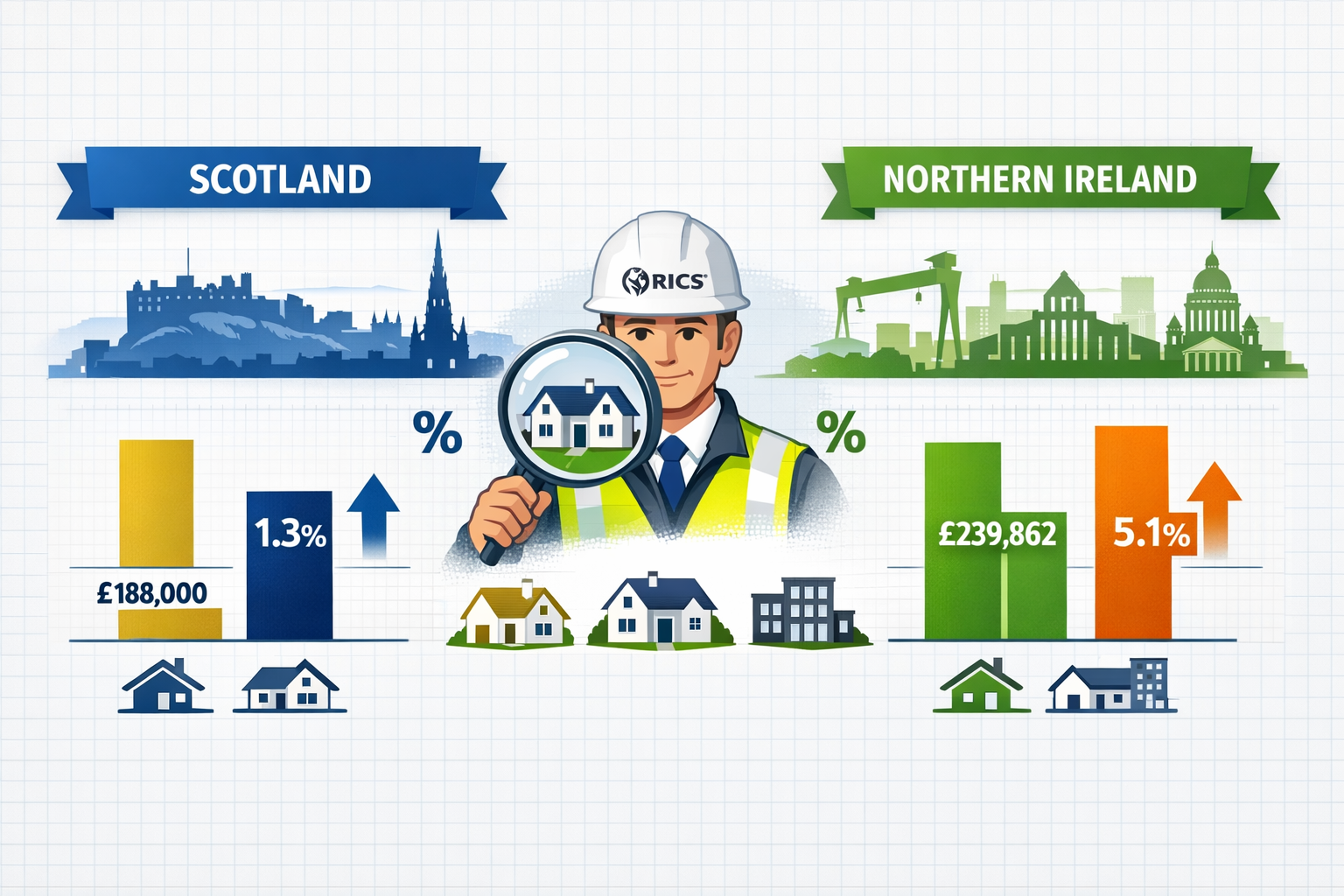

The UK property market landscape has shifted dramatically in 2026, with Scotland and Northern Ireland emerging as unexpected leaders in regional price momentum. While London and the South East traditionally dominated property valuations, RICS data from January 2026 reveals a compelling story: Northern Ireland house prices surged 5.1% year-on-year to reach £239,862, while Scotland's more modest 1.3% growth to £188,000 still presents unique opportunities for savvy investors and surveyors [4][2]. Understanding the Valuation Techniques for Scotland and Northern Ireland's 2026 Price Momentum: Regional Outperformance Strategies has become essential for property professionals seeking to capitalize on these emerging markets.

This fundamental shift requires surveyors, investors, and property professionals to recalibrate their valuation methodologies and comparable analysis tactics. The traditional London-centric approach no longer captures the full picture of UK property performance.

Key Takeaways

✅ Northern Ireland leads UK growth: Property prices increased 5.1% year-on-year in January 2026, with Derry City and Strabane showing exceptional 13.0% gains [4][1]

✅ Regional variation demands specialized valuation: Scotland's £188,000 average masks significant geographic disparities, from Edinburgh's £294,000 to Inverclyde's £115,000 [2]

✅ New builds outperform resales: Scotland's new construction properties gained 5.2% annually versus 0.0% for existing homes, requiring different valuation approaches [2]

✅ Affordability drives momentum: Northern Ireland first-time buyer mortgage payments (£790/month) now undercut equivalent rents (£894/month), fueling demand [4]

✅ Interest rate environment supports growth: Expected further rate cuts throughout 2026 will continue improving mortgage affordability in both regions [1]

Understanding the 2026 Regional Price Momentum Shift

The Northern Ireland Surge

Northern Ireland's property market has experienced remarkable transformation throughout 2025 and into 2026. The region led all UK territories with 9.7% annual price growth in 2025 according to Nationwide data [6]. This momentum continued into 2026, with January figures showing the average house price reaching £239,862, representing a substantial £14,000 increase from the previous year [4].

This growth pattern differs significantly from historical trends. Several key factors drive this exceptional performance:

Supply-demand imbalance: Property enquiries grew 13% year-on-year in January 2026, while new listings remained constrained [4]. This fundamental shortage creates upward price pressure that surveyors must account for in their commercial valuation and residential assessments.

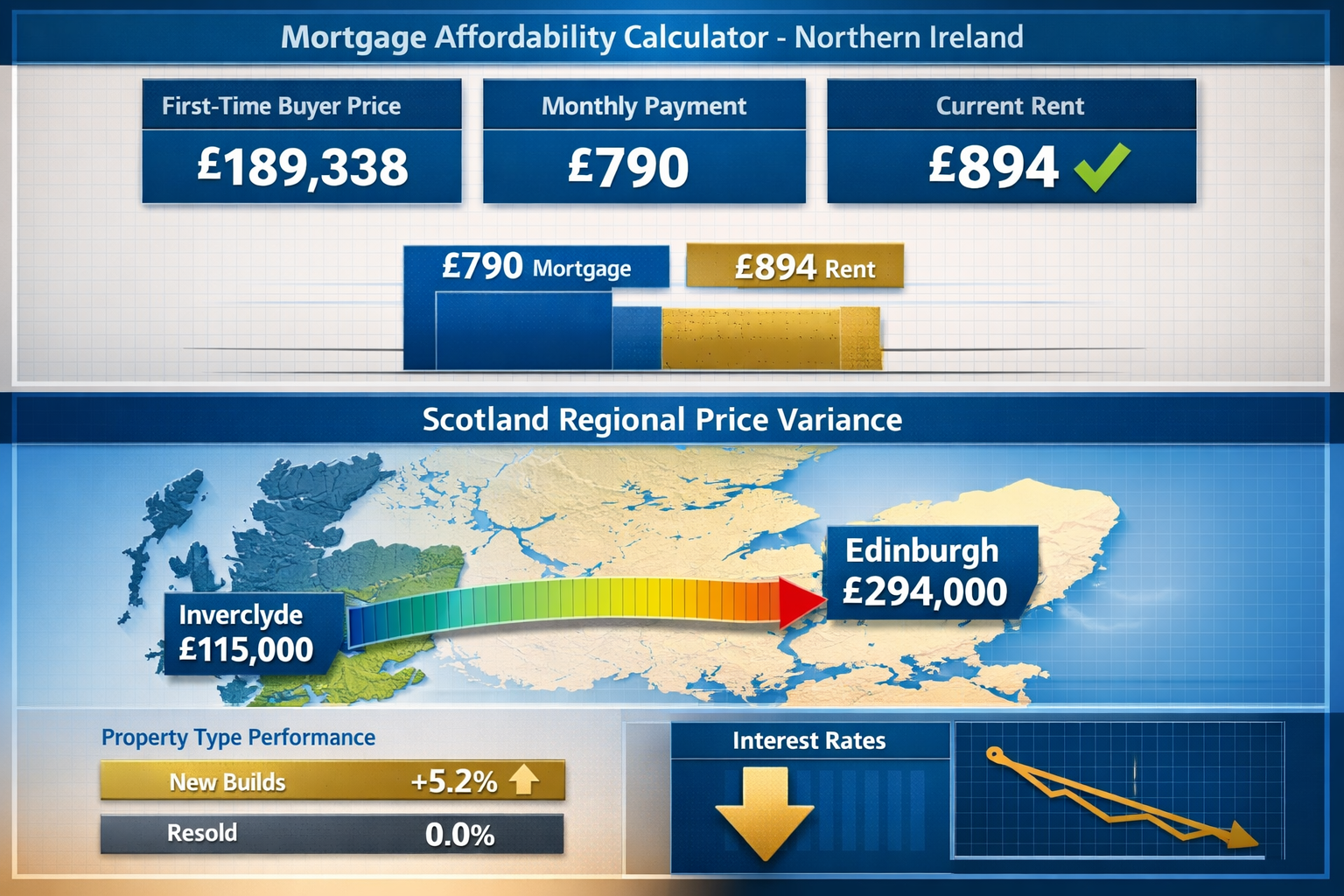

Mortgage affordability advantage: First-time buyers in Northern Ireland now face monthly mortgage repayments of £790 compared to equivalent rental costs of £894 [4]. This £104 monthly saving makes homeownership financially attractive, expanding the buyer pool and supporting price growth.

Regional economic stability: Unlike volatile markets in the South East, Northern Ireland's steady economic performance provides confidence for both buyers and lenders, reducing risk premiums in property valuations.

Scotland's Nuanced Market Performance

Scotland presents a more complex picture for valuation professionals. The headline figure of £188,000 average house price with 1.3% annual growth masks significant geographic and property-type variations that require sophisticated analysis [2].

Property type performance reveals important distinctions:

| Property Type | Average Price (Jan 2026) | Annual Change |

|---|---|---|

| Detached | £341,134 | -0.2% |

| Semi-detached | £212,267 | +1.8% |

| Terraced | £166,645 | +1.4% |

| Flats | £133,629 | +1.4% |

The new build premium stands out dramatically. New construction properties in Scotland appreciated 5.2% annually, while resold existing properties showed 0.0% growth [2]. This divergence requires surveyors to apply different comparable selection criteria and adjustment factors when conducting Red Book valuations.

Geographic price variation within Scotland demands localized expertise:

- Edinburgh (City of Edinburgh): £294,000 average (highest)

- East Renfrewshire: £268,000

- East Dunbartonshire: £253,000

- Inverclyde: £115,000 (lowest)

- North Ayrshire: £128,000

This £179,000 spread between highest and lowest markets represents a 61% price differential that fundamentally impacts valuation methodology [2].

Core Valuation Techniques for Scotland and Northern Ireland's 2026 Price Momentum

Comparable Sales Analysis with Regional Adjustments

The foundation of property valuation remains the comparable sales approach, but applying this technique to Scotland and Northern Ireland's 2026 markets requires sophisticated regional adjustments that reflect current momentum.

Time-based adjustments: With Northern Ireland experiencing 5.1% annual growth, comparable sales from just six months ago require upward adjustment of approximately 2.5% to reflect current market conditions [4]. Scotland's slower 1.3% growth demands more modest time adjustments, but the new build versus resale distinction creates complexity.

Geographic micro-market analysis: Within Northern Ireland, regional performance varies dramatically:

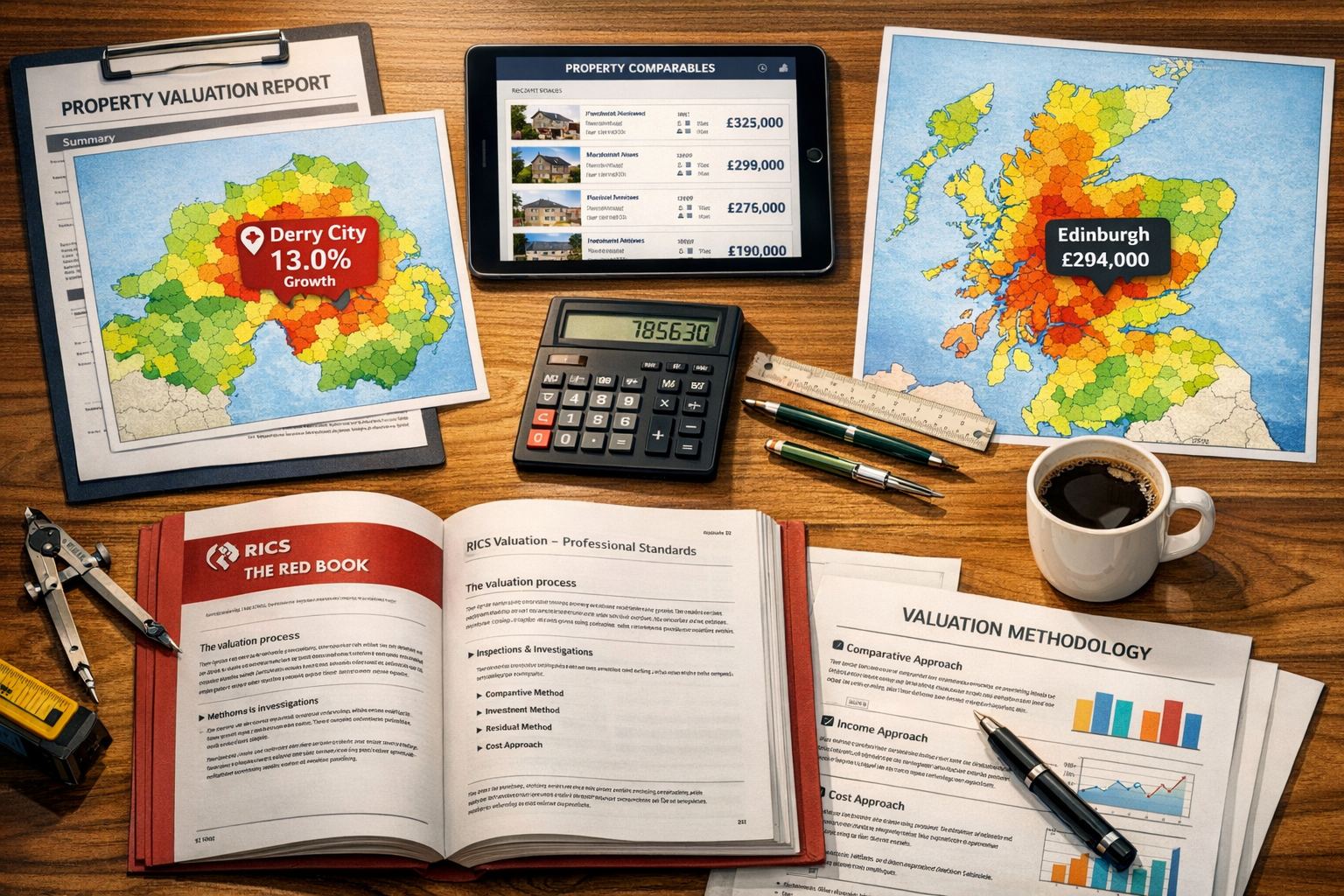

- Derry City and Strabane: +13.0% annual growth

- Mid Ulster: +11.2% annual growth

- Ards and North Down: +8.6% annual growth

- Belfast: More moderate growth rates

Surveyors conducting valuation types assessments must select comparables from the appropriate micro-market or apply substantial location adjustments when crossing regional boundaries [1].

Property condition and age premiums: The new build premium in Scotland (5.2% growth versus 0.0% for resales) suggests buyers place significant value on modern construction standards, energy efficiency, and warranty protection [2]. When valuing existing properties, surveyors should consider:

- Energy Performance Certificate (EPC) ratings and potential upgrade costs

- Remaining warranty coverage (NHBC or equivalent)

- Modern building standards compliance

- Maintenance and refurbishment requirements

Income Capitalization for Investment Properties

The affordability advantage in Northern Ireland creates compelling opportunities for buy-to-let investors, making income capitalization techniques particularly relevant for 2026 valuations.

Rental yield analysis: With average rents at £894 monthly and purchase prices averaging £239,862, Northern Ireland properties generate gross rental yields of approximately 4.5% [4]. This compares favorably to many UK markets where yields have compressed below 4%.

For investment property valuations, surveyors should:

- Calculate net operating income by deducting realistic expense estimates (property management, maintenance, insurance, void periods)

- Apply appropriate capitalization rates reflecting regional risk profiles and growth expectations

- Adjust for tenant demand patterns specific to each micro-market

- Consider mortgage serviceability at current interest rates with expected further cuts [1]

Commercial property considerations: Scotland and Northern Ireland commercial markets require specialized analysis. Our commercial valuation services incorporate regional economic indicators, employment trends, and sector-specific performance metrics that differ substantially from residential patterns.

Cost Approach for New Development

The strong performance of new builds in both regions makes the cost approach particularly relevant for development site valuations and new construction assessments [2].

Key components include:

Land value assessment: Development land values have appreciated alongside finished property prices. In high-growth areas like Derry City and Strabane (13.0% growth), land values may have increased even more rapidly than finished properties [1].

Construction cost inflation: Building material and labor costs must reflect 2026 market conditions. Scotland and Northern Ireland face different cost structures than South East England, requiring regional cost databases and local contractor consultation.

Developer profit margins: In strong growth markets, developers can command higher profit margins. Northern Ireland's momentum supports 15-20% profit margins versus 10-15% in slower markets, impacting residual land valuations.

Planning and regulatory factors: Scotland's distinct planning framework and building regulations differ from Northern Ireland's system. Surveyors must understand jurisdiction-specific requirements when applying cost approaches.

Regional Outperformance Strategies for Property Professionals

Identifying High-Growth Micro-Markets

Successfully implementing Valuation Techniques for Scotland and Northern Ireland's 2026 Price Momentum: Regional Outperformance Strategies requires identifying specific locations poised for continued outperformance.

Northern Ireland hotspots: The data reveals clear winners for 2026:

🏆 Derry City and Strabane leads with 13.0% growth, driven by economic regeneration, improved infrastructure, and relative affordability compared to Belfast [1]

🏆 Mid Ulster follows at 11.2%, benefiting from strong local employment and family-friendly communities

🏆 Ards and North Down at 8.6% growth attracts buyers seeking coastal lifestyle with Belfast accessibility

Surveyors should prioritize these areas for valuation factors analysis, as momentum typically persists for 12-18 months once established.

Scotland's opportunity zones: While overall growth remains modest at 1.3%, specific segments show promise:

- New build developments across all regions (+5.2% growth) [2]

- Semi-detached properties (+1.8%) outperform detached homes (-0.2%)

- Affordable price points below £200,000 show stronger demand

- Commuter towns near Edinburgh and Glasgow with lower entry prices

Strategic positioning: Property professionals should:

- Build comparable databases focused on high-growth micro-markets

- Develop relationships with local estate agents in target areas

- Monitor planning applications for new development activity

- Track employment and infrastructure investment announcements

- Understand local authority housing strategies and targets

Leveraging Affordability Trends

The mortgage-to-rent advantage in Northern Ireland represents a fundamental shift in market dynamics that savvy professionals can exploit [4].

First-time buyer focus: With monthly mortgage payments (£790) now £104 cheaper than renting (£894), first-time buyers represent the most active market segment. Valuation strategies should consider:

- Properties priced at typical first-time buyer budgets (£180,000-£200,000)

- Locations with strong rental markets providing exit strategies

- Property types suitable for young families and professionals

- Proximity to employment centers and transport links

Investment property targeting: The affordability gap creates buy-to-let opportunities where investors can:

- Purchase properties generating positive cash flow from day one

- Benefit from capital appreciation in high-growth areas

- Build portfolios in markets with strong tenant demand

- Leverage mortgage products with improving interest rates [1]

Shared ownership opportunities: Both regions offer shared ownership valuation prospects where affordability constraints limit full ownership. These hybrid products require specialized valuation techniques accounting for:

- Initial equity share percentages

- Rent charged on retained equity

- Staircasing provisions and future purchase options

- Housing association policies and restrictions

Adapting to Interest Rate Environment

The anticipated further interest rate cuts throughout 2026 create both opportunities and challenges for property valuations [1].

Mortgage affordability modeling: Surveyors conducting Help to Buy valuations should model multiple rate scenarios:

- Current rates (~4.5-5.0% for typical mortgages)

- Post-cut scenarios (potentially 4.0-4.5% by year-end)

- Impact on maximum borrowing capacity

- Monthly payment changes and buyer purchasing power

Valuation sensitivity analysis: Professional valuation reports should include sensitivity analysis showing how property values might respond to:

- 0.25% rate reduction (expected)

- 0.50% rate reduction (possible)

- Unexpected rate increases (risk scenario)

- Changes in lending criteria or deposit requirements

Regional impact differences: Interest rate changes affect markets differently:

- Northern Ireland may see accelerated growth as affordability improves further

- Scotland could experience stronger momentum, particularly in new builds

- High-priced segments (Edinburgh detached homes) may benefit most from rate cuts

- Investment properties become more attractive as financing costs decrease

Property Type Specialization Strategies

The divergent performance by property type suggests specialization opportunities for surveyors and investors [2].

New build focus in Scotland: The 5.2% growth premium for new construction creates several strategic approaches:

- Development site acquisition: Identify land parcels suitable for residential development in areas with planning support

- Off-plan purchasing: Advise clients on purchasing during construction phases to capture appreciation

- Partnership opportunities: Work with developers requiring RICS Help to Buy valuations and scheme compliance

- Energy efficiency premium: Emphasize EPC A-rated properties commanding price premiums

Semi-detached and flat opportunities: These property types show consistent positive growth in Scotland (+1.8% and +1.4% respectively), while detached homes declined [2]. This suggests:

- Middle-market properties attract strongest demand

- Family homes in £200,000-£300,000 range perform well

- Apartment markets in city centers remain resilient

- Detached homes may offer value opportunities if growth returns

Northern Ireland property type analysis: With one-bed apartments averaging £177,593 and three-bed apartments at £527,681, significant price stratification exists [4]. Surveyors should:

- Understand which property types suit specific buyer demographics

- Recognize the substantial premium for larger apartments

- Consider new build apartments (£270,782 average) versus resales

- Evaluate conversion and renovation opportunities

Advanced Valuation Methodologies for 2026 Markets

Data-Driven Comparable Selection

Modern valuation techniques increasingly rely on sophisticated data analysis rather than traditional "rule of thumb" approaches.

Statistical modeling: Advanced surveyors now employ regression analysis to identify which property characteristics most significantly impact values in Scotland and Northern Ireland:

- Location (postcode-level granularity)

- Property size (square footage, number of bedrooms)

- Property age and condition

- EPC rating and energy costs

- Proximity to amenities and transport

- Recent comparable sales within specific timeframes

Automated Valuation Models (AVMs): While not replacing professional judgment, AVMs provide useful benchmarks when calibrated for regional markets. Surveyors should:

- Use AVMs as initial screening tools

- Understand model limitations in thin markets

- Adjust AVM outputs based on local knowledge

- Combine automated and manual approaches

Market trend integration: Effective valuation factors analysis incorporates forward-looking indicators:

- Planning applications and approved developments

- Infrastructure investment announcements

- Employment growth projections

- Population migration patterns

- Government housing policy changes

Hybrid Valuation Approaches

The complexity of Scotland and Northern Ireland's 2026 markets often requires combining multiple valuation methodologies for comprehensive assessments.

Comparable + Income hybrid: For properties with investment potential, reconcile:

- Market value based on comparable sales analysis

- Investment value based on income capitalization

- Weighted average reflecting property's likely buyer profile

Cost + Market hybrid: For new builds and recent construction:

- Replacement cost less depreciation

- Market value from new build comparables

- Analysis of any value gap indicating market premium or discount

Scenario-based valuation: Given market momentum and interest rate uncertainty, sophisticated valuations present multiple scenarios:

- Base case: Current market conditions continue

- Optimistic case: Further rate cuts accelerate growth

- Conservative case: Economic headwinds slow momentum

- Probability-weighted value: Combining scenarios with likelihood estimates

Regulatory Compliance and Professional Standards

All valuation work in Scotland and Northern Ireland must adhere to RICS Valuation – Global Standards (Red Book) and jurisdiction-specific requirements.

Red Book compliance: Professional surveyors conducting Red Book valuations must ensure:

- Clear terms of engagement defining scope and purpose

- Appropriate valuation basis (Market Value, Investment Value, etc.)

- Competence and independence declarations

- Adequate inspection and investigation

- Proper comparable analysis and adjustments

- Clear reporting with assumptions and limitations stated

Scotland-specific considerations: Scottish property law differs from England and Wales:

- Home Report requirements for residential sales

- Different conveyancing processes

- Distinct planning and building regulations

- Scottish Land and Buildings Transaction Tax (LBTT)

Our guide on home report costs provides detailed information on Scottish requirements.

Northern Ireland distinctions: The Northern Ireland market operates under separate legal frameworks:

- Different stamp duty land tax structures

- Distinct planning system

- Separate professional bodies and regulations

- Unique market practices and conventions

Risk Management in High-Growth Regional Markets

Identifying Valuation Risks

While Scotland and Northern Ireland show strong momentum, professional surveyors must recognize and communicate potential risks.

Market correction risk: Rapid price growth (particularly Northern Ireland's 13.0% in some areas) may not be sustainable long-term [1]. Prudent valuations should:

- Avoid over-reliance on very recent comparables

- Consider longer-term price trends

- Identify potential market overheating indicators

- Communicate sustainability concerns to clients

Economic dependency risks: Regional economies face specific vulnerabilities:

- Northern Ireland's exposure to UK-EU trade dynamics

- Scotland's economic links to oil/gas sector performance

- Public sector employment concentration in some areas

- Demographic challenges in rural locations

Property-specific risks: Individual properties may face issues affecting value:

- Building defects or maintenance requirements

- Environmental concerns or contamination

- Planning restrictions or development limitations

- Tenure issues or title complications

Portfolio Diversification Strategies

Investors and institutions seeking exposure to Scotland and Northern Ireland's growth should employ diversification strategies to manage risk.

Geographic diversification: Spread investments across:

- Multiple micro-markets within each region

- Both Scotland and Northern Ireland

- Urban and suburban locations

- Established and emerging areas

Property type diversification: Balance portfolios with:

- Mix of new builds and quality resales

- Different property sizes and configurations

- Residential and commercial properties

- Various price points and buyer demographics

Timing diversification: Avoid concentration risk by:

- Phasing acquisitions over 12-24 months

- Building positions gradually as market develops

- Maintaining reserves for opportunistic purchases

- Planning exit strategies with multiple timeframes

Implementation Framework for Property Professionals

Building Regional Expertise

Successful application of Valuation Techniques for Scotland and Northern Ireland's 2026 Price Momentum: Regional Outperformance Strategies requires developing deep local knowledge.

Market intelligence systems: Establish processes for:

- Regular monitoring of regional price indices and reports

- Relationships with local estate agents and developers

- Attendance at property auctions and viewings

- Subscription to regional property databases

- Networking with local surveyors and professionals

Continuing professional development: Stay current through:

- RICS regional events and training

- Local property market seminars

- Economic development briefings

- Planning authority consultations

- Industry publications and research

Technology adoption: Leverage modern tools:

- Geographic Information Systems (GIS) for spatial analysis

- Property database platforms with regional filtering

- Automated alert systems for comparable sales

- Digital inspection and reporting tools

- Client communication and collaboration platforms

Client Advisory Services

Beyond technical valuation, property professionals should provide strategic advisory services helping clients capitalize on regional opportunities.

Investment strategy consulting: Guide clients on:

- Optimal property types for their objectives

- Geographic targeting within Scotland and Northern Ireland

- Timing considerations and market entry strategies

- Financing structures and mortgage products

- Tax planning and ownership structures

Portfolio optimization: For existing property owners:

- Review current holdings against regional performance

- Identify underperforming assets for disposal

- Recommend strategic acquisitions

- Rebalance geographic and property type allocations

- Maximize returns through active management

Development advisory: Support developers and landowners:

- Site selection and acquisition advice

- Feasibility studies and viability assessments

- Planning strategy and risk assessment

- Commercial property surveys for mixed-use schemes

- Exit strategy planning and marketing advice

Quality Assurance and Professional Standards

Maintaining high professional standards protects both clients and surveyors' reputations.

Valuation review processes: Implement internal quality controls:

- Peer review of significant valuations

- Comparable verification procedures

- Adjustment methodology documentation

- Assumption testing and sensitivity analysis

- Regular calibration against actual sales

Professional indemnity insurance: Ensure adequate coverage for:

- Regional valuation work

- Property types and values handled

- Advisory services provided

- Retroactive coverage for prior work

- Appropriate policy limits and deductibles

Complaints and dispute procedures: Establish clear processes for:

- Client feedback and satisfaction monitoring

- Complaint handling and investigation

- Professional standards compliance

- Continuing improvement initiatives

- Documentation and record retention

Future Outlook: Sustaining Regional Momentum

2026-2027 Market Projections

While predicting property markets involves uncertainty, several factors suggest continued outperformance potential for Scotland and Northern Ireland.

Supporting factors:

- Interest rate trajectory: Expected further cuts throughout 2026 will improve affordability [1]

- Supply constraints: Limited new construction continues supporting prices

- Relative affordability: Both regions remain cheaper than UK average

- Economic stability: Steady regional economies provide confidence

- Infrastructure investment: Government spending supports local markets

Potential headwinds:

- Economic recession risk: UK-wide downturn would impact all regions

- Mortgage availability: Lending criteria changes could restrict demand

- Political uncertainty: Constitutional questions affect long-term confidence

- Overheating concerns: Rapid growth may trigger correction

- Demographic trends: Population aging in some areas limits buyer pools

Realistic expectations: Professional surveyors should guide clients toward:

- Moderate growth expectations (3-5% annually) rather than 2025's exceptional rates

- Long-term investment horizons (5+ years)

- Focus on fundamentals (location, property quality, tenant demand)

- Risk management and diversification

- Regular portfolio review and rebalancing

Emerging Opportunities

Forward-thinking property professionals can position for next-generation opportunities in these regional markets.

Sustainability and energy efficiency: With new builds outperforming in Scotland, the energy efficiency premium will likely strengthen:

- Retrofit and renovation opportunities for existing stock

- Green financing products supporting improvements

- EPC rating enhancement strategies

- Renewable energy integration (solar, heat pumps)

- Net-zero carbon property development

Technology integration: Smart home technology and digital infrastructure increasingly influence values:

- High-speed broadband availability

- Smart home systems and automation

- Security and monitoring technology

- Energy management systems

- Electric vehicle charging infrastructure

Demographic shifts: Understanding changing buyer preferences:

- Remote working enabling location flexibility

- Downsizing demand from aging population

- First-time buyer focus on affordability

- Multi-generational living arrangements

- Lifestyle and amenity priorities

Alternative property uses: Creative approaches to property investment:

- Residential conversion opportunities

- Mixed-use development potential

- Short-term letting and holiday homes

- Build-to-rent schemes

- Co-living and shared housing models

Conclusion

The Valuation Techniques for Scotland and Northern Ireland's 2026 Price Momentum: Regional Outperformance Strategies represent a fundamental shift in UK property market dynamics. Northern Ireland's exceptional 5.1% annual growth to £239,862 average prices, combined with specific micro-markets like Derry City and Strabane achieving 13.0% gains, demonstrates genuine regional outperformance [4][1]. Scotland's more modest 1.3% overall growth masks significant opportunities in new builds (+5.2%) and specific property types that savvy professionals can exploit [2].

Successful property valuation in these markets requires sophisticated regional expertise that goes beyond traditional London-centric approaches. Surveyors must understand:

✅ Micro-market dynamics within each region, recognizing that average figures mask significant local variation

✅ Property type performance differences, particularly the new build premium in Scotland and affordability advantages in Northern Ireland

✅ Affordability trends driving first-time buyer demand, with mortgage payments now undercutting rents in Northern Ireland

✅ Interest rate sensitivity and how anticipated further cuts will impact buyer purchasing power and market momentum

✅ Regional regulatory frameworks including Scotland's Home Report requirements and Northern Ireland's distinct legal structures

The strategic opportunities for property professionals, investors, and homebuyers in 2026 are substantial. By applying rigorous comparable analysis with appropriate regional adjustments, leveraging income capitalization for investment properties, and understanding cost approaches for new development, surveyors can provide exceptional value to clients navigating these dynamic markets.

Actionable Next Steps

For property professionals seeking to capitalize on Scotland and Northern Ireland's momentum:

-

Build regional expertise through market intelligence systems, local relationships, and continuing professional development focused on these specific markets

-

Develop specialized capabilities in high-growth property types (new builds, semi-detached homes, investment properties) and geographic areas (Derry City, Mid Ulster, Edinburgh suburbs)

-

Implement robust valuation methodologies combining comparable sales analysis, income capitalization, and cost approaches with appropriate regional adjustments and sensitivity analysis

-

Establish quality assurance processes ensuring Red Book compliance, peer review, and professional standards that protect both clients and your reputation

-

Provide strategic advisory services beyond technical valuation, helping clients with investment strategy, portfolio optimization, and development advisory

-

Monitor market indicators continuously, tracking price trends, interest rate changes, planning applications, and economic developments affecting regional performance

-

Manage risks appropriately through diversification strategies, realistic growth expectations, and clear communication of market uncertainties to clients

The regional outperformance of Scotland and Northern Ireland in 2026 represents more than a temporary market anomaly—it reflects fundamental shifts in affordability, supply-demand dynamics, and buyer preferences that professional surveyors must understand and incorporate into their practice. Whether conducting Red Book valuations, commercial property assessments, or shared ownership valuations, regional expertise and sophisticated analytical techniques will differentiate successful professionals in these evolving markets.

By mastering the Valuation Techniques for Scotland and Northern Ireland's 2026 Price Momentum: Regional Outperformance Strategies outlined in this guide, property professionals position themselves at the forefront of UK market developments, delivering superior outcomes for clients while building sustainable competitive advantages in their practices.

References

[1] Article – https://www.sutherlandreay.com/blog/article.html?id=1772635696

[2] Uk House Price Index Scotland January 2026 – https://www.gov.uk/government/statistics/uk-house-price-index-for-january-2026/uk-house-price-index-scotland-january-2026

[3] Northern Ireland Property Market In 2026 Why Now Is A Good Time To Sell – https://www.reedsrains.co.uk/blog/northern-ireland-property-market-in-2026-why-now-is-a-good-time-to-sell

[4] Northern Ireland House Prices Up 5 In January 2026 Propertypal – https://theintermediary.co.uk/2026/02/northern-ireland-house-prices-up-5-in-january-2026-propertypal/

[5] Ni House Price Index Statistical Reports – https://www.finance-ni.gov.uk/publications/ni-house-price-index-statistical-reports

[6] House Prices – https://moneyweek.com/investments/house-prices/house-prices

[7] February2026 – https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/privaterentandhousepricesuk/february2026