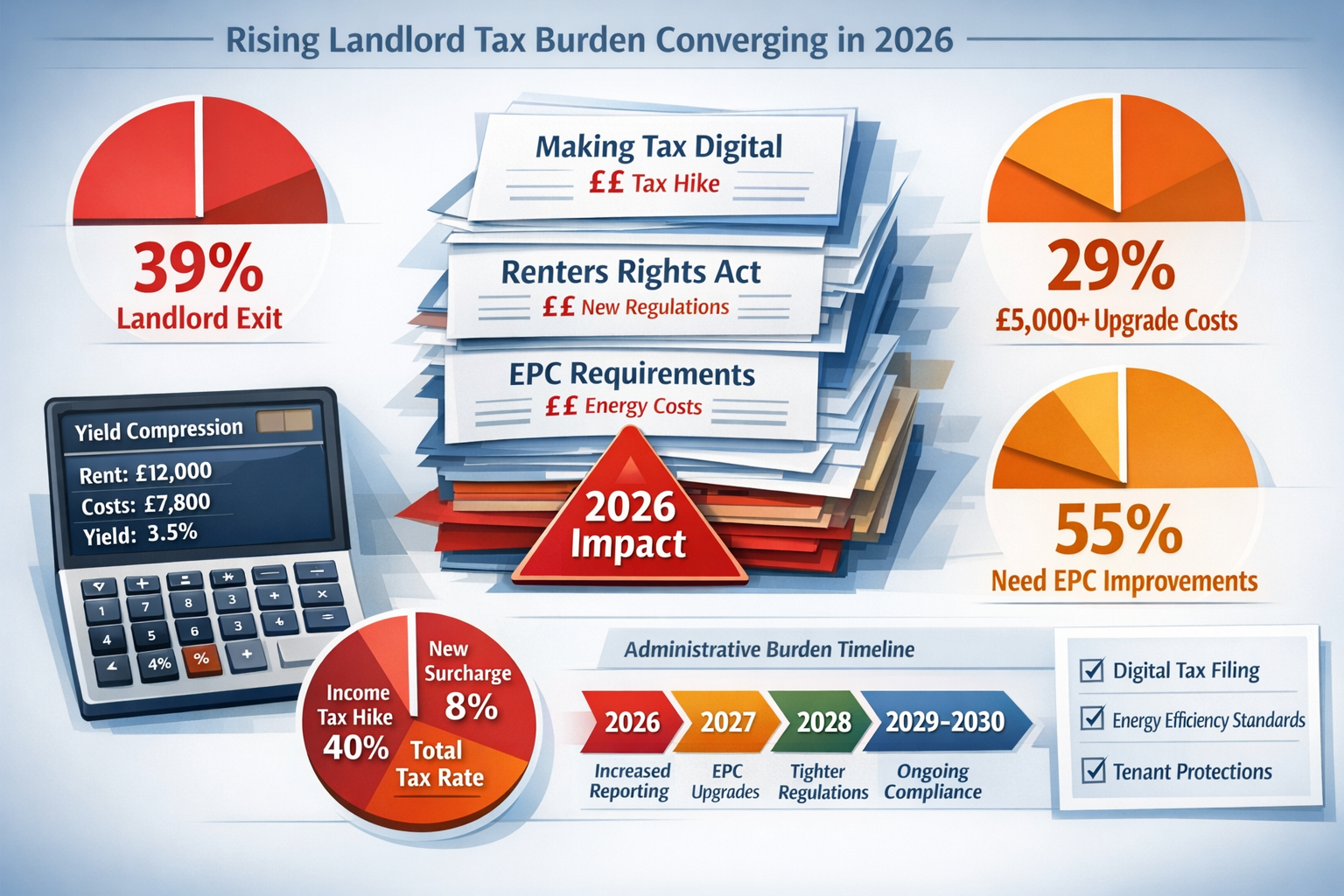

The convergence of Making Tax Digital implementation, the Renters' Rights Act (effective May 1, 2026), and escalating Energy Performance Certificate (EPC) requirements creates unprecedented challenges for yield calculations. With 39% of landlords considering market exit[2] and rental growth forecasted at just 2.6% for 2026[2], accurate property valuations must account for multiple regulatory headwinds that directly compress net returns.

Key Takeaways

- 📉 Rental inflation has slowed to 4.0% annually (December 2025), the lowest rate since May 2022, with forecasts predicting just 2.6% growth for 2026

- 💷 Tax and regulatory pressures are intensifying, with 39% of landlords stating the Renters' Rights Act may force market exit and 29% facing EPC upgrade costs exceeding £5,000 per property

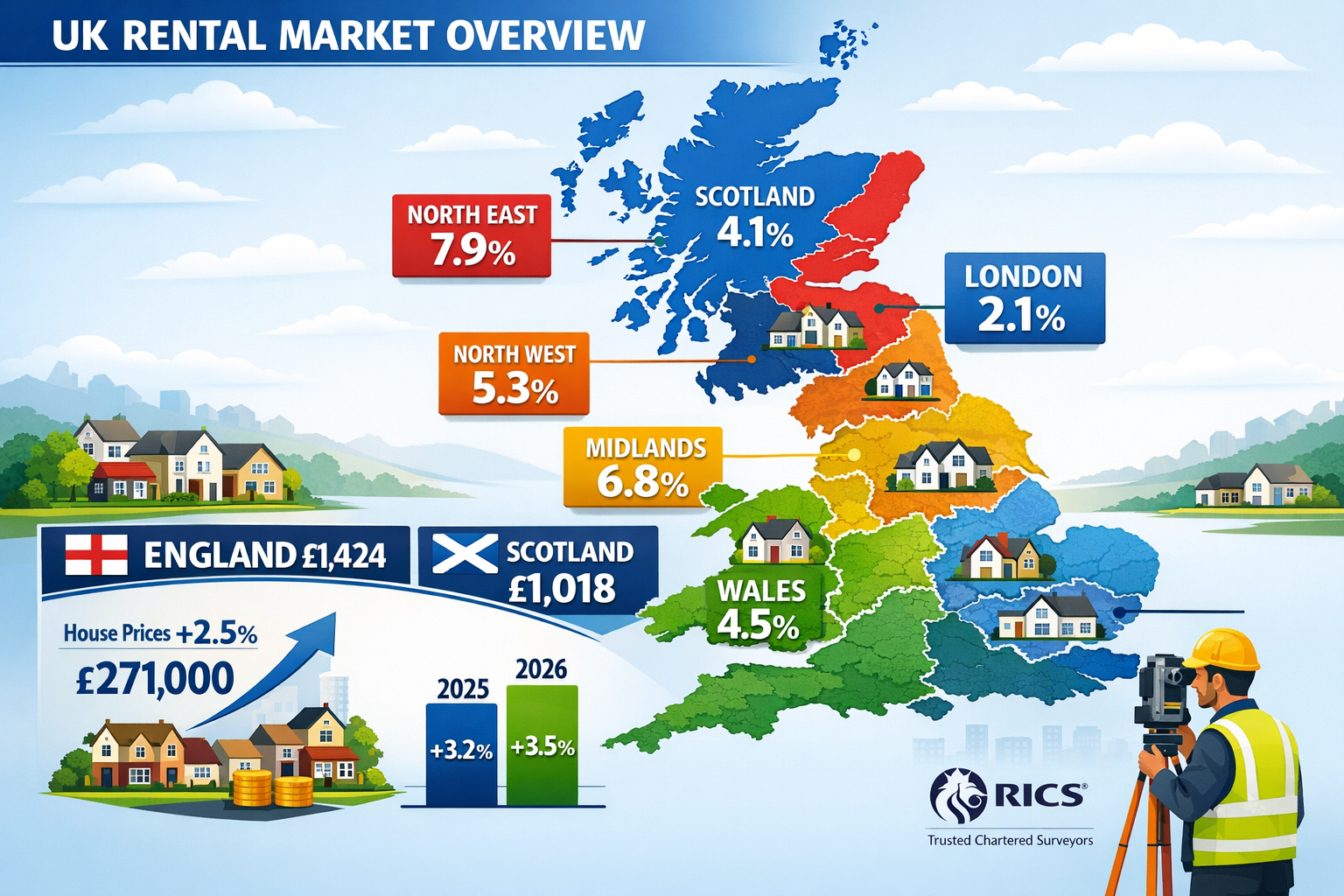

- 🏘️ Regional variations are substantial, ranging from 7.9% rental growth in the North East to just 2.1% in London, requiring location-specific valuation approaches

- 📊 Yield compression is accelerating as house prices grow 2.5% while rental growth moderates, necessitating sophisticated tax-adjusted valuation methodologies

- ⚖️ Supply-side contractions may offset demand, with potential landlord exits creating upward rental pressure that could support yields despite regulatory headwinds

Understanding the 2026 UK Rental Market Landscape

Current Rental Inflation Trends Across UK Regions

The UK rental market in 2026 presents a geographically fragmented picture that challenges traditional valuation approaches. Average monthly private rents increased by 4.0% to £1,368 in the 12 months to December 2025, representing a significant deceleration from 4.4% growth in November 2025[1]. This marks the lowest annual rental inflation since May 2022, signaling a fundamental shift in market dynamics.

Regional variations reveal critical valuation considerations:

| Region | Average Monthly Rent | Annual Growth Rate | Key Characteristics |

|---|---|---|---|

| England | £1,424 | 3.9% | Lowest growth since May 2022 |

| North East | Not specified | 7.9% | Highest regional inflation |

| London | Not specified | 2.1% | Lowest regional inflation |

| Scotland | £1,018 | 2.8% | Moderate growth trajectory |

| Wales | £822 | 5.7% | Strong rental growth despite low prices |

These regional disparities necessitate location-specific valuation adjustments. While Wales demonstrates attractive yield potential with 5.7% rental growth against an average price of just £822[1], London's 2.1% growth creates yield compression challenges despite higher absolute rents.

House Price Appreciation and Capital Value Context

Property capital values provide essential context for yield calculations. Average UK house prices increased by 2.5% to £271,000 in the 12 months to November 2025, up from 1.9% growth in the prior year[1]. This acceleration in capital appreciation relative to slowing rental growth creates a mathematical squeeze on gross yields.

Scotland demonstrates the strongest capital appreciation at 4.5%, reaching £193,000[1], while Wales shows minimal growth of just 0.7% to £209,000[1]. For investors focused on income rather than capital gains, understanding these dynamics is crucial for capital gains tax valuation strategies.

Forecasted Rental Growth for 2026

Industry forecasts suggest continued moderation in rental inflation. Zoopla has predicted rental growth of 2.6% for 2026[2], substantially below the 4.0% recorded in late 2025. This deceleration reflects multiple factors:

- 🏠 Supply-side adjustments as landlords exit the market

- 📊 Demand normalization following post-pandemic rental surges

- 💰 Affordability constraints limiting tenant capacity for rent increases

- ⚖️ Regulatory uncertainty dampening investor confidence

Professional surveyors conducting commercial valuation or residential assessments must incorporate these growth projections into discounted cash flow models and yield calculations.

Valuation Adjustments for 2026 Rental Market Shifts: Tax and Regulatory Pressures

Making Tax Digital: Administrative Burden and Compliance Costs

The Making Tax Digital (MTD) initiative represents a significant administrative shift for landlords in 2026. This digital reporting requirement mandates quarterly submission of income and expenses through compatible software, replacing traditional annual self-assessment processes.

Industry experts recommend landlords "act sooner rather than later"[2] to prepare for MTD implementation, which introduces several valuation considerations:

Direct Cost Impacts:

- Software subscription fees (£5-£20 monthly)

- Accountancy support for digital compliance

- Time investment for quarterly reporting

- Potential penalties for non-compliance

Indirect Yield Effects:

- Increased administrative burden reducing net returns

- Professional fees compressing profit margins

- Enhanced scrutiny of expense deductions

- Greater transparency potentially limiting tax optimization

For valuation purposes, surveyors should incorporate an additional 0.5-1.0% operational cost burden into net yield calculations to reflect MTD compliance requirements. This adjustment becomes particularly significant for smaller portfolio landlords without existing accounting infrastructure.

The Renters' Rights Act: Supply-Side Implications

The Renters' Rights Act, effective May 1, 2026, represents the most significant regulatory intervention in the UK rental market in decades. Its impact on property valuations extends beyond immediate compliance costs to fundamental supply-demand dynamics.

Critical provisions affecting valuations:

- Abolition of Section 21 "no-fault" evictions 🚫

- Enhanced tenant rights for challenging rent increases

- Stricter property condition standards

- Expanded grounds for possession with higher evidential requirements

The legislation's most alarming statistic for valuations: 39% of landlords state the Act may force them to leave the rental market[2]. This potential supply contraction creates competing valuation pressures:

Negative Yield Factors:

- Reduced landlord flexibility increasing void periods

- Higher legal costs for possession proceedings

- Enhanced maintenance obligations

- Reduced ability to optimize rental pricing

Positive Yield Factors:

- Supply reduction supporting rental growth

- Decreased competition from amateur landlords

- Professionalization benefiting experienced investors

- Potential for rental premium from quality compliance

Professional surveyors must assess individual property circumstances when applying these adjustments, particularly considering landlord experience levels and property condition standards.

Energy Performance Certificate Requirements: Capital Expenditure Pressures

The government's proposed minimum EPC rating of C by 2028 for new tenancies and 2030 for existing tenancies[2] creates the most quantifiable valuation adjustment for 2026 rental properties.

Current market impact statistics:

- 📊 55% of landlords expect to need EPC improvements[2]

- 💷 29% anticipate costs exceeding £5,000 per property[2]

- ⚠️ Regulatory uncertainty on spending caps and exemptions remains unresolved

Typical EPC upgrade costs by current rating:

| Current Rating | Target Rating | Typical Upgrade Cost | Common Improvements Required |

|---|---|---|---|

| E | C | £8,000-£15,000 | Insulation, boiler, double glazing |

| D | C | £3,000-£8,000 | Insulation upgrades, heating controls |

| C | Already compliant | £0 | Maintenance only |

For valuation purposes, these capital requirements must be reflected through:

- Immediate deduction from market value for non-compliant properties

- Yield adjustment reflecting amortized upgrade costs

- Risk premium for regulatory uncertainty

- Potential obsolescence for properties where upgrades are uneconomical

Properties currently rated D or E require particular scrutiny. A property valued at £250,000 requiring £10,000 in EPC upgrades effectively trades at a 4% discount before considering financing costs or yield compression during improvement works.

Surveyors conducting RICS homebuyer surveys should explicitly identify EPC ratings and provide cost estimates for compliance, as this directly affects investment viability.

Valuation Adjustments for 2026 Rental Market Shifts: RICS-Compliant Yield Calculation Methodologies

Gross Yield vs. Net Yield: Tax-Adjusted Returns

Understanding the distinction between gross and net yields becomes critical when evaluating Valuation Adjustments for 2026 Rental Market Shifts: Impact of Landlord Tax Pressures on UK Yields. Traditional gross yield calculations fail to capture the full impact of 2026's regulatory environment.

Gross Yield Calculation:

Gross Yield = (Annual Rental Income / Property Value) × 100

Example: £1,424 monthly rent × 12 = £17,088 annual income

Property value: £271,000

Gross yield: (£17,088 / £271,000) × 100 = 6.30%

However, this calculation ignores critical deductions:

Net Yield Calculation Components:

✅ Deductible Expenses:

- Mortgage interest (now restricted to 20% tax credit)

- Property management fees (10-15% of rent)

- Maintenance and repairs (1-2% of property value annually)

- Insurance (£200-£500 annually)

- Safety certifications (gas, electrical, EPC)

- Ground rent and service charges (leasehold)

- Void periods (assume 5-10% annually)

- MTD compliance costs (new for 2026)

- EPC upgrade amortization (new for 2026)

Tax Considerations:

- Income tax at marginal rate (20%, 40%, or 45%)

- Restricted mortgage interest relief (20% tax credit only)

- National Insurance (for incorporated landlords)

- Capital Gains Tax on disposal

Revised Net Yield Example:

| Item | Amount |

|---|---|

| Annual rental income | £17,088 |

| Less: Operating expenses | |

| Management fees (12%) | -£2,051 |

| Maintenance (1.5%) | -£4,065 |

| Insurance | -£350 |

| Safety certificates | -£400 |

| MTD compliance | -£240 |

| Void periods (7%) | -£1,196 |

| Net operating income | £8,786 |

| Less: Financing costs | |

| Mortgage interest (4%, 75% LTV) | -£8,130 |

| Pre-tax cash flow | £656 |

| Less: Income tax (40% taxpayer) | |

| Tax on rental profit | -£3,514 |

| Mortgage interest tax credit (20%) | +£1,626 |

| Net annual return | -£1,232 |

| Net yield | -0.45% |

This example demonstrates how higher-rate taxpayers can experience negative cash flow despite positive gross yields—a critical consideration for 2026 valuations.

Regional Yield Variations and Comparative Analysis

RICS-compliant valuations require comparable evidence from similar properties in the same market. The 2026 rental landscape demands regional segmentation:

Regional Yield Profiles (Estimated):

🏴 England (Average):

- Gross yield: 5.8-6.2%

- Net yield: 2.1-3.4% (basic rate taxpayer)

- Net yield: 0.8-2.1% (higher rate taxpayer)

🏴 Scotland:

- Gross yield: 6.3-6.8%

- Net yield: 2.6-3.9%

- Stronger capital appreciation (4.5%) offsets lower rental growth

🏴 Wales:

- Gross yield: 4.7-5.3%

- Net yield: 1.9-3.2%

- Attractive rental growth (5.7%) despite lower absolute rents

📍 London:

- Gross yield: 4.2-4.8%

- Net yield: 1.0-2.3%

- Lowest rental inflation (2.1%) creates yield compression

📍 North East England:

- Gross yield: 7.2-8.1%

- Net yield: 3.8-5.1%

- Highest rental inflation (7.9%) supports strong yields

Surveyors must select comparables from the appropriate regional market and adjust for property-specific factors including condition, EPC rating, and tenure type.

Incorporating Regulatory Costs into Discounted Cash Flow Models

Professional property valuations increasingly employ discounted cash flow (DCF) analysis to capture the time value of regulatory compliance costs. This methodology proves particularly valuable for properties requiring significant EPC upgrades or facing potential obsolescence under the Renters' Rights Act.

DCF Valuation Framework for 2026:

Step 1: Project Cash Flows (Years 1-10)

- Year 1-2: Current rental income with 2.6% annual growth[2]

- Year 3: Rental disruption for EPC upgrades (-20% for 3 months)

- Year 4-10: Normalized rental growth (2.5% annually)

Step 2: Incorporate Regulatory Costs

- Year 1: MTD implementation (£500 one-time + £200 annual)

- Year 2: EPC survey and planning (£1,000)

- Year 3: EPC upgrade capital expenditure (£7,500)

- Years 4-10: Enhanced maintenance standards (+15% annual costs)

Step 3: Apply Tax Adjustments

- Mortgage interest restriction (20% tax credit only)

- Marginal income tax rate (20%, 40%, or 45%)

- Capital allowances for qualifying improvements

Step 4: Calculate Terminal Value

- Exit yield assumption (adjust for market conditions)

- Disposal costs (1.5-2% of sale price)

- Capital Gains Tax (10% or 20% after annual exemption)

Step 5: Discount to Present Value

- Risk-adjusted discount rate (8-12% for residential)

- Higher rates for properties with regulatory uncertainty

- Lower rates for compliant, well-maintained properties

This methodology provides a comprehensive valuation that captures both immediate and long-term impacts of 2026's regulatory environment. For professional guidance on complex valuations, consider engaging chartered surveyors in Central London with expertise in rental market analysis.

Adjusting for Supply-Side Contractions

The potential for landlord exits creates a unique valuation consideration for 2026. With 39% of landlords contemplating market departure[2], supply-side contractions may offset regulatory pressures through enhanced rental pricing power.

Valuation scenarios:

Pessimistic (High Exit Scenario):

- 15-20% reduction in rental supply over 24 months

- Rental growth accelerates to 4-5% annually

- Yields stabilize despite regulatory costs

- Professional landlords gain market share

Base Case (Moderate Exit):

- 8-12% supply reduction

- Rental growth maintains 2.6-3.2% trajectory

- Yields compress moderately (0.5-1.0%)

- Mixed market with amateur and professional landlords

Optimistic (Low Exit):

- 3-5% supply reduction

- Rental growth slows to 1.8-2.4%

- Significant yield compression (1.5-2.5%)

- Regulatory compliance becomes competitive advantage

Surveyors should apply sensitivity analysis to valuation models, testing multiple supply scenarios to establish valuation ranges rather than single-point estimates.

Strategic Valuation Considerations for Different Property Types

Houses in Multiple Occupation (HMOs)

HMOs face intensified scrutiny under 2026 regulations, with enhanced licensing requirements and safety standards creating distinct valuation challenges:

Positive Factors:

- Higher gross yields (8-12% typical)

- Strong demand from young professionals

- Multiple income streams reducing void risk

Negative Factors:

- Enhanced fire safety requirements

- Stricter licensing (additional £1,000-£2,000 annually)

- Higher management intensity

- Greater exposure to Renters' Rights Act provisions

Valuation adjustments: Apply 15-20% discount to comparable single-let properties to reflect regulatory burden, then add 30-40% premium for income enhancement, resulting in net 10-20% premium for compliant HMOs.

Leasehold vs. Freehold Rental Properties

Tenure type significantly affects 2026 valuations, particularly regarding EPC upgrade responsibilities:

Leasehold Challenges:

- Ground rent and service charge inflation

- Freeholder permission required for improvements

- Potential licence to alter costs

- Shared responsibility for building-wide EPC improvements

Freehold Advantages:

- Complete control over property improvements

- No ground rent burden

- Ability to capitalize on energy efficiency investments

- Greater flexibility for regulatory compliance

Valuation impact: Leasehold properties typically trade at 5-10% discount to equivalent freeholds, with the discount widening to 12-18% for properties requiring significant EPC improvements requiring freeholder consent.

New Build vs. Period Properties

Property age creates distinct regulatory exposure profiles:

New Build Properties:

- ✅ Typically EPC rating A or B (no upgrade costs)

- ✅ Lower maintenance requirements

- ✅ NHBC warranty coverage

- ❌ Service charge inflation risk

- ❌ Potential building safety levy costs

Period Properties:

- ❌ Often EPC rating D or E (high upgrade costs)

- ❌ Higher maintenance requirements

- ❌ Listed building constraints on improvements

- ✅ Character premium supporting rental demand

- ✅ Stronger capital appreciation potential

For investors focused on yield optimization, new build properties present lower regulatory risk in 2026, while period properties may offer superior total returns through capital appreciation despite higher compliance costs.

Practical Surveyor Techniques for Accurate 2026 Valuations

Comparable Evidence Selection in Shifting Markets

RICS valuation standards require comparable evidence from recent market transactions. In 2026's rapidly evolving regulatory environment, selecting appropriate comparables demands enhanced scrutiny:

Essential Comparable Criteria:

- ✓ Transaction date within 6 months (3 months preferred)

- ✓ Same EPC rating or documented upgrade costs

- ✓ Similar tenure type (freehold/leasehold)

- ✓ Comparable location and property characteristics

- ✓ Similar regulatory compliance status

Red Flags for Comparables:

- ✗ Transactions predating Renters' Rights Act implementation

- ✗ Properties sold with deferred maintenance

- ✗ Forced sales or distressed transactions

- ✗ Properties with undisclosed regulatory non-compliance

When conducting a RICS building survey, surveyors should explicitly document EPC ratings and regulatory compliance status to support future valuation evidence.

Risk-Adjusted Valuation Approaches

The regulatory uncertainty surrounding spending caps, exemptions, and enforcement timelines for EPC requirements[2] necessitates risk-adjusted valuation methodologies:

Risk Premium Matrix:

| Risk Factor | Yield Adjustment | Capital Value Impact |

|---|---|---|

| EPC rating E or below | +0.8-1.2% yield | -8-12% value |

| Pending Renters' Rights Act litigation | +0.3-0.5% yield | -3-5% value |

| Uncertain EPC exemption eligibility | +0.5-0.8% yield | -5-8% value |

| Landlord inexperience | +0.4-0.6% yield | -4-6% value |

| Multiple regulatory non-compliance | +1.5-2.0% yield | -15-20% value |

These adjustments reflect the additional return investors require to compensate for regulatory uncertainty and compliance risk.

Documentation and Reporting Standards

Professional valuations for 2026 rental properties must include enhanced documentation:

Essential Valuation Report Components:

-

Executive Summary

- Property address and tenure

- Valuation figure with confidence range

- Key risk factors and assumptions

-

Market Context

- Regional rental inflation trends

- Comparable evidence analysis

- Supply-demand dynamics

-

Regulatory Compliance Assessment

- Current EPC rating and upgrade requirements

- Renters' Rights Act implications

- MTD compliance status

- Outstanding safety certifications

-

Financial Analysis

- Gross yield calculation

- Net yield (basic and higher rate taxpayer scenarios)

- DCF analysis with sensitivity testing

- Tax-adjusted returns

-

Risk Assessment

- Regulatory change exposure

- Market cycle positioning

- Property-specific risks

- Mitigation strategies

-

Valuation Methodology

- Approach selection justification

- Comparable evidence details

- Adjustments applied

- Assumptions and limitations

This comprehensive approach ensures valuations withstand scrutiny from lenders, investors, and regulatory authorities.

Future Outlook: Navigating Uncertainty in 2026 and Beyond

Potential Policy Developments

Several regulatory uncertainties remain unresolved as of March 2026, creating ongoing valuation challenges:

Outstanding Policy Questions:

🔍 EPC Spending Caps:

- Will government impose maximum expenditure limits?

- What exemptions will apply for listed buildings or conservation areas?

- How will enforcement operate for non-compliant properties?

🔍 Renters' Rights Act Implementation:

- How will courts interpret "reasonable" rent increase challenges?

- What evidence standards will apply for possession proceedings?

- Will enforcement resources match legislative ambition?

🔍 Tax Policy Evolution:

- Potential changes to mortgage interest relief restrictions

- Capital Gains Tax rates and allowances

- Stamp Duty Land Tax for additional properties

Surveyors should incorporate scenario planning into valuations, providing ranges that reflect potential policy outcomes rather than single-point estimates.

Market Cycle Positioning

The 2026 rental market occupies an uncertain position in the property cycle:

Indicators of Market Maturity:

- Slowing rental inflation (4.0% to 2.6% forecast)[1][2]

- Accelerating house price growth (2.5%)[1]

- Yield compression across most regions

- Regulatory pressure intensification

Indicators of Continued Strength:

- Persistent homeownership barriers

- Demographic demand from younger cohorts

- Undersupply in many regional markets

- Professional landlord market consolidation

For investors with long-term horizons, current yield compression may represent a strategic entry point, particularly for compliant properties in high-demand locations. Conversely, leveraged investors facing negative cash flow may need to reassess portfolio viability.

Technology and Valuation Innovation

The 2026 regulatory environment accelerates adoption of technology-enabled valuation approaches:

Emerging Tools:

- 🖥️ Automated Valuation Models (AVMs) incorporating regulatory data

- 📊 Real-time rental market analytics platforms

- 🏠 Digital property passports with compliance documentation

- 📱 Tenant demand forecasting using demographic data

Professional surveyors should embrace these technologies while maintaining human judgment for complex regulatory assessments and market interpretation that algorithms cannot replicate.

Conclusion

Valuation Adjustments for 2026 Rental Market Shifts: Impact of Landlord Tax Pressures on UK Yields represent a fundamental recalibration of the UK rental investment landscape. The convergence of slowing rental inflation—down to 4.0% annually with forecasts of just 2.6% for 2026[1][2]—alongside intensifying regulatory pressures creates unprecedented challenges for accurate property valuation.

The triple burden of Making Tax Digital implementation, the Renters' Rights Act, and escalating EPC requirements compresses yields across all property types and regions. With 39% of landlords contemplating market exit[2] and 29% facing EPC upgrade costs exceeding £5,000[2], supply-side contractions may partially offset regulatory headwinds through enhanced rental pricing power.

Key valuation principles for 2026:

✅ Adopt tax-adjusted net yield calculations rather than relying on gross yields that obscure regulatory costs

✅ Incorporate regional variations with North East yields (7.9% rental growth) substantially outperforming London (2.1%)[1]

✅ Apply risk-adjusted methodologies reflecting regulatory uncertainty and compliance costs

✅ Utilize DCF analysis to capture time-value of capital expenditure requirements

✅ Document EPC ratings and upgrade costs as material valuation factors

✅ Consider supply-demand dynamics as potential landlord exits reshape market fundamentals

Actionable Next Steps

For Landlords and Investors:

- Commission professional valuations incorporating 2026 regulatory adjustments before making acquisition or disposal decisions

- Assess EPC upgrade requirements and obtain detailed cost estimates for properties rated D or E

- Model tax-adjusted returns using both basic and higher rate taxpayer scenarios

- Review portfolio composition to identify properties with unfavorable regulatory exposure

- Engage qualified accountants for Making Tax Digital implementation support

For Property Professionals:

- Enhance comparable evidence databases with EPC ratings and regulatory compliance status

- Develop standardized adjustment matrices for common regulatory cost factors

- Implement sensitivity analysis in valuation models to reflect policy uncertainty

- Maintain continuing professional development on evolving rental market regulations

- Collaborate with tax specialists to ensure accurate net yield calculations

For Prospective Buyers:

- Request comprehensive surveys that explicitly address EPC ratings and upgrade costs—consider a Level 2 homebuyer survey for standard properties or Level 3 building survey for older properties

- Obtain independent rental valuations rather than relying on vendor estimates

- Factor regulatory compliance costs into maximum purchase price calculations

- Assess landlord experience requirements against personal capabilities and resources

- Consult with qualified surveyors who understand regional market dynamics

The UK rental market in 2026 rewards informed, professional investors who accurately assess regulatory costs and maintain high compliance standards. While yield compression challenges returns, strategic property selection in high-demand regions with favorable regulatory profiles can still deliver attractive risk-adjusted performance. The key lies in rigorous, RICS-compliant valuation methodologies that capture the full complexity of the modern rental investment landscape.

References

[1] January2026 – https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/privaterentandhousepricesuk/january2026

[2] 2026 Predictions For Landlords – https://www.simplybusiness.co.uk/knowledge/rental/2026-predictions-for-landlords/