The UK property market is experiencing its most significant transformation in decades. As 2026 approaches, building surveys under new homebuying rules: earlier inspections and risk mitigation in 2026 are reshaping how buyers, sellers, and surveyors approach property transactions. The shift toward mandatory upfront condition assessments promises to accelerate transactions, reduce fall-throughs, and provide unprecedented transparency in the homebuying process.

This reform-driven change means surveyors must adapt their practices, buyers need to understand new timelines, and sellers must prepare properties for earlier scrutiny. The traditional model of conducting surveys after offers are accepted is giving way to a more efficient system where property conditions are assessed and disclosed before serious negotiations begin.

Key Takeaways

- 🏠 Upfront surveys become mandatory under 2026 reforms, requiring property condition assessments before listing or early in the sales process

- ⚡ Transaction speeds increase dramatically with earlier inspections eliminating traditional survey delays and reducing fall-through rates

- 📊 RICS survey levels require strategic selection based on property type, age, and condition to meet new compliance standards

- 🛡️ Risk mitigation improves significantly through standardized defect prioritization and transparent reporting frameworks

- 🔄 Surveyor practices must evolve to deliver faster, digitally-enhanced reports that support accelerated transaction timelines

Understanding the 2026 Homebuying Reform Landscape

The property market has long suffered from inefficiencies that cost buyers and sellers time, money, and emotional stress. Traditional homebuying processes often saw surveys conducted weeks after offers were accepted, leading to renegotiations, delays, and transaction collapses when unexpected defects emerged.

What's Changing in 2026?

The new homebuying rules introduce mandatory upfront condition assessments that fundamentally alter the transaction timeline[1]. Rather than waiting until after an offer is accepted, property conditions must be evaluated and disclosed much earlier in the process.

This shift addresses several critical market failures:

- Reduced transaction fall-throughs from unexpected survey findings

- Greater price transparency with defects disclosed upfront

- Faster completion times by eliminating survey-related delays

- Improved buyer confidence through comprehensive pre-purchase information

The Role of Building Surveyors in the New System

Building surveyors now occupy a more prominent position in the sales process. Their assessments inform listing prices, guide seller preparations, and provide buyers with essential information before making offers[1].

Surveyors must adapt to several new expectations:

Speed and efficiency: Reports need to be delivered faster without compromising quality

Standardized reporting: Consistent formats that enable easy comparison between properties

Digital integration: Cloud-based platforms for instant report access and updates

Enhanced communication: Clear explanations that non-technical buyers can understand

For those wondering whether a survey is necessary when buying a house, the 2026 reforms make this question largely obsolete—surveys become an integral, often mandatory part of the process.

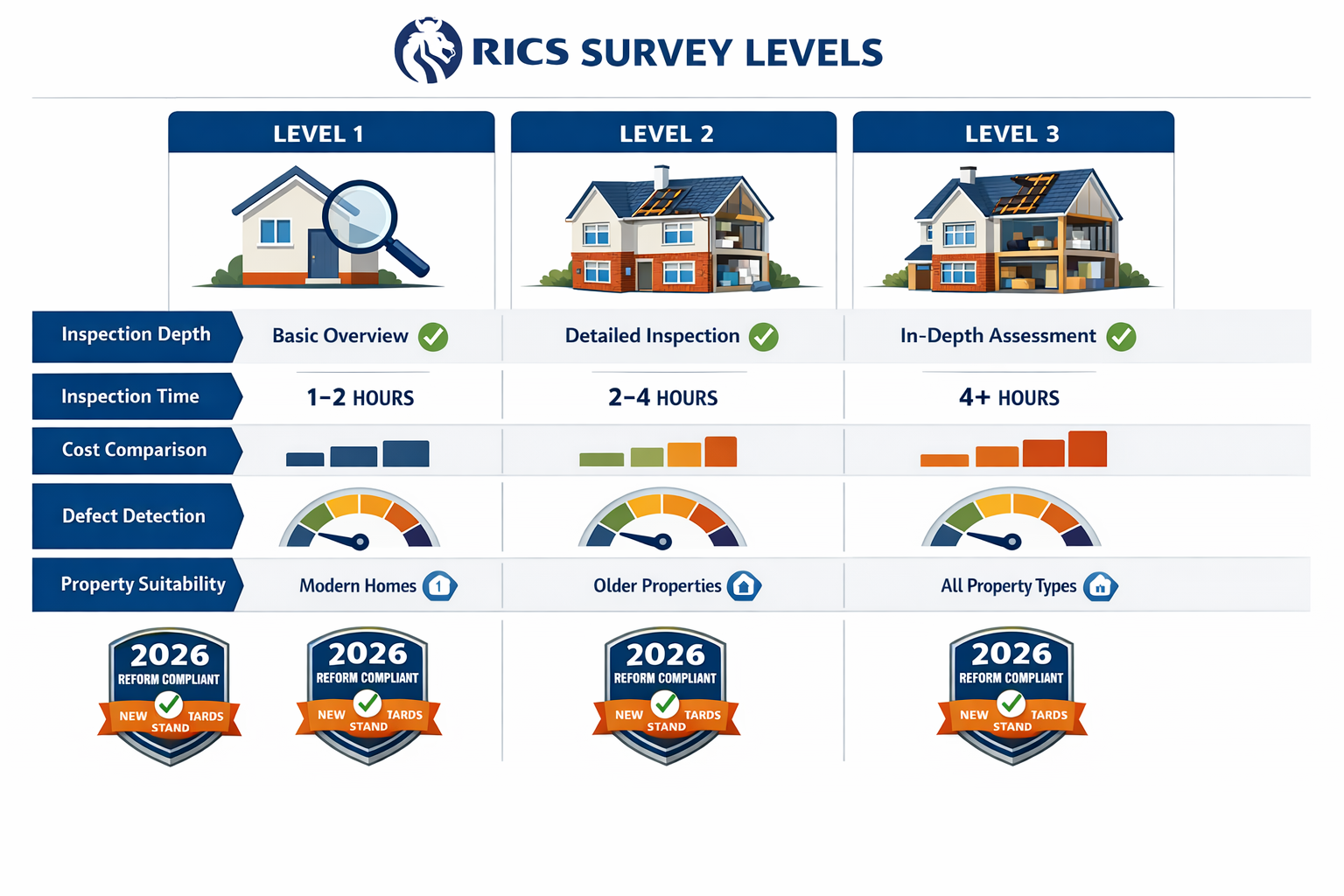

Building Surveys Under New Homebuying Rules: Comparing RICS Survey Levels

Selecting the appropriate survey level has never been more critical. Under the reformed system, the right survey choice impacts transaction speed, negotiation leverage, and long-term property satisfaction.

RICS Level 1: Condition Report

The RICS Level 1 survey provides a basic overview of property condition, suitable for newer homes in good repair.

Best suited for:

- Modern properties less than 10 years old

- Homes in excellent condition

- Properties built with conventional construction methods

- Buyers seeking basic condition confirmation

Limitations under new rules:

- May not satisfy lender requirements for older properties

- Limited defect detail could lead to post-purchase surprises

- Not recommended for properties requiring renovation

Typical turnaround: 3-5 working days

Cost range: £300-£500

RICS Level 2: HomeBuyer Report

The Level 2 home survey strikes a balance between comprehensiveness and cost, making it the most popular choice for standard residential properties.

Key features:

- Traffic light rating system (red, amber, green) for defects

- Guidance on urgent repairs and ongoing maintenance

- Market value assessment (optional)

- Suitable for conventional properties in reasonable condition

Ideal for:

- Properties built post-1900 in standard condition

- Conventional construction types

- Buyers seeking good value and reasonable detail

- Properties without obvious major defects

The timeline for Level 2 surveys typically ranges from 5-7 working days, making them compatible with accelerated transaction schedules.

Typical turnaround: 5-7 working days

Cost range: £450-£900

RICS Level 3: Building Survey

The comprehensive Level 3 building survey provides the most detailed property assessment available.

Comprehensive coverage includes:

- Detailed structural analysis

- In-depth defect descriptions with repair recommendations

- Guidance on maintenance priorities

- Suitability for major renovations or conversions

Essential for:

- Properties built before 1900

- Homes with unusual construction

- Properties in poor condition

- Buildings requiring significant renovation

- Listed or heritage properties

For buyers considering older or complex properties, reviewing a Level 3 building survey example helps understand the depth of information provided.

Typical turnaround: 7-10 working days

Cost range: £600-£1,500+

Survey Level Comparison Table

| Feature | Level 1 | Level 2 | Level 3 |

|---|---|---|---|

| Property age suitability | <10 years | Post-1900 | Any age |

| Condition requirement | Good | Reasonable | Any condition |

| Defect detail | Basic | Moderate | Comprehensive |

| Structural analysis | ❌ | Limited | ✅ Detailed |

| Repair cost guidance | ❌ | General | ✅ Specific |

| Renovation planning | ❌ | ❌ | ✅ |

| Average turnaround | 3-5 days | 5-7 days | 7-10 days |

| 2026 compliance | Limited | ✅ Standard | ✅ Premium |

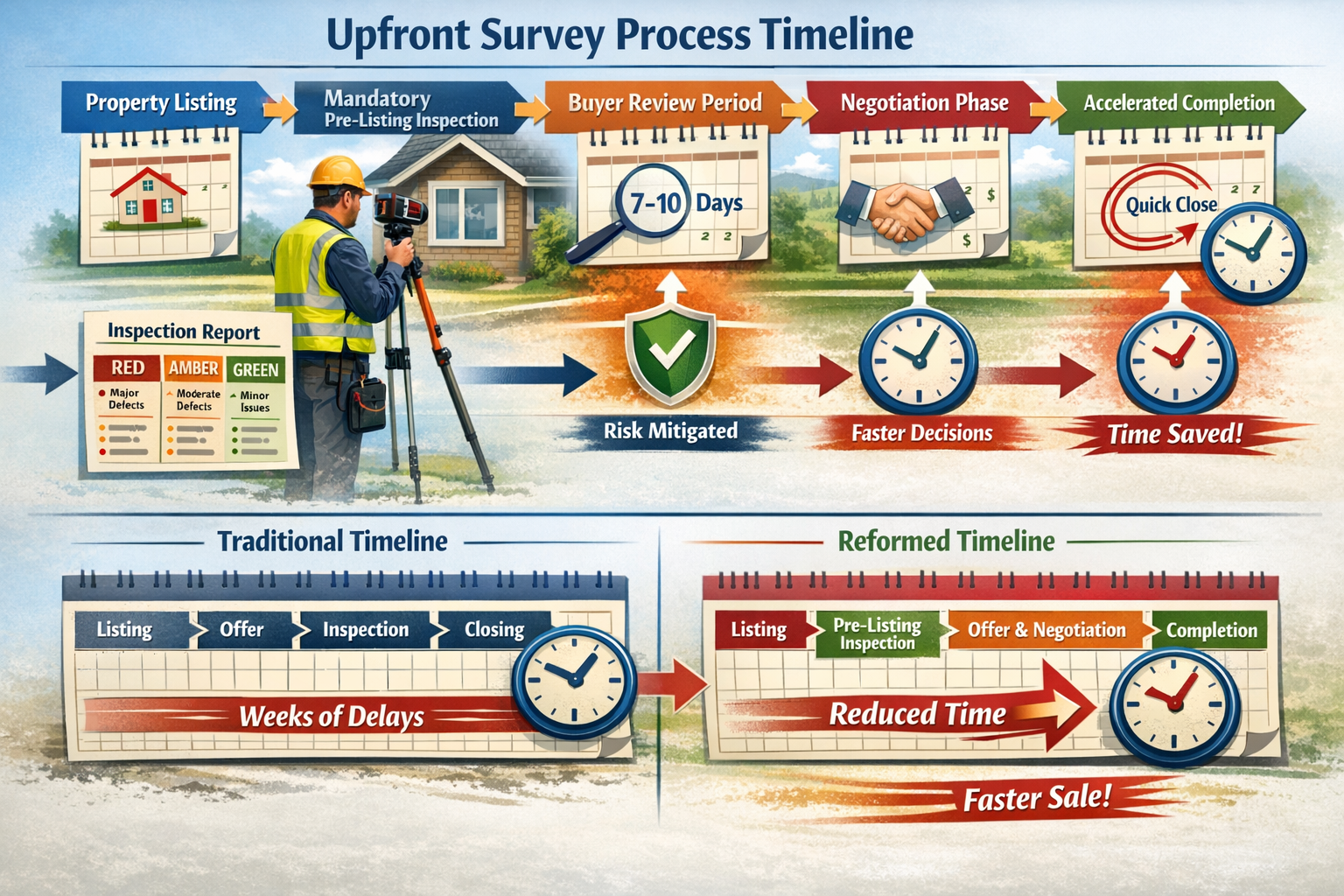

Earlier Inspections and Risk Mitigation Strategies

The shift to earlier inspections fundamentally changes risk management in property transactions. Both buyers and sellers benefit from understanding how building surveys under new homebuying rules: earlier inspections and risk mitigation in 2026 protect their interests.

The Upfront Survey Timeline

Traditional process (pre-2026):

- Property listed → 2. Offer accepted → 3. Survey commissioned → 4. Survey reveals issues → 5. Renegotiation or withdrawal

Reformed process (2026):

- Property assessed pre-listing → 2. Condition report available → 3. Informed offers made → 4. Faster progression to completion

This timeline shift reduces the average transaction time from 12-16 weeks to 8-12 weeks, with some straightforward sales completing even faster[1].

Defect Prioritization Framework

Effective risk mitigation requires systematic defect categorization. Surveyors now use standardized priority levels:

Priority 1 – Urgent (Red):

- Structural instability requiring immediate attention

- Active water ingress causing ongoing damage

- Electrical or fire safety hazards

- Severe subsidence or foundation issues

Priority 2 – Important (Amber):

- Roof repairs needed within 12 months

- Damp issues requiring investigation

- Aging heating systems nearing replacement

- Window or door security concerns

Priority 3 – Maintenance (Green):

- Routine decorative work

- Minor weatherproofing improvements

- Cosmetic repairs

- Preventative maintenance recommendations

This traffic light system enables buyers to quickly assess risk levels and make informed decisions about proceeding with purchases.

Risk Mitigation for Buyers

Before making an offer:

- ✅ Review the upfront condition report thoroughly

- ✅ Identify deal-breaker defects early

- ✅ Budget for known repairs in offer calculations

- ✅ Commission specialist surveys for specific concerns (e.g., drainage surveys, subsidence surveys)

During negotiations:

- ✅ Use prioritized defect lists to justify price adjustments

- ✅ Request seller remediation of urgent issues

- ✅ Obtain repair cost estimates for major defects

- ✅ Consider retention agreements for unresolved issues

Post-purchase protection:

- ✅ Schedule Priority 1 repairs immediately

- ✅ Create maintenance schedules for Priority 2 items

- ✅ Budget for long-term maintenance needs

- ✅ Keep survey reports for future reference

Understanding snagging survey costs becomes particularly relevant for new-build properties, where additional inspections may complement standard surveys.

Risk Mitigation for Sellers

Pre-listing preparation:

- ✅ Commission a pre-sale survey to identify issues

- ✅ Address urgent defects before marketing

- ✅ Obtain repair quotes for known problems

- ✅ Gather documentation for completed works

Disclosure strategy:

- ✅ Provide transparent condition information

- ✅ Highlight recent improvements and maintenance

- ✅ Offer warranties for recent repair work

- ✅ Price realistically based on property condition

Transaction management:

- ✅ Respond promptly to survey queries

- ✅ Provide access for specialist inspections

- ✅ Consider negotiation flexibility for genuine defects

- ✅ Maintain realistic expectations about price adjustments

Specialist Survey Integration

Certain property types or conditions require additional specialized assessments beyond standard RICS surveys:

Structural concerns: Engage structural engineers for foundation issues, cracking, or movement

Commercial elements: Commercial building surveys for mixed-use properties

New construction: Snagging reports for recently completed builds

Boundary disputes: Boundary surveys to resolve property line questions

Rental properties: Compliance with new Decent Homes Standard requirements, including mandatory child-resistant window restrictors on windows presenting fall risks

These specialist assessments complement primary surveys and provide comprehensive risk assessment for complex properties.

How Surveyors Can Adapt Reports for Faster Transactions

Building surveyors must evolve their practices to meet the demands of building surveys under new homebuying rules: earlier inspections and risk mitigation in 2026. Speed, clarity, and digital accessibility become paramount without compromising professional standards.

Digital Transformation in Survey Reporting

Cloud-based platforms:

Modern survey reports need instant accessibility. Cloud platforms enable:

- Real-time report access for all stakeholders

- Mobile-friendly formats for on-the-go review

- Secure sharing with solicitors, lenders, and agents

- Version control and update tracking

Enhanced visual documentation:

- High-resolution photographs with annotations

- Thermal imaging for hidden defects

- Drone footage for roof and chimney assessments

- 360-degree virtual property tours

- Video walkthroughs highlighting key concerns

Interactive reporting features:

- Clickable defect locations on floor plans

- Expandable sections for detailed explanations

- Embedded cost estimate calculators

- Priority filtering (show only urgent issues)

- Downloadable summary reports for quick review

Standardized Report Templates

Consistency across the industry facilitates faster decision-making. Standardized templates should include:

Executive summary (1 page):

- Overall condition rating

- Critical defects requiring immediate attention

- Estimated repair costs (ranges)

- Recommendation to proceed, negotiate, or withdraw

Priority matrix:

- Visual grid showing defect severity vs. urgency

- Color-coded categories for quick scanning

- Estimated timeframes for repairs

- Indicative cost brackets

Detailed findings:

- Room-by-room assessments

- Structural element analysis

- Building services evaluation

- External envelope condition

- Grounds and boundaries

Maintenance schedule:

- Short-term priorities (0-6 months)

- Medium-term needs (6-24 months)

- Long-term planning (2-5 years)

- Ongoing maintenance recommendations

Training and Compliance Essentials

Surveyors must stay current with evolving standards and regulations. Essential training areas include:

Regulatory updates:

- RICS professional standards revisions

- Building safety regulations post-Grenfell

- Fire safety requirements for high-rise buildings (18+ meters requiring two staircases from September 2026)

- Energy performance requirements

Technology proficiency:

- Digital survey tools and equipment

- Report writing software

- Data security and GDPR compliance

- Client communication platforms

Communication skills:

- Translating technical findings for lay audiences

- Managing client expectations

- Handling difficult conversations about defects

- Negotiation support and guidance

For comprehensive preparation, surveyors should consult resources on preparing for 2026 homebuying reforms[2].

Quality Without Compromise

Speed cannot come at the expense of thoroughness. Surveyors maintain quality through:

Systematic inspection protocols:

- Comprehensive checklists for each property type

- Standardized defect identification criteria

- Consistent photographic documentation

- Thorough note-taking during inspections

Peer review processes:

- Second-opinion reviews for complex findings

- Quality assurance checks before report release

- Continuous professional development

- Regular calibration of assessment standards

Professional indemnity considerations:

- Adequate insurance coverage for accelerated timelines

- Clear scope-of-work documentation

- Limitation clauses where appropriate

- Transparent communication about inspection constraints

Client Communication Strategies

Effective communication accelerates understanding and decision-making:

Pre-inspection briefings:

- Explain survey scope and limitations

- Set realistic expectations about turnaround times

- Discuss property-specific concerns

- Clarify reporting format and accessibility

Post-inspection consultations:

- Offer telephone or video debriefs

- Walk through key findings in plain language

- Answer questions about repair priorities

- Provide guidance on next steps

Ongoing support:

- Availability for follow-up questions

- Recommendations for specialist contractors

- Assistance with lender or solicitor queries

- Support during negotiation phases

Understanding that many buyers experience house survey anxiety, surveyors who communicate clearly and compassionately add significant value beyond technical reporting.

Navigating Lender Requirements and Insurance Implications

The reformed homebuying process affects not just buyers and sellers, but also mortgage lenders and insurers who rely on survey information for risk assessment.

Lender Survey Requirements

Minimum standards:

Most lenders now require at minimum a Level 2 HomeBuyer Report for properties over 50 years old, with Level 3 surveys mandatory for:

- Properties built before 1900

- Non-standard construction types

- Properties with known structural issues

- Homes requiring significant renovation

Valuation vs. survey:

It's crucial to understand that a mortgage valuation is not a building survey. Valuations assess market value for lending purposes, while surveys evaluate property condition for buyer protection.

Upfront survey benefits for lenders:

- Reduced mortgage fraud risk

- Better informed lending decisions

- Lower default rates from unexpected repair costs

- Faster mortgage processing with pre-existing condition reports

Insurance Considerations

Buildings insurance:

Survey reports inform insurance underwriting:

- Known defects may require disclosure

- Unrepaired Priority 1 issues could affect coverage

- Some insurers offer premium reductions for recently surveyed properties

- Specialist policies may be needed for non-standard construction

Survey-related insurance:

- Professional indemnity insurance for surveyors

- Survey report insurance protecting buyers against missed defects

- Warranty products for specific building elements

Cost-Benefit Analysis of Earlier Inspections

Understanding the financial implications of building surveys under new homebuying rules: earlier inspections and risk mitigation in 2026 helps stakeholders make informed decisions.

Direct Costs

Survey fees:

- Level 1: £300-£500

- Level 2: £450-£900

- Level 3: £600-£1,500+

- Specialist surveys: £200-£800 each

Additional assessment costs:

- Structural engineer reports: £500-£1,200

- Drainage surveys: £300-£600

- Electrical safety certificates: £150-£300

- Energy Performance Certificates: £60-£120

Indirect Benefits

Avoided costs:

- Reduced transaction fall-throughs (average cost: £3,000-£5,000 per failed purchase)

- Eliminated renegotiation delays

- Prevented post-purchase surprise repairs

- Reduced legal fees from streamlined processes

Time savings:

- 4-6 weeks faster completion on average

- Reduced temporary accommodation costs

- Earlier access to property for renovations

- Minimized chain disruption

Negotiating power:

A comprehensive survey report provides concrete evidence for:

- Price reduction requests (average: 5-15% for significant defects)

- Seller-funded repairs before completion

- Retention agreements for unresolved issues

- Informed walk-away decisions before significant costs

For those questioning whether a homebuyer's survey is worth it, the reformed system makes the value proposition clearer than ever.

Regional Variations and Market Adaptation

The implementation of 2026 reforms may vary across UK regions, with different property markets adapting at different paces.

London and Southeast

Market characteristics:

- Higher property values justify comprehensive surveys

- Greater surveyor availability and competition

- Faster adoption of digital reporting tools

- More complex properties requiring specialist assessments

Typical survey choices:

- Level 2 for standard flats and modern houses

- Level 3 for period properties and conversions

- Multiple specialist surveys for high-value properties

Regional Markets

Northern England, Wales, Scotland:

- More traditional construction types

- Higher proportion of older properties

- Potentially slower technology adoption

- Greater emphasis on structural assessments

Rural vs. Urban:

- Rural properties often require more extensive surveys

- Access challenges may affect inspection timelines

- Specialist surveys for agricultural buildings or land

- Limited surveyor availability in remote areas

Future Developments and Industry Evolution

The 2026 reforms represent the beginning of ongoing transformation in property transactions.

Technology Integration

Emerging tools:

- AI-assisted defect identification

- Automated report generation

- Blockchain-based property condition histories

- Integrated transaction platforms linking all stakeholders

Data analytics:

- Predictive maintenance modeling

- Comparative market analysis for repair costs

- Regional defect pattern identification

- Historical property performance tracking

Regulatory Evolution

Anticipated developments:

- Standardized national survey databases

- Mandatory survey portability between buyers

- Enhanced building safety requirements

- Stricter energy efficiency standards

Professional standards:

- Continuous RICS standard updates

- Enhanced surveyor certification requirements

- Specialized credentials for complex property types

- Mandatory continuing professional development

Conclusion

Building surveys under new homebuying rules: earlier inspections and risk mitigation in 2026 represents a fundamental shift in UK property transactions. The move toward mandatory upfront condition assessments promises faster, more transparent, and less stressful homebuying experiences for all parties.

For buyers, the reformed system provides unprecedented access to property condition information before making financial commitments. The ability to review comprehensive survey reports early in the process enables informed decision-making, realistic budgeting, and confident negotiations.

For sellers, upfront surveys may seem like an additional burden, but they actually facilitate faster sales, reduce fall-throughs, and attract serious buyers who appreciate transparency. Properties with clear condition reports often command premium prices when defects are minimal or when sellers demonstrate proactive maintenance.

For surveyors, 2026 brings both challenges and opportunities. Those who embrace digital tools, streamline reporting processes, and enhance communication skills will thrive in the accelerated transaction environment. The profession's importance has never been greater, with surveyors serving as essential gatekeepers of property quality and transaction integrity.

Actionable Next Steps

For homebuyers:

- Research RICS home survey options appropriate for your target property type

- Budget for survey costs early in your property search

- Request upfront condition reports before making offers

- Engage qualified surveyors with proven track records

- Use survey findings strategically in negotiations

For sellers:

- Commission a pre-sale survey to identify issues before listing

- Address urgent defects to maximize property appeal

- Gather documentation for completed maintenance and improvements

- Price realistically based on condition assessment

- Prepare for transparent disclosure of property condition

For surveyors:

- Invest in digital reporting tools and platforms

- Pursue training on 2026 regulatory requirements

- Develop standardized report templates for efficiency

- Enhance client communication and support services

- Build specialist expertise in high-demand property types

The transformation of homebuying processes in 2026 marks a positive evolution toward greater efficiency, transparency, and consumer protection. By understanding and embracing these changes, all stakeholders can navigate the reformed landscape successfully and benefit from faster, more reliable property transactions.

For comprehensive guidance on navigating building surveys under the new rules, consult with qualified chartered surveyors who understand both traditional best practices and emerging regulatory requirements.

References

[1] Impact Of Homebuying Reforms On Building Surveyors Mandatory Upfront Condition Assessments In 2026 – https://nottinghillsurveyors.com/blog/impact-of-homebuying-reforms-on-building-surveyors-mandatory-upfront-condition-assessments-in-2026

[2] Preparing Building Surveyors For 2026 Homebuying Reforms Rics Training And Compliance Essentials – https://nottinghillsurveyors.com/blog/preparing-building-surveyors-for-2026-homebuying-reforms-rics-training-and-compliance-essentials