The UK property market stands at a pivotal moment. As 2026 unfolds, improved mortgage affordability is drawing unprecedented numbers of first-time buyers back into the market after years of being sidelined by high interest rates and escalating prices. This surge presents both tremendous opportunity and significant challenges for property valuers, surveyors, and lenders who must adapt their methodologies to accommodate regulatory reforms, changing buyer demographics, and evolving risk profiles. Preparing valuations for first-time buyer surge in 2026: affordability and reform impacts requires a comprehensive understanding of market dynamics, regulatory landscapes, and the unique needs of this critical buyer segment.

The convergence of falling mortgage rates, pent-up demand, and government reform initiatives creates a perfect storm of activity that will reshape how properties are valued and assessed throughout 2026 and beyond.

Key Takeaways

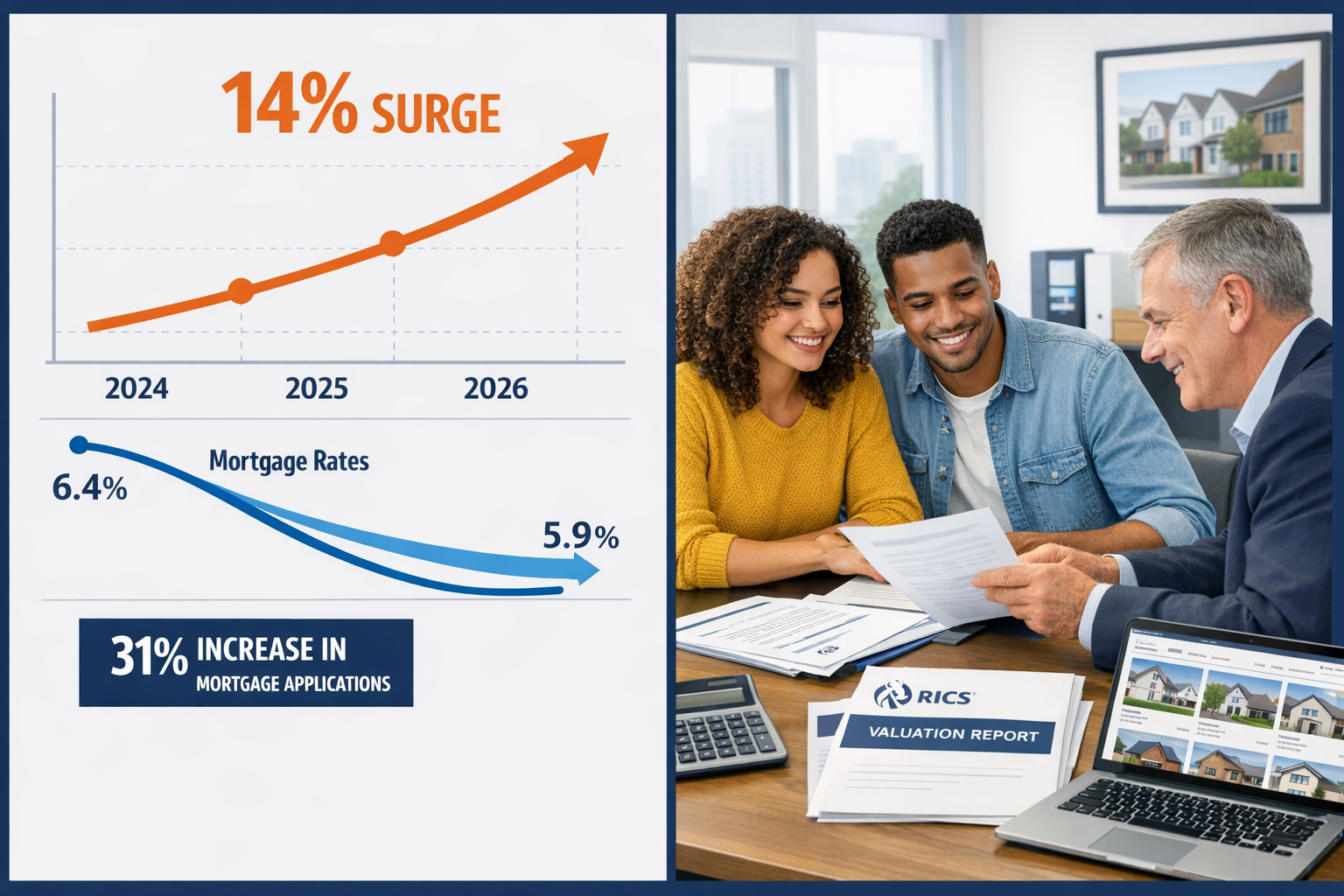

- Home sales are projected to surge 9-14% in 2026, driven by mortgage rates declining to approximately 5.9% and a 31% year-over-year increase in mortgage applications[1][3]

- First-time buyers currently represent only 21% of purchases (a historic low), creating significant upside potential as affordability improves and this demographic re-enters the market[1][2]

- Valuation methodologies must adapt to accommodate mandatory survey requirements, enhanced energy efficiency standards, and stabilizing price environments that characterize reform-driven markets

- Professional RICS-compliant valuations become increasingly critical as lenders tighten requirements and first-time buyers require additional protection against overpaying in competitive conditions

- Strategic preparation including updated comparable analysis, reform compliance checklists, and first-time buyer-specific risk assessments will differentiate successful valuation practices in 2026

Understanding the 2026 First-Time Buyer Surge: Market Fundamentals

Mortgage Rate Decline Driving Affordability

The single most significant factor enabling the anticipated first-time buyer surge is the projected decline in 30-year mortgage rates to 5.9% by the end of 2026, down from 6.4% at the end of 2025[3]. This seemingly modest reduction translates into substantial monthly payment savings that bring homeownership within reach for thousands of previously priced-out buyers.

For a typical first-time buyer purchasing a £250,000 property with a 10% deposit, the difference between a 6.4% and 5.9% mortgage rate represents approximately £70-80 in monthly savings—nearly £1,000 annually. Over the life of a 25-year mortgage, this reduction saves tens of thousands of pounds, fundamentally altering affordability calculations.

Pent-Up Demand Released

Mortgage applications have surged 31% year-over-year, indicating massive pent-up demand from buyers who have been waiting on the sidelines[1][2]. This cohort represents individuals and families who:

- ✅ Delayed purchases during the 2022-2024 high-rate environment

- ✅ Continued saving for larger deposits while waiting for improved conditions

- ✅ Maintained stable employment and improved credit profiles

- ✅ Watched property prices stabilize or decline in many markets

When these buyers enter the market simultaneously, the result is intensified competition, faster transaction timelines, and increased pressure on valuation services to deliver accurate, timely assessments.

National Sales Projections

Multiple forecasting organizations predict substantial growth in home sales for 2026:

| Forecaster | Projected Increase | Methodology |

|---|---|---|

| National Association of Realtors | 14% surge | Based on mortgage rate trends and buyer demand indicators[2][3] |

| Fannie Mae | 9.2% increase | Conservative estimate reaching 4.446 million annualized sales[3] |

| Redfin | 3% rise | Existing home sales at 4.2 million annualized rate[4] |

Even the most conservative projections indicate meaningful growth that will strain existing valuation capacity and require strategic preparation from surveying professionals.

The First-Time Buyer Deficit

Perhaps most telling is the historic low of 21% first-time buyer market share in 2024, down from 24% in 2023[1][2]. This represents the smallest proportion of first-time buyers in modern real estate history, creating enormous upside potential as conditions improve.

Historically, first-time buyers comprise 30-40% of all home purchases in healthy markets. The current deficit suggests that hundreds of thousands of potential first-time buyers are waiting to enter the market, and 2026's improved affordability conditions may finally trigger this long-delayed entry.

For valuation professionals, this demographic shift requires understanding the specific requirements and processes for first-time buyer valuations, including government scheme participation and enhanced lender scrutiny.

Preparing Valuations for First-Time Buyer Surge in 2026: Methodology Adaptations

Enhanced Comparable Analysis for Stabilizing Markets

As property prices stabilize after years of rapid appreciation, valuation methodologies must adapt to less predictable appreciation patterns. Traditional comparable analysis relied heavily on consistent upward price momentum, but 2026's market requires more nuanced approaches.

Key methodology adjustments include:

-

Expanded comparable timeframes: Rather than focusing solely on sales from the past 3-6 months, valuers should analyze 12-18 month trends to identify genuine stabilization versus temporary fluctuations

-

Location-specific micro-market analysis: First-time buyer hotspots may experience different price dynamics than overall market trends, requiring granular neighborhood-level data

-

Condition-adjusted comparables: With first-time buyers typically purchasing lower-priced properties that may require renovation, accurately adjusting for property condition becomes critical

-

Scheme-specific considerations: Properties eligible for Help to Buy, shared ownership, or other first-time buyer schemes require specialized valuation approaches that account for program restrictions

Professional valuation factors must be weighted differently in stabilizing markets, with greater emphasis on intrinsic property characteristics and less reliance on momentum-driven appreciation.

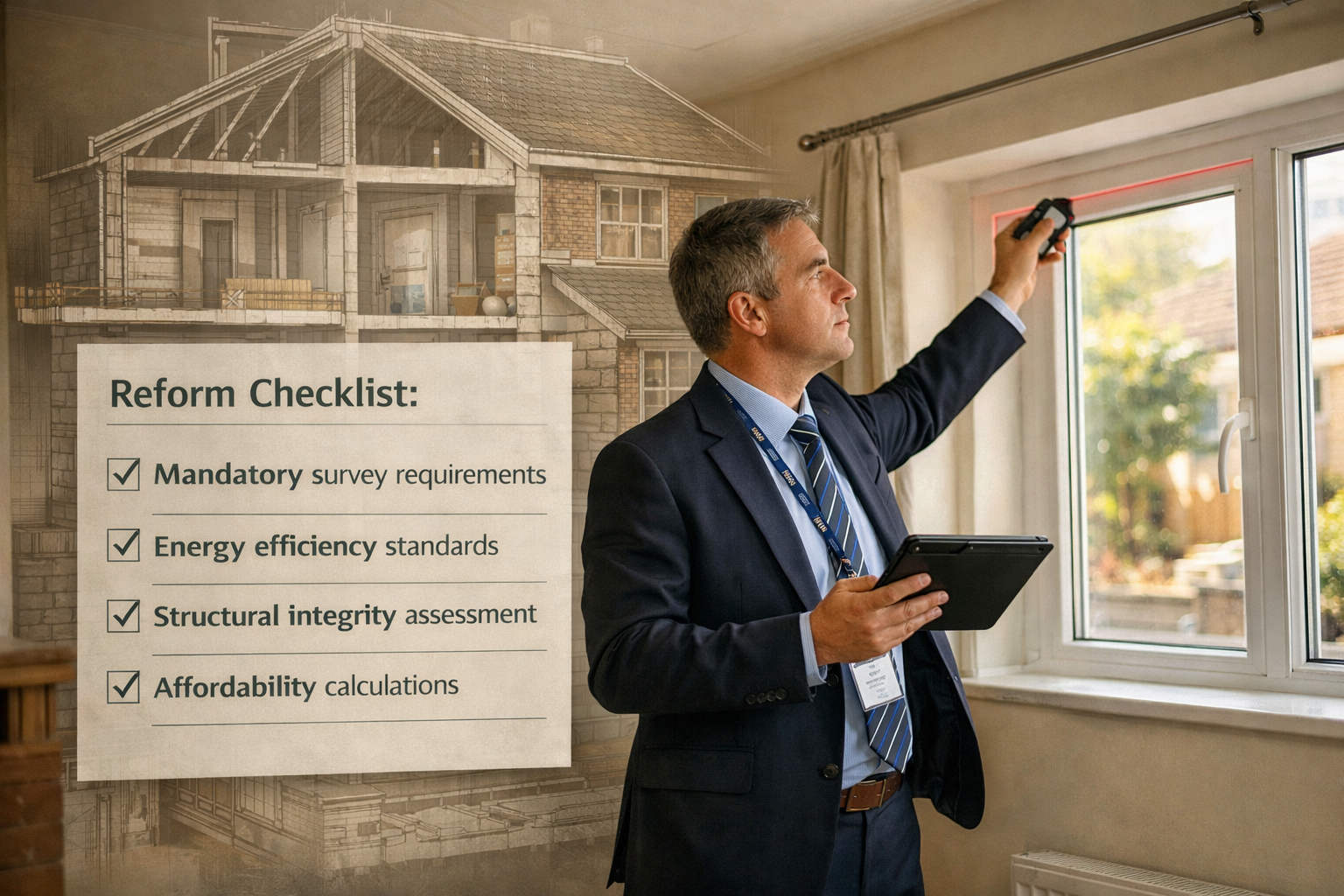

Reform-Driven Mandatory Survey Requirements

Government reforms aimed at protecting first-time buyers increasingly mandate comprehensive property surveys before purchase completion. These requirements fundamentally alter the valuation landscape by:

- Increasing transparency: Mandatory surveys reveal defects that previously went undiscovered until after purchase

- Adjusting price expectations: Buyers armed with detailed survey information negotiate more aggressively on price

- Standardizing assessment criteria: Regulatory frameworks establish minimum survey standards that valuers must incorporate

Valuers preparing for the 2026 surge must integrate survey findings into their assessments, understanding that properties with identified defects will face downward price pressure even in competitive markets. This requires establishing clear protocols for incorporating RICS building survey findings into final valuation figures.

Energy Efficiency and Sustainability Standards

Regulatory reforms increasingly emphasize energy efficiency, with minimum Energy Performance Certificate (EPC) ratings becoming prerequisites for mortgage approval in many cases. First-time buyers, often more environmentally conscious and cost-sensitive to utility expenses, prioritize energy-efficient properties.

Valuation implications include:

- Properties with EPC ratings below C face valuation penalties of 5-15% compared to similar properties with higher ratings

- Retrofit potential becomes a valuation factor, with properties easily upgraded commanding premiums

- Solar panels, heat pumps, and modern insulation add measurable value that must be quantified

- Future-proofing against stricter regulations influences long-term value projections

Valuers must develop expertise in assessing energy efficiency improvements and their impact on property values, incorporating these factors into comprehensive Red Book valuations.

Preparing Valuations for First-Time Buyer Surge in 2026: Risk Assessment and Lender Requirements

Heightened Lender Scrutiny

As first-time buyers flood the market, lenders face increased risk exposure from borrowers with limited equity, smaller deposits, and less property ownership experience. This translates into more rigorous valuation requirements:

Enhanced lender expectations:

- Desktop valuations decline: Lenders increasingly require physical inspections rather than automated valuation models (AVMs) for first-time buyer mortgages

- Second valuations: Disputed initial valuations trigger second opinions more frequently, requiring clear documentation and justification

- Condition reporting: Detailed condition assessments beyond simple valuation figures become standard requirements

- Comparable documentation: Lenders demand comprehensive comparable evidence with detailed adjustment explanations

Understanding the cost implications of different valuation types helps buyers and lenders budget appropriately while ensuring adequate assessment depth.

Overpayment Risk in Competitive Markets

The surge of first-time buyers creates intensely competitive bidding environments, particularly for starter homes and properties in desirable school catchment areas. Emotional buyers with limited experience may offer above-market prices, creating valuation challenges.

Valuer responsibilities include:

- Market value vs. purchase price distinction: Clearly differentiating between what a buyer has agreed to pay and the property's genuine market value

- Comparable evidence: Providing robust comparable evidence when valuation comes in below purchase price

- Risk flagging: Identifying when purchase prices significantly exceed supportable valuations, protecting both lender and buyer

- Communication clarity: Explaining valuation rationale in accessible terms for first-time buyers unfamiliar with the process

"The valuer's role extends beyond number calculation to buyer protection, particularly when inexperienced first-time buyers face pressure to overpay in competitive markets."

Scheme-Specific Valuation Considerations

Many first-time buyers access the market through government-backed schemes including Help to Buy, shared ownership, and Right to Buy programs. Each requires specialized valuation approaches:

Help to Buy valuations must account for equity loan provisions and future repayment obligations, requiring understanding of specific Help to Buy valuation processes.

Shared ownership valuations present unique challenges in determining market value when only a percentage share is being purchased, necessitating expertise in shared ownership valuation methodologies.

Right to Buy valuations require understanding of statutory discount calculations and resale restrictions, covered in specialized Right to Buy valuation services.

Geographic Variation in First-Time Buyer Activity

The first-time buyer surge will not impact all markets equally. Urban areas with strong employment, good transport links, and relatively affordable housing stock will experience disproportionate activity.

High-activity regions include:

- 🏙️ London suburbs: Areas like Kilburn, Battersea, and East London offering relative affordability with city access

- 🚄 Commuter belt: Towns with excellent rail connections to major employment centers

- 🎓 University cities: Locations with strong graduate retention and diverse employment

- 🏘️ Regeneration areas: Neighborhoods benefiting from infrastructure investment and development

Valuers operating in these hotspots must develop deep local market knowledge and maintain extensive comparable databases to support accurate assessments in rapidly moving markets.

Operational Preparation for Valuation Practices

Capacity Planning and Resource Allocation

The projected 9-14% increase in home sales translates directly into surging valuation demand[1][3][4]. Practices unprepared for this volume increase risk:

- ⚠️ Extended turnaround times that frustrate clients and lose business

- ⚠️ Rushed assessments that compromise quality and accuracy

- ⚠️ Staff burnout from unsustainable workloads

- ⚠️ Reputational damage from delayed or inadequate service

Strategic capacity planning includes:

- Staffing adjustments: Recruiting additional qualified valuers or training existing staff in residential valuation

- Technology investment: Implementing efficient scheduling, reporting, and comparable database systems

- Process optimization: Streamlining administrative tasks to maximize valuer time on core assessment activities

- Partnership development: Establishing referral networks with other practices to manage overflow during peak periods

Technology and Data Infrastructure

Modern valuation practices require robust technology infrastructure to deliver efficient, accurate assessments at scale:

Essential technology components:

- Comprehensive comparable databases: Regularly updated with recent sales, current listings, and withdrawn properties

- Mobile assessment tools: Tablet-based inspection software enabling on-site data capture and report generation

- Client portals: Secure platforms for document sharing, report delivery, and communication

- Automated quality checks: Systems that flag inconsistencies, missing data, or outlier valuations for review

Investment in technology infrastructure pays dividends through increased throughput, reduced errors, and enhanced client experience.

Continuing Professional Development

The evolving regulatory landscape and changing market dynamics require ongoing professional development for valuation practitioners:

Priority training areas for 2026:

- 📚 Updated energy efficiency assessment and EPC interpretation

- 📚 Reform-driven survey requirements and integration into valuations

- 📚 First-time buyer scheme regulations and valuation implications

- 📚 Stabilizing market valuation techniques and comparable analysis

- 📚 Enhanced communication skills for explaining complex valuations to inexperienced buyers

Maintaining RICS accreditation and staying current with regulatory changes ensures valuers deliver compliant, defensible assessments that protect all parties.

Client Communication and Education

Managing First-Time Buyer Expectations

First-time buyers often lack understanding of the valuation process, its purpose, and its implications for their purchase. Clear communication prevents misunderstandings and builds trust:

Key educational points:

- Valuation vs. survey distinction: Explaining that valuations assess market value for lending purposes while surveys evaluate property condition

- Independence requirements: Clarifying that valuers work independently and cannot be influenced by desired purchase prices

- Comparable methodology: Describing how recent sales inform valuation conclusions

- Downvaluation implications: Preparing buyers for potential outcomes when valuations come in below purchase price

Providing educational resources, whether through blog content, video explainers, or consultation guides, positions practices as trusted advisors rather than mere service providers.

Transparent Pricing and Service Tiers

First-time buyers operate on tight budgets and appreciate clear, transparent pricing structures. Offering tiered service options allows buyers to select appropriate assessment levels:

| Service Tier | Scope | Typical Use Case | Price Range |

|---|---|---|---|

| Basic Valuation | Market value assessment only | Straightforward properties in good condition | £250-400 |

| Valuation + Condition Report | Market value plus basic condition overview | Standard properties with minor concerns | £400-600 |

| Comprehensive Assessment | Full valuation, detailed condition report, defect identification | Older properties, unusual construction, or buyer concerns | £600-1,000+ |

Clear service descriptions and pricing help buyers make informed decisions while ensuring practices adequately compensate for the work performed.

Post-Valuation Support

The valuation report delivery should not end the client relationship. First-time buyers benefit from post-valuation support including:

- 📞 Follow-up calls to answer questions and clarify report contents

- 📞 Guidance on negotiating purchase price adjustments based on valuation findings

- 📞 Referrals to qualified contractors for identified repair needs

- 📞 Connections to mortgage advisors, solicitors, and other professionals

This comprehensive support approach builds lasting relationships that generate referrals and repeat business as first-time buyers eventually move up the property ladder.

Regulatory Compliance and Professional Standards

RICS Red Book Adherence

All professional valuations must comply with RICS Valuation – Global Standards (the "Red Book"), which establishes mandatory practices and ethical standards. The 2026 first-time buyer surge increases scrutiny on valuation quality, making strict Red Book compliance essential.

Core Red Book requirements include:

- ✅ Clear terms of engagement establishing scope, purpose, and limitations

- ✅ Appropriate valuation methodology selection and application

- ✅ Adequate inspection and investigation

- ✅ Proper comparable evidence and adjustment documentation

- ✅ Clear assumptions and special assumptions disclosure

- ✅ Professional indemnity insurance coverage

Working with RICS-accredited chartered surveyors ensures valuations meet these professional standards and withstand lender and regulatory scrutiny.

Documentation and Defensibility

In competitive markets with heightened emotions and significant financial stakes, valuation challenges become more common. Comprehensive documentation protects valuers and supports valuation conclusions:

Essential documentation includes:

- Detailed inspection notes with photographs

- Comprehensive comparable analysis with adjustment justifications

- Market condition assessments and trend analysis

- Correspondence records with clients, lenders, and agents

- Professional judgment rationale for complex or unusual assessments

Well-documented valuations withstand challenges and demonstrate professional competence, protecting both the valuer's reputation and professional indemnity insurance position.

Data Protection and Client Confidentiality

Valuation practices handle sensitive financial and personal information requiring robust data protection measures:

- 🔒 Secure storage systems with encryption and access controls

- 🔒 GDPR-compliant data processing and retention policies

- 🔒 Staff training on confidentiality obligations and data handling

- 🔒 Secure communication channels for report delivery and sensitive discussions

Demonstrating commitment to data protection builds client trust and ensures regulatory compliance in an increasingly scrutinized environment.

Strategic Positioning for Long-Term Success

Building First-Time Buyer Specialization

Practices that develop recognized expertise in first-time buyer valuations and related services position themselves advantageously for sustained growth beyond the 2026 surge:

Specialization strategies include:

- 🎯 Marketing specifically to first-time buyer demographics through targeted digital advertising

- 🎯 Developing educational content addressing common first-time buyer concerns and questions

- 🎯 Establishing partnerships with first-time buyer mortgage brokers and financial advisors

- 🎯 Creating streamlined service packages specifically designed for first-time buyer needs and budgets

Specialization allows practices to command premium pricing while delivering superior value through deep expertise and tailored service offerings.

Geographic Expansion Opportunities

The uneven geographic distribution of first-time buyer activity creates expansion opportunities for established practices. Strategic expansion into high-growth areas positions practices to capture market share during the surge.

Expansion considerations:

- Identifying underserved markets with strong first-time buyer fundamentals

- Establishing satellite offices or partnerships in target markets

- Developing local market expertise and comparable databases

- Building relationships with area estate agents, solicitors, and mortgage brokers

Geographic diversification also provides business resilience by reducing dependence on single-market conditions.

Relationship Development with Volume Lenders

Establishing preferred provider relationships with high-volume first-time buyer lenders generates consistent instruction flow:

Relationship building approaches:

- Demonstrating consistent quality, accuracy, and turnaround time performance

- Offering competitive pricing for volume instructions

- Providing dedicated account management and streamlined processes

- Investing in lender-specific technology integrations and reporting formats

Panel membership with major lenders provides business stability and growth opportunities, though practices must maintain independence and professional standards regardless of instruction source.

Conclusion: Seizing the 2026 Opportunity

The anticipated first-time buyer surge in 2026 represents a transformative opportunity for property valuation practices willing to prepare strategically. With home sales projected to increase 9-14% driven by declining mortgage rates and massive pent-up demand, the market dynamics are fundamentally shifting[1][3][4].

Successful preparation requires:

✅ Methodological adaptation incorporating reform-driven requirements, enhanced energy efficiency considerations, and stabilizing market dynamics

✅ Operational readiness through capacity planning, technology investment, and process optimization to handle increased volume without compromising quality

✅ Enhanced client communication that educates first-time buyers, manages expectations, and builds lasting relationships

✅ Unwavering professional standards maintaining RICS Red Book compliance, comprehensive documentation, and ethical practice regardless of competitive pressures

✅ Strategic positioning through specialization, geographic expansion, and lender relationship development for sustained growth

The practices that invest in these preparations will not only capitalize on the immediate 2026 surge but establish themselves as trusted first-time buyer specialists for years to come. As mortgage rates stabilize around 5.9% and hundreds of thousands of previously sidelined buyers enter the market, the demand for accurate, professional, reform-compliant valuations will reach unprecedented levels.

Next Steps for Valuation Practices

Immediate actions to take:

- Assess current capacity and identify resource gaps that would prevent handling 15-20% volume increases

- Review and update valuation methodologies to incorporate energy efficiency, reform requirements, and stabilizing market considerations

- Invest in technology infrastructure including comparable databases, mobile tools, and client communication platforms

- Develop educational content specifically targeting first-time buyer concerns and questions

- Establish partnerships with mortgage brokers, estate agents, and other professionals serving first-time buyers

- Pursue continuing professional development in areas critical to first-time buyer valuations and regulatory compliance

The 2026 first-time buyer surge is not merely a temporary spike but the beginning of a sustained shift as an entire demographic cohort—delayed by years of affordability challenges—finally accesses homeownership. Valuation practices that recognize this structural change and prepare accordingly will thrive in the evolving market landscape.

For professional guidance on preparing your valuation practice or obtaining expert assessments for first-time buyer properties, consult with experienced RICS chartered surveyors who understand both the opportunities and challenges of the 2026 market environment.

References

[1] Watch – https://www.youtube.com/watch?v=dohAxJcnYOk

[2] Watch – https://www.youtube.com/watch?v=rEKxV0pyeQg

[3] Home Sales To Jump Nearly 10 In 2026 Forecasters Say – https://www.realestatenews.com/2025/09/23/home-sales-to-jump-nearly-10-in-2026-forecasters-say

[4] Housing Market Predictions 2026 – https://www.redfin.com/news/housing-market-predictions-2026/