The UK property market has entered a period of stark regional divergence, with the February 2026 RICS Residential Market Survey revealing a dramatic split between northern resilience and southern decline. While national headline prices hover near flat territory with a net balance of -12%, the underlying regional dynamics tell a far more complex story—one that demands sophisticated valuation strategies and nuanced market understanding from surveyors, investors, and property professionals navigating these turbulent waters.

The Valuation Impacts of February 2026 RICS Survey: Strategies for Regional Price Divergence in UK Markets present both challenges and opportunities for those equipped to interpret the data correctly. London's valuation headwinds have intensified to unprecedented levels, while northern regions continue their upward trajectory, creating a two-speed market that requires fundamentally different approaches to property assessment, pricing strategy, and risk management.

Key Takeaways

- 📉 National prices show downward momentum with a net balance of -12% in February 2026, worsening from -10% in January, signaling flat to marginally negative pricing trends

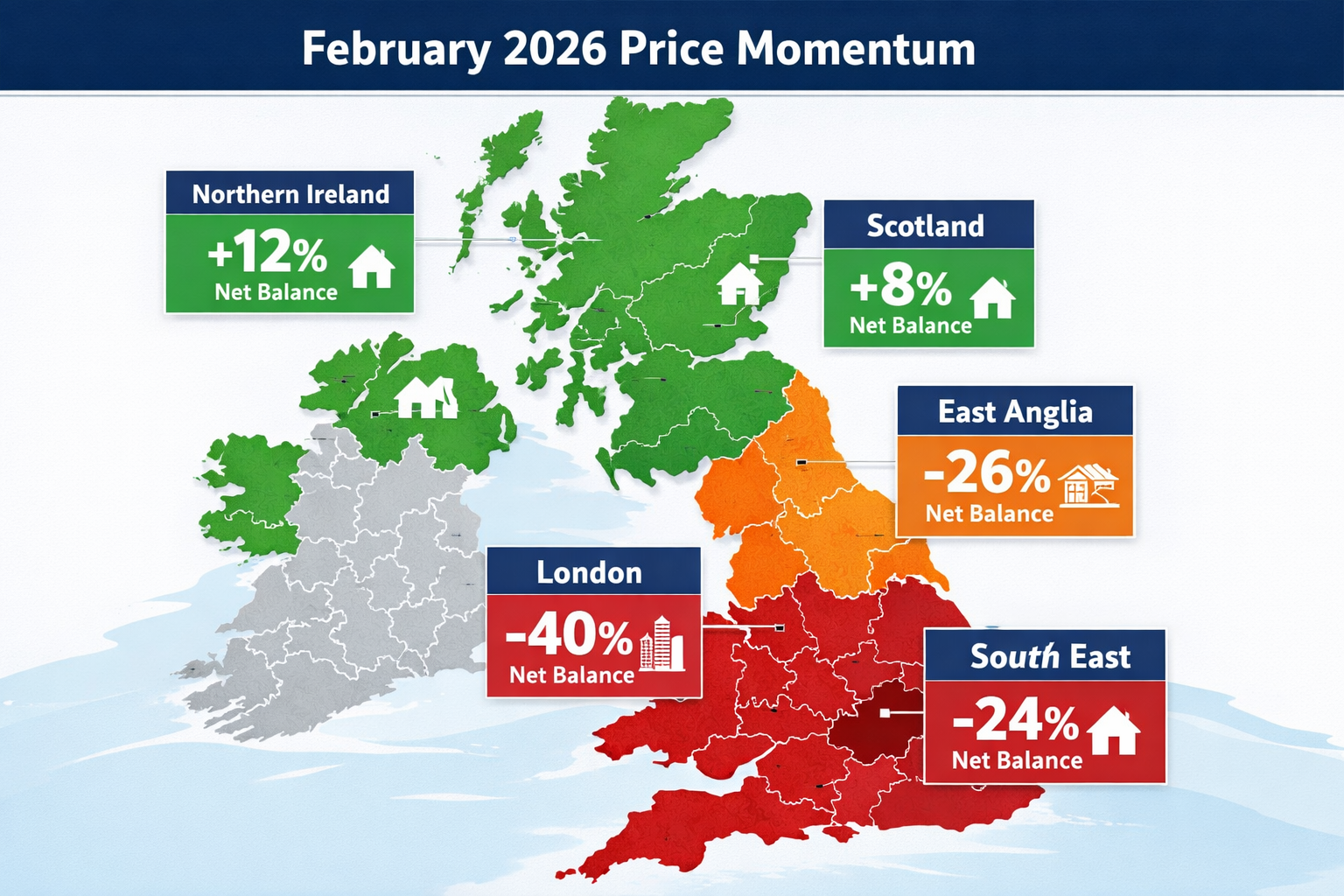

- 🏙️ London faces severe valuation pressure with a -40% net balance and 12-month expectations collapsing from +56% to just +7%, representing the most dramatic regional weakness

- 🌍 Geographic split intensifies as Northern Ireland, Scotland, and North West England maintain price growth while South East (-24%) and East Anglia (-26%) experience concentrated declines

- 📊 Buyer demand destabilized with enquiries posting -26% net balance, driven by geopolitical concerns and transaction volumes tracking 9% below 2025 levels

- 🎯 Strategic valuation approaches required with region-specific methodologies, enhanced risk assessment protocols, and adaptive pricing strategies essential for accurate property assessment

Understanding the February 2026 RICS Survey Data: National Overview

The Royal Institution of Chartered Surveyors (RICS) February 2026 Residential Market Survey has captured a critical inflection point in UK property markets. The headline price momentum declined significantly, with the net balance falling to -12% from -10% in January, indicating that more surveyors are reporting price decreases than increases across their local markets.[1]

This deterioration extends beyond simple pricing metrics. Buyer enquiry activity has destabilized materially, posting a net balance of -26% in February 2026—a substantial worsening from -15% in January. The escalation of Middle East conflict has been cited as a key factor dampening buyer sentiment, creating uncertainty that ripples through transaction volumes and valuation confidence.[1][2]

Transaction Momentum and Market Velocity

The agreed sales measure posted a -12% net balance in February 2026, representing material weakening from -9% previously. More concerning for market participants, transaction growth has plunged from 1.3% to approximately -15% on a three-month basis, indicating a sharp deceleration in market velocity.[1][3]

Transaction volumes are now tracking 9% below the strong start seen in 2025, with buyer confidence described as "cautious" across multiple regions. This constraint in activity levels has particular implications for valuation factors that depend on comparable sales data and market liquidity.[2]

Near-Term vs. Long-Term Price Expectations

A critical divergence has emerged between short-term and long-term price expectations:

| Time Horizon | Net Balance (Feb 2026) | Net Balance (Jan 2026) | Change |

|---|---|---|---|

| 3-Month Outlook | -18% | -6% | ↓ -12 points |

| 12-Month Outlook | +33% | +43% | ↓ -10 points |

Short-term headline price expectations fell sharply to -18% net balance in February 2026, down from -6% in January, signaling renewed caution over the coming three months. However, twelve-month price recovery expectations remain moderately positive at +33%, though tempered from the previous month's +43%.[1]

This divergence suggests that while professionals anticipate near-term headwinds, the underlying structural factors—including constrained supply and demographic demand—are expected to support modest price appreciation over the medium term.

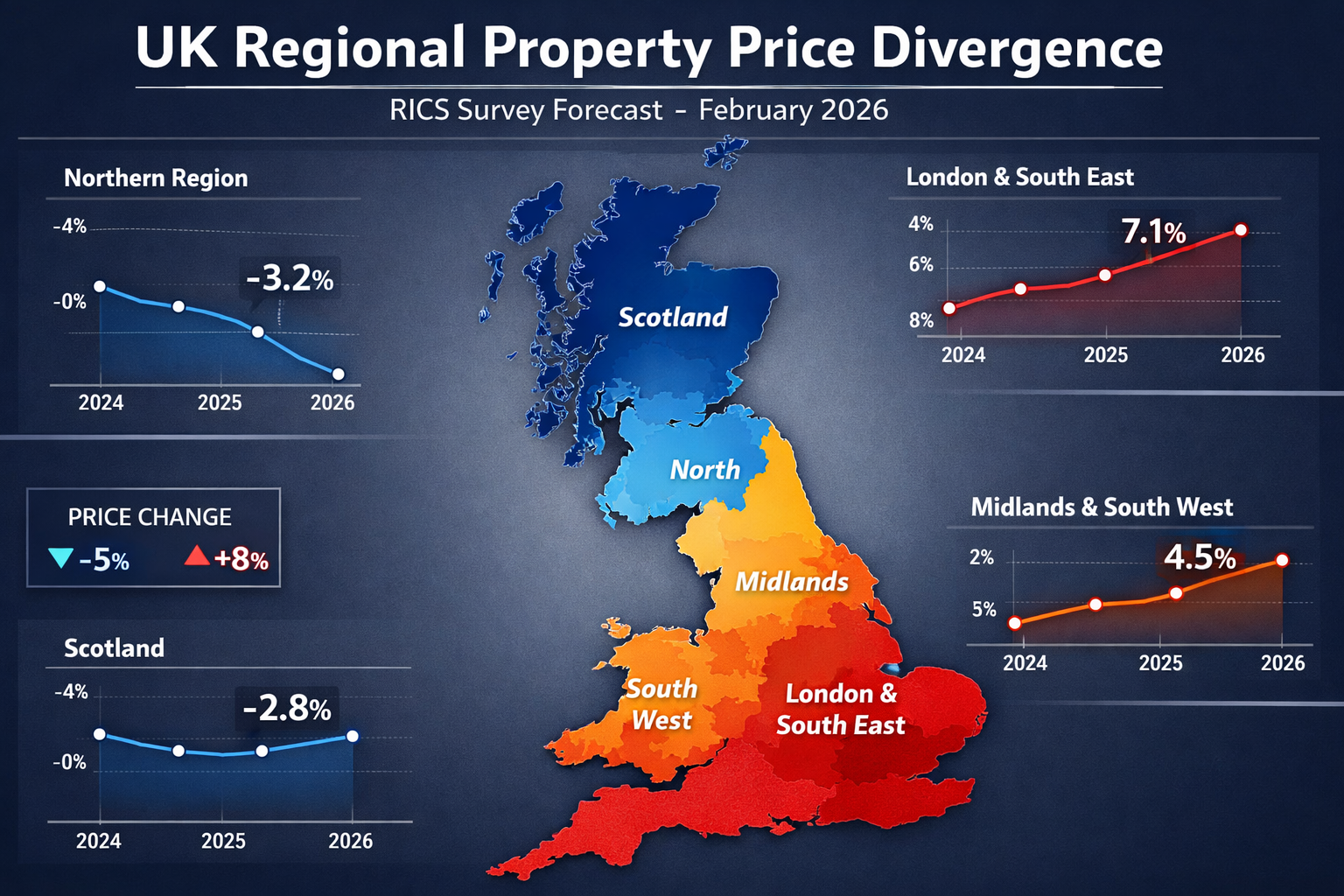

Regional Price Divergence: Analyzing the Valuation Impacts of February 2026 RICS Survey

The most striking feature of the February 2026 RICS data is the profound regional divergence in price momentum, transaction activity, and valuation outlook. This geographic split demands region-specific valuation strategies rather than one-size-fits-all approaches.

London: Unprecedented Valuation Headwinds

London has emerged as the epicenter of valuation pressure, recording a net balance of -40% for price momentum in February 2026—the most pronounced regional weakness in the survey. Even more dramatic is the collapse in 12-month price expectations, which plummeted from +56% in January to just +7% in February.[1]

This represents a fundamental reassessment of London's near-term prospects. Several factors contribute to this weakness:

- Affordability constraints reaching critical levels after years of price growth

- Stamp duty implications affecting higher-value transactions disproportionately

- Economic uncertainty concentrated in financial services and professional sectors

- Outmigration trends continuing from the pandemic period

For surveyors conducting RICS home surveys in the capital, these conditions necessitate conservative valuation approaches, enhanced scrutiny of comparable evidence, and explicit discussion of market uncertainty with clients. Chartered surveyors in Chelsea, Camden, and Central London must adapt their methodologies to reflect this challenging environment.

South East and East Anglia: Concentrated Downward Pressure

The South East posted -24% and East Anglia -26% net balance for price declines, significantly exceeding the national average. These regions, which include commuter belt areas in Hertfordshire, Essex, and Berkshire, face particular challenges.[1]

The concentrated valuation pressure in southeastern markets reflects:

✅ Affordability ceiling effects as prices reached unsustainable multiples of local incomes

✅ Interest rate sensitivity with higher average mortgage sizes amplifying payment impacts

✅ Reduced London premium as hybrid working diminishes commuter location advantages

✅ Supply-demand rebalancing after pandemic-era migration surge

Professionals conducting valuations in areas like St Albans, Hemel Hempstead, and surrounding Home Counties must incorporate these regional headwinds into their assessments, particularly for capital gains tax valuation and probate valuation purposes where accuracy is paramount.

Northern Regions and Scotland: Resilience and Growth

In stark contrast, Northern Ireland, Scotland, and the North West of England continue to see rising prices, offering a completely different valuation landscape. These regions benefit from:

🏡 Relative affordability maintaining accessibility for first-time buyers and upgraders

🏡 Economic diversification with less concentration in vulnerable sectors

🏡 Infrastructure investment supporting long-term growth prospects

🏡 Demographic tailwinds including internal migration from higher-cost regions

This resilience creates distinct opportunities for investors and requires different valuation approaches that recognize continued growth potential rather than defensive positioning. The regional contrast underscores the importance of local market knowledge and the limitations of national-level analysis for property-specific decisions.

Strategic Valuation Approaches for Navigating Regional Divergence

The Valuation Impacts of February 2026 RICS Survey: Strategies for Regional Price Divergence in UK Markets demand sophisticated, adaptive approaches from property professionals. Generic valuation methodologies fail to capture the nuanced realities of today's fragmented market.

Region-Specific Valuation Methodologies

For London and South East Markets:

Professional valuers must adopt conservative comparable selection criteria, prioritizing recent transactions (within 3 months) and applying downward adjustments where market evidence suggests weakening momentum. Time adjustments should reflect the -40% net balance reality in London, with explicit consideration of:

- Transaction velocity changes affecting liquidity premiums

- Buyer negotiating leverage in slower markets

- Increased time on market impacting vendor expectations

- Potential for further near-term softening

For Northern and Scottish Markets:

Conversely, valuations in resilient regions should recognize continued growth trajectories while avoiding over-exuberance. Appropriate strategies include:

- Positive time adjustments reflecting ongoing price appreciation

- Recognition of supply constraints supporting values

- Consideration of infrastructure and economic development catalysts

- Balanced assessment of sustainability of current growth rates

Enhanced Risk Assessment Protocols

Given the heightened uncertainty reflected in the February 2026 data, valuers should implement enhanced risk disclosure frameworks that explicitly address:

- Market volatility indicators – documenting the -26% buyer enquiry decline and its implications

- Geopolitical factors – acknowledging Middle East conflict impacts on sentiment[2][3]

- Interest rate sensitivity – modeling valuation implications of potential rate movements

- Regional divergence risks – highlighting geographic concentration effects

For lease extension valuations and insurance reinstatement valuations, these risk factors require explicit consideration in methodology and reporting.

Adaptive Pricing Strategies for Different Market Conditions

In Declining Markets (London, South East, East Anglia):

Pricing strategies must acknowledge buyer leverage and reduced competition:

- Competitive positioning below recent comparables to attract limited buyer pool

- Flexibility provisions allowing for negotiation within realistic ranges

- Transparent disclosure of market conditions to manage vendor expectations

- Strategic timing considerations for discretionary transactions

In Growing Markets (Northern regions, Scotland):

Pricing can be more assertive while maintaining credibility:

- Premium positioning for exceptional properties in supply-constrained areas

- Growth trajectory incorporation in forward-looking valuations

- Scarcity value recognition where appropriate

- Market momentum leverage in negotiation contexts

Leveraging Technology and Data Analytics

Modern valuation practice increasingly relies on sophisticated data analytics to navigate complex market conditions. Professionals should leverage:

📊 Automated valuation models (AVMs) as cross-checks against traditional methods

📊 Real-time market monitoring platforms tracking listing and transaction trends

📊 Geographic information systems (GIS) for micro-market analysis

📊 Predictive analytics incorporating multiple data sources beyond simple comparables

These tools complement rather than replace professional judgment, particularly when chartered surveyors must reconcile conflicting market signals or assess unique properties without close comparables.

Supply Dynamics and Their Valuation Implications

While demand-side factors dominate headlines, supply dynamics remain critical to understanding valuation trajectories. The February 2026 RICS data shows the new instructions gauge posted a net balance of +2%, indicating broadly stable supply conditions despite demand weakness.[1]

This supply-demand imbalance has important implications:

Limited Supply Supporting Price Floors

The absence of forced selling or significant inventory increases provides a floor under prices even in weakening markets. Vendors who don't need to sell can simply withdraw from the market rather than accept material discounts, limiting downside price momentum.

For valuers, this suggests:

- Downward price adjustments should be measured rather than dramatic

- Transaction evidence may understate true market values as distressed sales are limited

- Time on market becomes a more important indicator than simple price reductions

Regional Supply Variations

Supply constraints vary significantly by region, with northern markets experiencing tighter inventory than southern counterparts. This contributes to the regional divergence, as limited supply in growing markets amplifies upward price pressure while adequate supply in declining markets facilitates buyer negotiation leverage.

Surveyors conducting RICS specific defect surveys or commercial building surveys must consider local supply dynamics when assessing investment value and marketability.

Interest Rate Environment and Mortgage Market Impacts

While not explicitly detailed in the February 2026 RICS survey, the broader interest rate environment significantly influences the valuation impacts observed in the data. Buyer affordability remains constrained by elevated borrowing costs, which disproportionately affect higher-value markets like London and the South East.

Affordability Calculations in Valuation Context

Professional valuers should incorporate affordability analysis into their market assessments, particularly for residential properties. Key considerations include:

- Average income-to-price ratios in the local market

- Typical mortgage terms and loan-to-value ratios for target buyer demographics

- Monthly payment implications at current interest rates

- Comparison to rental equivalents affecting buy-versus-rent decisions

This analysis helps explain why regions with lower absolute prices maintain stronger momentum—they remain accessible to a broader buyer pool despite elevated interest rates.

Mortgage Availability and Lending Standards

Beyond interest rates, mortgage availability and lending criteria affect market dynamics. Tighter lending standards or reduced product availability can constrain demand independent of price levels, requiring valuers to consider:

- Typical loan-to-value ratios achievable for the property type

- Lender appetite for specific geographic areas or property characteristics

- Impact of mortgage market conditions on buyer pool size

- Alternative financing routes (cash buyers, portfolio landlords) and their market share

Transaction Volume Trends and Liquidity Considerations

The 9% decline in transaction volumes relative to the strong 2025 start has significant implications for valuation practice.[2] Reduced liquidity affects both the availability of comparable evidence and the fundamental marketability of properties.

Comparable Evidence Challenges

Lower transaction volumes create data scarcity issues for valuers relying on comparable sales methodology:

- Fewer recent transactions available for analysis

- Increased time gaps between comparables requiring larger time adjustments

- Greater variability in transaction characteristics requiring more subjective adjustments

- Reduced confidence in statistical measures of central tendency

Professional standards require valuers to acknowledge these limitations explicitly in their reports, particularly for formal valuations used in litigation, taxation, or financing contexts.

Marketability and Liquidity Premiums

Reduced transaction velocity affects marketability assessments, which should be reflected in valuation approaches:

- Extended marketing periods required to achieve optimal prices

- Greater uncertainty in price realization for forced or time-constrained sales

- Liquidity discounts appropriate for properties with limited buyer pools

- Recognition that "market value" assumes reasonable marketing time, which varies by market conditions

For expert witness reports or dispute resolution contexts, these liquidity considerations often become central to valuation disagreements.

Geopolitical and Economic Uncertainty Factors

The February 2026 RICS survey explicitly cites escalation of Middle East conflict as a factor dampening buyer sentiment.[1][2] This highlights how external shocks can rapidly alter market dynamics independent of fundamental housing market factors.

Incorporating Uncertainty into Valuation Practice

Professional valuers must balance precision with acknowledgment of uncertainty:

"In periods of heightened geopolitical or economic uncertainty, valuation confidence intervals widen significantly. Professional practice requires explicit discussion of these limitations rather than false precision in point estimates."

Appropriate approaches include:

✔️ Scenario analysis presenting valuations under different market trajectory assumptions

✔️ Confidence ranges rather than single-point estimates where appropriate

✔️ Explicit assumption documentation allowing users to understand valuation basis

✔️ Regular revaluation recommendations in rapidly changing markets

Economic Indicators Beyond Housing Data

Comprehensive valuation practice considers broader economic indicators that influence housing markets:

- Employment trends and wage growth in the local area

- Business investment and economic development projects

- Consumer confidence indices

- Inflation trajectories affecting real asset values

- Government policy changes affecting housing taxation or regulation

These factors provide context for the RICS survey data and help distinguish temporary disruptions from structural shifts requiring fundamental valuation approach changes.

Practical Strategies for Surveyors and Property Professionals

For professionals navigating the Valuation Impacts of February 2026 RICS Survey: Strategies for Regional Price Divergence in UK Markets, several practical strategies enhance service delivery and client outcomes:

Client Communication and Expectation Management

Transparent communication about market conditions builds trust and reduces disputes:

- Present RICS survey data and regional trends in accessible formats

- Explain methodology choices and their rationale given market conditions

- Discuss uncertainty explicitly rather than projecting false confidence

- Provide context for how current conditions compare to historical patterns

For professionals offering services from North West London to Fulham, Hammersmith, and beyond, local market expertise combined with transparent communication creates competitive advantage.

Continuing Professional Development

The rapidly evolving market environment demands ongoing education in:

- Advanced statistical techniques for sparse data environments

- Technology tools for market analysis and valuation support

- Regional market dynamics and micro-market analysis

- Regulatory changes affecting valuation practice

- Economic and geopolitical factors influencing property markets

Professional bodies including RICS provide resources and training to support members in maintaining cutting-edge expertise.

Diversification and Specialization Balance

Surveyors should balance geographic and service diversification with deep specialization:

- Maintain expertise across multiple regions to capture opportunities where they emerge

- Develop specialized knowledge in particular property types or valuation purposes

- Build networks across regions to support referral relationships

- Invest in technology enabling efficient service delivery across broader geographic areas

This balanced approach provides resilience during regional market divergences like those evident in the February 2026 data.

Quality Assurance and Professional Standards

Heightened market uncertainty increases the importance of rigorous quality assurance:

- Peer review of valuations in complex or uncertain markets

- Systematic documentation of methodology and assumption choices

- Regular calibration against market outcomes to identify systematic biases

- Compliance with professional standards and regulatory requirements

These practices protect both clients and professionals while maintaining the integrity of the valuation profession.

Future Outlook and Emerging Trends

While the February 2026 RICS survey captures current conditions, forward-looking professionals must anticipate emerging trends that will shape future valuation practice:

Technology Disruption in Valuation

Artificial intelligence and machine learning continue advancing, with implications for:

- Automated valuation accuracy improving in data-rich markets

- Enhanced ability to identify micro-market trends and anomalies

- Real-time market monitoring replacing periodic survey-based insights

- Integration of non-traditional data sources (satellite imagery, social media sentiment)

Professional valuers who embrace these tools while maintaining critical judgment will thrive in evolving markets.

Climate and Sustainability Considerations

Environmental factors increasingly influence property values:

- Energy performance ratings affecting marketability and regulatory compliance

- Flood risk and climate adaptation requirements

- Sustainability credentials commanding price premiums in certain segments

- Retrofit costs and opportunities affecting net valuation positions

These considerations require integration into mainstream valuation practice rather than treatment as niche specializations.

Demographic and Social Shifts

Long-term demographic trends continue reshaping housing demand:

- Aging population affecting property type preferences

- Household formation patterns influencing location choices

- Work-from-home normalization altering location value hierarchies

- Generational wealth transfer creating new buyer cohorts

Understanding these structural shifts helps distinguish cyclical market movements from permanent changes requiring valuation methodology adaptation.

Conclusion

The Valuation Impacts of February 2026 RICS Survey: Strategies for Regional Price Divergence in UK Markets present both significant challenges and opportunities for property professionals. The data reveals a market characterized by stark regional divergence, with London and southeastern markets experiencing substantial downward pressure while northern regions and Scotland maintain resilience and growth.

Key findings from the February 2026 survey include:

📌 National price momentum declining to -12% net balance, with near-term expectations turning notably negative at -18%

📌 London facing unprecedented valuation headwinds with -40% price pressure and collapsed 12-month expectations

📌 South East and East Anglia experiencing concentrated downward pressure at -24% and -26% respectively

📌 Northern regions and Scotland maintaining positive price growth, creating a two-speed market

📌 Buyer demand destabilized by geopolitical concerns, with enquiries posting -26% net balance

📌 Transaction volumes tracking 9% below strong 2025 levels, affecting market liquidity

These conditions demand sophisticated, region-specific valuation strategies rather than one-size-fits-all approaches. Professional surveyors must adapt their methodologies to reflect local market realities, implement enhanced risk assessment protocols, and communicate uncertainty transparently to clients.

Actionable Next Steps

For property professionals navigating these challenging conditions:

- Review and update valuation methodologies to reflect current regional divergence and market uncertainty

- Enhance data analytics capabilities through technology investment and professional development

- Strengthen client communication around market conditions, methodology choices, and valuation limitations

- Develop region-specific expertise recognizing the limitations of national-level analysis

- Implement rigorous quality assurance processes to maintain professional standards during uncertain periods

- Monitor emerging trends in technology, sustainability, and demographics that will shape future practice

The February 2026 RICS survey provides invaluable insights into current market conditions, but professional success requires ongoing vigilance, adaptation, and commitment to excellence in valuation practice. Those who embrace these challenges while maintaining rigorous professional standards will not only navigate current market complexity but position themselves for long-term success as market conditions inevitably evolve.

For property owners, investors, and professionals requiring expert valuation services that account for these complex regional dynamics, engaging qualified chartered surveyors with deep local market knowledge and sophisticated analytical capabilities remains essential to making informed property decisions in 2026's challenging market environment.

References

[1] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[2] UK Residential Market Survey February 2026 – https://www.navah-consulting.co.uk/news/uk-residential-market-survey-february-2026

[3] UK RICS Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[4] UK Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf