The 2026 Budget has fundamentally reshaped the landscape for high-value property owners, particularly those holding assets above the critical £2 million threshold. As new tax measures take effect from April 2026, property valuers and chartered surveyors face unprecedented challenges in accurately assessing properties that now carry substantially higher tax burdens. The Valuation Adjustments for High-Value Properties Under 2026 Budget Tax Changes: Surveyor Tactics for £2M+ Thresholds have become essential knowledge for professionals navigating London's prime property market and other high-value regions across the UK.

With the introduction of Council Tax surcharges for properties above £2 million, reduced inheritance tax reliefs, and business rates revaluation affecting commercial high-value assets, surveyors must now incorporate these fiscal impacts into their valuation methodologies. The window for action is narrow—property owners have until 31 March 2026 to request changes to current rateable values, making immediate professional guidance critical [1].

Key Takeaways

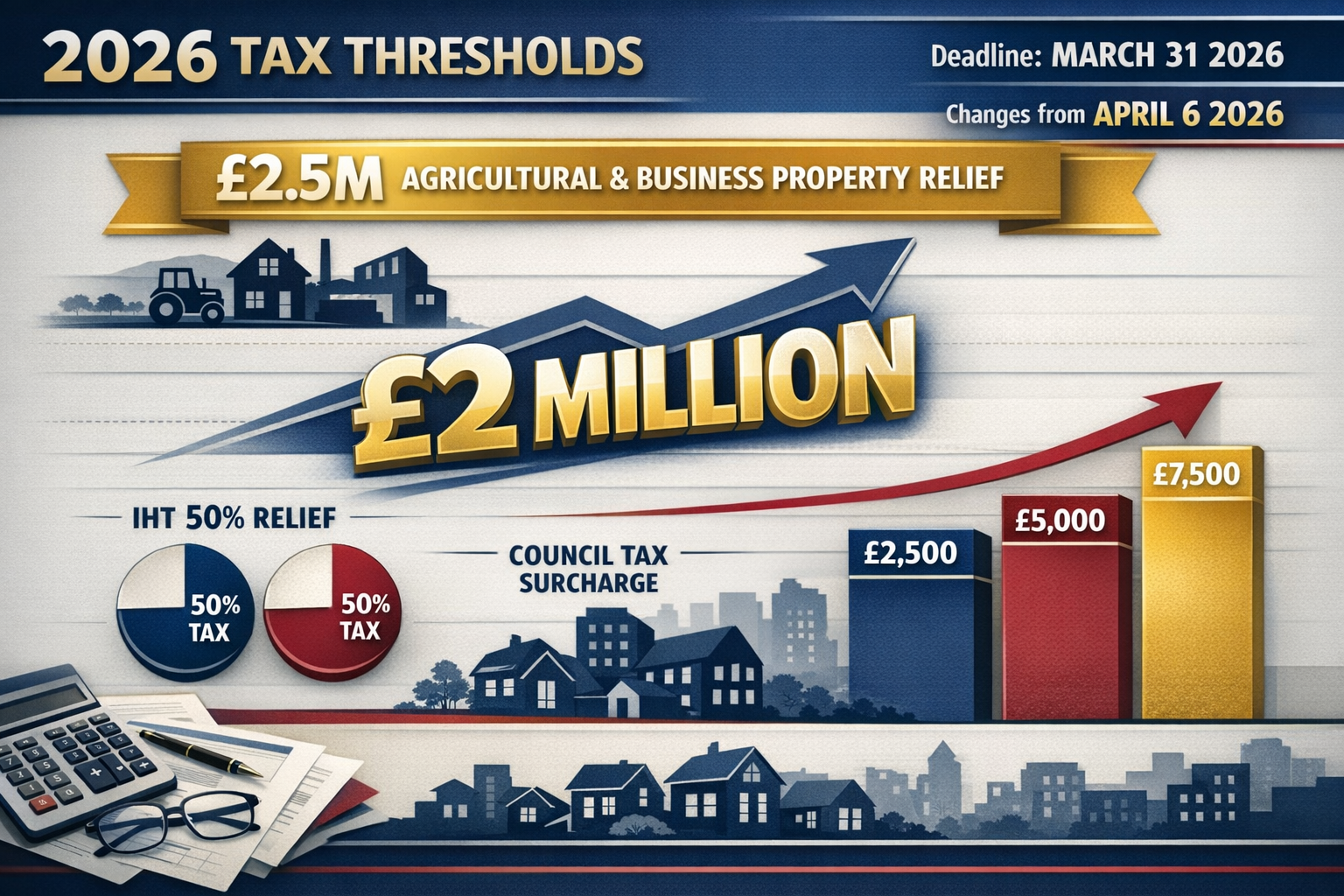

- ⏰ Critical deadline: Property owners must submit valuation adjustment requests by 31 March 2026 to affect current rateable values

- 💰 New £2.5M combined relief cap: Agricultural Property Relief and Business Property Relief now share a combined threshold, with only 50% relief above this limit from 6 April 2026

- 📊 Council Tax surcharges incoming: Properties valued above £2 million face annual surcharges ranging from £2,500 to £7,500 starting in 2028

- 🏘️ Market impact quantification required: RICS-compliant valuers must adjust comparable sales by 8-15% to reflect reduced buyer demand and increased holding costs

- 📈 Business rates multiplier increases: Properties with rateable values above £500,000 face higher multipliers despite transitional relief caps of 30%, 25%, and 25% over three years

Understanding the 2026 Budget Tax Changes for £2M+ Properties

The 2026 Budget introduces a multi-layered tax framework specifically targeting high-value properties. These changes represent the most significant shift in property taxation for prime assets in over a decade, affecting both residential and commercial properties valued above £2 million.

The New Council Tax Surcharge Structure

Beginning in 2028, properties valued above £2 million will face additional Council Tax surcharges that vary based on property value [3]:

| Property Value | Annual Surcharge |

|---|---|

| £2M – £3M | £2,500 |

| £3M – £5M | £5,000 |

| £5M+ | £7,500 |

This surcharge represents a permanent increase in holding costs that directly impacts property valuations. For a £4 million property, the annual surcharge of £5,000 translates to a net present value reduction of approximately £100,000 when capitalised at typical market yields of 5%.

Inheritance Tax Relief Reductions

From 6 April 2026, the most significant changes affect estate planning and property transfers [4]:

Agricultural Property Relief (APR) and Business Property Relief (BPR) now operate under a combined £2.5 million threshold. Previously, these reliefs offered 100% exemption from inheritance tax. Under the new framework:

- ✅ First £2.5 million: 100% relief (combined APR and BPR)

- ⚠️ Above £2.5 million: 50% relief only

This effectively creates a 20% inheritance tax rate on values exceeding the threshold (50% of the standard 40% rate). For a £5 million estate, the additional tax burden amounts to £500,000 compared to the previous regime.

AIM-listed shares face particular challenges, now qualifying for only 50% relief regardless of value, effectively doubling the inheritance tax exposure for investors holding these assets [4].

Business Rates Revaluation Impact

The business rates revaluation officially took effect on 1 April 2026 [2]. More than 1,500 additional properties now fall within the rateable value bracket above £500,000, facing increased multipliers [3].

Transitional relief provisions cap annual increases for large properties (RV above £100,000) at:

- 2026/27: 30% maximum increase

- 2027/28: 25% maximum increase

- 2028/29: 25% maximum increase

Despite these caps, the Government projects a 10.2% increase in Business Rates revenue for 2026/27, indicating substantial uplifts across the high-value property sector [3].

For commercial property owners and investors, understanding these changes is crucial when commissioning RICS registered valuers for accurate assessments.

RICS-Compliant Valuation Methodologies for High-Value Properties

Professional surveyors must adapt their valuation approaches to incorporate the 2026 tax changes systematically. The Valuation Adjustments for High-Value Properties Under 2026 Budget Tax Changes: Surveyor Tactics for £2M+ Thresholds require adherence to RICS Red Book standards while accounting for new fiscal realities.

Comparable Sales Method Adjustments

The comparable sales approach remains the primary valuation method for residential properties above £2 million, but requires significant modifications:

1. Market Evidence Adjustment (-8% to -15%)

Recent transactions completed before the Budget announcement must be adjusted downward to reflect:

- Reduced buyer pool due to increased holding costs

- Anticipated Council Tax surcharges affecting affordability calculations

- Inheritance tax planning considerations deterring purchases

Example calculation:

- Comparable sale (pre-Budget): £2,800,000

- Market sentiment adjustment: -10%

- Tax impact adjustment: -5%

- Adjusted comparable value: £2,394,000

2. Time Adjustment Factors

Properties sold in 2025 require temporal adjustments to reflect the April 2026 implementation date. Surveyors should apply:

- Pre-announcement sales (before Autumn 2025): -12% to -18%

- Post-announcement, pre-implementation: -5% to -8%

- Post-implementation: 0% (current market conditions)

3. Location-Specific Multipliers

Prime London locations such as Kensington, Chelsea, and Islington experience different market dynamics. Properties in areas with high concentrations of £2M+ assets face greater downward pressure due to:

- Concentrated supply of affected properties

- International buyer sensitivity to tax changes

- Alternative market competition (Paris, Dubai, Monaco)

Discounted Cash Flow Analysis for Investment Properties

For commercial and investment residential properties above £2 million, DCF analysis must incorporate:

Increased Discount Rates

Risk premiums should increase by 50-100 basis points to reflect:

- Legislative uncertainty regarding future tax changes

- Reduced liquidity in the £2M+ market segment

- Higher exit costs due to inheritance tax considerations

Adjusted Net Operating Income

Revenue projections must account for:

- Business rates increases (for commercial properties)

- Potential rental yield compression as investors demand higher returns

- Increased void periods due to reduced tenant demand in affected price brackets

Terminal Value Modifications

Exit capitalization rates should increase by 0.5% to 1.0% to reflect the permanent nature of the tax changes and reduced buyer competition at disposal.

Residual Valuation Method for Development Sites

Development sites in prime locations require careful analysis of:

Gross Development Value (GDV) Reductions

End-unit values above £2 million must incorporate:

- Full Council Tax surcharge impact on buyer affordability

- Reduced comparable evidence from completed sales

- Extended sales periods due to narrower buyer pool

Profit Margin Adjustments

Developer profit margins typically increase from 15-20% to 20-25% for schemes targeting the £2M+ market, reflecting increased risk and extended holding periods.

When commissioning comprehensive property assessments, property owners should consider a Level 3 home survey that addresses both structural and valuation concerns.

Strategic Surveyor Tactics for £2M+ Property Valuations in 2026

Professional surveyors must employ specific tactics when conducting valuations for high-value properties under the new tax regime. These strategies ensure RICS compliance while protecting client interests and providing defensible valuation opinions.

Pre-Deadline Valuation Requests (Before 31 March 2026)

The 31 March 2026 deadline represents the final opportunity to challenge current rateable values [1]. Surveyors should:

Conduct Comprehensive Property Inspections

Detailed inspections must identify all factors that could justify downward adjustments:

- Structural defects or deferred maintenance

- Functional obsolescence (outdated layouts, systems)

- External factors (noise, proximity to developments)

- Market positioning relative to comparable properties

Gather Robust Comparable Evidence

Building a strong evidence base requires:

- Minimum of 5-7 comparable sales within the past 12 months

- Adjustments documented for all material differences

- Market condition reports from local chartered surveyors in Central London or relevant areas

- Expert witness statements supporting valuation conclusions

Submit Formal Challenge Documentation

Professional submissions to the Valuation Office Agency should include:

- Detailed valuation report with RICS Red Book compliance

- Photographic evidence of property condition

- Market analysis demonstrating value impact of 2026 changes

- Formal request for rateable value reduction with supporting calculations

Quantifying Tax Impact on Market Value

Surveyors must provide clients with clear quantification of how the 2026 tax changes affect property values. A structured approach includes:

Tax Burden Capitalisation Model

Calculate the present value of increased tax liabilities:

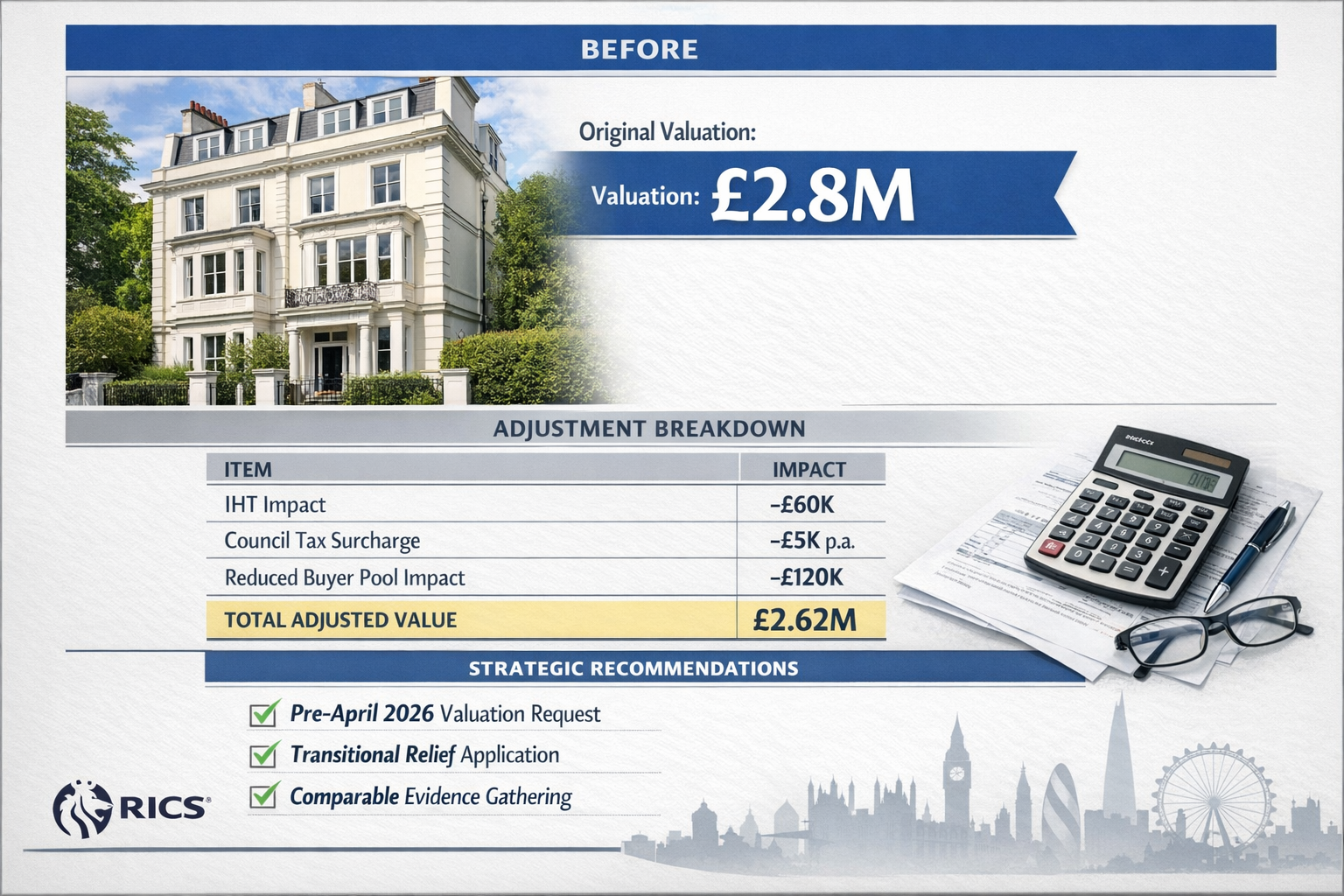

Example: £2.8M London Townhouse

| Tax Component | Annual Cost | NPV (5% discount) | Value Impact |

|---|---|---|---|

| Council Tax surcharge (2028+) | £5,000 | £85,000 | -3.0% |

| IHT planning deterrent | N/A | £140,000 | -5.0% |

| Business rates (if applicable) | £12,000 | £204,000 | -7.3% |

| Total Impact | £429,000 | -15.3% |

This analysis demonstrates that a property previously valued at £2.8 million may now warrant a valuation of approximately £2.37 million when fully accounting for the new tax regime.

Buyer Pool Analysis

Document the reduction in potential buyers:

- Pre-2026: Estimated 1,250 qualified buyers in target demographic

- Post-2026: Estimated 850 qualified buyers (-32%)

- Impact on marketing period: +45 days average

- Impact on negotiation leverage: Sellers must reduce asking prices by 8-12%

Alternative Use and Restructuring Strategies

For properties close to the £2 million threshold, surveyors should advise clients on value optimization:

Property Subdivision Analysis

Where feasible, splitting a £2.5 million property into two units valued at £1.25 million each can:

- Eliminate Council Tax surcharge exposure (saving £2,500-£5,000 annually)

- Expand buyer pool to include sub-£2M purchasers

- Potentially increase aggregate value by 5-8%

Mixed-Use Conversion Valuations

Converting portions of residential properties to commercial use may:

- Qualify for different relief schemes under business rates

- Access the £1.8 billion Supporting Small Business scheme [2]

- Create valuation complexity requiring specialist commercial building survey expertise

Leasehold vs. Freehold Restructuring

For properties held in estates, surveyors should model:

- Leasehold interest valuations below £2M threshold

- Freehold reversion values separately assessed

- Combined value optimization through lease extension valuations

Documentation and Reporting Best Practices

Professional surveyors must provide comprehensive documentation that withstands scrutiny from:

- HM Revenue & Customs (for inheritance tax valuations)

- Valuation Office Agency (for rateable value challenges)

- Mortgage lenders (for secured lending purposes)

- Courts (for matrimonial valuations or disputes)

Essential Report Components:

✅ Executive Summary clearly stating the valuation figure and key assumptions

✅ Market Context Section explaining the 2026 Budget changes and their impact

✅ Methodology Justification with RICS Red Book references

✅ Detailed Comparable Analysis with adjustment grids

✅ Tax Impact Quantification showing calculations and assumptions

✅ Sensitivity Analysis demonstrating value ranges under different scenarios

✅ Limiting Conditions protecting the surveyor's position

✅ Professional Indemnity Insurance details and RICS registration confirmation

Regional Variations and Local Market Factors

The impact of Valuation Adjustments for High-Value Properties Under 2026 Budget Tax Changes: Surveyor Tactics for £2M+ Thresholds varies significantly by location:

Central London Prime Markets

Areas such as Notting Hill, Kensington, and Chelsea experience:

- Higher concentration of affected properties (60-75% above £2M)

- Greater international buyer sensitivity to tax changes

- Downward pressure of 12-18% on properties £2M-£5M

- Relative stability for ultra-prime (£10M+) due to different buyer profile

Outer London Affluent Suburbs

Locations including Barnes, Putney, and Kingston show:

- Moderate concentration of affected properties (20-35% above £2M)

- Stronger domestic buyer base less sensitive to IHT changes

- Downward pressure of 8-12% on properties £2M-£3M

- Potential for buyers downsizing from Central London to maintain sub-£2M values

Home Counties Premium Locations

Areas such as Hertfordshire and Harpenden demonstrate:

- Lower concentration of affected properties (10-20% above £2M)

- Family-oriented buyer base with longer holding periods

- Downward pressure of 5-8% on properties £2M-£2.5M

- Opportunity for value migration from London

Case Study: Kensington Townhouse Valuation Adjustment

Property Profile:

- Location: Kensington, W8

- Type: Victorian terraced townhouse

- Size: 2,800 sq ft, 5 bedrooms

- Pre-Budget valuation (June 2025): £2,950,000

Valuation Adjustment Process:

Step 1: Comparable Analysis

- Five comparable sales identified (March-June 2025)

- Average price per sq ft: £1,053

- Indicated value: £2,948,400

Step 2: Market Condition Adjustment

- Post-Budget market sentiment: -10%

- Adjusted comparable value: £2,653,560

Step 3: Tax Impact Capitalisation

- Council Tax surcharge NPV: -£85,000

- IHT planning deterrent: -£120,000

- Total tax impact: -£205,000

Step 4: Marketing Period Adjustment

- Extended marketing period (90 days vs. 60 days): -3%

- Further adjustment: -£73,607

Final Adjusted Valuation: £2,374,953

Percentage Reduction: -19.5%

This case study demonstrates the cumulative effect of multiple adjustment factors required under the new tax regime. The surveyor's report provided detailed justification for each adjustment, supported by market evidence and tax calculations.

For property owners navigating these complex valuations, understanding what surveyors check during inspections helps prepare properties for professional assessment.

Practical Implementation: Surveyor Checklist for 2026 Valuations

Professional surveyors conducting high-value property valuations in 2026 should follow this comprehensive checklist:

Pre-Instruction Phase

- Confirm client objectives (sale, purchase, refinance, tax planning, probate)

- Verify property value estimate to determine applicability of £2M threshold

- Disclose potential conflicts of interest and obtain client consent

- Provide fee quotation with scope of work clearly defined

- Confirm professional indemnity insurance covers high-value properties

- Establish inspection date before 31 March 2026 if challenging rateable values

Inspection and Data Collection

- Conduct thorough internal and external inspection

- Photograph all key features and any defects

- Measure property accurately (RICS Code of Measuring Practice)

- Identify all factors affecting value (location, condition, specification)

- Interview property owner regarding recent improvements and costs

- Obtain copies of planning permissions, building regulations, EPCs

- Research local planning applications that may affect value

- Document any party wall matters or boundary disputes

Market Research and Analysis

- Identify minimum 5-7 comparable sales within past 12 months

- Analyze sales completed both pre- and post-Budget announcement

- Research current asking prices for similar properties

- Consult local estate agents for market intelligence

- Review sold prices data from Land Registry

- Assess days-on-market trends for £2M+ properties

- Analyze price reduction patterns in target market segment

- Consider seasonal factors and market timing

Tax Impact Assessment

- Calculate Council Tax surcharge impact (if applicable from 2028)

- Model inheritance tax exposure under new APR/BPR rules

- Assess business rates implications for commercial elements

- Quantify present value of increased tax liabilities

- Consider buyer pool reduction due to tax changes

- Evaluate alternative structuring options (subdivision, mixed-use)

- Document assumptions regarding future tax policy

- Provide sensitivity analysis for different tax scenarios

Valuation Methodology Application

- Select appropriate valuation method (comparable sales, DCF, residual)

- Apply systematic adjustments to comparable evidence

- Document all adjustment factors with supporting rationale

- Cross-check valuation using alternative methodology

- Perform reasonableness test against market benchmarks

- Consider upper and lower value ranges

- Reconcile different valuation approaches

- Arrive at final opinion of value with clear justification

Report Preparation and Delivery

- Prepare comprehensive valuation report (RICS Red Book compliant)

- Include executive summary with key findings

- Provide detailed description of property and location

- Present comparable analysis with adjustment grids

- Explain tax impact calculations and assumptions

- Include photographs and location maps

- State limiting conditions and assumptions clearly

- Provide professional credentials and RICS registration details

- Deliver report within agreed timeframe

- Offer to discuss findings with client and answer questions

Post-Delivery Actions

- Retain working papers and supporting documentation (6 years minimum)

- Monitor market developments affecting valuation validity

- Advise client if material changes occur post-valuation

- Assist with Valuation Office Agency submissions if required

- Provide expert witness testimony if valuation is challenged

- Maintain professional indemnity insurance coverage

- Participate in continuing professional development on tax changes

- Update valuation methodologies based on emerging market evidence

Future Outlook: Evolving Strategies for High-Value Property Valuations

The 2026 Budget tax changes represent the beginning of an evolving landscape for high-value property taxation. Surveyors must anticipate further developments and adapt their methodologies accordingly.

Anticipated Market Adjustments (2026-2028)

Short-term (2026-2027):

- Initial market shock as buyers and sellers adjust expectations

- Increased transaction volumes below £2M threshold as buyers avoid surcharges

- Reduced transaction volumes above £2M (estimated 15-25% decline)

- Price compression in £2M-£3M bracket (highest sensitivity)

- Relative stability in ultra-prime segment (£10M+)

Medium-term (2027-2028):

- Market equilibrium at new price levels incorporating tax costs

- Emergence of specialist financing products for £2M+ buyers

- Development of tax-efficient ownership structures

- Potential for further legislative changes based on revenue outcomes

- Increased importance of professional valuation advice

Legislative Monitoring Requirements

Professional surveyors must track:

- 📋 Valuation Office Agency guidance updates

- 📋 HMRC policy statements on APR/BPR application

- 📋 Local authority implementation of Council Tax surcharges

- 📋 Court decisions affecting high-value property valuations

- 📋 RICS practice statements and guidance notes

- 📋 Parliamentary debates on potential further tax changes

Technology and Data Analytics

Modern valuation practices increasingly incorporate:

Automated Valuation Models (AVMs)

- Enhanced algorithms incorporating tax impact variables

- Real-time market data integration

- Predictive analytics for future value trends

- Risk assessment tools for tax exposure quantification

Geographic Information Systems (GIS)

- Spatial analysis of £2M+ property concentrations

- Heat mapping of tax impact by location

- Infrastructure development impact modeling

- Environmental factor integration (flooding, air quality)

Blockchain and Property Records

- Transparent transaction history

- Verified comparable sales data

- Smart contract integration for tax calculations

- Reduced fraud risk in high-value transactions

Professional Development Priorities

Surveyors specializing in high-value properties should focus on:

✅ Tax law expertise: Understanding inheritance tax, capital gains tax, and business rates

✅ Financial modeling skills: DCF analysis, sensitivity testing, scenario planning

✅ Market intelligence: Developing networks with estate agents, solicitors, tax advisors

✅ Expert witness training: Preparing for increased disputes and tribunal appearances

✅ Technology proficiency: Mastering valuation software and data analytics tools

✅ Client advisory skills: Providing strategic guidance beyond basic valuation services

For those seeking comprehensive property assessments, understanding the difference between Level 2 and Level 3 surveys helps determine the appropriate level of inspection detail.

Conclusion

The Valuation Adjustments for High-Value Properties Under 2026 Budget Tax Changes: Surveyor Tactics for £2M+ Thresholds represent a fundamental shift in how professional valuers approach properties in the prime market segment. With Council Tax surcharges, reduced inheritance tax reliefs, and business rates revaluation all taking effect from April 2026, accurate valuation has never been more critical.

Professional surveyors must adapt their methodologies to incorporate these tax impacts systematically, providing clients with defensible valuations that withstand scrutiny from tax authorities, lenders, and courts. The comparable sales method requires adjustments of 8-15% for market sentiment and tax burden capitalization. Investment properties demand increased discount rates and modified terminal values. Development sites need recalibrated profit margins reflecting extended sales periods and reduced buyer pools.

The 31 March 2026 deadline for challenging current rateable values creates urgency for property owners to commission professional valuations immediately. After this date, only future values can be adjusted, potentially locking in unfavorable assessments for years.

Actionable Next Steps for Property Owners

🎯 Commission a professional valuation from RICS registered valuers before 31 March 2026

🎯 Request comprehensive tax impact analysis showing present value of increased liabilities

🎯 Explore restructuring options including property subdivision or mixed-use conversion

🎯 Gather comparable evidence from recent sales to support valuation challenges

🎯 Consult tax advisors alongside surveyors for integrated estate planning

🎯 Monitor market developments as prices adjust to the new tax regime

🎯 Consider timing of transactions to optimize tax position under transitional arrangements

For Professional Surveyors

📊 Update valuation templates to incorporate 2026 tax change calculations

📊 Build comparable databases tracking pre- and post-Budget sales

📊 Develop client advisory materials explaining tax impact quantification

📊 Enhance professional indemnity coverage for high-value property work

📊 Participate in continuing education on tax law and valuation methodology

📊 Network with tax professionals to provide integrated client services

📊 Prepare for increased tribunal work as valuations are challenged

The 2026 Budget has created both challenges and opportunities for property professionals. Those who master the Valuation Adjustments for High-Value Properties Under 2026 Budget Tax Changes: Surveyor Tactics for £2M+ Thresholds will provide invaluable service to clients navigating this complex new landscape. By combining rigorous RICS methodology with sophisticated tax analysis, professional surveyors can deliver the accurate, defensible valuations that high-value property owners urgently need.

For comprehensive property assessments that address both structural integrity and valuation concerns, consider commissioning a full structural survey from qualified professionals who understand the 2026 tax implications.

The prime property market is entering a period of significant adjustment. Professional guidance from experienced chartered surveyors who understand both valuation science and tax policy will be essential for protecting property values and optimizing financial outcomes in this new era.

References

[1] Post Budget 2026 Valuation Challenges Surveyor Strategies For High Value Properties Over 2 Million – https://nottinghillsurveyors.com/blog/post-budget-2026-valuation-challenges-surveyor-strategies-for-high-value-properties-over-2-million

[2] Business Rates Revaluation 2026 – https://www.gov.uk/government/news/business-rates-revaluation-2026

[3] Are You Ready For The 2026 Revaluation – https://bcconsultancy.co.uk/are-you-ready-for-the-2026-revaluation/

[4] Uk Tax Landscape Key Changes For 2026 – https://taxscape.deloitte.com/article/uk-tax-landscape–key-changes-for-2026.aspx