The 2026 Budget has fundamentally reshaped the landscape for high-value property transactions in the UK, particularly affecting properties valued above £2 million. Treasury fees and enhanced tax burdens are now slowing prime markets across London and the South East, creating unprecedented challenges for property professionals. For chartered surveyors navigating post-budget 2026 tax hikes on high-value properties, understanding valuation strategies for surveyors facing £2M+ threshold fees has become essential to maintaining accuracy and client confidence amid these wealth taxes.

The changes extend far beyond simple rate adjustments. With Agricultural Property Relief (APR) and Business Property Relief (BPR) now capped at £2.5 million combined, alongside increased Capital Gains Tax rates and separated property income tax bands, surveyors must recalibrate their entire approach to valuing premium properties. This comprehensive guide explores the practical RICS-aligned adjustments required to deliver accurate valuations in this transformed market environment.

Key Takeaways

- Combined relief cap: APR and BPR now share a £2.5 million allowance per individual with 100% relief, with only 50% relief above this threshold, creating an effective 20% IHT rate on excess values[1][2]

- Market slowdown impact: Enhanced SDLT surcharges of 10% for additional properties valued £250,001-£925,000 are significantly reducing transaction volumes in prime markets[7]

- Valuation methodology shifts: RICS-compliant surveyors must now incorporate tax efficiency implications, separated property income tax rates (22%-47% from April 2027), and reduced market liquidity into their assessments[6]

- Business asset considerations: The BADR rate increase to 18% adds £40,000 in tax liability per £1 million qualifying gain, requiring revised exit valuations for commercial property holdings[2]

- Transferable allowances: Married couples and civil partners can access up to £5 million in combined relief, making ownership structure a critical valuation factor[2]

Understanding the 2026 Budget Changes Affecting High-Value Properties

The 2026 Budget introduced a comprehensive restructuring of property-related taxation that directly impacts valuation methodologies for properties exceeding the £2 million threshold. These changes represent the most significant shift in wealth taxation policy in over a decade, with far-reaching implications for surveyors conducting valuations in the premium property sector.

The £2.5 Million Combined Relief Cap

The most consequential change for high-value property owners involves the combined cap on Agricultural Property Relief (APR) and Business Property Relief (BPR) at £2.5 million per individual[1][2]. Previously, these reliefs could provide 100% inheritance tax exemption on qualifying assets without monetary limits. Under the new regime:

- Properties and assets receive 100% relief up to £2.5 million combined

- Values exceeding this threshold receive only 50% relief

- This creates an effective IHT rate of 20% on amounts above the cap

- The allowance transfers between spouses and civil partners, permitting up to £5 million per couple[2]

For a surveyor valuing a £5 million agricultural estate, the IHT implications have changed dramatically. Previously, the entire value might have qualified for 100% relief. Now, only £2.5 million receives full relief, while the remaining £2.5 million faces a 20% effective rate, adding £500,000 to the estate's tax liability.

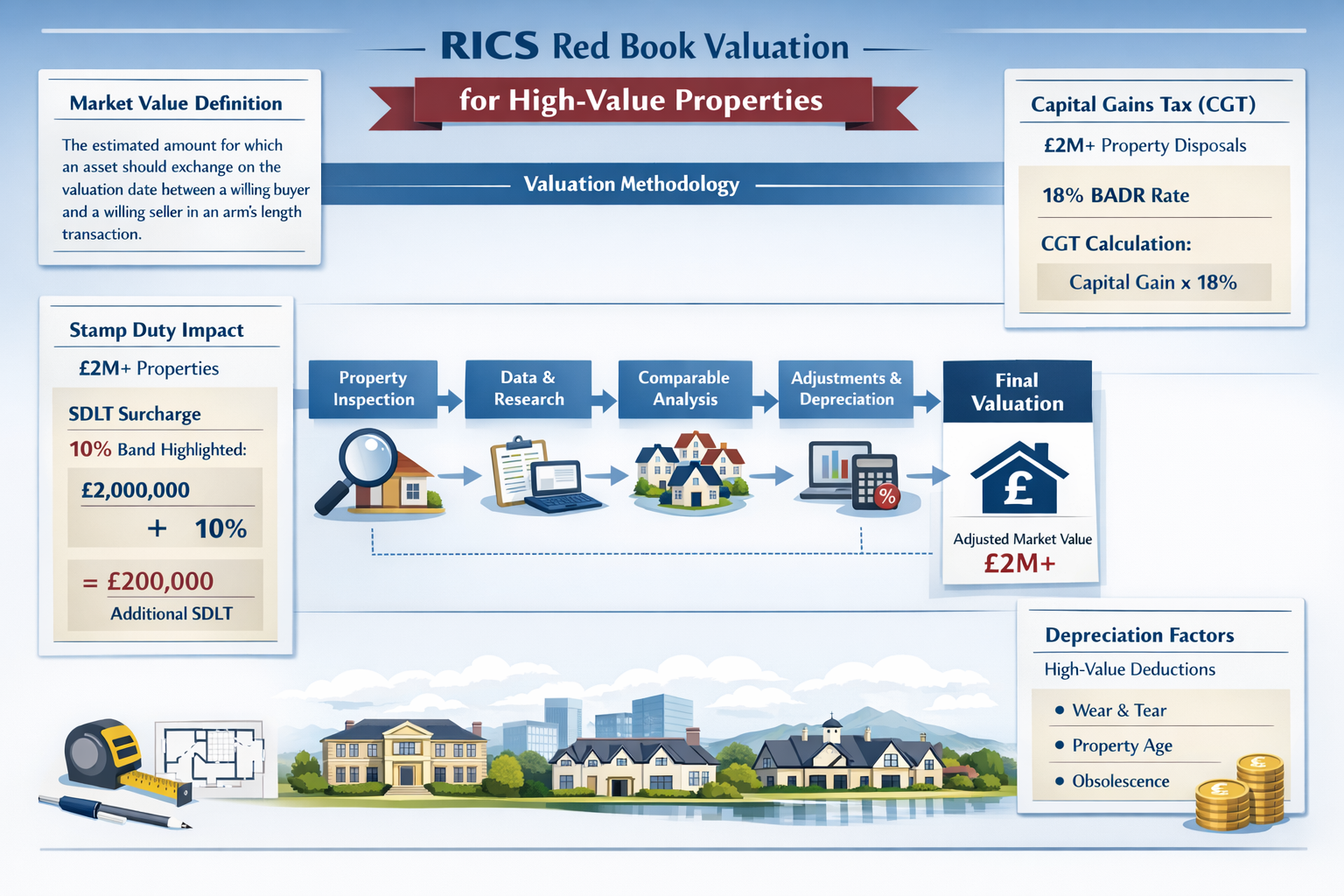

Enhanced Stamp Duty Land Tax Surcharges

Portfolio investors and second-home buyers face significantly increased SDLT burdens that directly affect market demand and transaction volumes. Properties valued between £250,001 and £925,000 now attract a 10% SDLT rate for purchasers already owning residential properties, compared to just 5% for first-time buyers[7].

This differential creates a substantial price sensitivity at the £2 million threshold, where the cumulative SDLT burden becomes prohibitive for many potential buyers. Surveyors must account for this reduced buyer pool when establishing market value through comparable analysis.

Business Asset Disposal Relief Rate Increases

The Capital Gains Tax rate for Business Asset Disposal Relief (BADR) has risen from 14% to 18% as of April 2026[2]. For a business owner disposing of commercial property with a £1 million qualifying gain, the tax liability increases from £140,000 to £180,000—an additional £40,000 burden.

This change particularly affects valuation strategies for commercial properties where business owners are planning exit strategies. Surveyors must now factor in reduced net proceeds when advising clients on realistic sale expectations.

Separated Property Income Tax Bands

From April 2027, property income will be taxed under separate rate structures[6]:

| Tax Band | Property Income Rate | Standard Income Rate |

|---|---|---|

| Basic Rate | 22% | 20% |

| Higher Rate | 42% | 40% |

| Additional Rate | 47% | 45% |

This separation means high-value property portfolios will face enhanced tax burdens on rental income, affecting investment yield calculations and ultimately influencing property valuations for income-producing assets.

Navigating Post-Budget 2026 Tax Hikes: RICS-Aligned Valuation Adjustments for Surveyors

Professional surveyors must adapt their methodologies to reflect the changed market dynamics created by these tax hikes. RICS standards require valuations to reflect market conditions as they exist, not as they were previously. This means incorporating tax implications into every stage of the valuation process.

Adjusting Comparable Analysis for Reduced Transaction Volumes

The slowdown in prime property markets creates significant challenges for comparable analysis. With fewer transactions occurring above the £2 million threshold, surveyors face a narrower evidence base for establishing market value.

Best practices for navigating post-budget 2026 tax hikes on high-value properties include:

- ✅ Expanding the geographical search area to capture sufficient comparable evidence

- ✅ Extending the time period for comparables while applying appropriate time adjustments

- ✅ Weighting more recent transactions more heavily to reflect current market sentiment

- ✅ Documenting market conditions thoroughly to support valuation conclusions

- ✅ Considering pre-budget transactions with explicit adjustments for changed tax environment

When conducting a Level 3 building survey on high-value properties, surveyors should explicitly note how tax changes affect marketability and value.

Incorporating Tax Efficiency into Market Value Assessments

RICS Red Book standards require valuations to reflect the price a willing buyer would pay in current market conditions. With tax efficiency now a primary consideration for high-value property purchasers, surveyors must account for:

Ownership structure implications: Properties held in structures that maximize the £2.5 million relief allowance (or £5 million for couples) command premium values compared to those without such advantages.

Income tax optimization: For rental properties, the separated tax bands create varying value propositions depending on the buyer's existing income profile. A basic-rate taxpayer faces only a 2% penalty on property income, while an additional-rate taxpayer faces a 2% premium[6].

Capital gains planning: Properties with significant embedded gains now carry additional buyer resistance due to the 18% BADR rate. Surveyors should consider this when valuing properties with substantial appreciation since acquisition.

Applying Appropriate Adjustments for Market Liquidity

The reduced transaction velocity in the £2M+ segment creates a liquidity discount that professional surveyors must quantify. Properties that previously sold within 3-6 months may now require 9-12 months or longer to find suitable buyers.

When preparing insurance reinstatement valuations for high-value properties, this extended marketing period should inform the assessment of market value versus replacement cost differentials.

Liquidity adjustment framework:

- Analyze days-on-market data for properties above £2 million in the relevant location

- Compare pre-budget and post-budget marketing periods to quantify the change

- Apply a percentage adjustment to comparable values to reflect extended holding costs

- Document the rationale clearly in the valuation report

For surveyors working in prime London locations, our chartered surveyors in Richmond and chartered surveyors in Kingston have developed specialized expertise in valuing properties affected by these tax changes.

Addressing Business Property Relief Implications

For properties qualifying for BPR (such as furnished holiday lets, trading premises, or agricultural land), the £2.5 million combined cap fundamentally changes valuation approaches. Surveyors must now:

📊 Segregate qualifying and non-qualifying elements within mixed-use properties

📊 Calculate the effective IHT burden on values exceeding the threshold

📊 Adjust market value to reflect the tax disadvantage for buyers who will exceed the cap

📊 Consider alternative ownership structures that might preserve relief eligibility

For example, a £4 million agricultural property previously enjoying 100% APR now faces a £300,000 IHT liability on the £1.5 million excess (£1.5M × 40% × 50% relief = £300,000). This reduces the net value to heirs and should inform purchase price negotiations.

Our specialists in non-domicile tax valuation can provide detailed guidance on how these changes interact with international ownership structures.

Practical Valuation Strategies for Surveyors Facing £2M+ Threshold Fees

Implementing effective valuation strategies requires a systematic approach that balances technical accuracy with practical market realities. The following frameworks provide surveyors with actionable methodologies for navigating the post-budget 2026 landscape.

The Three-Tier Valuation Framework

Professional surveyors should adopt a three-tier approach when valuing properties near or above the £2 million threshold:

Tier 1: Base Market Value (Pre-Tax Consideration)

Establish the property's value using traditional comparable analysis, replacement cost, and income capitalization methods as appropriate. This provides the fundamental value baseline before tax considerations.

Tier 2: Tax-Adjusted Market Value

Apply adjustments reflecting the actual tax burden a typical buyer would face:

- SDLT surcharges for additional property purchases

- IHT implications for estates exceeding relief thresholds

- CGT considerations for properties with embedded gains

- Separated income tax rates for rental properties

Tier 3: Optimized Structure Value

Calculate the maximum value achievable through optimal ownership structures:

- Spousal transfers to maximize combined £5 million relief

- Corporate ownership for commercial properties

- Trust structures where appropriate

- Strategic timing of transactions

The difference between Tier 2 and Tier 3 values represents the value of tax planning, which sophisticated buyers increasingly demand.

Specialized Considerations for Different Property Types

Different property categories require tailored valuation approaches under the post-2026 tax regime:

🏡 Prime Residential Properties (£2M-£5M)

These properties face the most significant market impact from SDLT surcharges. Surveyors should:

- Weight comparables from the past 6 months most heavily

- Apply a 3-7% liquidity discount depending on location

- Document buyer resistance at specific price points

- Consider the impact of the £925,000 SDLT band threshold

🏢 Commercial Properties with Business Relief

Properties qualifying for BPR require careful analysis of:

- The proportion of value covered by the £2.5M allowance

- Alternative valuation approaches that might reduce assessable value

- The impact of the reduced trust rate (3% vs. 6%) for relevant property trusts[1]

🌾 Agricultural Properties

Agricultural estates face unique challenges under the combined APR/BPR cap:

- Segregate land value from buildings and equipment

- Consider farmhouse exemption rules

- Analyze the impact of foreign property scope expansion[1]

- Evaluate succession planning implications

🏘️ Rental Property Portfolios

Investment portfolios must now account for:

- Separated property income tax rates from April 2027[6]

- Reduced net yields affecting capitalization rates

- Portfolio restructuring opportunities

- The 10% SDLT surcharge on additional properties[7]

For comprehensive guidance on selecting the appropriate survey level for high-value properties, review our resource on what survey you need.

Documentation and Reporting Best Practices

Transparent documentation is essential when navigating post-budget 2026 tax hikes on high-value properties. Valuation reports should include:

✍️ Explicit tax assumption statements: Clearly state the assumed buyer profile and applicable tax position

✍️ Sensitivity analysis: Show how value varies under different tax scenarios

✍️ Market conditions commentary: Document the reduced transaction volumes and extended marketing periods

✍️ Comparable adjustment schedules: Detail all adjustments made to comparable evidence, including tax-related factors

✍️ Limitation of liability clauses: Specify that tax advice should be sought from qualified tax advisors

✍️ Compliance statements: Confirm adherence to RICS Red Book standards and relevant practice statements

When preparing reports for clients, surveyors should reference our guide on understanding the importance of survey home reports to help property owners appreciate the value of professional valuation services.

Leveraging Technology and Data Analytics

Modern surveyors have access to advanced analytical tools that can enhance valuation accuracy in the changed market environment:

📈 Transaction database analysis: Utilize comprehensive property databases to identify pre-budget and post-budget transaction patterns, quantifying the market impact with statistical precision.

📈 Tax modeling software: Implement specialized software that calculates tax implications across different ownership structures and buyer profiles.

📈 Geographic information systems: Map transaction density and price trends to identify micro-markets less affected by the tax changes.

📈 Automated valuation models (AVMs): Use AVMs as a cross-check against traditional valuation methods, particularly for properties with limited comparable evidence.

Our cost of valuation guide provides transparency on pricing for different valuation services, helping clients understand the investment required for comprehensive analysis.

Regional Variations and Location-Specific Strategies

The impact of the 2026 tax changes varies significantly by geographical location, requiring surveyors to develop location-specific expertise.

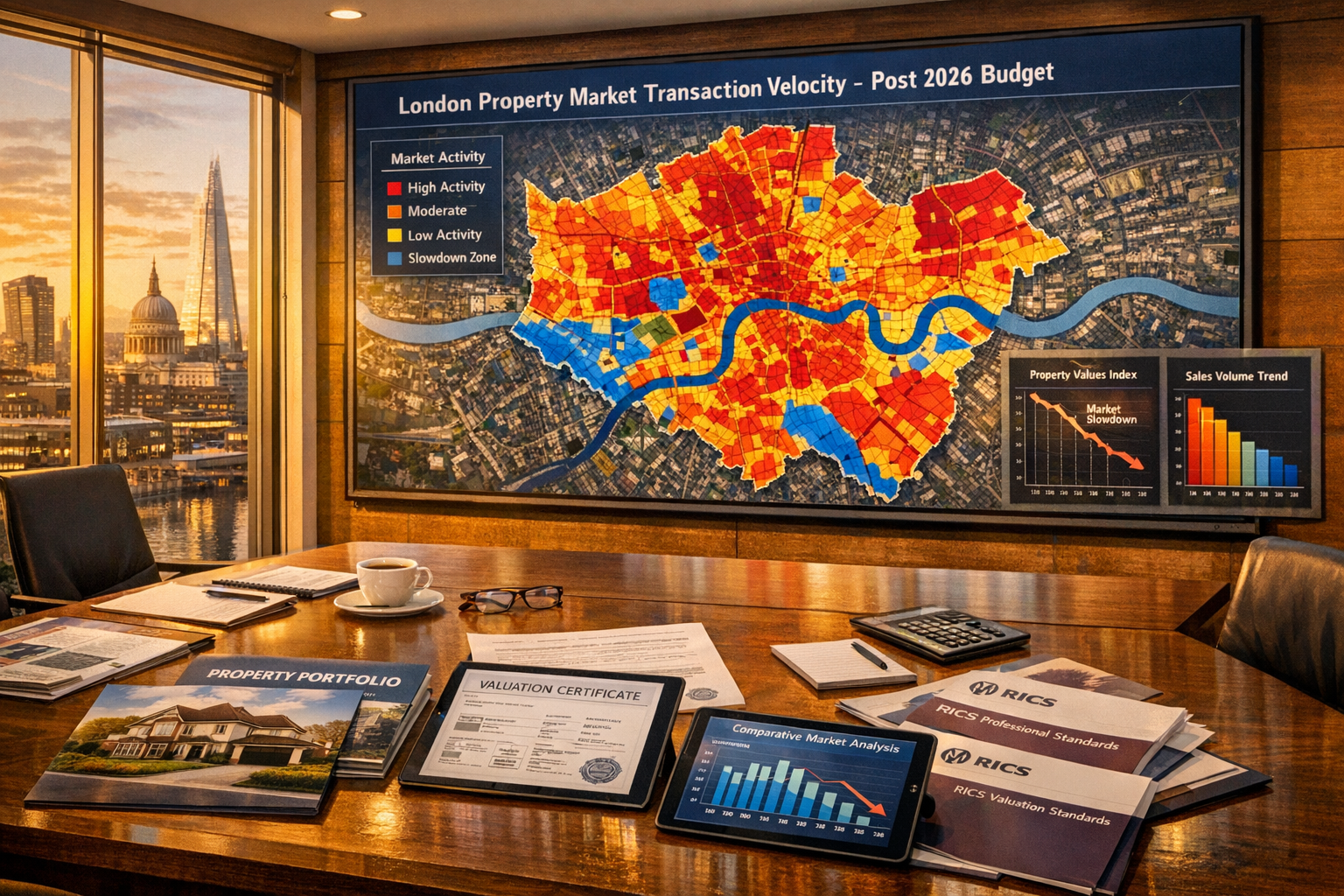

London and Prime Central Markets

London's prime property market has experienced the most pronounced slowdown following the budget changes. Properties in areas like Kensington, Chelsea, and Hampstead face:

- Extended marketing periods of 12-18 months for properties above £3 million

- Price reductions of 5-10% compared to pre-budget expectations

- Increased negotiation leverage for cash buyers who can move quickly

- Flight to quality as buyers focus on truly exceptional properties

Our chartered surveyors in Hampstead specialize in valuing properties in these premium markets and understand the nuanced factors affecting value.

Commuter Belt and Home Counties

Areas within commuting distance of London, including Surrey, Berkshire, and Buckinghamshire, show more resilient markets with:

- Shorter marketing periods than central London (6-9 months)

- Smaller price adjustments (2-5% below pre-budget levels)

- Continued demand from families seeking larger properties

- Less sensitivity to the £2 million threshold

Surveyors operating in these regions should consult our location-specific resources for chartered surveyors in Berkshire, Buckinghamshire, and Guildford.

Regional Cities and Secondary Markets

Markets outside the South East demonstrate varying degrees of impact:

- Limited effect on properties under £1.5 million

- Moderate impact on properties £1.5M-£3M

- Significant resistance above £3 million in most regional cities

- Opportunity zones where values remain attractive relative to London

Future-Proofing Valuation Practices

As the market continues to adjust to the 2026 tax changes, surveyors must anticipate further developments and prepare for ongoing evolution in valuation methodologies.

Monitoring Regulatory Changes

The tax landscape remains dynamic, with potential future adjustments including:

- 🔍 Modifications to relief thresholds based on revenue collection data

- 🔍 Changes to business rates revaluation cycles

- 🔍 Adjustments to SDLT bands and rates

- 🔍 Refinements to the separated property income tax structure

Surveyors should maintain active membership in professional organizations like RICS and participate in continuing professional development (CPD) focused on tax implications for property valuation.

Building Specialist Tax Knowledge

While surveyors are not tax advisors, developing working knowledge of tax principles enables more informed valuations. Consider:

- Partnering with tax advisory firms for complex cases

- Attending tax-focused property seminars

- Reviewing HMRC guidance on property taxation

- Understanding trust and estate planning basics

Adapting to Market Evolution

The high-value property market will continue evolving in response to the tax changes. Successful surveyors will:

- Track market sentiment through regular client consultations

- Analyze transaction data quarterly to identify emerging trends

- Adjust valuation models as new comparable evidence becomes available

- Communicate proactively with clients about market conditions

For surveyors seeking to expand their expertise, our comprehensive guide to what is a property surveyor provides foundational knowledge on professional roles and responsibilities.

Conclusion

Navigating post-budget 2026 tax hikes on high-value properties requires surveyors to fundamentally rethink valuation strategies for properties facing £2M+ threshold fees. The combined £2.5 million cap on APR and BPR, enhanced SDLT surcharges, increased BADR rates, and separated property income tax bands have created a transformed market landscape where tax efficiency drives purchasing decisions as much as property characteristics.

Professional surveyors must adopt RICS-aligned methodologies that incorporate these tax implications while maintaining technical rigor and independence. The three-tier valuation framework—establishing base market value, applying tax adjustments, and calculating optimized structure value—provides a systematic approach to delivering accurate valuations in this changed environment.

Key action steps for surveyors include:

- Expand comparable analysis to account for reduced transaction volumes in the £2M+ segment

- Document market conditions thoroughly to support valuation conclusions and defend against challenges

- Develop location-specific expertise recognizing that impact varies significantly by geographical market

- Invest in technology and data analytics to enhance valuation accuracy and efficiency

- Build collaborative relationships with tax advisors to better serve clients with complex holdings

- Commit to ongoing professional development as the tax and regulatory landscape continues evolving

The prime property market slowdown presents both challenges and opportunities for skilled surveyors. Those who master the technical complexities of valuing high-value properties in the post-2026 tax environment will position themselves as indispensable advisors to clients navigating these wealth taxes.

For professional valuation services that account for the latest tax implications and market conditions, contact our chartered surveyors who specialize in high-value property assessments across London and the South East.

References

[1] Uk Tax Landscape Key Changes For 2026 – https://taxscape.deloitte.com/article/uk-tax-landscape–key-changes-for-2026.aspx

[2] 10 Key Tax Changes April 2026 – https://www.armstrongwatson.co.uk/news/2026/03/10-key-tax-changes-april-2026

[3] How Property Taxes Contributed To The Uks Record Budget Surplus – https://davidturnbull.exp.uk.com/2026/02/26/how-property-taxes-contributed-to-the-uks-record-budget-surplus/

[4] Watch – https://www.youtube.com/watch?v=APQWNMqcyLs

[5] March 2026 Tax News – https://www.wilson-partners.co.uk/latest-news/tax/march-2026-tax-news/

[6] Changes To Tax Rates For Property Savings And Dividend Income – https://www.gov.uk/government/publications/changes-to-tax-rates-for-property-savings-and-dividend-income

[7] November 2026 Budget And What It Could Mean For Landlords – https://uklandlordtax.co.uk/november-2026-budget-and-what-it-could-mean-for-landlords/