The UK residential property market recorded a net price balance of -10% in January 2026 — a figure that, on the surface, suggests broad weakness. Dig beneath that headline, however, and a far more complex picture emerges: Scotland and Northern Ireland are posting consistent price growth, while London and the South East continue to drag the national average downward [1]. For surveyors and valuers operating across this fractured landscape, applying a single national lens to property assessment is no longer defensible practice.

This article examines Valuation Strategies for Regional Price Flatness in Spring 2026: RICS Data for Divergent UK Markets, offering a structured framework for professionals who must navigate a market where postcode geography now dictates pricing reality more than any macro trend.

Key Takeaways 📌

- National price stabilization masks deep regional splits — Scotland and the North outperform while London and the South lag significantly.

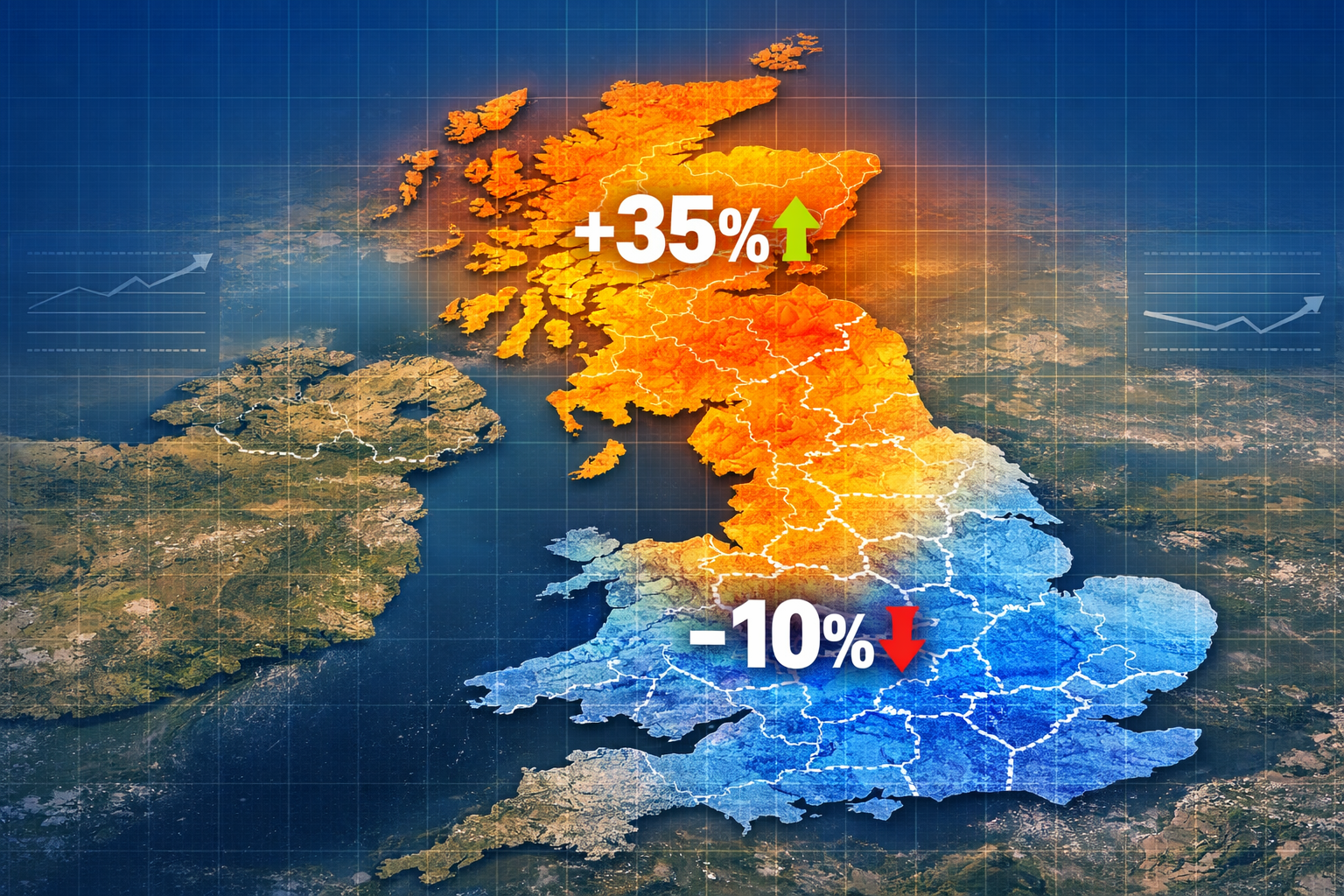

- RICS January 2026 data shows improving but still negative national sentiment, with a net balance of -10%, up from -19% in October 2025.

- 12-month forward sentiment surged to +35%, signalling medium-term optimism even where near-term conditions remain flat.

- Surveyors must apply region-specific valuation adjustments rather than relying on national indices alone.

- Comparable evidence selection, weighting, and market commentary within RICS Red Book reports must reflect local divergence explicitly.

Understanding the RICS Data: A Market Divided in Spring 2026

The National Picture Is Misleading

The RICS UK Residential Market Survey for January 2026 tells a story of cautious recovery at the aggregate level [1][6]. The net balance for house prices over the prior three months stood at -10%, a meaningful improvement from the -19% trough recorded in October 2025. New buyer enquiries rose for the fourth consecutive month, and agreed sales showed modest positive momentum.

Yet these national averages obscure more than they reveal. When regional breakdowns are examined, the divergence is striking:

| Region | Price Trend (Jan 2026) | Direction |

|---|---|---|

| Scotland | Positive growth | ⬆️ Strong |

| Northern Ireland | Positive growth | ⬆️ Strong |

| North West England | Upward trend | ⬆️ Moderate |

| North of England | Upward trend | ⬆️ Moderate |

| London | Below national average | ⬇️ Lagging |

| South East | Below national average | ⬇️ Lagging |

| South West | Below national average | ⬇️ Lagging |

| East Anglia | Below national average | ⬇️ Lagging |

💬 "House prices appear to have stabilised at a national level, although regional disparities are widening." — RICS UK Residential Market Survey, January 2026 [1]

This table is not merely academic. For a valuer preparing a RICS Red Book valuation, these regional signals must directly inform how comparable evidence is selected, weighted, and narrated within the report.

Why London and the South Are Cooling

Affordability remains the primary brake on southern markets. After years of price inflation outpacing wage growth, buyer purchasing power in London, the South East, South West, and East Anglia has been significantly eroded. Higher mortgage rates through 2024 and into 2025 compounded this effect, and while rates have eased modestly, the cumulative affordability gap has not closed [1][6].

The result is a market where properties in these regions are sitting longer, price reductions are more common, and surveyors are increasingly being asked to justify valuations that lenders view with scepticism.

Why the North and Scotland Are Outperforming

Relative affordability, stronger local employment bases in certain sectors, and a catch-up effect from historically lower price levels are all contributing to northern and Scottish outperformance [1]. These markets also tend to have lower average mortgage-to-income ratios, meaning rate sensitivity is somewhat reduced.

For valuers working in these regions, the challenge is different: ensuring that upward momentum is captured accurately without over-inflating assessments based on short-term enthusiasm.

Valuation Strategies for Regional Price Flatness in Spring 2026: Practical Frameworks for Surveyors

Selecting and Weighting Comparable Evidence

The cornerstone of any robust residential valuation is the comparable evidence analysis. In a divergent market, this process requires greater granularity than standard practice might demand.

Key principles for comparable selection in 2026:

-

Prioritise recency aggressively — In flat or declining markets (London, South East), comparables older than three months may already misrepresent current conditions. In rising markets (Scotland, North West), even recent sales may understate current achievable values.

-

Apply directional adjustments explicitly — Where the RICS net balance for a region is negative, surveyors should consider whether a downward time adjustment is warranted on older comparables. This should be documented clearly in the report narrative.

-

Use micro-market data, not regional averages — A borough-level or even street-level analysis is increasingly necessary. South East as a region may be lagging, but specific commuter towns with new infrastructure investment may behave differently.

-

Weight active listings alongside completed sales — In flat markets, asking price data and the frequency of reductions provide real-time signals that Land Registry data (which lags by weeks or months) cannot.

Understanding the full range of valuation factors that influence property pricing — from condition and tenure to local amenity and transport links — is essential when calibrating adjustments in these divergent conditions.

Adjusting for Flat Price Environments: The Southern Market Challenge

In London and the South, surveyors face a specific professional risk: over-valuing on the basis of peak-era comparables. With the RICS data confirming continued underperformance in these regions [1][6], the following adjustments are recommended:

-

Negative time adjustments: Where a comparable sold 6–12 months ago in a market that has since softened, a downward adjustment of 1–3% (market-dependent) may be appropriate. This must be supported by local evidence, not assumed.

-

Increased weighting on distressed sales data: In markets with higher volumes of price reductions, forced sales, or extended days-on-market, these data points become more representative of true market value.

-

Explicit market commentary: RICS Red Book standards require surveyors to comment on market conditions. In 2026, a generic statement is insufficient. Reports should reference regional RICS survey data, local Land Registry trends, and any material changes in mortgage availability or buyer demand.

For professionals handling complex cases such as shared ownership valuations or Help to Buy valuations in southern markets, these adjustments carry particular weight — lenders and housing associations are scrutinising valuations more closely than at any point in the past five years.

Capturing Upward Momentum: The Northern and Scottish Opportunity

The opposite challenge exists in Scotland, Northern Ireland, and the North West. Here, surveyors risk under-valuing if they anchor too heavily on historical comparables that predate the current growth phase.

Recommended approaches:

-

Forward-looking market commentary: Acknowledge the positive RICS net balance for the region and reference the 12-month sentiment reading of +35% [1] as contextual evidence of sustained buyer demand.

-

Reduced negative time adjustments or positive adjustments: Where a comparable sold in a rising market six months ago, a modest upward time adjustment may be justified — but only where active market evidence supports it.

-

Scrutinise new-build premiums carefully: In rising markets, new-build developments can distort comparable pools. Ensure like-for-like comparisons between new and second-hand stock are clearly differentiated.

Applying RICS Data to Specific Valuation Contexts in Divergent UK Markets

Mortgage Valuations and Lender Risk

Lenders are acutely aware of regional divergence. In 2026, several major UK lenders have tightened their loan-to-value thresholds in specific southern postcodes while maintaining or relaxing them in northern regions. Surveyors providing mortgage valuations must:

- Flag regional market conditions explicitly in the report's market commentary section.

- Avoid over-reliance on automated valuation models (AVMs) — these tools typically lag real market conditions and are particularly unreliable in rapidly diverging regional markets.

- Document the basis for any time adjustments with reference to published data sources, including RICS survey results.

Those working in London and surrounding areas can access chartered surveyors in South East London and West London who specialise in navigating these complex urban valuation environments.

Capital Gains Tax and Matrimonial Valuations

For capital gains tax valuations and matrimonial valuations, the regional divergence creates specific challenges around the valuation date. A property valued at a specific date in 2024 may have moved materially in either direction depending on its region — and the direction of that movement is now strongly geography-dependent.

Key considerations:

-

Historical date valuations in southern markets: Where the valuation date falls within the period of London/South East underperformance (broadly mid-2024 onwards), the valuer must carefully reconstruct market conditions at that specific point rather than interpolating from current levels.

-

Historical date valuations in northern markets: The reverse applies — northern markets have generally been on an upward trajectory, meaning a 2024 historical valuation may be lower than current market value by a meaningful margin.

-

Document the regional context: Any retrospective valuation report should include a section explicitly addressing regional market conditions at the valuation date, supported by RICS survey data and Land Registry evidence from that period.

Building Survey Integration with Valuation Advice

In flat or declining markets, condition-related value adjustments become more significant. Buyers in a buyer's market have greater negotiating power, and defects that might have been absorbed in a rising market now translate more directly into price reductions.

Surveyors conducting RICS building surveys alongside valuation work should ensure that:

- Condition ratings are clearly cross-referenced with any valuation advice provided.

- In flat markets, the cost of remediation is more likely to be reflected in achievable sale price — this should be noted explicitly.

- Clients are directed to understand what a surveyor checks so they can make informed decisions about negotiation.

The 12-Month Outlook: Planning Valuations Around Improving Sentiment

The RICS January 2026 data recorded a 12-month price sentiment balance of +35% — the strongest reading since December 2024 [1]. Near-term (3-month) sentiment stood at +4%, indicating that the recovery is expected to build gradually rather than surge immediately.

For valuers, this medium-term optimism has practical implications:

- Development appraisals and residual valuations should incorporate improving market assumptions for 2026–2027 exit values, particularly in northern and Scottish markets.

- Phased development projects may benefit from a stepped approach to exit value assumptions, reflecting near-term flatness followed by improving conditions.

- Investment valuations should note the divergence between near-term caution and medium-term optimism, and reflect this in yield assumptions and sensitivity analysis.

Practical Checklist: Valuation Strategies for Regional Price Flatness in Spring 2026

For surveyors seeking to apply these principles immediately, the following checklist provides a structured approach:

✅ Identify the regional RICS net balance for the subject property's location before beginning comparable analysis.

✅ Apply time adjustments explicitly — upward in rising regions, downward in lagging regions — and document the evidence base.

✅ Select a minimum of three comparables from within the same micro-market, prioritising sales within the past three months.

✅ Include a dedicated market conditions section in all Red Book reports, referencing RICS survey data and local Land Registry trends.

✅ Flag lender-specific regional risk factors in mortgage valuation reports where the subject property is in a demonstrably underperforming postcode.

✅ Cross-reference condition findings from any associated building survey with valuation assumptions.

✅ Review the 12-month RICS sentiment data when preparing development appraisals or investment valuations to ensure exit value assumptions are appropriately calibrated.

Conclusion: Acting on Regional Divergence in 2026

The spring 2026 UK property market is not one market — it is several, moving in different directions at different speeds. Valuation Strategies for Regional Price Flatness in Spring 2026: RICS Data for Divergent UK Markets demands that surveyors move beyond national indices and apply genuinely localised, evidence-based methodologies.

The RICS data is clear: Scotland and the North are growing, London and the South are lagging, and medium-term sentiment is improving nationally [1][6]. The professional obligation is to translate these signals into precise, defensible valuation adjustments that reflect the reality on the ground — not the comfort of a national average.

Actionable next steps for surveyors:

- Subscribe to RICS regional survey data and integrate it into every valuation report as standard practice.

- Build regional comparable databases that allow rapid identification of micro-market trends.

- Review your time adjustment methodology and ensure it is explicitly calibrated to regional rather than national conditions.

- Engage with clients proactively about regional market conditions — particularly those commissioning capital gains tax or matrimonial valuations where the regional context materially affects the outcome.

- Consult with specialist valuers in your region if operating outside your primary geographic area — regional expertise is now a professional necessity, not a luxury.

For those seeking expert valuation support across divergent UK markets in 2026, contact a qualified RICS surveyor who understands the regional nuances that national data alone cannot capture.

References

[1] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Regional Price Parities State And Metro Area – https://www.bea.gov/data/prices-inflation/regional-price-parities-state-and-metro-area

[3] Home Price Growth Continue To Moderate But Trends Divided – https://www.rismedia.com/2026/04/09/home-price-growth-continue-to-moderate-but-trends-divided/

[4] Major Housing Markets With Falling Rising Home Prices April 2026 – https://www.resiclubanalytics.com/p/major-housing-markets-with-falling-rising-home-prices-april-2026

[6] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf