The property market in 2026 presents a unique opportunity that hasn't existed for years: wages are finally outpacing house price growth in key regions across the UK. For first-time buyers who have watched affordability slip away year after year, this represents a genuine window to enter the market with improved negotiating power and strategic valuation advantages. Understanding how to leverage these Valuation Strategies for First-Time Buyers in 2026: Leveraging Affordability Gains and Regional Price Variations can mean the difference between overpaying and securing exceptional value.

With house prices growing at just 2% in Scotland and Northern England while wages climb faster, combined with mortgage rates stabilizing around 6.25% and improving inventory levels, first-time buyers who employ RICS-backed valuation tactics can recalibrate their approach to property acquisition.[2] This comprehensive guide explores how to capitalize on regional price variations, negotiate from a position of strength, and implement professional valuation strategies that protect your investment.

Key Takeaways

- Wage growth is outpacing house price increases in Scotland and Northern England, creating improved affordability conditions for first-time buyers in 2026

- RICS valuation strategies help buyers identify genuine market value and negotiate effectively in regions with varying price dynamics

- Builder incentives currently stand at 65%, offering first-time buyers significant valuation advantages through rate buy-downs, closing cost assistance, and upgraded finishes[1]

- Seasonal timing matters: purchasing in Q1 2026 provides lower pricing compared to spring/summer peaks, though competition may increase

- Professional surveys and valuations are essential tools for leveraging improved buyer negotiating power in the current market environment

Understanding the 2026 Market Shift: Affordability Gains and Regional Dynamics

The Wage-to-Price Growth Advantage

For the first time in nearly a decade, real wages are growing faster than property prices in several UK regions. This fundamental shift creates genuine affordability improvements, particularly in Scotland and Northern England where house price growth has moderated to approximately 2% annually while wage increases have accelerated beyond this rate.

This economic recalibration means that first-time buyers' purchasing power is actually improving rather than deteriorating. The debt-to-income ratios that determine mortgage eligibility are becoming more favorable, and the percentage of annual income required for deposits is gradually declining in these regions.

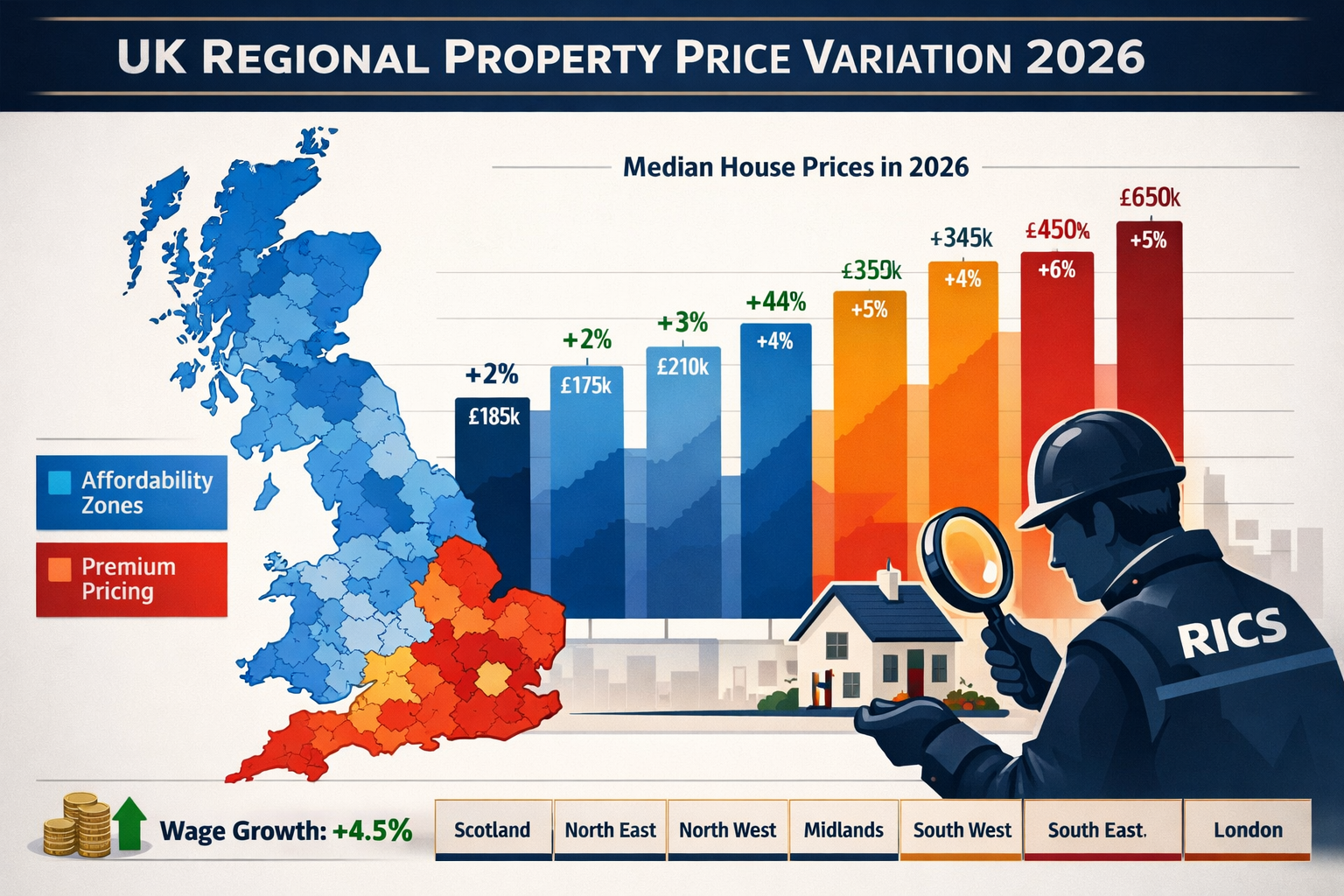

Regional Price Variation Patterns in 2026

The UK property market has never been more geographically fragmented. Understanding these regional price variations is essential for implementing effective valuation strategies:

| Region | Average Price Growth | Affordability Index | First-Time Buyer Advantage |

|---|---|---|---|

| Scotland | 2.0% | Improving ✅ | High negotiating power |

| Northern England | 2.1% | Improving ✅ | Strong buyer position |

| Midlands | 3.2% | Stable | Moderate advantages |

| Southeast | 4.5% | Declining ⚠️ | Limited leverage |

| London | 5.1% | Declining ⚠️ | Competitive market |

This geographical disparity creates strategic opportunities for first-time buyers willing to consider locations where affordability gains are most pronounced. Working with chartered surveyors in regions like North West London or Hertfordshire can help identify pockets of value even within higher-priced areas.

Mortgage Rate Environment and Valuation Impact

Mortgage rates in 2026 are expected to remain relatively stable in the low 6% range, with most buyers securing rates around 6.25% throughout the year.[2] While this is higher than the historic lows of previous years, the stability allows for more predictable valuation calculations and affordability planning.

This rate environment affects valuation strategies in several ways:

- Monthly payment calculations are more predictable for budgeting purposes

- Seller expectations have adjusted to the higher rate environment, reducing inflated pricing

- Rate buy-down incentives from builders become more valuable as permanent rate reductions

- Affordability assessments by lenders are more stringent, requiring accurate property valuations

Core Valuation Strategies for First-Time Buyers in 2026: RICS-Backed Approaches

Professional RICS Valuations: Your Foundation

The cornerstone of any effective valuation strategy is obtaining a professional assessment from a RICS-qualified surveyor. These independent valuations provide objective market value assessments that protect first-time buyers from overpaying in any market condition.

RICS valuations serve multiple critical purposes:

- Mortgage lender confidence: Ensures the property value supports the loan amount

- Negotiation leverage: Provides evidence-based justification for price reductions

- Investment protection: Identifies overpricing before commitment

- Regional context: Incorporates local market conditions and comparable sales data

For first-time buyers navigating Valuation Strategies for First-Time Buyers in 2026: Leveraging Affordability Gains and Regional Price Variations, a Red Book valuation provides the gold standard assessment recognized by all UK lenders and legal professionals.

Comparative Market Analysis in Regional Contexts

Understanding how your target property compares to recent sales in the specific region is fundamental to effective valuation. In 2026, this requires granular regional analysis rather than broad national trends.

Key comparative factors to evaluate:

- 📊 Recent comparable sales within 0.5 miles in the past 3-6 months

- 🏘️ Property condition relative to similar homes in the neighborhood

- 🔧 Modernization level and required renovation costs

- 📍 Micro-location factors such as school catchment areas and transport links

- 📈 Local market velocity (how quickly properties are selling)

In regions with 2% price growth like Scotland and Northern England, comparable sales from even 6 months ago may overstate current market value, giving buyers additional negotiating room.

The Builder Incentive Valuation Advantage

New construction properties offer exceptional valuation opportunities in 2026, with builder incentives at 65% across the market.[1] These incentives effectively reduce the true cost of the property while maintaining its nominal valuation.

Common builder incentives that enhance value:

- ✅ Rate buy-downs: Reducing mortgage rates by 1-2% for initial years

- ✅ Closing cost assistance: Covering £3,000-£8,000 in transaction fees

- ✅ Deposit contributions: Reducing upfront cash requirements

- ✅ Upgraded finishes: Including premium fixtures, appliances, or flooring

- ✅ Stamp duty assistance: Particularly valuable for properties near thresholds

When evaluating new construction, calculate the effective purchase price by subtracting the monetary value of all incentives. A £250,000 property with £15,000 in incentives has an effective valuation of £235,000, providing immediate equity.

Survey-Based Valuation Adjustments

Professional property surveys reveal defects and issues that directly impact valuation. A Level 3 building survey provides the most comprehensive assessment, particularly valuable for older properties common in Northern England and Scotland.

Survey findings that justify valuation reductions:

| Issue Identified | Typical Valuation Impact | Negotiation Strategy |

|---|---|---|

| Damp/moisture problems | £5,000-£15,000 | Request remediation or price reduction |

| Roof repairs needed | £8,000-£25,000 | Obtain specialist quotes, negotiate accordingly |

| Electrical rewiring required | £4,000-£8,000 | Factor into offer price with evidence |

| Structural movement | £10,000-£50,000+ | Seek structural engineer assessment |

| Outdated heating system | £3,000-£6,000 | Request replacement or cost contribution |

Understanding what surveyors check during inspections helps buyers anticipate potential valuation adjustments before making offers.

Implementing Valuation Strategies for First-Time Buyers in 2026: Practical Negotiation Tactics

Leveraging Improved Inventory for Negotiation Power

One of the most significant shifts in 2026 is improving inventory levels in many markets, giving buyers increased negotiating leverage compared to the seller's market of previous years.[2] This inventory improvement is particularly pronounced in regions experiencing modest price growth.

Negotiation tactics for the current environment:

- Request inspection credits: Ask sellers to contribute toward repair costs identified in surveys

- Negotiate closing cost assistance: Particularly effective when multiple properties compete for buyers

- Seek rate buy-down contributions: Sellers may contribute to temporary rate reductions

- Request extended contingency periods: More time for thorough due diligence and valuation

- Propose delayed closing dates: Accommodating seller timelines in exchange for price concessions

The key is demonstrating that your offer is credible and well-researched, supported by professional valuations and survey evidence. Working with residential surveyors who understand local markets strengthens your negotiating position considerably.

The 9% Down Payment Benchmark Strategy

Research indicates that the median down payment for first-time homebuyers in 2026 is 9% of the purchase price.[3] This benchmark provides a strategic framework for valuation and affordability planning.

Strategic implications of the 9% benchmark:

- Valuation ceiling: Reverse-engineer maximum property value from available deposit funds

- Negotiation reference: Industry-standard expectation for first-time buyer transactions

- Budget discipline: Prevents overextending on properties requiring larger deposits

- Competitive positioning: Aligns offers with typical first-time buyer profiles

For example, with £25,000 available for deposit, the 9% benchmark suggests targeting properties valued at approximately £278,000. This creates clear valuation parameters and prevents emotional overspending on properties beyond realistic affordability.

Seasonal Timing and Valuation Optimization

Property prices demonstrate predictable seasonal patterns, with values typically increasing from winter through spring and summer.[2] First-time buyers implementing effective valuation strategies should consider these timing dynamics.

Q1 2026 advantages for first-time buyers:

- 🌨️ Lower competition: Fewer buyers active in winter months

- 💰 Better pricing: Properties listed before spring premium pricing kicks in

- ⏰ Motivated sellers: Those listing in winter often have urgency to sell

- 📉 Negotiation flexibility: Less competitive pressure allows for thorough valuation processes

However, inventory may be somewhat limited in Q1, requiring buyers to balance timing advantages against property selection. The optimal strategy often involves beginning the search in Q1 while remaining flexible to continue through Q2 if the right property hasn't emerged.

Evidence-Based Offer Strategies

In the improved buyer's market of 2026, particularly in regions with modest price growth, evidence-based offers carry significant weight. Sellers and their agents recognize that well-researched buyers are more likely to complete transactions successfully.

Components of a compelling evidence-based offer:

- Professional valuation report: Demonstrates objective market value assessment

- Comparable sales analysis: Shows how offer price aligns with recent transactions

- Survey findings: Documents any defects or issues affecting value

- Mortgage pre-approval: Proves financial capability to complete purchase

- Realistic timeline: Demonstrates serious intent and preparation

This approach is particularly effective when the asking price exceeds recent comparable sales or when survey findings reveal issues. The combination of RICS homebuyer surveys and professional valuations creates an irrefutable case for adjusted pricing.

Regional-Specific Valuation Strategies: Scotland and Northern England Focus

Scotland's Unique Market Dynamics

Scotland's property market operates under different legal frameworks and demonstrates distinct valuation characteristics in 2026. With house price growth at just 2% while wages accelerate, Scottish first-time buyers enjoy particularly strong positioning.

Scottish valuation considerations:

- Home Report requirement: Sellers must provide professional survey and valuation upfront

- Closing date system: Sealed bids above valuation are common practice

- Note of interest: Signals serious intent without committing to specific price

- Survey accessibility: Buyer can review Home Report before viewing, streamlining valuation process

The Home Report system actually benefits first-time buyers by providing transparent valuation information before emotional attachment develops. Buyers can identify properties where the Home Report valuation exceeds recent comparable sales, indicating negotiation opportunities.

Northern England's Affordability Advantage

Northern England encompasses diverse markets from Manchester to Newcastle, all sharing the common characteristic of modest price growth relative to wage increases in 2026. This creates exceptional opportunities for strategic first-time buyers.

Valuation strategies specific to Northern England:

- Victorian and Edwardian stock: Many properties require modernization, creating valuation negotiation opportunities

- Regeneration areas: Identifying emerging neighborhoods before price acceleration

- Commuter belt expansion: Properties within new transport links offer value appreciation potential

- Terraced property valuations: Understanding the premium for end-terrace versus mid-terrace positioning

Working with chartered surveyors familiar with specific Northern England locations ensures valuation assessments account for hyper-local factors that significantly impact property values.

Identifying Value in Emerging Micro-Markets

Within regions experiencing modest overall price growth, certain micro-markets demonstrate stronger fundamentals that suggest future appreciation. Identifying these areas requires sophisticated valuation analysis beyond simple price-per-square-foot calculations.

Indicators of emerging value micro-markets:

- 🚇 Transport infrastructure investment: New stations or improved services

- 🏫 School rating improvements: Rising Ofsted ratings increase family demand

- 🏗️ Commercial development: New retail or employment centers

- 👥 Demographic shifts: Young professional population growth

- 📊 Rental yield strength: Strong rental demand indicates fundamental value

These factors suggest that current valuations may understate medium-term appreciation potential, making properties in these micro-markets particularly attractive for first-time buyers planning to hold for 5+ years.

Advanced Valuation Considerations: Beyond Basic Market Value

Reinstatement Cost Valuation for Insurance Accuracy

While market valuation determines purchase price, reinstatement cost valuation establishes the appropriate insurance coverage level. This is particularly important for first-time buyers who may underinsure properties, leaving them financially vulnerable.

Reinstatement cost valuation calculates the cost to completely rebuild the property to its current standard, which often differs significantly from market value. In regions with lower property prices relative to construction costs, reinstatement values may actually exceed market values.

Shared Ownership Valuation Strategies

For first-time buyers unable to afford full ownership even in affordable regions, shared ownership schemes provide an entry point. However, these arrangements require specialized valuation approaches.

RICS shared ownership valuations assess both the initial share being purchased and the full property value, ensuring the arrangement represents fair value. This is particularly relevant in 2026 as shared ownership schemes expand in response to affordability challenges.

Freehold vs. Leasehold Valuation Implications

The distinction between freehold and leasehold ownership significantly impacts property valuation, particularly for flats and apartments common in urban areas of Northern England and Scotland.

Freehold valuations typically command a premium over comparable leasehold properties due to:

- No ground rent obligations

- No service charge uncertainties

- Complete control over property decisions

- No lease length depreciation concerns

For first-time buyers, understanding these valuation differences helps in comparing properties on a like-for-like basis and negotiating appropriate price adjustments for leasehold limitations.

Financial Preparation and Valuation Alignment

Aligning Budget with Realistic Valuations

One of the most common mistakes first-time buyers make is falling in love with properties beyond their realistic budget. Effective valuation strategies require disciplined financial boundaries established before property searching begins.

Financial preparation steps for 2026:

- Obtain mortgage pre-approval: Establishes definitive budget ceiling[4]

- Calculate total ownership costs: Include insurance, maintenance, utilities, and council tax

- Build emergency reserves: Maintain 3-6 months expenses beyond deposit and closing costs[3]

- Account for survey-identified repairs: Budget additional 5-10% for immediate property improvements

- Consider rate environment: Calculate affordability at current 6.25% rates rather than hoping for reductions[2]

This financial discipline ensures that valuation strategies focus on properties genuinely within reach, preventing disappointment and wasted time on unrealistic targets.

Understanding Lender Valuation Requirements

Mortgage lenders conduct their own valuations to protect their loan security, which may differ from market valuations or survey assessments. Understanding lender valuation processes helps first-time buyers navigate potential complications.

Key lender valuation considerations:

- Conservative approach: Lenders often value properties at or below purchase price

- Down-valuation risk: If lender values property below agreed price, buyers must cover the gap

- Property condition impact: Significant defects may result in mortgage refusal until remediated

- Comparable sales emphasis: Lenders rely heavily on recent transaction evidence

- Regional expertise: Lenders use local surveyors familiar with specific market conditions

When implementing Valuation Strategies for First-Time Buyers in 2026: Leveraging Affordability Gains and Regional Price Variations, anticipating lender valuation outcomes prevents last-minute financing complications. Obtaining an independent RICS valuation before making offers helps ensure lender valuations will support the transaction.

Tax Implications and Valuation Planning

First-time buyers in the UK benefit from stamp duty relief on properties up to £425,000 (or £625,000 in some cases), making valuation positioning relative to these thresholds strategically important.

Tax-efficient valuation strategies:

- Negotiate below thresholds: Even small reductions below £425,000 save thousands in stamp duty

- Separate chattels valuation: Furniture and appliances can be valued separately, reducing property price

- Timing considerations: Be aware of any changes to first-time buyer relief programs

- Future tax planning: Consider potential capital gains tax implications if property becomes a rental

While tax considerations shouldn't override fundamental valuation principles, they provide additional negotiating leverage when properties sit near threshold boundaries.

Common Valuation Mistakes First-Time Buyers Must Avoid

Emotional Valuation vs. Market Reality

The single biggest valuation error first-time buyers make is allowing emotional attachment to override objective market assessment. In competitive situations, this leads to overpaying and immediate negative equity.

Warning signs of emotional over-valuation:

- ⚠️ Justifying prices above comparable sales with subjective factors

- ⚠️ Dismissing survey findings as "not that serious"

- ⚠️ Competing against yourself by increasing offers without counter-offers

- ⚠️ Focusing on monthly payment affordability rather than total price

- ⚠️ Ignoring red flags because "it's the perfect location"

The antidote is maintaining disciplined valuation boundaries established before viewing properties. If a property exceeds your pre-determined maximum valuation by more than 5%, walk away regardless of emotional attachment.

Neglecting Professional Survey Investment

Some first-time buyers attempt to save money by skipping professional surveys, relying only on lender valuations. This is a false economy that frequently costs far more than survey fees.

The question "is a homebuyers survey worth it" has a clear answer in 2026: absolutely yes. Survey costs of £400-£1,200 pale in comparison to discovering £20,000 in hidden defects after purchase.

Ignoring Regional Market Velocity

A property's valuation exists within the context of how quickly properties are selling in that specific market. In slower markets with improving inventory, valuations should be more conservative than in fast-moving markets with multiple offers.

Market velocity indicators:

- Days on market: Properties sitting 60+ days suggest negotiating room

- Price reductions: Multiple reductions indicate overpricing

- Seasonal patterns: Winter listings often indicate motivated sellers

- Comparable sales velocity: How quickly similar properties sold after listing

In regions with 2% price growth like Scotland and Northern England, market velocity tends to be slower, giving buyers time for thorough valuation processes and stronger negotiating positions.

Conclusion: Capitalizing on 2026's Unique Valuation Opportunities

The convergence of wage growth outpacing house prices, stable mortgage rates, improving inventory, and substantial builder incentives creates an exceptional environment for first-time buyers in 2026—particularly in Scotland and Northern England. However, these advantages only materialize for buyers who implement disciplined, professional valuation strategies rather than emotional decision-making.

The Valuation Strategies for First-Time Buyers in 2026: Leveraging Affordability Gains and Regional Price Variations outlined in this guide provide a comprehensive framework for entering the property market from a position of strength. By combining RICS-backed professional valuations, evidence-based negotiation tactics, regional market analysis, and financial discipline, first-time buyers can secure properties at genuine market value while avoiding the overpayment that has characterized previous market cycles.

Actionable Next Steps

To implement these valuation strategies effectively, first-time buyers should:

- Engage a RICS-qualified surveyor early in the process to establish realistic valuation expectations for target regions and property types

- Obtain mortgage pre-approval to define precise budget boundaries before emotional attachment develops

- Research regional market dynamics thoroughly, focusing on areas where wage growth exceeds price appreciation

- Time market entry strategically, considering Q1 advantages while remaining flexible through Q2

- Invest in comprehensive surveys for any property under serious consideration, using findings as negotiation leverage

- Build evidence-based offers supported by professional valuations, comparable sales analysis, and survey documentation

- Maintain negotiating discipline, walking away from properties that exceed objective valuation assessments

The improved affordability conditions of 2026 represent a genuine opportunity for first-time buyers who have been priced out of previous markets. By approaching property acquisition as a strategic valuation exercise rather than an emotional journey, buyers can secure homes that represent both excellent value today and sound investments for the future.

The regional variations across the UK mean that opportunities exist at multiple price points and locations—the key is identifying where your budget intersects with genuine value. With professional guidance, thorough preparation, and disciplined execution of proven valuation strategies, 2026 can be the year that first-time buyer aspirations become reality.

References

[1] Blog 142499 First Time Home Buyers In 2026 Overcoming The Real Obstacles – https://www.har.com/blog_142499_first-time-home-buyers-in-2026-overcoming-the-real-obstacles

[2] Home Buyer Preparation 2026 – https://themortgagereports.com/125202/home-buyer-preparation-2026

[3] Top 6 Financial Tips Every First Time Homebuyer Should Know In 2026 – https://resourcecenter.lennar.com/lennar-news/top-6-financial-tips-every-first-time-homebuyer-should-know-in-2026/

[4] How To Prepare Finances To Buy 2026 – https://www.rocketmortgage.com/learn/how-to-prepare-finances-to-buy-2026