More than seven years after the Grenfell Tower tragedy, an estimated 1.5 million leaseholders in England alone still live in buildings with unresolved fire safety defects — and the challenge of accurately valuing those properties remains one of the most complex tasks a residential surveyor faces in 2026. Valuing Properties Affected by Cladding, Fire Safety Remediation and EWS1: A Practical Guide for Residential Surveyors is not just a professional standard; it is a structured framework that helps valuers navigate legal obligations, lender requirements, and real-world market stigma in a single coherent methodology.

This guide breaks down that methodology step by step, covering everything from the correct use of the EWS1 form to adjusting for remediation costs and reporting obligations under the latest RICS standards.

Key Takeaways 🔑

- EWS1 forms should only be requested when there is a defined reason to do so — not automatically for every flat in a tall building.

- The new RICS standard takes effect on 1 November 2026, with early adoption strongly encouraged [3].

- An EWS1 form is a valuation and lending tool only — it is not a fire safety certificate [7].

- Valuers must account for remediation funding, market stigma, and lender appetite when forming an opinion of value.

- Buyers should always obtain a copy of the building's fire risk assessment before exchange of contracts [7].

Understanding the EWS1 Form: Scope, Purpose and Limitations

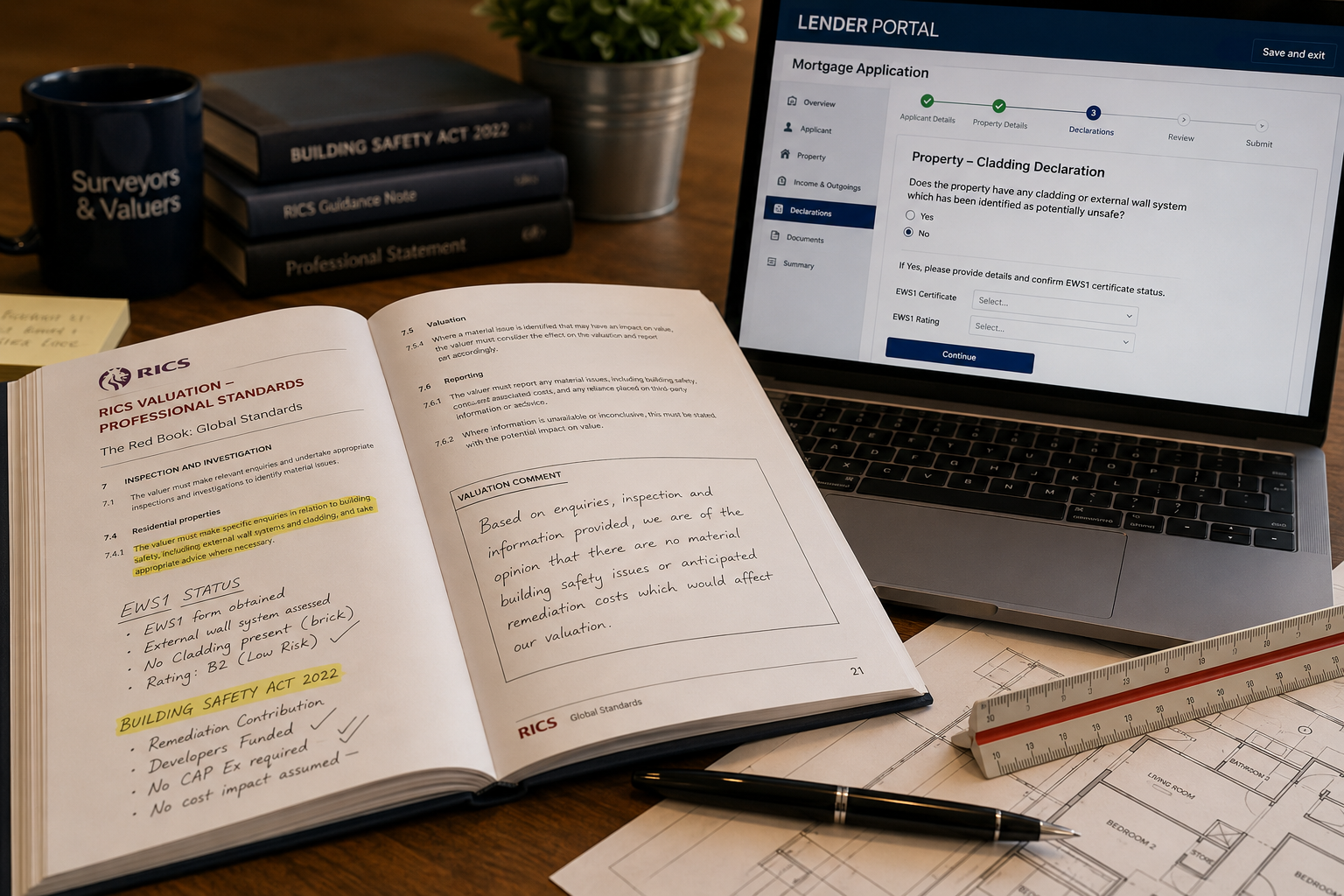

What Is an EWS1 Form?

The External Wall System (EWS1) form was introduced in December 2019 as a standardised way for building owners to confirm to lenders and valuers whether the external wall construction of a residential building had been assessed for fire safety. It is completed by a qualified professional — typically a fire engineer or similarly competent person — and records whether the external wall materials require further investigation or remediation.

💡 Pull Quote: "An EWS1 form is intended for valuation and lending purposes only and does not serve as a fire safety certificate or replace a professional life safety fire risk assessment." — RICS [7]

It is critical that surveyors understand what the EWS1 form does not do:

- It does not assess internal fire safety features such as compartmentation, sprinklers, or fire doors.

- It does not replace a full fire risk assessment under the Regulatory Reform (Fire Safety) Order 2005.

- It does not guarantee that a building is safe to occupy.

Buyers should be advised to seek a copy of the existing fire risk assessment for the building before purchasing, as the EWS1 form cannot substitute for that document [7].

When Should a Valuer Request an EWS1 Form?

Under the updated RICS guidance, valuers are advised to request an EWS1 form only when there is a defined reason to do so [1]. This proportionate approach was developed following consultations with fire safety professionals, valuers, insurers, and lenders [2]. The aim is to reduce unnecessary delays for buyers, sellers, and homeowners seeking to remortgage.

Defined reasons to request an EWS1 form typically include:

| Trigger | Example |

|---|---|

| Visible cladding on the external wall | ACM, HPL, or other potentially combustible panels |

| Balconies with combustible materials | Timber-decked or GRP balconies |

| Insulation concerns | Suspected combustible insulation behind render |

| Lender requirement | Specific lender policy triggers |

For buildings where there is no cladding and no combustible materials on the external wall, an EWS1 form is generally not required. This distinction is important: requesting one unnecessarily can stall transactions and cause distress to leaseholders.

A Structured Methodology for Valuing Properties Affected by Cladding, Fire Safety Remediation and EWS1

Step 1: Pre-Inspection Research

Before attending the property, the valuer should gather as much information as possible about the building's fire safety status. This includes:

- Checking whether the building is registered on the Building Safety Register (for buildings over 18m in England).

- Identifying whether a Principal Accountable Person has been appointed under the Building Safety Act 2022.

- Reviewing any publicly available information about the building's participation in government remediation schemes.

- Confirming whether an EWS1 form already exists for the building — and if so, its category outcome.

The RICS guidance explicitly requires valuers to maintain awareness of the latest government regulations and advice throughout the valuation process [6]. This is a professional duty, not an optional step.

For a broader understanding of what a chartered surveyor is expected to examine during an inspection, see this guide on what a surveyor checks during a property inspection.

Step 2: On-Site Inspection

During the physical inspection, the valuer should note and record:

- External wall construction: Identify cladding type, insulation, and any visible defects or repairs.

- Building height: Determine whether the building falls within the scope of the Building Safety Act (over 11m or 5+ storeys for some provisions; over 18m for higher-risk building status).

- Signage and notices: Fire evacuation strategy (stay put vs. simultaneous evacuation), waking watch arrangements, or interim measures.

- Condition of common parts: Evidence of fire door upgrades, sprinkler retrofits, or ongoing remediation works.

🔍 Important: Even if the subject property is a lower-floor flat, the valuation must reflect the status of the entire building, not just the individual unit.

Step 3: Reviewing the EWS1 Form (Where Available)

EWS1 outcomes fall into two broad categories — Category A (no combustible cladding) and Category B (combustible cladding present) — each with sub-ratings:

| EWS1 Rating | Meaning | Typical Lender Response |

|---|---|---|

| A1 | No cladding, no action needed | Mortgage available |

| A2 | Cladding present, no action needed | Mortgage usually available |

| A3 | Cladding present, action needed | Lender caution; may decline |

| B1 | Combustible cladding, low risk | Mortgage may be available |

| B2 | Combustible cladding, high risk | Mortgage often declined |

A B2 rating is the most serious outcome and will typically result in a lender declining to lend until remediation is complete or funding is confirmed. The valuer must reflect this in the valuation narrative.

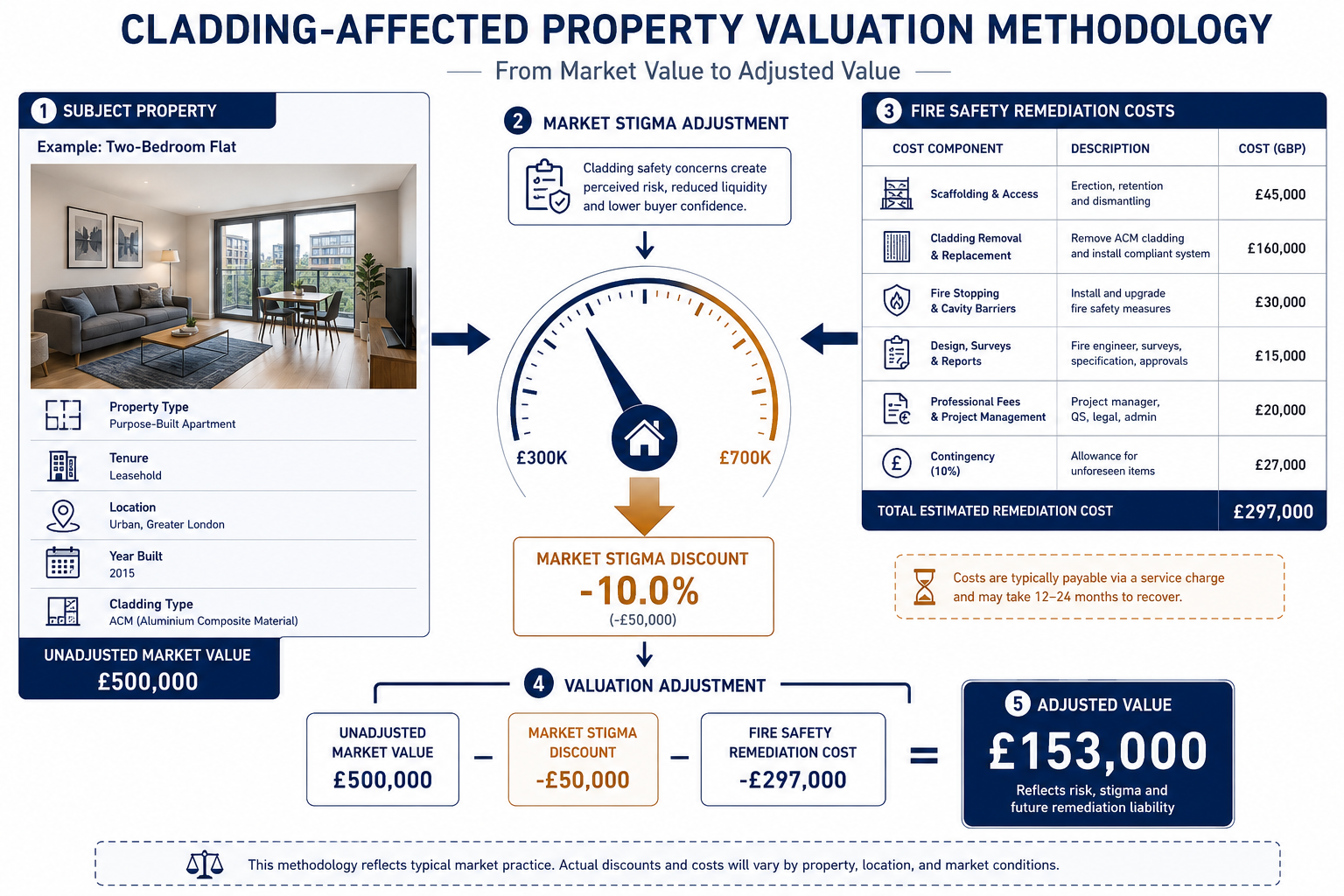

Step 4: Assessing Remediation Funding and Liability

This is arguably the most complex element of valuing properties affected by cladding, fire safety remediation and EWS1. The valuer must determine:

Who is paying for remediation?

- Developer remediation: Under the Building Safety Act 2022 and the Developer Remediation Contract, qualifying developers have committed to remediate buildings they developed or refurbished. Where a developer has signed the contract and works are scheduled, this significantly reduces the financial burden on leaseholders.

- Building Safety Fund (BSF): For buildings over 18m where the developer is insolvent or cannot be traced, the BSF provides government funding. Confirmed BSF funding removes leaseholder liability and should positively influence value.

- Leaseholder-funded remediation: Where no external funding is available and costs fall to leaseholders, the impact on value can be severe. Legal protections under the Building Safety Act 2022 cap qualifying leaseholders' contributions, but the position must be carefully verified.

The RICS guidance takes into account the effect of government remediation schemes in England and Wales and their impact on property values [5]. Valuers must clearly state in their report which funding position applies and how it has influenced their opinion of value.

💡 Pull Quote: "Where remediation funding is confirmed and leaseholder liability is extinguished, the valuation discount for fire safety risk may be significantly reduced or eliminated."

Step 5: Quantifying Market Stigma

Even where remediation is fully funded and underway, market stigma can depress values. This occurs because:

- Buyers and their solicitors may be uncertain about timescales for completion of works.

- Some lenders remain cautious even after funding confirmation.

- Prospective buyers may simply prefer buildings without a fire safety history.

Valuers should use comparable evidence from similar buildings in similar remediation positions to support any stigma adjustment. Where comparables are limited, the valuer should explain their reasoning clearly, referencing the building's specific circumstances.

For context on how professional valuers approach complex residential assessments, a RICS Red Book valuation provides the formal framework within which these opinions must be expressed.

Reporting Obligations and the Updated RICS Standard

The New RICS Standard: What Changes in November 2026?

The updated RICS standard for valuing homes in multi-storey, multi-occupancy residential buildings with cladding takes effect on 1 November 2026, with the professional body encouraging early adoption [3]. The standard applies to:

- Multi-storey, multi-occupancy residential buildings with cladding [2].

- Mixed-use blocks of flats where the residential element includes cladding.

- Buildings in England, Wales, Scotland, and Northern Ireland (with jurisdiction-specific variations).

The UK government has confirmed its support for the guidance, recognising it as a risk-based and proportionate basis for valuation assessments [4]. Major lenders, including those represented by UK Finance and the Building Societies Association, have welcomed the updated guidance and anticipate it will reduce the number of EWS1 requests [4].

What Must a Valuation Report Include?

A compliant valuation report for a cladding-affected property should address the following:

✅ Mandatory report elements:

- Building description: Height, number of storeys, construction type, cladding materials identified.

- EWS1 status: Whether a form exists, its category, date of assessment, and the name of the assessing professional.

- Remediation position: Funding source confirmed, works scheduled, or liability outstanding.

- Lender-specific considerations: Any known lender restrictions based on EWS1 outcome or building height.

- Market evidence: Comparables used, with commentary on how fire safety status has been reflected.

- Assumptions and special assumptions: Clearly stated, particularly where the valuation is conditional on remediation completion.

- Caveats: Where information is unavailable (e.g., no EWS1 form exists), the valuer must clearly caveat the valuation and recommend further investigation.

For surveyors who want to understand how these obligations sit within the broader context of residential survey work, the complete guide to home surveying provides useful background on professional responsibilities.

Advising Clients: Practical Steps for Buyers

When acting for a buyer purchasing a flat in a cladding-affected building, surveyors should recommend the following actions:

- 📋 Request the EWS1 form (if applicable) and review its category before exchange.

- 🔥 Obtain the building's fire risk assessment — not just the EWS1 form [7].

- 💰 Confirm the remediation funding position with the freeholder or managing agent in writing.

- 🏦 Check lender appetite before proceeding — some lenders have building-specific restrictions.

- ⚖️ Take legal advice on leaseholder protections under the Building Safety Act 2022.

Understanding the full scope of a professional survey is essential before committing to a purchase. A Level 2 HomeBuyer Survey may be appropriate for standard flats, but a more detailed Level 3 Building Survey may be warranted where significant structural or fire safety concerns are identified.

For buyers who want to understand the full financial case for professional advice, this article on why hiring a residential surveyor could save you thousands is worth reading before instructing a valuer.

Common Pitfalls to Avoid

| ❌ Common Mistake | ✅ Best Practice |

|---|---|

| Requesting EWS1 for every flat without justification | Only request when a defined trigger exists [1] |

| Treating EWS1 as a fire safety certificate | Clearly distinguish EWS1 from a fire risk assessment [7] |

| Ignoring remediation funding when valuing | Adjust value based on confirmed funding position [5] |

| Failing to caveat where information is missing | Always state assumptions and limitations clearly |

| Applying a blanket stigma discount | Use market evidence to support any adjustment |

Conclusion: Actionable Next Steps for Residential Surveyors

Valuing properties affected by cladding, fire safety remediation and EWS1 requires a disciplined, evidence-based approach that goes well beyond a standard residential valuation. The stakes are high: an under-informed valuation can trap leaseholders in unsellable properties, while an overly cautious one can stall legitimate transactions unnecessarily.

Here are the key actions every residential surveyor should take in 2026:

- Familiarise yourself with the updated RICS standard ahead of its 1 November 2026 implementation date — early adoption is encouraged [3].

- Build a pre-inspection checklist that covers EWS1 status, remediation funding, and Building Safety Act registration before every relevant instruction.

- Develop a library of cladding-affected comparables in your local market to support evidence-based stigma adjustments.

- Engage with lender panels to understand current lending policies for B1 and B2-rated buildings in your area.

- Advise clients clearly on the distinction between EWS1 forms and fire risk assessments — this is a professional duty, not optional guidance [6].

- Review your professional indemnity position to ensure it covers valuations of higher-risk buildings under the Building Safety Act framework.

The regulatory landscape will continue to evolve as remediation programmes progress. Surveyors who invest in understanding these frameworks now will be best placed to serve their clients — and protect their own professional standing — in the years ahead.

For expert valuation support on cladding-affected properties, or to discuss a specific instruction, explore the RICS-compliant valuation services available from qualified chartered surveyors.

References

[1] Rics Releases Updated Guidance On Home Valuations – https://propertyindustryeye.com/rics-releases-updated-guidance-on-home-valuations/?utm_source=openai

[2] Rics Publishes Updated Standard For Valuation Of Homes In Multi Storey Residential Buildings With Cladding – https://www.housingmmonline.co.uk/news/rics-publishes-updated-standard-for-valuation-of-homes-in-multi-storey-residential-buildings-with-cladding/?utm_source=openai

[3] Updated Valuation Standards For Multi Storey Residential Buildings With Cladding – https://todaysconveyancer.co.uk/updated-valuation-standards-for-multi-storey-residential-buildings-with-cladding/?utm_source=openai

[4] Uk Finance And The Bsa Respond To The Rics Final Guidance On Cladding Valuation – https://www.ukfinance.org.uk/press/press-releases/uk-finance-and-the-bsa-respond-to-the-rics-final-guidance-on-cladding-valuation?utm_source=openai

[5] Valuation Approach For Properties In Residential Buildings With – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards/valuation-approach-for-properties-in-residential-buildings-with-?utm_source=openai

[6] Valuation Approach For Multi Storey Properties With Cladding Ps Dec 2022 – https://www.rics.org/content/dam/ricsglobal/documents/to-be-sorted/valuation-approach-for-multi-storey-properties-with-cladding_ps_dec-2022.pdf?utm_source=openai

[7] Cladding External Wall System Ews Faqs – https://www.rics.org/news-insights/current-topics-campaigns/fire-safety/cladding-external-wall-system-ews-faqs?utm_source=openai