The UK property landscape is experiencing a dramatic shift in 2026. Young professionals are fleeing the unaffordable housing markets of London and the South East, setting their sights on northern cities where property dreams remain within reach. This migration trend is creating unprecedented opportunities for first-time buyers willing to look beyond traditional southern hotspots. However, Building Surveys for First-Time Buyers in Northern Markets: Capturing 2026 Migration Demand from Southern Slump requires careful planning, expert guidance, and thorough property inspections to avoid costly mistakes in unfamiliar territories.

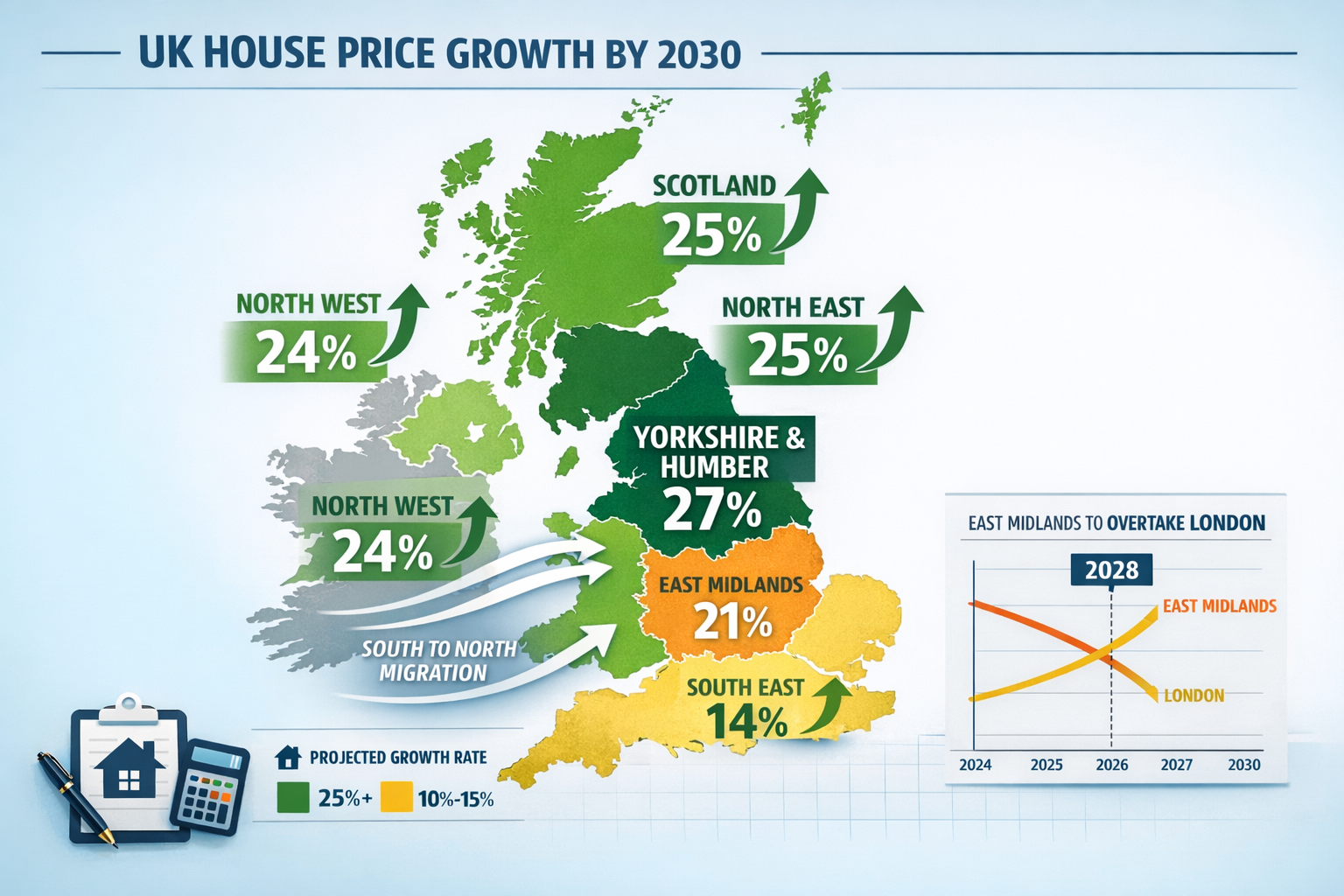

With Yorkshire and the Humber projected to see approximately 27% cumulative house price growth through 2030[1], and the East Midlands forecast to overtake London in cumulative growth by 2028[1], northern markets represent compelling value. Yet these opportunities come with unique challenges that demand comprehensive building surveys tailored to regional property characteristics.

Key Takeaways

- 🏘️ Northern markets are outperforming southern regions, with Yorkshire, Scotland, and the North East forecast for 25-27% growth through 2030 compared to weaker London performance[1]

- 💷 Affordability drives migration, as London's average flat price of £539,000 is more than double northern equivalents, pushing first-time buyers northward[1]

- 🔍 Comprehensive building surveys are essential for first-time buyers entering unfamiliar northern markets to identify hidden defects, EPC upgrade requirements, and regional property issues

- 📊 Houses outperform flats with semi-detached properties seeing 2.4% annual appreciation versus overall 0.6% UK average[1]

- ⚡ Energy efficiency matters more than ever, as buyers must budget for EPC upgrades in older northern housing stock to meet rental and resale standards

Understanding the 2026 Migration Phenomenon: Why First-Time Buyers Are Moving North

The Southern Affordability Crisis

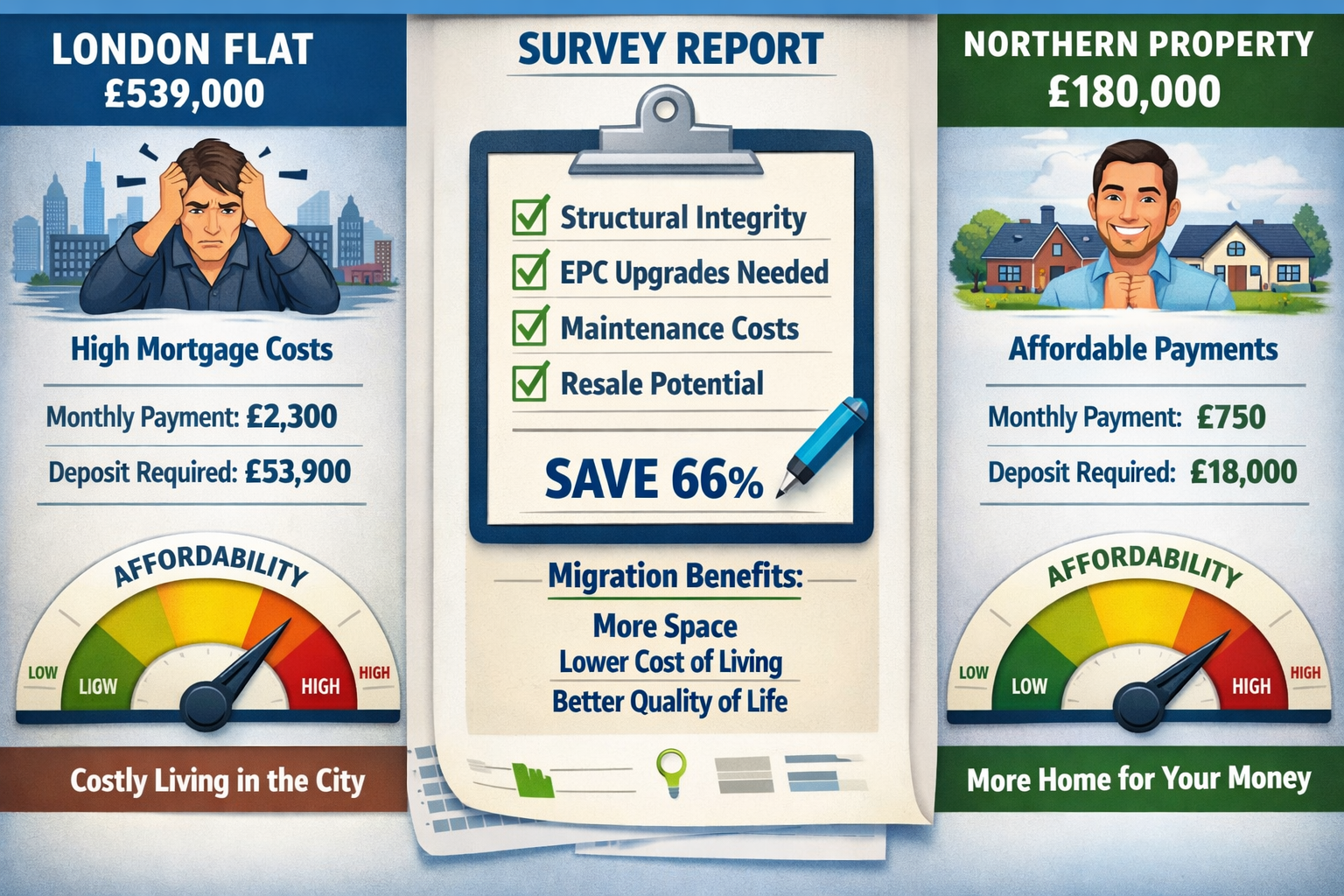

The numbers tell a stark story. London's property market has become increasingly inaccessible to first-time buyers, with average flat prices hovering around £539,000—more than double the average in Scotland, Wales, Northern Ireland, and northern England[1]. This affordability gap isn't just a London problem; it extends across much of the South East where property prices have outpaced wage growth for years.

Mortgage rates remaining approximately three times higher than post-pandemic lows have compounded these challenges[1]. First-time buyers face a perfect storm: high property prices, elevated borrowing costs, and stretched affordability metrics that make southern homeownership feel increasingly unattainable.

Northern Markets: The New Frontier

In contrast, northern markets offer compelling value propositions. Cities like Leicester, Nottingham, Derby, Leeds, Manchester, and Newcastle provide:

✅ Substantially lower entry prices

✅ Strong employment opportunities in growing sectors

✅ Excellent transport links and infrastructure investment

✅ Vibrant cultural scenes attractive to young professionals

✅ Projected growth rates exceeding southern counterparts

Yorkshire and the Humber's projected 27% cumulative house price growth through 2030[1] represents not just affordability but genuine investment potential. Scotland and the North East follow closely with approximately 25% forecast growth[1], compared to just 22% UK-wide and weaker expectations for London and the South East.

Migration Patterns Reshaping Demand

Internal migration from expensive southern regions is fundamentally reshaping northern property markets[1]. This isn't temporary—it reflects structural changes in work patterns, lifestyle preferences, and economic realities. University towns and major northern cities are particularly benefiting from this influx, with demand supporting sustained value growth.

International migration to major cities also supports northern values[1], creating diverse, dynamic communities that enhance long-term investment prospects. Meanwhile, parts of the South East face potential softening as buyers reassess value propositions.

Building Surveys for First-Time Buyers in Northern Markets: Essential Considerations

Why Standard Surveys Aren't Enough

First-time buyers venturing into northern markets face unique challenges that demand specialized survey approaches. Many northern properties feature Victorian and Edwardian construction, solid wall construction without cavity insulation, aging infrastructure, and regional building techniques unfamiliar to buyers from southern areas.

A comprehensive Level 3 building survey becomes essential rather than optional when purchasing in unfamiliar territories. These detailed inspections identify hidden defects that could derail affordability calculations or create unexpected financial burdens.

Regional Property Characteristics Requiring Expert Assessment

Northern housing stock presents specific considerations:

Structural Issues:

- Subsidence and settlement in areas with historical mining activity

- Solid wall construction requiring external or internal insulation for EPC compliance

- Slate roof deterioration common in older northern properties

- Damp and moisture penetration in properties with inadequate damp-proof courses

Energy Efficiency Challenges:

- Poor EPC ratings in older terraced housing (often D, E, or F ratings)

- Single-glazed windows requiring replacement

- Outdated heating systems with inefficient boilers

- Lack of loft insulation in period properties

Maintenance Backlogs:

- Deferred maintenance in properties purchased as value investments

- Aging electrical systems not meeting current regulations

- Outdated plumbing with lead pipes or deteriorating systems

- Chimney and flue issues in properties with historical features

Understanding what surveyors check during inspections helps first-time buyers appreciate the value of thorough assessments.

EPC Upgrades: A Critical Budget Consideration

Energy Performance Certificate (EPC) requirements are reshaping property values and buyer calculations. Properties with poor EPC ratings face:

🔴 Rental restrictions (minimum EPC rating E for new tenancies)

🔴 Reduced resale appeal as buyers factor upgrade costs

🔴 Higher running costs impacting affordability

🔴 Potential future regulations requiring minimum standards

First-time buyers must budget for EPC improvements when purchasing older northern properties. A building survey should specifically assess:

- Current EPC rating and improvement potential

- Cost estimates for insulation upgrades

- Heating system replacement requirements

- Window and door efficiency improvements

- Renewable energy installation feasibility

These upgrades can cost £5,000-£25,000 depending on property condition, representing significant additional investment beyond purchase price.

Capturing 2026 Migration Demand: Strategic Approaches for First-Time Buyers

Identifying High-Growth Northern Locations

Not all northern markets offer equal opportunity. Strategic first-time buyers focus on locations with:

Strong Fundamentals:

- Employment growth in technology, professional services, and creative industries

- University presence supporting rental demand and cultural vibrancy

- Transport connectivity including rail links to other major cities

- Regeneration investment in infrastructure and amenities

- Population growth driven by both internal and international migration

Property Market Indicators:

- Sustainable price-to-income ratios allowing for future appreciation

- Limited new supply preventing oversupply issues

- Diverse property types offering upgrade pathways

- Established communities with long-term stability

The East Midlands' forecast to overtake London in cumulative house price growth since 2010 by 2028[1] highlights how previously overlooked markets are delivering exceptional returns.

Property Type Selection: Houses vs. Flats

Market data reveals significant performance divergence between property types. Semi-detached houses saw annual appreciation of around 2.4% in December 2025—roughly four times the overall UK average of 0.6%[1]. This reflects lasting post-pandemic demand for space, gardens, and home working flexibility.

Conversely, flats are expected to underperform, particularly high-rise developments with significant service charges[1]. First-time buyers should carefully consider:

Houses (Terraced, Semi-Detached):

✅ Stronger appreciation potential

✅ Greater space and flexibility

✅ Lower ongoing service charges

✅ Better suited to remote/hybrid working

✅ More attractive to future buyers

Flats:

⚠️ Weaker growth prospects

⚠️ High service charges eroding affordability

⚠️ Leasehold complications

⚠️ Limited space for lifestyle changes

⚠️ Potential oversupply in some markets

For first-time buyers with limited budgets, a smaller terraced house often represents better long-term value than a larger flat at similar price points.

Leveraging Professional Survey Expertise

Navigating unfamiliar northern markets requires expert guidance. Chartered surveyors with local knowledge provide invaluable insights into:

- Regional construction methods and common defects

- Local market conditions affecting property values

- Area-specific risks (flooding, subsidence, contamination)

- Realistic renovation costs based on local contractor rates

- Future development plans impacting property desirability

When considering whether a homebuyer survey is worth it, first-time buyers entering new markets should recognize that comprehensive surveys offer insurance against costly surprises.

Building Surveys for First-Time Buyers in Northern Markets: Practical Implementation Guide

Survey Type Selection for Different Property Scenarios

Choosing the appropriate survey level depends on property age, condition, and buyer risk tolerance:

Level 2 RICS Homebuyer Survey:

- Suitable for: Modern properties (post-1990) in good condition

- Coverage: Standard inspection of visible elements

- Cost: £400-£800 typically

- Timeline: Usually completed within 3-5 business days

Level 3 Building Survey (Recommended for Northern Properties):

- Suitable for: Pre-1990 properties, unusual construction, visible defects

- Coverage: Comprehensive inspection including accessible areas

- Cost: £600-£1,500 depending on property size

- Timeline: Typically 5-10 business days for completion

For most first-time buyers purchasing Victorian or Edwardian northern properties, a comprehensive Level 3 building survey provides essential protection. Understanding the difference between Level 2 and Level 3 surveys helps buyers make informed decisions.

Essential Survey Checklist for Northern Properties

First-time buyers should ensure their building survey addresses these critical areas:

Structural Integrity:

- Foundation condition and settlement evidence

- Wall construction type and stability

- Subsidence risk assessment (particularly in mining areas)

- Structural movement indicators

- Load-bearing wall integrity

Roof and External Elements:

- Slate/tile condition and remaining lifespan

- Chimney stack stability and pointing

- Guttering and drainage effectiveness

- External wall condition and weatherproofing

- Window and door condition

Damp and Moisture:

- Damp-proof course presence and effectiveness

- Rising damp evidence

- Penetrating damp from external sources

- Condensation and ventilation issues

- Timber decay and rot

Services and Systems:

- Electrical system age and compliance

- Heating system efficiency and condition

- Plumbing materials and condition

- Drainage system functionality

- Gas safety (if applicable)

Energy Efficiency:

- Current EPC rating

- Insulation levels (walls, loft, floors)

- Window glazing efficiency

- Heating system efficiency

- Renewable energy potential

Legal and Planning:

- Building regulation compliance

- Alteration approval documentation

- Conservation area restrictions

- Future development impact

- Rights of way or easements

Interpreting Survey Results: Red Flags vs. Negotiable Issues

Not all survey findings are equal. First-time buyers must distinguish between:

Critical Issues (Potential Deal-Breakers):

🚨 Active subsidence requiring underpinning

🚨 Structural instability threatening building integrity

🚨 Severe damp causing timber decay

🚨 Dangerous electrical systems

🚨 Major roof failure requiring complete replacement

🚨 Asbestos requiring professional removal

Significant Issues (Negotiation Opportunities):

⚠️ Boiler nearing end of life (£2,000-£4,000 replacement)

⚠️ Windows requiring replacement (£5,000-£15,000)

⚠️ Damp-proof course repairs needed (£1,500-£5,000)

⚠️ Roof repairs required (£3,000-£10,000)

⚠️ Outdated electrical consumer unit (£500-£1,500)

Minor Issues (Budget for Maintenance):

✓ Cosmetic repairs

✓ Minor pointing work

✓ Gutter cleaning and minor repairs

✓ Decorative improvements

✓ Garden maintenance

Armed with detailed survey findings, first-time buyers can:

- Renegotiate purchase price to reflect repair costs

- Request seller remediation before completion

- Budget accurately for post-purchase improvements

- Make informed decisions about proceeding with purchase

- Plan renovation priorities based on urgency

Financial Planning: Making Northern Migration Work

True Cost of Ownership Beyond Purchase Price

First-time buyers must budget comprehensively:

Upfront Costs:

- Deposit (typically 10-15% minimum)

- Survey fees (£600-£1,500 for Level 3)

- Legal fees (£1,000-£2,000)

- Stamp duty (varies by price and first-time buyer relief)

- Removal costs (£500-£2,000)

- Initial furnishing and setup (£2,000-£10,000)

Immediate Post-Purchase:

- EPC upgrade works (£5,000-£25,000)

- Essential repairs identified in survey (£2,000-£20,000)

- Decoration and personalization (£2,000-£10,000)

- Emergency fund for unexpected issues (£5,000 minimum)

Ongoing Costs:

- Mortgage payments (calculate at higher rates for stress testing)

- Buildings insurance (£200-£600 annually)

- Maintenance and repairs (budget 1-2% of property value annually)

- Council tax (varies by location and band)

- Utilities (potentially higher in poorly insulated properties)

- Service charges (if applicable)

Mortgage Considerations for Northern Purchases

With mortgage rates remaining approximately three times higher than post-pandemic lows[1], affordability calculations require conservative assumptions:

Stress Testing:

- Calculate affordability at current rate plus 2-3%

- Ensure monthly payments don't exceed 30-35% of take-home income

- Account for potential rate increases at fixed-term end

- Consider impact of children, career changes, or income reduction

Deposit Strategies:

- Larger deposits (15-25%) secure better rates

- Consider Help to Buy schemes where applicable

- Evaluate shared ownership as stepping stone

- Factor in survey-identified repair costs when determining deposit level

Lender Requirements:

- Survey findings may impact mortgage offers

- Serious defects can result in reduced valuations

- Some lenders require specific repairs before completion

- Building insurance may be difficult for properties with significant issues

Long-Term Investment Perspective

Northern markets offer compelling long-term prospects. UK house price growth is forecast to remain at sustainable steady levels[2], with northern regions outperforming London[2]. Recent data shows average UK house prices increased by 2.4% to £270,000 in the 12 months to December 2025[4], with northern markets contributing strongly to this growth.

First-time buyers should adopt 5-10 year investment horizons, recognizing that:

📈 Regional rebalancing favors northern appreciation

📈 Infrastructure investment enhances long-term values

📈 Demographic trends support sustained demand

📈 Affordability advantages attract continued migration

📈 Quality of life improvements make northern cities increasingly desirable

Avoiding Common Pitfalls: Lessons from 2026 Migration Buyers

Pitfall #1: Underestimating Renovation Costs

Many first-time buyers stretch budgets to maximum purchase prices, leaving insufficient reserves for necessary improvements. Northern properties often require:

- EPC upgrades to meet rental/resale standards

- Heating system replacements in properties with aging boilers

- Insulation improvements for comfort and running costs

- Electrical upgrades to meet current regulations

- Damp remediation in properties with solid wall construction

Solution: Budget minimum £10,000-£15,000 renovation reserve beyond purchase costs. Obtain detailed quotes for survey-identified works before committing to purchase.

Pitfall #2: Skipping Comprehensive Surveys

Some buyers opt for basic valuations to save costs, only to discover expensive defects post-purchase. This is particularly risky in unfamiliar markets with different construction methods.

Solution: Invest in comprehensive Level 3 building surveys for older properties. The £600-£1,500 cost is negligible compared to potential £20,000+ repair bills.

Pitfall #3: Ignoring Location-Specific Risks

Northern markets vary significantly. Some areas face:

- Historical mining subsidence risks

- Flood zones requiring expensive insurance

- Industrial contamination affecting property values

- Declining employment in former industrial towns

- Oversupply of certain property types

Solution: Research thoroughly beyond property itself. Examine local employment trends, infrastructure investment, and area development plans. Choose locations with strong fundamentals.

Pitfall #4: Overlooking Rental Market Dynamics

Many first-time buyers plan to rent rooms or eventually let properties. However:

- EPC minimum ratings restrict rental options

- Selective licensing schemes add costs in some areas

- Oversupply of student accommodation affects some university towns

- Tenant demand varies significantly by location

Solution: Research local rental markets before purchase. Ensure property meets or can economically achieve minimum EPC standards for rental.

Pitfall #5: Emotional Decision-Making

The excitement of affording a larger property in northern markets can cloud judgment. Buyers sometimes overlook serious defects or overpay relative to local market conditions.

Solution: Maintain disciplined approach. Use survey findings objectively. Compare prices to local comparables. Don't let southern price perspectives distort northern value assessments.

The Rental Market Context: How It Influences First-Time Buyer Decisions

Rental Shortage Driving Purchase Decisions

The UK continues facing a shortage of rental homes, with landlord instructions in negative territory throughout 2025[2]. This scarcity drives some renters toward first-time buyer decisions, particularly in northern markets where purchase prices more closely align with rental costs.

Rent vs. Buy Calculations:

In many northern markets, monthly mortgage payments (including insurance and maintenance) now compete favorably with rental costs:

| Location | Average Monthly Rent | Equivalent Mortgage Payment (£150k property, 15% deposit, 5.5% rate) |

|---|---|---|

| Leeds | £950-£1,200 | £850-£950 (including insurance/maintenance) |

| Manchester | £1,100-£1,400 | £900-£1,000 |

| Newcastle | £800-£1,000 | £750-£850 |

| Nottingham | £850-£1,100 | £800-£900 |

These calculations demonstrate how first-time buyers can achieve ownership for comparable or lower monthly costs than renting, while building equity.

Rental Growth Trends

Average UK monthly private rents increased by 3.5% to £1,367 in the 12 months to January 2026, down from 4.0% in the previous 12-month period[4]. While rental growth is moderating, it remains above general inflation, making ownership increasingly attractive for those who can access deposits.

Northern rental markets show particular strength due to:

- Student demand in university cities

- Young professional migration from southern regions

- Limited new rental supply as landlords exit market

- Affordability advantages over southern alternatives

Building Surveys for First-Time Buyers in Northern Markets: Regional Spotlight

Yorkshire and the Humber: The Growth Leader

With projected 27% cumulative house price growth through 2030[1], Yorkshire represents the UK's strongest regional market. Key cities include:

Leeds:

- Strong professional services and financial sector

- Excellent transport links (HS2 planned)

- Vibrant cultural scene

- Property types: Victorian terraces, modern apartments, suburban semis

- Survey focus: Solid wall construction, roof condition, drainage

Sheffield:

- Diversified economy with advanced manufacturing and digital

- Affordable entry prices

- Green spaces and quality of life

- Property types: Stone terraces, suburban houses

- Survey focus: Stone wall condition, hillside drainage, subsidence

York:

- Historic city with tourism and education sectors

- Higher prices but strong demand

- Conservation area considerations

- Property types: Period properties, modern developments

- Survey focus: Listed building restrictions, flood risk, historical features

Scotland: 25% Growth Potential

Scotland's forecast 25% cumulative growth[1] combines affordability with quality of life:

Edinburgh:

- Capital city with financial services and tourism

- Strong international appeal

- Higher prices but exceptional amenities

- Property types: Tenement flats, Georgian townhouses

- Survey focus: Tenement maintenance, shared responsibilities, stone condition

Glasgow:

- Economic regeneration and cultural renaissance

- Excellent value for money

- Growing technology sector

- Property types: Tenement flats, Victorian terraces, new builds

- Survey focus: Tenement common repairs, damp in sandstone, electrical systems

East Midlands: The Overtaking Story

Forecast to overtake London in cumulative house price growth since 2010 by 2028[1], the East Midlands offers exceptional value:

Leicester:

- Diverse economy and demographics

- Strong university presence

- Excellent transport connectivity

- Property types: Victorian terraces, suburban semis, new developments

- Survey focus: Victorian construction, EPC potential, structural alterations

Nottingham:

- Two major universities driving demand

- Creative and digital sector growth

- Affordable prices with appreciation potential

- Property types: Terraced houses, student areas, suburban family homes

- Survey focus: Rental conversion quality, damp issues, maintenance standards

Derby:

- Manufacturing heritage with modern industries

- Lower entry prices

- Good transport links

- Property types: Terraced houses, semis, new builds

- Survey focus: Industrial proximity impacts, construction quality, subsidence

Expert Recommendations: Maximizing Success in Northern Markets

Working with Local Professionals

Success in unfamiliar markets requires local expertise:

RICS Chartered Surveyors:

Choose RICS-accredited professionals with specific regional experience. They understand:

- Local construction methods and materials

- Common regional defects and issues

- Realistic repair costs using local contractors

- Area-specific risks and considerations

- Market conditions affecting property values

Local Estate Agents:

Establish relationships with agents in target areas who can:

- Provide market intelligence on pricing trends

- Identify off-market opportunities

- Advise on neighborhood characteristics

- Recommend other local professionals

- Negotiate effectively on your behalf

Solicitors with Regional Knowledge:

Local conveyancing solicitors understand:

- Regional searches and requirements

- Local authority planning considerations

- Area-specific legal issues

- Mining searches and historical concerns

- Efficient local processes

Timing Your Purchase

Market timing influences success:

Seasonal Considerations:

- Spring (March-May): Peak market activity, more choice, higher competition

- Summer (June-August): Family-friendly timing, continued activity

- Autumn (September-November): Motivated sellers, good negotiation opportunities

- Winter (December-February): Fewer buyers, better negotiation leverage, serious sellers

Economic Factors:

- Monitor mortgage rate trends and fix when favorable

- Consider broader economic indicators affecting employment

- Watch for local infrastructure announcements boosting areas

- Track new development supply potentially affecting values

Personal Readiness:

- Ensure deposit and reserves fully available

- Obtain mortgage agreement in principle

- Research thoroughly before beginning viewings

- Have survey and legal teams identified and ready

Post-Purchase Success Strategies

Maximizing northern property investments requires active management:

Immediate Priorities:

- Address critical survey findings promptly

- Improve EPC rating to minimum C if possible

- Establish maintenance schedule for preventive care

- Build relationships with reliable local contractors

- Ensure adequate insurance coverage

Medium-Term Value Enhancement:

- Modernize kitchens and bathrooms for rental/resale appeal

- Improve energy efficiency beyond minimum standards

- Enhance outdoor spaces and curb appeal

- Address deferred maintenance systematically

- Consider loft conversions or extensions where viable

Long-Term Wealth Building:

- Maintain property to high standards

- Monitor local market trends and comparable sales

- Consider refinancing when equity builds and rates favor

- Evaluate rental income potential if circumstances change

- Plan upgrade pathway to larger properties as equity grows

Conclusion: Seizing the Northern Opportunity

The 2026 migration from southern markets to northern regions represents a generational opportunity for first-time buyers. With Yorkshire and the Humber projected for 27% cumulative growth through 2030[1], Scotland and the North East at 25%[1], and the East Midlands forecast to overtake London by 2028[1], the economic case for northern investment is compelling.

However, success requires more than simply buying cheaper properties. Building Surveys for First-Time Buyers in Northern Markets: Capturing 2026 Migration Demand from Southern Slump demands comprehensive due diligence, expert professional guidance, and realistic financial planning.

The key takeaways for first-time buyers include:

✅ Invest in comprehensive Level 3 building surveys for older northern properties to identify hidden defects and avoid costly surprises

✅ Budget realistically for EPC upgrades, essential repairs, and ongoing maintenance beyond purchase price

✅ Choose locations strategically based on employment growth, infrastructure investment, and sustainable fundamentals rather than just low prices

✅ Prioritize houses over flats given the 2.4% appreciation for semi-detached properties versus 0.6% overall average[1]

✅ Work with local professionals who understand regional construction methods, common defects, and realistic costs

✅ Adopt long-term perspectives recognizing that northern markets offer sustainable growth rather than speculative gains

✅ Maintain financial discipline despite excitement about affording larger properties, ensuring adequate reserves for improvements

The affordability crisis in London and the South East—with average flat prices of £539,000 versus half that in northern regions[1]—is driving fundamental restructuring of UK property markets. First-time buyers who approach northern opportunities with thorough research, comprehensive surveys, and realistic budgets position themselves for both immediate homeownership and long-term wealth building.

Actionable Next Steps

For first-time buyers ready to capture northern migration opportunities:

- Define target locations based on employment, lifestyle preferences, and investment potential

- Obtain mortgage agreement in principle to understand realistic budgets

- Research local markets including price trends, rental yields, and development plans

- Identify RICS chartered surveyor with regional expertise for when you find suitable property

- Budget comprehensively including deposit, survey, legal fees, and £10,000+ renovation reserve

- View properties critically focusing on structural condition and improvement potential

- Commission Level 3 building survey for any serious purchase consideration

- Negotiate based on findings using survey results to adjust price or request repairs

- Plan improvements systematically prioritizing EPC upgrades and essential maintenance

- Build local professional network of contractors, agents, and advisors for ongoing support

The northern property opportunity of 2026 rewards prepared, informed buyers who combine enthusiasm with diligence. By investing in comprehensive building surveys and approaching purchases strategically, first-time buyers can successfully navigate this market transition and build lasting wealth in thriving northern communities.

References

[1] Uk Price Forecasts – https://investropa.com/blogs/news/uk-price-forecasts

[2] Residential Forecast – https://www.cushmanwakefield.com/en/united-kingdom/insights/residential-forecast

[3] Watch – https://www.youtube.com/watch?v=qyh_Sl6ZtgI

[4] February2026 – https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/privaterentandhousepricesuk/february2026