A net balance of -35% for house prices recorded in the RICS UK Residential Market Survey for May 2026 tells a story that many surveyors in the South East and East Anglia already know from the ground up: the market has not simply slowed, it has entered a period of cautious, uneven stabilisation that demands precise, defensible valuations [1]. Valuing stabilised house prices in lagging regions: RICS techniques for South East and East Anglia 2026 is therefore not an academic exercise. It is a practical discipline that determines whether a mortgage is approved, an estate is settled fairly, or a buyer avoids overpaying in a market that still carries significant downside risk.

Key Takeaways

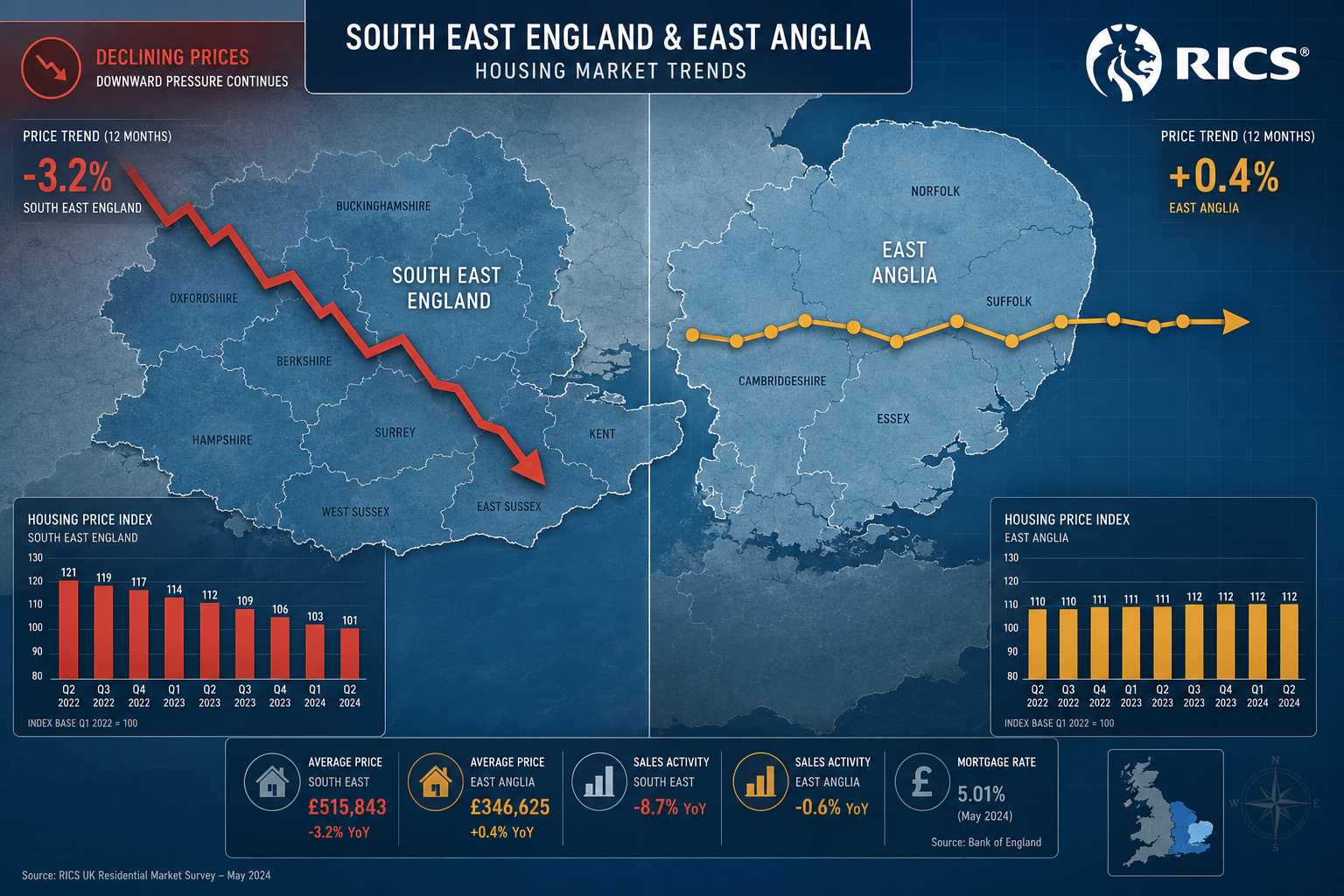

- The South East and East Anglia continue to lag behind national recovery signals, with buyer demand, sales volumes, and short-term price expectations all recording negative net balances in 2026.

- RICS-endorsed valuation methods — particularly the comparable and investment approaches — require careful calibration in affordability-challenged, low-transaction markets.

- Surveyors must treat withdrawn listings, price reductions, and extended time-on-market as active market signals, not background noise.

- Conservative, evidence-led adjustments are the most defensible strategy when comparable evidence is thin or contradictory.

- Twelve-month price expectations have turned marginally positive (+6%), suggesting stabilisation is emerging — but regional divergence means local evidence must always override national sentiment.

Understanding the Regional Lag: South East and East Anglia in 2026

Before any valuation technique can be applied correctly, the market context must be understood clearly. The South East and East Anglia are not simply experiencing the same pressures as the rest of England at a slower pace. They are experiencing a structurally distinct set of affordability constraints that have created a persistent lag relative to regions such as Scotland and Northern Ireland, where price growth has continued [5].

The Data Picture in 2026

The January 2026 RICS survey recorded a national net balance for prices of -10%, an improvement from -19% in October 2025, suggesting early stabilisation at a headline level [5]. However, that headline masks pronounced regional divergence. The South East and East Anglia recorded more significant downward pressure, driven by:

- Affordability ceilings: House price-to-earnings ratios in commuter belt towns remain stretched, limiting the pool of qualifying buyers.

- Weak buyer demand: April 2026 recorded a net balance of -34% for new buyer enquiries nationally, with the South East among the softer performers [2].

- Declining sales volumes: A net balance of -36% in sales activity for April 2026 reflects a market where agreed sales are genuinely scarce [2].

- Negative short-term expectations: As of May 2026, a net balance of -45% of surveyors anticipated further price declines over the following three months [1].

The one constructive signal is that 12-month price expectations have turned marginally positive at +6% [1]. This does not mean prices are rising. It means that the market may be approaching a floor — which is precisely the condition that makes accurate, stabilisation-era valuation both more important and more technically demanding.

| Indicator | Net Balance (2026) | Direction |

|---|---|---|

| House prices (May 2026) | -35% | Declining |

| New buyer enquiries (Apr 2026) | -34% | Weak |

| Sales volumes (Apr 2026) | -36% | Falling |

| 3-month price expectations (May 2026) | -45% | Negative |

| 12-month price expectations (May 2026) | +6% | Marginally positive |

Core RICS Valuation Methods Applied to Stabilised Markets

RICS endorses three primary valuation approaches — market, income, and cost — within which five specific methods are deployed: comparable, investment, profits, residual, and depreciated replacement cost [3]. In stabilised or declining regional markets, the choice of method and the quality of adjustments made within it are what separate a defensible valuation from one that will be challenged.

The Comparable Method: The Primary Tool and Its Limitations

The comparable method remains the most widely used approach for residential property valuation. It relies on recent, arm's-length transactions of similar properties to establish a market value. In active markets, this is straightforward. In the South East and East Anglia in 2026, it requires considerably more discipline.

Key adjustments surveyors must make in low-transaction environments:

- Time adjustments: When comparable sales are more than three months old in a declining market, a downward time adjustment is necessary. Using a stale comparable without adjustment will produce an inflated figure.

- Condition and specification adjustments: Properties that sold quickly may have been priced below market sentiment, while those with extended marketing periods may reflect price reductions from an original aspirational asking price.

- Price reduction analysis: Withdrawn listings and publicly visible price reductions are legitimate market signals. RICS guidance supports treating these as evidence of where the market rejected a price, which is itself informative [6].

- Location micro-adjustments: Within the South East, there are significant sub-market differences. A commuter town with direct rail access to London will behave differently from a coastal town in East Anglia with limited employment links.

"In regions experiencing market cooling, valuers are advised to adopt conservative approaches, prioritising recent transactions and considering withdrawn listings and price reductions as market signals." [6]

For surveyors seeking to understand the full scope of what a property survey covers before a valuation is commissioned, the complete guide to buying a house survey provides useful context for clients navigating this process.

The Investment Method: Relevant for Mixed-Use and Rental Stock

East Anglia in particular contains a significant proportion of properties that function as rental investments, including coastal holiday lets and agricultural worker accommodation. The investment method — which capitalises a property's income stream at an appropriate yield — is relevant here, but yields must be calibrated to current market conditions.

In a market where tenant demand is also softening, gross-to-net income deductions for voids, management fees, and maintenance must be applied conservatively. Yield compression assumptions that may have been reasonable in 2021 or 2022 are not defensible in 2026.

The Depreciated Replacement Cost Method: Heritage and Non-Standard Stock

Approximately 20% of English housing pre-dates 1919 [8]. In the South East and East Anglia, this includes a substantial stock of listed buildings, flint cottages, timber-framed farmhouses, and Victorian seaside villas. Where comparable evidence is thin or non-existent for heritage properties, the depreciated replacement cost (DRC) method provides a structured alternative.

The DRC approach requires:

- Estimating the current cost of constructing an equivalent building.

- Applying depreciation for age, condition, and functional obsolescence.

- Adding land value separately.

This method is also relevant for non-standard construction properties, which are more common in rural East Anglia than in urban areas and which present particular challenges when comparable evidence is sought.

For properties requiring a full structural assessment before valuation, a RICS Level 3 Building Survey will identify defects that must be reflected in the final valuation figure.

Practical Valuation Adjustments for Lagging Regions: Defending Assessments in 2026

Valuing stabilised house prices in lagging regions: RICS techniques for South East and East Anglia 2026 ultimately comes down to one professional obligation — producing a figure that can be defended under scrutiny. This section sets out the practical steps surveyors should follow.

Step 1: Build a Robust Comparable Evidence Base

In thin markets, surveyors should cast a wider geographic net while applying tighter time filters. A comparable from a neighbouring town six months ago may be more reliable than a comparable from the same street twelve months ago in a declining market.

Recommended evidence hierarchy:

- Completed sales within the same postcode sector in the last three months.

- Completed sales in comparable locations within the last six months, with time adjustments applied.

- Under-offer properties (used cautiously, as these have not completed).

- Asking prices of active listings (used only as a ceiling, not a floor).

- Withdrawn listings and price reduction histories (used as negative market signals).

Step 2: Apply Transparent, Documented Adjustments

Every adjustment made to a comparable must be documented with a rationale. In a market where lenders, solicitors, and clients may challenge a valuation, the paper trail is as important as the figure itself.

Common adjustment categories include:

- Size: Price per square metre adjustments for floor area differences.

- Condition: Percentage deductions for properties requiring significant remedial work.

- Tenure: Leasehold properties with short unexpired terms require specific adjustments — the cost of a lease extension is a material factor that must be reflected.

- Aspect and amenity: Garden size, parking, and outlook all affect value in ways that must be quantified rather than assumed.

Step 3: Assess Climate and Environmental Risk

RICS guidance now explicitly encourages valuers to account for extreme conditions, including climate change impacts, in their assessments [7]. This is particularly relevant in East Anglia, where coastal erosion, flood risk, and agricultural land drainage issues affect a meaningful proportion of the housing stock.

A property in a flood-risk zone in Norfolk or Suffolk carries a measurable value discount that must be reflected in the comparable analysis. Insurance costs, mortgage availability, and resale liquidity are all affected by flood risk designation, and these factors compound in a market already experiencing weak demand.

Step 4: Calibrate for Specific Valuation Purposes

The purpose of a valuation affects the methodology and the appropriate level of conservatism. RICS-registered valuers must be clear about which standard they are working to:

- Mortgage valuations: Lenders require a figure reflecting current market value, which in a declining market means the surveyor must resist pressure to support a purchase price that the evidence does not justify.

- Help to Buy and shared ownership: These government-backed schemes have specific RICS requirements. Surveyors handling RICS Help to Buy valuations or shared ownership valuations must apply the relevant Red Book standards precisely.

- Probate valuations: Estate administration requires a valuation at the date of death, which may differ significantly from current market value if the market has moved since then. The probate valuation process has its own evidential requirements.

- Right to Buy: Council tenants exercising their right to purchase require an independent valuation. Right to Buy valuations must reflect open market value without the sitting tenant discount already applied by the local authority.

Step 5: Document Market Conditions Explicitly

A valuation report produced in 2026 for a property in the South East or East Anglia should include an explicit market conditions section that references the current RICS survey data. This protects the valuer professionally and ensures the client understands the context of the figure provided.

The RICS APC Valuation competency — a core technical requirement across Commercial Real Estate and Residential pathways — emphasises strict adherence to RICS Valuation Global Standards (the Red Book) [9]. Surveyors should ensure their reports meet these standards in full, particularly when market conditions are unusual or when the evidence base is thinner than normal.

Valuation Costs in Context

As of April 2026, the average cost of a RICS house valuation was approximately £354, varying by property type, size, and location [4]. In the South East, where property values are higher and the complexity of the valuation exercise is greater, fees at the upper end of this range are standard. Clients should understand that a thorough, defensible valuation in a challenging market requires more professional time than a straightforward assessment in an active market.

Working with RICS registered valuers who hold the relevant Red Book competencies and have active knowledge of South East and East Anglia sub-markets is the most reliable way to ensure that a valuation will withstand scrutiny.

Conclusion

The combination of weak buyer demand, falling sales volumes, and negative short-term price expectations makes the South East and East Anglia two of the most technically demanding regions for residential valuation in England in 2026. The stabilisation signals emerging at a national level do not yet translate into straightforward comparable evidence at a local level, which means that surveyors must work harder to justify their figures and document their reasoning more thoroughly than in a rising market.

Actionable next steps for surveyors and property professionals:

- Refresh comparable evidence databases monthly rather than quarterly in declining markets — stale data produces indefensible figures.

- Treat price reductions and withdrawn listings as formal market evidence, not anecdotal background.

- Apply explicit time adjustments to any comparable more than 90 days old in a market recording negative price net balances.

- For heritage, non-standard, or flood-risk properties, consider whether the comparable method alone is sufficient or whether a DRC or investment approach should supplement it.

- Ensure all reports include a market conditions narrative that references current RICS survey data, protecting both the valuer and the client.

- Engage with the RICS APC Valuation competency framework to ensure methodology remains aligned with Red Book requirements, particularly for specialist valuation types such as Help to Buy, shared ownership, and probate.

The professionals who navigate this market most effectively will be those who treat conservative, evidence-led valuation not as a limitation but as a professional strength — one that protects clients, supports lenders, and upholds the integrity of the market itself.

References

[1] UK Residential Survey May 2026 – https://www.rics.org/news-insights/uk-residential-survey-may-2026?utm_source=openai

[2] House Sales Under Pressure As Buyer Demand Remains Weak RICS – https://theintermediary.co.uk/2026/05/house-sales-under-pressure-as-buyer-demand-remains-weak-rics/?utm_source=openai

[3] APC 5 Valuation Methods – https://ww3.rics.org/uk/en/journals/property-journal/apc-5-valuation-methods.html?utm_source=openai

[4] RICS Valuation Cost – https://www.comparemymove.com/guides/surveying/rics-valuation-cost?utm_source=openai

[5] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution?utm_source=openai

[6] Regional Valuation Strategies Post RICS February 2026 Survey North West Growth Vs London Price Cooling – https://wimbledonsurveyors.com/regional-valuation-strategies-post-rics-february-2026-survey-north-west-growth-vs-london-price-cooling/?utm_source=openai

[7] Real Estate Valuation Extreme Conditions – https://ww3.rics.org/uk/en/journals/property-journal/real-estate-valuation-extreme-conditions.html?utm_source=openai

[8] Valuing Heritage Assets – https://ww3.rics.org/uk/en/journals/property-journal/valuing-heritage-assets.html?utm_source=openai

[9] APC Valuation Competency Advice – https://ww3.rics.org/uk/en/journals/property-journal/apc-valuation-competency-advice.html?utm_source=openai