Landlord instructions fell by a net balance of -27% in February 2026 — yet tenant demand held steady and rent expectations climbed. That combination creates a deceptively complex valuation environment for buy-to-let (BTL) properties, one where supply constraints flatter rental income projections even as buyer sentiment softens and regulatory headwinds intensify. For surveyors navigating this landscape, the RICS UK Residential Survey February 2026 offers granular data that must sit at the heart of every BTL valuation instruction this quarter.

This article unpacks the key findings from the RICS February 2026 survey, explains how those findings translate into practical valuation methodology for BTL assets, and highlights the regulatory pressures — particularly the Renters' Rights Act — that are reshaping landlord behaviour and, by extension, market supply. Valuing BTL properties amid Q2 2026 market caution: RICS February survey insights for surveyors is not just a headline; it is an active professional challenge requiring updated frameworks and sharper judgement.

Key Takeaways 📌

- Landlord supply is shrinking fast: A net balance of -27% of agents reported fewer landlord instructions, directly tightening rental supply and supporting yield assumptions in BTL valuations [1].

- Tenant demand is stable: A net balance of +2% indicates steady occupier demand, underpinning income reliability for BTL assets [1].

- Rent growth is expected: +20% of respondents anticipate rental price increases over the next three months, strengthening forward-looking yield models [1].

- Buyer sentiment has softened: New buyer enquiries and agreed sales both showed negative net balances in February 2026, signalling caution in the sales market that affects exit strategy assumptions [2].

- Regulatory risk is material: The Renters' Rights Act is accelerating landlord exits, which simultaneously reduces supply and introduces valuation uncertainty around tenancy structures.

Understanding the RICS February 2026 Data Landscape

What the Survey Tells Surveyors About BTL Market Conditions

The RICS UK Residential Market Survey for February 2026 paints a picture of a market caught between structural supply constraints and cautious buyer sentiment [2]. For BTL-focused surveyors, this duality demands careful disaggregation: the sales market and the rental market are moving in different directions, and conflating them leads to valuation error.

On the sales side, new buyer enquiries registered a negative net balance, and near-term price expectations remained subdued in many regions. Capital Economics noted that the February 2026 RICS data pointed to continued hesitancy among purchasers, with affordability pressures and mortgage rate uncertainty weighing on transaction volumes [3]. This matters for BTL valuations because the exit strategy — the ability to sell a tenanted or vacant property at a reasonable capital value — is a core component of investment worth.

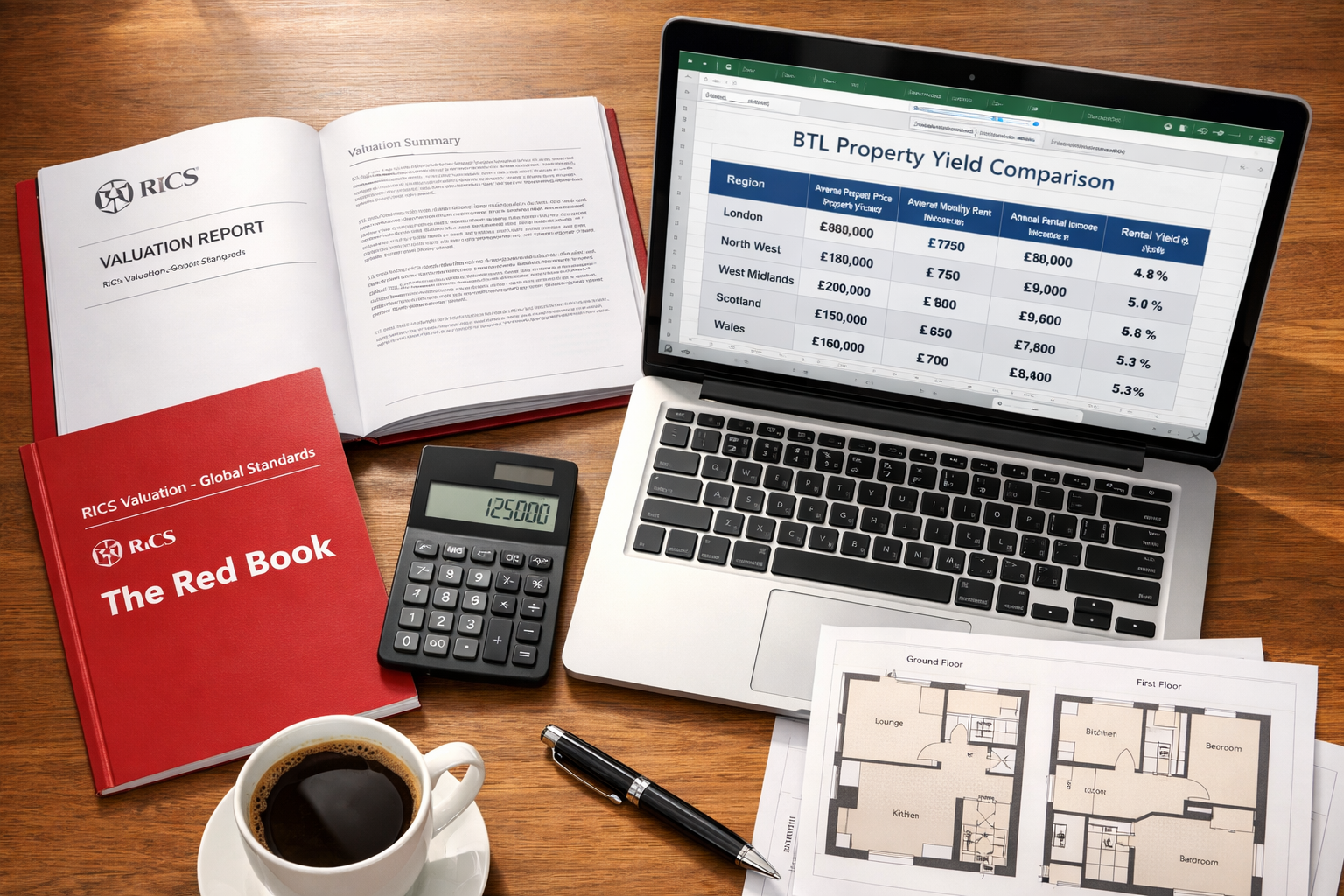

On the rental side, the picture is more constructive:

| Indicator | Net Balance (Feb 2026) | Implication for BTL Valuation |

|---|---|---|

| Landlord instructions | -27% | Reduced supply supports yield assumptions |

| Tenant demand | +2% | Stable occupier base reduces void risk |

| 3-month rent expectations | +20% | Positive rental growth trajectory |

| CBRE rental value index | +3% vs Jan 2025 | Sustained appreciation in rental values [4] |

💡 Pull Quote: "A net balance of -27% reporting fewer landlord instructions is not just a supply statistic — it is a yield-support mechanism that surveyors must weight appropriately in BTL income models."

The CBRE composite rental value index, cited in the RICS UK Economy & Property Market Update for February 2026, showed a 3% gain compared to the beginning of 2025 [4]. This sustained appreciation provides a credible evidence base for rental growth assumptions in discounted cash flow (DCF) models and income capitalisation approaches.

Buyer Demand Softness and Its Effect on BTL Capital Values

Softening buyer demand has a direct read-across to BTL capital values, particularly for properties that are dual-purpose — attractive to both owner-occupiers and investors. When the owner-occupier pool shrinks, BTL vendors face a narrower buyer universe, which can compress achievable sale prices.

Surveyors should note that this compression is not uniform. Properties in high-demand rental corridors — typically urban centres, university towns, and transport hubs — retain stronger investor appetite even when general buyer sentiment weakens. Regional divergence in price expectations, as highlighted in related RICS analysis [5], means that a blanket discount for market caution is methodologically unsound. Location-specific comparable evidence remains paramount.

Practical Valuation Tactics for BTL Properties in a Cautious Q2 2026 Market

Applying RICS Red Book Standards to BTL Instructions

Every formal BTL valuation instruction in 2026 must comply with the RICS Valuation — Global Standards (the Red Book). This is non-negotiable for RICS valuations used for mortgage, tax, or legal purposes. The Red Book's Market Value definition — the estimated amount for which an asset should exchange on the date of valuation between a willing buyer and a willing seller — requires surveyors to reflect current market conditions, not aspirational ones.

In a cautious market, this means:

- Comparable selection must be recent: Use sales evidence from Q4 2025 and Q1 2026 where available. Older comparables may overstate values in a softening market.

- Yield-based cross-checks are essential: For investment properties, a yield-based approach (gross and net initial yield) should corroborate the comparable evidence method. The RICS February 2026 data supports rental income assumptions, but surveyors must stress-test these against void periods and management costs.

- Tenancy structure affects value: An assured shorthold tenancy (AST) at market rent is typically value-neutral. However, with the Renters' Rights Act removing the ability to serve no-fault evictions under Section 21, the tenancy structure now carries greater risk weight. Surveyors should consider whether a sitting tenant — previously a minor discount factor — now warrants a more material adjustment.

Understanding what a chartered surveyor does in this context is important: the role extends beyond measurement and inspection to include market analysis, risk assessment, and defensible professional judgement.

Rental Yield Modelling in Light of February 2026 Data

With a net balance of +20% expecting rents to rise over the coming three months [1], surveyors have reasonable grounds to apply modest rental growth assumptions in forward-looking income models. However, caution is warranted:

Gross yield calculation remains the starting point:

Gross Yield (%) = (Annual Rent / Property Value) × 100

Net yield — which lenders and sophisticated investors prioritise — requires deductions for:

- 🏠 Management fees (typically 8–12% of rent)

- 🔧 Maintenance and repair allowances

- 📅 Void periods (even in a tight market, allow 2–4 weeks per annum)

- 📋 Regulatory compliance costs (EPC upgrades, licensing fees)

- ⚖️ Renters' Rights Act compliance costs

The CBRE rental value index growth of 3% since early 2025 [4] provides a useful benchmark for rental growth assumptions, but surveyors should not extrapolate this linearly. Regional variation is significant, and properties in areas with high landlord exit rates may see sharper near-term rental increases followed by demand-side corrections.

Adjusting for Renters' Rights Act Risk

The Renters' Rights Act represents the most significant structural shift in the BTL market since the introduction of Section 21 itself. Its key implications for BTL valuation include:

-

Increased landlord exit pressure: The -27% net balance in landlord instructions [1] is partly attributable to landlords exiting ahead of or in response to the Act. This reduces supply but also signals that some properties coming to market are distressed sales, which can skew comparable evidence downward.

-

Tenancy security and value: Properties with long-term, reliable tenants may now command a premium from investors seeking income security. Conversely, properties where vacant possession is desired (e.g., for refurbishment or owner-occupation) face a more complex disposal route.

-

Licensing and compliance: Houses in Multiple Occupation (HMOs) and properties in selective licensing areas carry additional compliance burdens. A thorough house survey checklist should include verification of current licensing status and any outstanding enforcement notices.

Structural and Physical Inspection Considerations for BTL Valuations

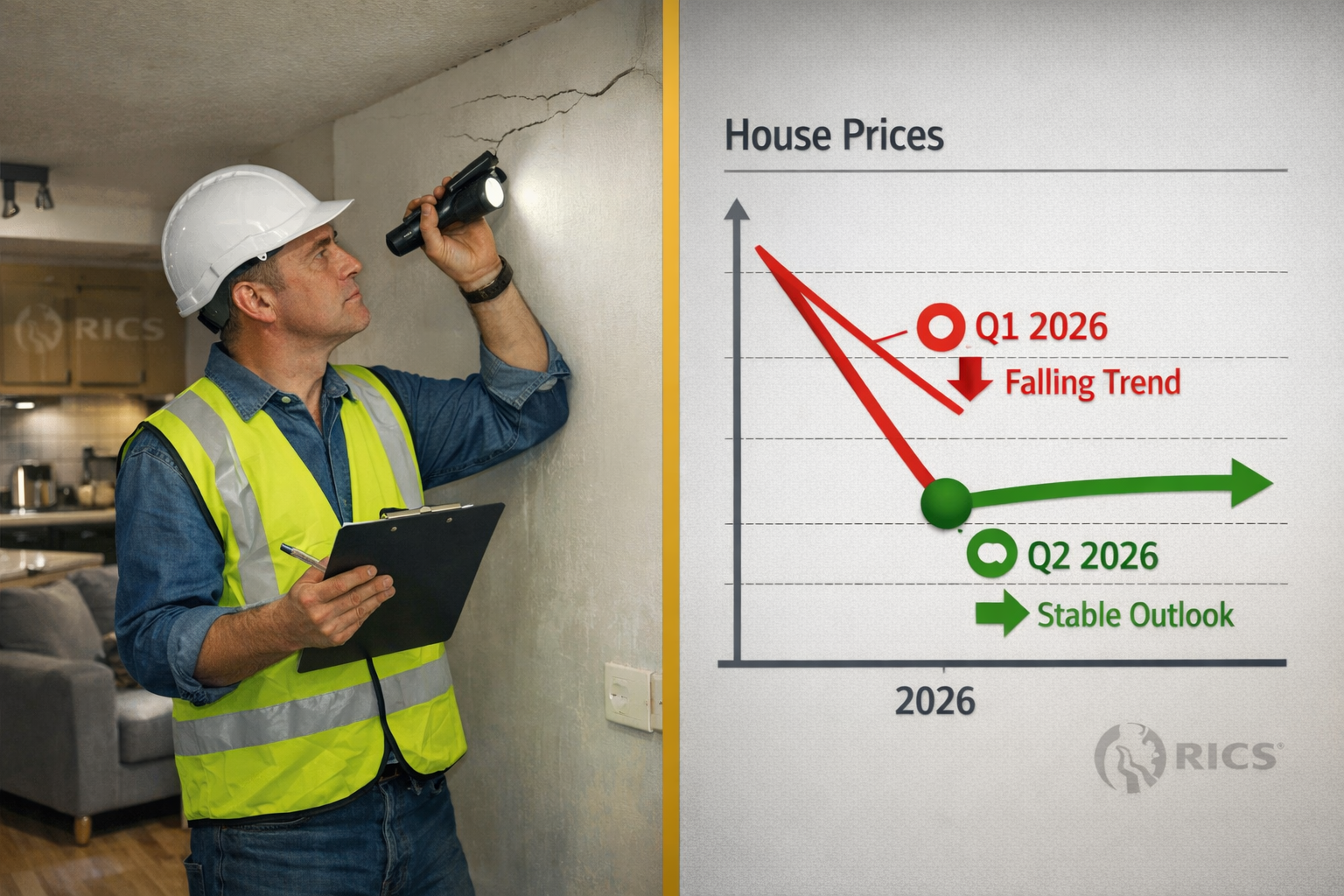

Why Physical Condition Matters More in a Cautious Market

In a buoyant market, buyers and investors sometimes overlook physical defects in the race to transact. In a cautious Q2 2026 market, lenders and investors are scrutinising properties more carefully. For surveyors, this means that the physical inspection component of a BTL valuation carries greater weight in determining final opinion of value.

Key areas requiring particular attention in BTL properties include:

- EPC rating: Proposed minimum EPC standards for rental properties (targeting EPC C) mean that properties rated D or below carry a latent capital expenditure risk. This should be reflected in the valuation through a deduction for estimated improvement costs.

- Roof condition: Deferred maintenance is common in investment properties. A roof survey may be warranted where visual inspection reveals concerns.

- Subsidence indicators: Older terraced properties common in BTL portfolios are susceptible to subsidence, particularly in clay-rich areas. Surveyors should be alert to crack patterns and door/window distortion. Specialist subsidence surveys provide the evidence base for any value adjustments.

- Non-standard construction: Many BTL properties, particularly ex-local authority stock, may be of non-standard construction. This affects mortgageability and, therefore, the pool of potential buyers — a material consideration for market value. Learn more about non-standard construction implications for valuations.

Stock Condition and Portfolio Valuations

For landlords with multiple BTL properties, a stock condition survey provides a systematic assessment of the physical condition of a portfolio. In a market where regulatory compliance costs are rising and maintenance liabilities are increasingly scrutinised by lenders, this type of survey is becoming a standard pre-valuation step for portfolio instructions.

Surveyors instructed on portfolio BTL valuations should ensure that:

- Each property is assessed individually against current market evidence

- Portfolio discounts (where applied) are justified by reference to marketability and liquidity, not applied as a blanket percentage

- Compliance status (licensing, EPC, gas/electrical safety) is documented and any remediation costs are reflected in the valuation

Regional Considerations and Market Divergence in Q2 2026

Why Location Remains the Dominant Value Driver

The RICS February 2026 data does not tell a single national story. Price expectations, transaction volumes, and rental demand vary significantly by region [5]. Surveyors operating in different markets must calibrate their valuation assumptions accordingly.

Key regional dynamics in Q2 2026:

- London and South East: Buyer demand softness is more pronounced due to affordability constraints, but rental demand remains robust. The chartered surveyors in West London market, for example, continues to see strong rental competition despite muted sales activity.

- Northern England and Midlands: Higher gross yields attract investor interest, but capital growth assumptions should be more conservative given weaker price expectation data.

- University cities: Tenant demand is structurally strong, supporting HMO and student BTL valuations, though licensing complexity adds a layer of risk.

For surveyors working across multiple regions, accessing localised comparable evidence and staying current with regional RICS data releases is essential. Those based in areas like North London or South East London will find the February 2026 survey data particularly relevant given the concentration of BTL stock in these areas.

Reinstatement Cost Valuations for BTL Landlords

Alongside market value, many BTL landlords require reinstatement cost valuations for insurance purposes. In a period of sustained construction cost inflation, historic reinstatement figures are frequently inadequate. Surveyors should ensure that reinstatement cost assessments are updated regularly — at least every three years — and that they reflect current BCIS data and any property-specific features (e.g., listed status, non-standard materials).

Conclusion: Actionable Steps for Surveyors Valuing BTL Properties in Q2 2026

Valuing BTL properties amid Q2 2026 market caution: RICS February survey insights for surveyors requires a dual-track approach — rigorous engagement with rental market fundamentals on one side, and careful calibration of capital value assumptions against softening buyer sentiment on the other.

The RICS February 2026 data is clear: rental supply is constrained (-27% landlord instructions), demand is stable (+2% tenant demand), and rents are expected to rise (+20% three-month expectation) [1]. These are genuine supports for BTL income valuations. But they exist alongside a sales market characterised by caution, where exit strategy assumptions must be stress-tested and Renters' Rights Act risks must be explicitly addressed.

✅ Actionable Next Steps for Surveyors

- Update comparable databases: Ensure sales and rental evidence is drawn from Q4 2025 and Q1/Q2 2026 to reflect current conditions accurately.

- Apply dual methodology: Use both comparable evidence and yield-based approaches on every BTL instruction, cross-checking the two outputs.

- Quantify regulatory risk: Explicitly address Renters' Rights Act implications — tenancy structure, licensing status, and EPC compliance — in every valuation report.

- Conduct thorough physical inspections: In a cautious market, physical condition and latent defect risk carry greater weight. Do not underestimate the value impact of deferred maintenance or below-threshold EPC ratings.

- Engage with regional data: Do not apply national averages to local markets. Use RICS regional breakdowns and local comparable evidence to calibrate assumptions.

- Review reinstatement costs: Ensure insurance valuations for BTL clients are current and reflect construction cost inflation.

- Stay current with RICS guidance: The February 2026 survey [2] and economy update [4] should be reviewed alongside Red Book standards for every formal BTL instruction.

The surveyors who navigate Q2 2026 most effectively will be those who treat market caution not as a reason to defer judgement, but as a prompt to sharpen it.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] UK RICS Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[4] UK Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf

[5] Valuation Impacts of February 2026 RICS Survey: Strategies for Regional Price Divergence in UK Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets