The landscape for high-value property owners and investors has shifted dramatically in 2026. With the introduction of the High Value Council Tax Surcharge (HVCTS) and a noticeable cooling in the prime property market, Valuation Surveys for Properties Over £2 Million: Navigating New Wealth Taxes and Prime Market Slowdown in 2026 has become a critical concern for property owners, buyers, and professionals across England's luxury residential sector.

For the first time, residential properties valued at £2 million or more face an additional annual tax burden, fundamentally changing the financial equation for prime property ownership. Meanwhile, market dynamics in prestigious areas like Prime Central London are experiencing unprecedented shifts, with forecasts revised downward and listing volumes surging. These twin pressures—regulatory and market-driven—make accurate, professional property valuations more essential than ever.

Understanding how to navigate these changes requires expertise in both valuation methodology and the evolving tax landscape. Whether you're purchasing a luxury home, managing a high-value portfolio, or seeking to understand your tax obligations, this comprehensive guide will equip you with the knowledge needed to make informed decisions in 2026's transformed property environment.

Key Takeaways

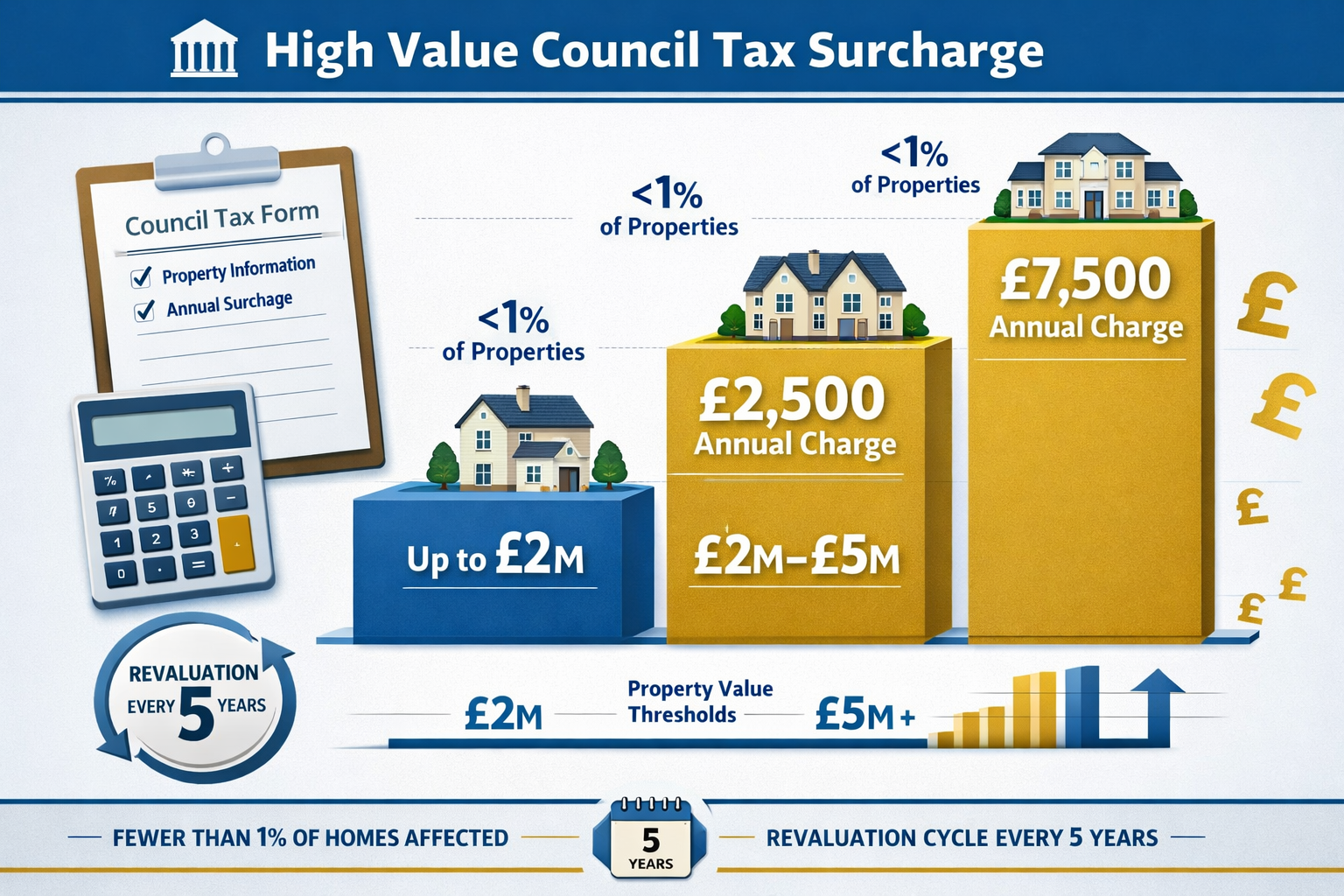

- 💷 New wealth tax: Properties valued over £2 million face a £2,500 annual surcharge, rising to £7,500 for homes worth £5 million or more, affecting fewer than 1% of English properties[1]

- 📊 Market slowdown: Prime Central London prices are forecast to remain steady in 2026, while Greater London growth has been revised down to 2%[4]

- 🔍 Valuation importance: The Valuation Office will conduct targeted revaluations every five years, making accurate professional surveys critical for tax assessment[1]

- 📉 Regional divide: Northern England and Scotland continue to outperform southern markets, with eight of the top ten growth areas located outside the traditional prime southern markets[4]

- 🏡 Strategic timing: Understanding current market conditions and tax thresholds can significantly impact purchase decisions and long-term property investment strategies

Understanding the High Value Council Tax Surcharge in 2026

The High Value Council Tax Surcharge represents one of the most significant reforms to England's property tax system in decades. Introduced in 2026, this new levy addresses what many considered a fundamental fairness gap in the council tax structure[1].

How the HVCTS Works

The surcharge operates as an additional annual charge on top of existing council tax obligations. Here's the breakdown:

| Property Value | Annual Surcharge |

|---|---|

| £2 million – £4.99 million | £2,500 |

| £5 million and above | £7,500 |

This tax structure means that a property valued at £2.5 million in Kensington will incur an extra £2,500 annually, while a £10 million Mayfair mansion faces a £7,500 surcharge[6]. When combined with existing band H council tax (typically around £3,000-£4,000 annually), total property tax obligations for ultra-high-value homes have increased substantially.

The Fairness Argument

The government's rationale for introducing the HVCTS centers on addressing inequities in the current system. Under the previous structure, a typical family home in band D paid approximately £2,280 annually in council tax—more than a £10 million property in band H[1]. This anomaly existed because council tax bands were established in 1991 based on property values at that time, with band H capping at properties worth more than £320,000 in 1991 values.

The introduction of the surcharge creates a more progressive tax system where the wealthiest property owners contribute proportionally more to local services.

Who Is Affected?

Despite the significant impact on individual property owners, the HVCTS affects a remarkably small portion of the market. Fewer than 1% of properties in England are expected to exceed the £2 million threshold[1]. These properties are heavily concentrated in:

- 🏛️ Prime Central London (Kensington, Chelsea, Westminster, Mayfair)

- 🌳 Prime Outer London (Richmond, Wimbledon, Hampstead)

- 🏡 High-value commuter towns (parts of Surrey, Hertfordshire, Buckinghamshire)

- 🏰 Historic market towns with exceptional period properties

For property professionals and owners in these areas, understanding valuation becomes paramount, as crossing the £2 million threshold triggers immediate and ongoing tax consequences.

The Valuation Process: How Properties Are Assessed for the HVCTS

The Valuation Office has been tasked with conducting a comprehensive, targeted valuation exercise to identify all properties above the £2 million threshold[1]. This process differs significantly from standard property valuations and carries substantial financial implications.

Initial Assessment and Revaluation Cycles

The Valuation Office conducts assessments using a combination of:

- Market data analysis from recent sales of comparable properties

- Property characteristics including size, location, condition, and features

- Professional surveyor inspections for properties near the threshold

- Automated valuation models supplemented by manual review

Critically, these valuations are conducted every five years[1], meaning property owners may move in and out of the surcharge bands as market conditions change. A property valued at £1.95 million in 2026 might exceed £2 million in the 2031 revaluation due to market appreciation, triggering the surcharge.

Why Professional Valuation Surveys Matter

Given the financial stakes—£2,500 to £7,500 annually—property owners have strong incentives to ensure valuations are accurate and defensible. This is where professional RICS building surveys and specialized valuation services become invaluable.

Professional valuation surveys provide:

- ✅ Accurate market valuations based on current comparable sales data

- ✅ Detailed property condition assessments that may affect value

- ✅ Documentation to support appeals or challenges to Valuation Office assessments

- ✅ Strategic insights for properties near valuation thresholds

- ✅ Compliance with RICS Red Book standards for formal valuations

For properties valued close to the £2 million or £5 million thresholds, even a small adjustment in valuation can result in significant annual savings. A property assessed at £2.05 million faces a £2,500 surcharge, while a successful challenge reducing the valuation to £1.95 million eliminates the charge entirely.

Red Book Valuations and HVCTS Compliance

The Royal Institution of Chartered Surveyors (RICS) Red Book provides the professional standards for property valuations in the UK. For high-value properties subject to the HVCTS, obtaining a Red Book valuation offers several advantages:

- Professional credibility when challenging Valuation Office assessments

- Standardized methodology recognized by tax authorities

- Comprehensive reporting that documents all value-affecting factors

- Expert witness capability if disputes escalate to tribunal

Property owners should consider commissioning independent Red Book valuations before the five-year revaluation cycles, particularly if they believe their property may be overvalued or if significant defects or market changes have affected value.

Challenging Valuations

If a property owner disagrees with the Valuation Office assessment, formal challenge mechanisms exist. Supporting documentation from professional surveyors, including:

- Detailed building surveys identifying defects

- Comparative market analysis

- Evidence of property-specific factors affecting value

- Professional valuation reports from RICS-accredited surveyors

These elements strengthen appeals and increase the likelihood of successful valuation adjustments.

Prime Market Slowdown: Understanding 2026's Shifting Landscape

While the HVCTS introduces new tax obligations, the broader prime property market is experiencing its own transformation in 2026. Valuation Surveys for Properties Over £2 Million: Navigating New Wealth Taxes and Prime Market Slowdown in 2026 must account for both regulatory changes and fundamental market dynamics.

Prime Central London: From Growth to Stability

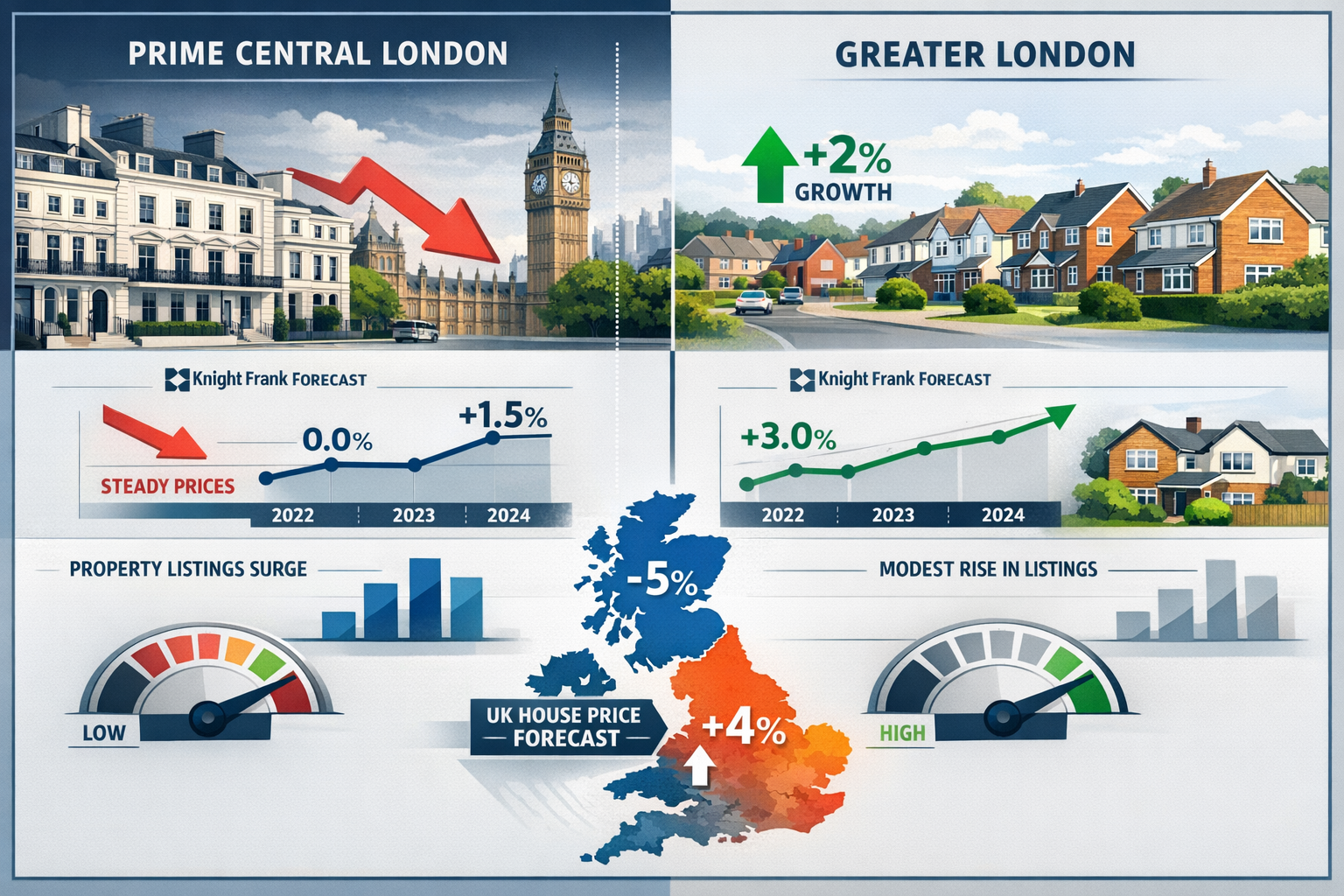

Prime Central London has long been considered one of the world's most resilient luxury property markets. However, 2026 forecasts tell a different story. Knight Frank, one of the leading authorities on prime property, has revised its predictions, now expecting Prime Central London prices to hold steady rather than appreciate[4].

This represents a significant shift from previous growth trajectories and reflects several converging factors:

- 📊 Surge in property listings: Supply has increased as some owners seek to exit before tax changes fully materialize

- 💼 Weaker buyer confidence: Economic uncertainty and new tax burdens have dampened demand

- 🌍 International buyer hesitation: Currency fluctuations and global economic concerns affect overseas purchasers

- 🏛️ Policy uncertainty: Ongoing discussions about further wealth taxes create investment caution

Greater London and Prime Outer London Forecasts

The slowdown extends beyond the most exclusive central postcodes:

| Market Segment | Previous Forecast | Revised 2026 Forecast | Change |

|---|---|---|---|

| Prime Central London | Modest growth | Steady (0%) | Downward revision |

| Greater London | 3% growth | 2% growth | -1% revision[4] |

| Prime Outer London | 3.5% growth | 2% growth | -1.5% revision[4] |

These downward revisions reflect the combined impact of the HVCTS, broader economic conditions, and shifting buyer preferences. Areas like Richmond, Wimbledon, and Hampstead—traditionally strong performers—are experiencing more modest appreciation than anticipated.

The North-South Divide Intensifies

One of the most striking features of the 2026 property market is the persistent north-south divide. As of late 2025 and continuing into 2026, eight of the top ten areas showing the biggest price growth are located in northern or central England and Scotland[4].

This geographical shift reflects:

- 💰 Relative affordability in northern markets attracting first-time buyers and investors

- 🏢 Remote work flexibility reducing the premium on London proximity

- 🏗️ Infrastructure investment in northern cities improving connectivity and amenities

- 📈 Higher growth potential from lower baseline prices

For investors and property professionals, this suggests opportunities may lie outside traditional prime southern markets, while southern high-value properties face headwinds from both market dynamics and new taxation.

National Market Context

To understand the prime market slowdown, it's helpful to contextualize it within broader UK property trends:

The average UK house price in early 2026 stands at approximately £271,000, with expectations for around 2% growth over the course of the year[2][3]. Various industry forecasters project:

- Nationwide: 2–4% growth

- Halifax: 1–3% growth

- Zoopla: Approximately 1.5% growth

- Rightmove: 2% growth

- Hamptons: 2.5% growth by year-end[2]

Interestingly, semi-detached and terraced houses are projected to appreciate 2.5–3.5% in 2026, outperforming both the national average and the prime market[2]. This suggests family homes in mid-market segments remain more resilient than ultra-high-value properties.

Long-Term Outlook: 2026-2030

Despite near-term headwinds, longer-term projections remain moderately optimistic. Over a five-year horizon (2026–2030), UK property prices are expected to rise approximately 22% cumulatively, potentially moving the average home from £271,000 to roughly £330,000[2].

For prime properties, this long-term perspective is crucial. While 2026 may represent a period of consolidation and adjustment, the fundamental drivers of prime property value—scarcity, location quality, and wealth concentration—remain intact. Property owners and investors with longer time horizons may view current market conditions as a normalization rather than a permanent decline.

Strategic Considerations for Valuation Surveys in the High-Value Segment

Given the dual challenges of new wealth taxes and market slowdown, Valuation Surveys for Properties Over £2 Million: Navigating New Wealth Taxes and Prime Market Slowdown in 2026 requires strategic thinking beyond simple property assessment.

Timing Your Valuation

The timing of professional valuations can significantly impact both tax obligations and transaction outcomes:

For Sellers:

- 📅 Pre-listing valuations help set realistic asking prices in a slower market

- 💡 Identifying value-enhancing improvements before marketing can maximize returns

- 🔍 Understanding defects allows for proactive remediation or price adjustment

- 📊 Market positioning based on accurate valuation prevents extended listing periods

For Buyers:

- ✅ Pre-purchase surveys identify issues that may affect value and tax classification

- 💷 Negotiating power from identified defects can reduce purchase price below tax thresholds

- 🏛️ Future tax planning based on current and projected valuations

- 📋 Due diligence protects against overpaying in a softening market

Comprehensive Survey Types for High-Value Properties

Different survey types serve different purposes in the high-value property context. Understanding when to commission each type is essential:

RICS Building Survey (Level 3)

The most comprehensive option, RICS building surveys provide detailed analysis of property condition, defects, and repair recommendations. For properties over £2 million, this level of detail is often warranted given:

- Complex architectural features common in period properties

- Higher stakes for both purchase decisions and tax assessments

- Greater financial capacity to address identified issues

- Need for comprehensive documentation for valuation purposes

A thorough Level 3 home survey can identify structural issues, damp, subsidence, or other defects that materially affect property value.

Specific Defect Surveys

When particular concerns exist—such as visible cracking, water damage, or structural movement—a RICS specific defect survey provides targeted investigation. These focused assessments can:

- Quantify repair costs that may justify valuation reductions

- Provide evidence for price negotiations

- Inform decisions about whether to proceed with purchases

- Support appeals to Valuation Office assessments

Reinstatement Cost Valuations

For insurance purposes and comprehensive financial planning, reinstatement cost valuations determine the cost to rebuild a property from scratch. This differs from market value but is essential for:

- Adequate insurance coverage on high-value properties

- Understanding total asset exposure

- Estate planning and wealth management

- Mortgage and lending requirements

Insurance reinstatement valuations ensure properties aren't underinsured—a common problem with period and luxury homes featuring bespoke finishes and architectural details.

Valuation Factors Specific to Properties Over £2 Million

High-value properties present unique valuation challenges that standard approaches may not fully capture:

Location Premiums:

- Proximity to elite schools, parks, and cultural amenities

- Exclusive postcodes and street prestige

- Privacy and security features

- Access to private clubs and services

Architectural and Historical Significance:

- Listed building status and heritage value

- Architect pedigree and design significance

- Period features and original details

- Restoration quality and authenticity

Bespoke Features and Finishes:

- Custom kitchens and bathrooms from premium brands

- Smart home technology and automation

- Wine cellars, home cinemas, and leisure facilities

- Landscaping and garden design

Condition and Maintenance:

- Recent refurbishment and modernization

- Ongoing maintenance programs

- Building defects and deferred maintenance

- Energy efficiency and sustainability features

Professional surveyors experienced in the prime market understand how these factors interact to determine value and can provide nuanced assessments that generic valuation models miss.

Tax Planning Strategies

Strategic property owners are employing various approaches to manage HVCTS obligations:

Threshold Management:

For properties valued near £2 million or £5 million, small value adjustments can eliminate or reduce surcharges. Strategies include:

- Commissioning professional valuations that accurately reflect defects and condition issues

- Timing major improvements to occur after valuation cycles

- Considering whether certain chattels (removable items) should be excluded from valuations

- Documenting market-specific factors that may depress value

Portfolio Restructuring:

Some high-value property owners are reconsidering their holdings:

- Selling properties just above thresholds and purchasing slightly below

- Diversifying from single high-value properties to multiple mid-value properties

- Relocating from Prime Central London to Prime Outer London or regional markets

- Transferring properties into different ownership structures (though tax advice is essential)

Long-Term Holding Strategies:

For those committed to prime property ownership despite new taxes:

- Accepting the surcharge as part of total ownership costs

- Focusing on properties with strong long-term appreciation potential

- Prioritizing locations and property types with enduring scarcity value

- Maintaining properties to preserve value across revaluation cycles

Working with Professional Surveyors: What to Expect

Engaging qualified professionals for Valuation Surveys for Properties Over £2 Million: Navigating New Wealth Taxes and Prime Market Slowdown in 2026 requires understanding the process and selecting the right expertise.

Choosing the Right Surveyor

Not all surveyors have equivalent experience with high-value properties. When selecting a professional, consider:

✅ RICS Accreditation: Ensure your surveyor is a member of the Royal Institution of Chartered Surveyors, which sets professional and ethical standards.

✅ Prime Market Experience: Look for surveyors with demonstrated expertise in properties over £2 million, particularly in your specific location.

✅ Valuation Specialization: For HVCTS purposes, surveyors experienced in formal Red Book valuations offer additional credibility.

✅ Local Knowledge: Understanding micro-markets within prime areas (specific streets, buildings, or developments) is crucial for accurate valuations.

✅ Comprehensive Services: Firms offering multiple survey types can provide integrated advice across different needs.

The Survey Process

A typical comprehensive survey for a high-value property follows this timeline:

- Initial Consultation (1-2 days): Discuss property specifics, concerns, and survey objectives

- Site Inspection (0.5-1 day): Detailed examination of the property, typically lasting several hours for large or complex properties

- Analysis and Research (3-5 days): Comparable sales research, defect analysis, and valuation calculations

- Report Preparation (2-3 days): Comprehensive written report with photographs, findings, and recommendations

- Report Delivery and Discussion (1 day): Presentation of findings and opportunity for questions

Total turnaround time typically ranges from 7-14 days for standard surveys, though complex properties or urgent requests may vary.

Understanding Survey Reports

Professional survey reports for high-value properties typically include:

- Executive Summary: Key findings and valuation conclusions

- Property Description: Detailed description of construction, layout, and features

- Condition Assessment: Room-by-room analysis of condition and defects

- Defect Analysis: Categorization of issues by severity and urgency

- Repair Recommendations: Guidance on addressing identified problems

- Valuation Section: Market value assessment with supporting evidence

- Photographic Evidence: Images documenting key features and defects

- Comparable Sales Data: Evidence of recent transactions supporting valuation

For properties near HVCTS thresholds, particular attention should be paid to the valuation section and any factors that materially affect value.

Cost Considerations

Professional survey costs for high-value properties reflect the expertise required and the stakes involved:

| Survey Type | Typical Cost Range | Best For |

|---|---|---|

| RICS Building Survey (Level 3) | £1,500 – £4,000+ | Comprehensive assessment of properties over £2m |

| Red Book Valuation | £1,000 – £3,000+ | Formal valuations for tax, legal, or lending purposes |

| Specific Defect Survey | £500 – £2,000 | Targeted investigation of particular concerns |

| Reinstatement Valuation | £800 – £2,500 | Insurance purposes for high-value properties |

While these costs may seem substantial, they represent a small fraction of potential tax savings or protection against overpaying. A £3,000 survey that results in a valuation reduction from £2.05 million to £1.95 million saves £2,500 annually—paying for itself in just over one year.

Regional Variations: Where the HVCTS Has Greatest Impact

The High Value Council Tax Surcharge affects different regions very differently, creating geographical hotspots of impact and opportunity.

London: The Primary Impact Zone

Unsurprisingly, London bears the brunt of the HVCTS, with the vast majority of affected properties concentrated in the capital:

Prime Central London Boroughs:

- Kensington & Chelsea: The highest concentration of properties over £2 million

- Westminster: Mayfair, Belgravia, and St. James's contain numerous ultra-high-value properties

- Camden: Hampstead and Primrose Hill feature significant numbers of affected properties

Prime Outer London:

- Richmond upon Thames: Riverside properties and period homes frequently exceed thresholds

- Wandsworth: Clapham, Battersea, and Wandsworth Common areas include many high-value properties

- Hammersmith & Fulham: Selective streets and developments cross the £2 million mark

For property professionals and owners in these areas, understanding local market dynamics through experienced chartered surveyors in Central London or specialists in specific boroughs like Hammersmith, Fulham, or Islington is essential.

The Commuter Belt

Beyond London, certain commuter towns and counties contain pockets of high-value properties:

Surrey:

- Weybridge, Cobham, and Esher feature substantial properties regularly exceeding £2 million

- Proximity to London and excellent schools drive premium valuations

- Chartered surveyors in Weybridge and Leatherhead understand local market nuances

Hertfordshire:

- St. Albans, Harpenden, and parts of Watford contain high-value period properties

- Historic market towns with excellent transport links command premium prices

- Local expertise from chartered surveyors in St Albans, Watford, and Hemel Hempstead provides market insight

Other Hotspots:

- Buckinghamshire: Beaconsfield, Gerrards Cross, and surrounding villages

- Berkshire: Windsor, Ascot, and Maidenhead areas

- Hampshire: Winchester and select New Forest locations

Working with chartered surveyors in Hampshire or Hertfordshire who understand regional markets ensures valuations reflect local conditions rather than generic national trends.

Areas of Minimal Impact

The HVCTS has negligible effect in most of the UK. In northern England, Scotland, Wales, and many parts of southern England outside London and the commuter belt, fewer than 0.1% of properties exceed the £2 million threshold.

This geographical concentration creates interesting market dynamics. Some high-net-worth individuals are considering relocating from affected areas to regions where property values remain well below thresholds, securing larger properties with superior amenities while avoiding the surcharge entirely.

Future-Proofing: Preparing for the Next Five Years

With revaluations scheduled every five years, property owners must think strategically about the 2026-2031 period and beyond.

Market Appreciation and Threshold Crossing

Even with the current market slowdown, properties valued near £2 million today may exceed that threshold in the 2031 revaluation. The projected 22% cumulative price growth over 2026-2030[2] means:

- A property worth £1.8 million in 2026 could reach £2.2 million by 2031

- Properties currently just below the £5 million threshold may cross into the higher surcharge band

- Strategic decisions made today have multi-year tax implications

Maintenance and Value Preservation

For properties already subject to the HVCTS, maintaining value becomes a dual consideration:

Preventing Value Decline:

- Regular maintenance prevents defects that could reduce valuations

- Addressing issues promptly maintains property condition

- Modernization keeps properties competitive in their market segment

Strategic Improvements:

- Timing major improvements to occur after revaluation cycles maximizes benefit

- Focus on improvements that enhance livability rather than pushing value over thresholds

- Consider whether certain upgrades are worth the potential tax implications

Documentation and Record-Keeping

Maintaining comprehensive property records supports future valuation challenges:

- Survey reports documenting condition at various points in time

- Maintenance records showing repairs and improvements

- Comparable sales data for your area and property type

- Professional correspondence with surveyors and valuers

- Photographic evidence of property condition and any deterioration

This documentation becomes invaluable when challenging Valuation Office assessments or supporting specific valuation positions.

Monitoring Market Conditions

Staying informed about prime market trends helps property owners make timely decisions:

- Track local sales data and price trends in your specific micro-market

- Monitor economic indicators affecting high-value property demand

- Stay updated on potential tax policy changes that could affect property ownership

- Maintain relationships with professional advisors who understand the prime market

The Broader Context: Wealth Taxes and Property Ownership

The HVCTS exists within a broader discussion about wealth taxation in the UK. Understanding this context helps property owners anticipate potential future changes.

The Wealth Tax Debate

Property has long been considered an undertaxed form of wealth in the UK compared to income and consumption. The HVCTS represents a modest step toward addressing this, but discussions continue about:

- Annual wealth taxes on total net worth above certain thresholds

- Mansion taxes with multiple tiers rather than just two bands

- Capital gains tax reforms affecting property sales

- Inheritance tax changes impacting intergenerational wealth transfer

While the HVCTS itself is relatively modest—£2,500 to £7,500 annually—it may signal the beginning of more comprehensive wealth taxation targeting high-value property owners.

International Comparisons

The UK's approach to high-value property taxation remains relatively light compared to some international jurisdictions:

- France imposes wealth taxes on worldwide assets for residents

- Switzerland has cantonal wealth taxes varying by region

- Spain charges annual wealth tax on property and assets

- United States has property taxes typically ranging from 0.5-2% of value annually

In this context, the HVCTS represents a moderate policy intervention rather than an extreme measure, though it does represent a philosophical shift in UK property taxation.

Political Considerations

Tax policy remains subject to political change. Property owners should be aware that:

- Different political parties have varying positions on wealth taxation

- Economic conditions may drive policy changes

- Public opinion on wealth inequality influences tax policy debates

- International tax competition affects how aggressively the UK taxes wealth

While predicting future policy changes is impossible, maintaining flexibility in property holdings and staying informed about political developments helps property owners adapt to changing circumstances.

Practical Action Steps for Property Owners and Buyers

Whether you currently own a property over £2 million, are considering purchasing one, or own a property approaching the threshold, specific actions can help you navigate the current environment.

For Current Owners of Properties Over £2 Million

-

Commission a Professional Valuation: Obtain an independent Red Book valuation to understand where your property stands relative to thresholds and whether the Valuation Office assessment is accurate.

-

Conduct a Comprehensive Building Survey: If you haven't had a recent building survey, commission one to identify any defects or issues that might affect value or justify a valuation challenge.

-

Review Your Property Portfolio: Consider whether your current holdings remain optimal given new tax obligations and market conditions.

-

Maintain Detailed Records: Document all maintenance, improvements, and professional assessments for future reference.

-

Consult Tax Advisors: Ensure you understand all tax implications and explore legitimate planning opportunities.

For Prospective Buyers of High-Value Properties

-

Factor HVCTS into Affordability Calculations: Include the annual surcharge in your total cost of ownership analysis.

-

Commission Pre-Purchase Surveys: Invest in comprehensive RICS building surveys to understand exactly what you're buying and identify negotiating points.

-

Consider Properties Just Below Thresholds: Properties valued at £1.8-£1.95 million may offer better value than those just over £2 million, avoiding the surcharge while providing similar amenities.

-

Negotiate Based on Tax Implications: Use HVCTS obligations as a negotiating point, particularly for properties marginally over thresholds.

-

Think Long-Term: Consider how market appreciation might affect future tax obligations and whether the property remains a good investment across multiple revaluation cycles.

For Owners of Properties Approaching £2 Million

-

Monitor Your Property's Value: Stay informed about local market conditions and comparable sales that might indicate your property is approaching the threshold.

-

Time Improvements Strategically: Consider whether major improvements should be deferred until after the next revaluation cycle.

-

Obtain Baseline Valuations: Commission professional valuations now to establish a documented baseline for future reference.

-

Understand Your Options: If your property is likely to exceed £2 million in the next revaluation, consider whether selling before that occurs makes financial sense.

-

Plan for the Surcharge: If threshold crossing seems inevitable, incorporate the future tax obligation into your financial planning.

Conclusion: Navigating the New Landscape with Confidence

Valuation Surveys for Properties Over £2 Million: Navigating New Wealth Taxes and Prime Market Slowdown in 2026 represents more than just a technical challenge—it's a fundamental shift in how high-value property ownership is structured in England. The introduction of the High Value Council Tax Surcharge, combined with a cooling prime market, creates a complex environment requiring professional expertise and strategic thinking.

The key insights for property owners, buyers, and professionals are clear:

🎯 Professional valuations are no longer optional—they're essential tools for managing tax obligations, making informed purchase decisions, and challenging potentially inaccurate assessments.

🎯 Market conditions favor informed buyers—the prime market slowdown creates opportunities for those who understand true property values and can identify properties offering genuine value.

🎯 Strategic timing matters—understanding revaluation cycles, market trends, and tax thresholds enables better decision-making about when to buy, sell, improve, or hold properties.

🎯 Expertise pays dividends—working with experienced chartered surveyors who understand both the technical aspects of valuation and the nuances of prime markets provides competitive advantages worth far more than their fees.

🎯 Long-term thinking wins—while 2026 presents challenges, the fundamental appeal of prime property remains intact for those with appropriate time horizons and financial resources.

Your Next Steps

Don't navigate this complex landscape alone. Whether you're dealing with HVCTS obligations, considering a high-value property purchase, or simply want to understand your property's true value in the current market, professional guidance makes all the difference.

Take action today:

- Schedule a professional valuation to understand exactly where your property stands

- Commission a comprehensive building survey if you're purchasing or haven't had a recent assessment

- Consult with experienced surveyors who understand prime markets and current tax implications

- Review your property strategy in light of new taxes and market conditions

- Stay informed about market trends, tax policy developments, and valuation best practices

The property market has always rewarded those who combine professional expertise with strategic thinking. In 2026's transformed landscape, that principle is more important than ever. By understanding the interplay between valuations, taxation, and market dynamics, you can make confident decisions that protect your interests and maximize your property's value—both now and in the years ahead.

For expert guidance on valuation reports and comprehensive survey services tailored to high-value properties, connect with qualified professionals who understand the unique challenges of the 2026 market. Your property deserves nothing less than the highest standard of professional assessment and strategic advice.

References

[1] High Value Council Tax Surcharge – https://www.gov.uk/government/publications/high-value-council-tax-surcharge/high-value-council-tax-surcharge

[2] Uk Price Forecasts – https://investropa.com/blogs/news/uk-price-forecasts

[3] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/

[4] The 2026 Uk Property Market Outlook – https://nedbankprivatewealth.com/insights/the-2026-uk-property-market-outlook/

[5] The 2026 Property Reset Market Forecasts Budget Impacts Investor Focus – https://surveyingcorp.com/2025/12/the-2026-property-reset-market-forecasts-budget-impacts-investor-focus/

[6] Rightmove 2026 Uk House Price Predictions – https://www.proffitt-holt.co.uk/articles/rightmove-2026-uk-house-price-predictions