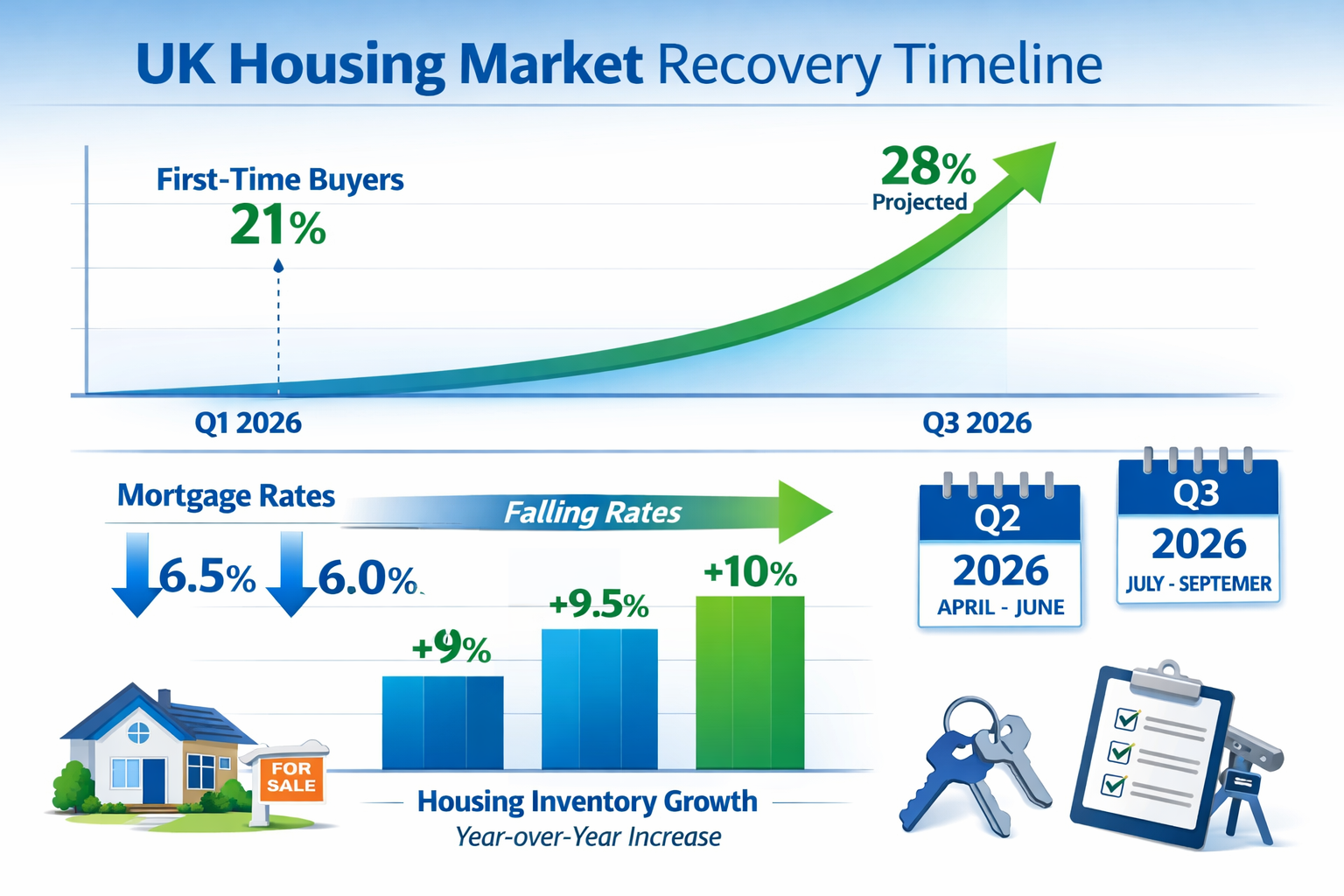

First-time homebuyers currently represent just 21% of the market—a record low—with the typical buyer age reaching an unprecedented 40 years old[2]. Yet RICS February 2026 survey data reveals a surprising reversal: first-time buyers are now leading the recovery despite cautious market sentiment. As mortgage rates decline toward 6.00% and inventory expands for the third consecutive year, surveyor firms face an urgent operational challenge: scaling capacity to meet surging demand for building surveys during the critical Q2-Q3 2026 recovery window.

This surge in First-Time Buyer Market Surge and Building Survey Demand: Scaling Surveyor Operations for Q2-Q3 2026 Recovery requires immediate strategic planning. With the National Association of Realtors estimating that declining mortgage rates could activate 5.5 million buyers, including 1.6 million renters currently on the sidelines[2], surveying firms must prepare for unprecedented demand while maintaining quality standards and competitive turnaround times.

Key Takeaways

- 🏠 First-time buyers are leading the 2026 market recovery, with RICS data showing increased activity despite overall cautious sentiment

- 📈 Building survey demand is projected to surge 25-40% in Q2-Q3 2026 as mortgage rates decline and inventory expands 9-10% year-over-year

- ⚡ Surveyor firms must scale operations strategically through technology adoption, workforce planning, and quality assurance protocols

- 🎯 Turnaround time management becomes critical, with first-time buyers requiring faster survey completion timelines to secure competitive properties

- 💡 Regional variations require flexible capacity allocation, with South and Midwest markets showing stronger growth than coastal regions

Understanding the First-Time Buyer Market Surge and Building Survey Demand: Scaling Surveyor Operations for Q2-Q3 2026 Recovery

The Market Dynamics Driving First-Time Buyer Activity

The 2026 housing market represents a fundamental shift from the challenges of recent years. While first-time buyers have been largely sidelined, multiple converging factors are creating a perfect storm of opportunity for this demographic:

Mortgage Rate Trajectory: Financial analysts project mortgage rates declining to approximately 6.00% by mid-2026, down from peaks exceeding 7.5% in 2023-2024[2]. This seemingly modest decline translates to significant purchasing power restoration for first-time buyers operating on tight budgets.

Inventory Expansion: Active listings are expected to rise 9-10% year-over-year in 2026, marking the third consecutive year of inventory gains[2]. This expansion directly benefits first-time buyers who previously faced bidding wars and limited selection in constrained markets.

Affordability Improvements: Zillow's four key affordability metrics show promising trends:

- More affordable rent today (reducing savings barriers)

- Increased homes within reach for median-income buyers

- Reduced competition for affordable listings

- Higher concentration of households in prime homebuying years (ages 29-43)[1]

Regional Price Stabilization: Markets like Rochester, NY project 10.3% appreciation while Birmingham, AL forecasts 6.2% growth[1]—modest increases that allow first-time buyers to enter without fear of being priced out immediately.

Why Building Surveys Become Critical for First-Time Buyers

First-time buyers represent a unique client segment for surveying firms. Unlike experienced buyers or investors, they:

✅ Lack property assessment experience and rely heavily on professional surveys to identify issues

✅ Operate with limited financial buffers, making unexpected repair costs potentially catastrophic

✅ Require comprehensive education about property conditions and maintenance requirements

✅ Depend on survey findings for mortgage approval and negotiation leverage

This demographic shift toward first-time buyer dominance fundamentally changes the surveying landscape. These clients typically request Level 2 surveys or Level 3 building surveys rather than basic valuations, increasing both revenue potential and operational complexity.

The Q2-Q3 2026 Timeline: Why These Quarters Matter

Multiple market analysts project Q2-Q3 2026 as the market stabilization point[3]. This timing creates a compressed window where:

- Buyer confidence returns as rate declines materialize

- Spring/summer seasonal demand peaks naturally

- Inventory reaches optimal levels before potential winter slowdown

- Lenders ease qualification standards in response to competitive pressure

For surveying firms, this means preparing for a 25-40% demand surge concentrated in approximately 6 months—a challenge requiring immediate operational planning.

Operational Challenges in Scaling Surveyor Capacity for First-Time Buyer Market Surge and Building Survey Demand

Workforce Planning and Capacity Constraints

The surveying profession faces unique scaling challenges compared to other service industries:

Qualification Requirements: Only RICS-qualified surveyors can conduct regulated building surveys, creating an immediate talent pool limitation. Verifying surveyor credentials becomes essential when expanding teams rapidly.

Training Timeline: Even experienced construction professionals require 6-12 months of mentorship before conducting independent surveys to RICS standards.

Regional Coverage Gaps: First-time buyer activity concentrates in specific markets—North London, Richmond, Islington, and emerging areas—requiring strategic surveyor deployment.

Seasonal Variation: The Q2-Q3 surge creates feast-or-famine dynamics that make permanent hiring risky without flexible workforce models.

Strategic Workforce Solutions

| Strategy | Implementation | Expected Impact |

|---|---|---|

| Associate Surveyor Network | Develop relationships with qualified independent surveyors for overflow work | 30-50% capacity increase without permanent overhead |

| Apprenticeship Acceleration | Partner with RICS training programs to pipeline talent | Long-term capacity building (12-24 month horizon) |

| Regional Hub Model | Establish satellite offices in high-demand areas | Reduced travel time, increased daily survey capacity |

| Specialist Team Structure | Create dedicated first-time buyer survey teams with streamlined processes | 15-20% efficiency improvement through specialization |

Technology Integration for Efficiency Gains

Modern surveying firms must leverage technology to scale without proportional cost increases:

Digital Inspection Tools: Thermal imaging cameras, moisture meters, and tablet-based checklists reduce on-site time by 20-30% while improving documentation quality.

Automated Report Generation: Template-based reporting systems with pre-populated sections for common property types accelerate report delivery from 5-7 days to 3-4 days.

Client Portal Systems: Self-service booking, document upload, and progress tracking reduce administrative burden by 40%, freeing staff for value-added activities.

Drone Surveys: Roof and exterior inspections via drone technology reduce ladder time and safety risks while providing superior documentation for clients.

Quality Assurance Under Pressure

Scaling operations while maintaining RICS building survey standards represents the primary risk during rapid growth:

🔍 Peer Review Protocols: Implement mandatory senior surveyor review for all reports from associates or junior team members

📋 Standardized Checklists: Develop property-type-specific inspection protocols ensuring consistent coverage across all surveyors

📊 Quality Metrics Dashboard: Track key indicators including client complaints, missed defects (discovered post-purchase), and report comprehensiveness scores

🎓 Continuous Training: Monthly case study reviews and technical updates keep entire team current on emerging issues and best practices

Managing Turnaround Times and Client Expectations for First-Time Buyer Market Surge and Building Survey Demand

The Speed-Quality Balance

First-time buyers in competitive markets face intense pressure to move quickly. Properties receive multiple offers within 48-72 hours of listing in hot markets[5]. This creates unrealistic expectations for survey turnaround times.

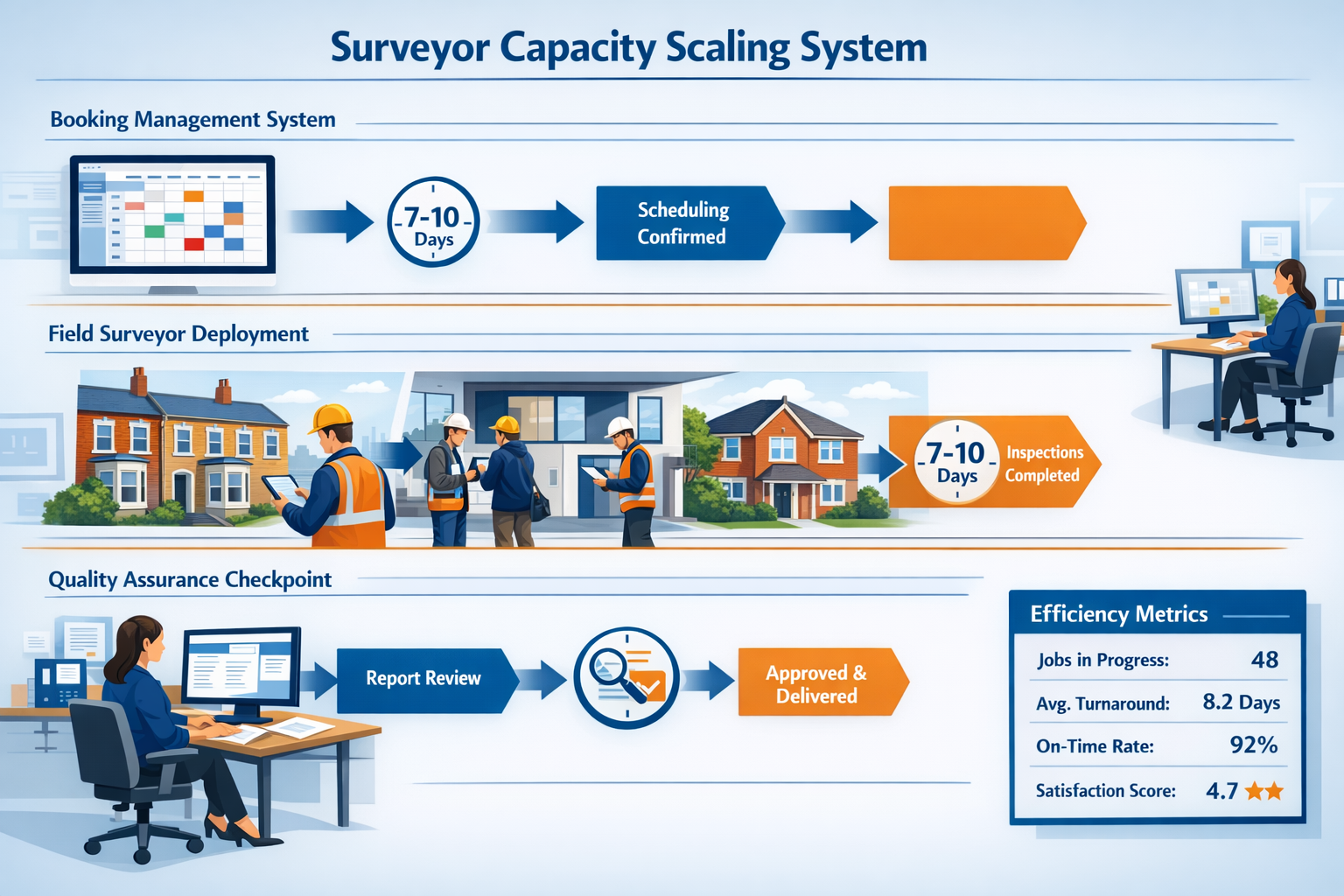

Industry Standard Timeline:

- Initial consultation and booking: 1-2 days

- On-site inspection scheduling: 3-5 days

- Survey completion: 1 day

- Report writing and review: 3-5 days

- Total timeline: 7-14 days[https://nottinghillsurveyors.com/blog/how-long-does-a-home-buyers-survey-take-a-complete-timeline-guide]

First-Time Buyer Expectations:

- Many expect 3-5 day total turnaround

- Some request "rush" services for competitive situations

- Limited understanding of survey complexity

Setting Realistic Expectations

Effective client communication prevents dissatisfaction and negative reviews:

Pre-Booking Education: Explain that thorough surveys require adequate time, and rushed inspections miss critical defects that could cost thousands in repairs.

Tiered Service Options:

- Standard Service: 10-14 day turnaround at base pricing

- Priority Service: 7-9 day turnaround with 20% premium

- Express Service: 4-6 day turnaround with 40% premium (limited availability)

Transparent Scheduling: Provide real-time booking calendars showing actual availability rather than vague "we'll call you" promises.

Progress Updates: Automated notifications when inspection is scheduled, completed, and report enters review phase reduce anxiety and support calls.

Operational Strategies for Faster Turnaround

Meeting compressed timelines without sacrificing quality requires systematic process optimization:

Pre-Inspection Preparation: Gather property details, previous surveys, and specific client concerns before site visit, reducing on-site time by 15-20%.

Mobile Reporting: Surveyors dictate preliminary findings on-site using voice-to-text technology, creating report framework during inspection rather than from memory later.

Report Templates by Era: Victorian, Edwardian, 1930s, post-war, and modern property templates with era-specific common issues accelerate writing while ensuring comprehensive coverage.

Dedicated Report Writers: Administrative staff handle formatting, photo insertion, and document assembly, allowing surveyors to focus on technical analysis and recommendations.

Quality Assurance Protocols for Scaled Operations During First-Time Buyer Market Surge and Building Survey Demand

Maintaining RICS Standards at Scale

The Royal Institution of Chartered Surveyors maintains strict standards for building surveys and homebuyer reports. Rapid scaling introduces quality risks that can damage firm reputation and create professional liability exposure.

Critical Quality Control Points:

-

Pre-Inspection Briefing: Senior surveyor reviews property type, age, and client concerns with assigned surveyor before site visit

-

On-Site Documentation Standards: Minimum photo requirements (100+ images for typical property), mandatory thermal imaging for suspected damp, detailed measurement records

-

Technical Review Gate: All reports undergo technical review by senior surveyor before client delivery, focusing on:

- Structural assessment accuracy

- Damp and timber issue identification

- Electrical and plumbing system evaluation

- Roof condition assessment

- Realistic repair cost estimates

-

Client Feedback Loop: Systematic post-delivery surveys and follow-up calls identify quality issues before they escalate to complaints

-

Continuing Professional Development: Mandatory quarterly training on emerging issues (e.g., cladding concerns, Japanese knotweed identification, modern construction defects)

Specialized Survey Types for First-Time Buyers

Different property types require specialized knowledge and protocols:

Period Properties (Victorian/Edwardian): These homes popular with first-time buyers require expertise in:

- Original feature condition (sash windows, ornate plasterwork, fireplaces)

- Structural movement patterns in solid-wall construction

- Rising damp vs. condensation differentiation

- Historic alteration impact assessment

Leasehold Flats: First-time buyers often purchase flats, requiring additional survey considerations:

- Shared structure assessment limitations

- Service charge and maintenance reserve adequacy

- Lease term implications for mortgageability

- Building insurance arrangements

Modern New-Builds: Surprising defects appear in properties less than 10 years old:

- NHBC warranty coverage verification

- Snagging issues vs. structural concerns

- Modern construction method understanding (timber frame, steel frame, MMC)

- Energy efficiency system functionality

For properties requiring deeper investigation, firms should offer Level 3 building surveys with comprehensive analysis suitable for older or altered properties.

Risk Management and Professional Indemnity

Scaled operations increase professional liability exposure. Robust risk management includes:

Limitation of Liability Clauses: Clear terms of engagement specifying survey scope, limitations (non-invasive inspection), and liability caps

Photographic Evidence: Comprehensive documentation protects against claims that defects were present but not reported

Conservative Cost Estimates: Repair cost ranges rather than precise figures, with recommendations for specialist contractor quotes

Follow-Up Recommendations: Clear guidance when specialist surveys are needed (structural engineers, damp specialists, electrical contractors)

Regional Market Variations and Capacity Allocation

Geographic Demand Patterns

First-time buyer activity concentrates in specific markets based on affordability metrics:

High-Demand UK Markets for Q2-Q3 2026:

🏘️ Outer London Boroughs: Ealing, Hounslow, Hammersmith offer relative affordability with transport links

🌳 Commuter Belt: Berkshire, Essex, Sussex see increased first-time buyer activity as remote work normalizes

🏙️ Regional Cities: Birmingham, Manchester, Leeds offer strong first-time buyer fundamentals with inventory growth

🌊 Coastal Towns: Brighton, Portsmouth, Southampton attract London relocators seeking affordability

Flexible Capacity Allocation Models

Surveying firms must deploy capacity strategically across geographic markets:

Data-Driven Demand Forecasting: Track leading indicators including:

- Mortgage application volumes by postcode

- Estate agent listing velocity

- Local economic indicators (employment, wage growth)

- Regional mortgage rate variations

Mobile Survey Teams: Rather than fixed regional offices, develop teams willing to travel 30-60 minutes to high-demand areas with premium pricing for travel time

Partnership Networks: Establish reciprocal referral relationships with surveying firms in adjacent markets for overflow capacity sharing

Dynamic Pricing: Implement surge pricing (10-20% premium) for high-demand postcodes during peak periods, naturally balancing demand across regions

Technology and Systems for Operational Excellence

Essential Technology Stack for Scaled Operations

Modern surveying firms require integrated technology platforms:

Customer Relationship Management (CRM):

- Lead tracking and conversion optimization

- Automated follow-up sequences

- Client communication history

- Review and referral management

Scheduling and Dispatch:

- Real-time surveyor availability calendars

- Automated appointment booking

- Route optimization for multiple daily surveys

- Mobile app for surveyors with job details and navigation

Report Generation and Delivery:

- Template-based report creation with property-specific customization

- Photo integration and annotation tools

- Automated quality checks (completeness, required sections)

- Secure client portal for report delivery and payment

Financial Management:

- Integrated invoicing and payment processing

- Surveyor commission tracking

- Job costing and profitability analysis

- Financial forecasting based on booking pipeline

Data Analytics for Continuous Improvement

Firms that leverage operational data gain competitive advantages:

Key Performance Indicators (KPIs):

- Average turnaround time by survey type

- Surveyor utilization rates (target: 75-85%)

- Client satisfaction scores (NPS)

- Repeat and referral business percentage

- Revenue per surveyor per day

- Quality control failure rates

Predictive Analytics: Historical booking patterns combined with market indicators forecast demand 4-8 weeks ahead, enabling proactive capacity adjustments

Client Segmentation: First-time buyers, experienced buyers, investors, and estate agents require different service approaches and communication styles

Marketing and Client Acquisition During the Recovery

Positioning for First-Time Buyer Market

First-time buyers research extensively before selecting surveyors. Effective positioning includes:

Educational Content Marketing:

- Blog posts explaining survey types and differences

- Video guides on what happens during inspections

- Case studies showing how surveys saved buyers money

- Downloadable first-time buyer checklists

Transparent Pricing: First-time buyers on tight budgets appreciate clear, upfront pricing rather than "contact for quote" approaches

Social Proof: Testimonials specifically from first-time buyers resonate with this demographic more than generic reviews

Partnership Development: Relationships with first-time buyer mortgage brokers, estate agents specializing in affordable properties, and solicitors generate qualified referrals

Digital Marketing Strategies

With first-time buyers predominantly researching online, digital presence becomes critical:

Local SEO Optimization: Target location-specific keywords like "chartered surveyors in Fulham" or "building surveyors in Putney"

Google Business Profile: Optimized profile with current photos, regular posts, and review management drives local discovery

Paid Search Campaigns: Targeted Google Ads for high-intent keywords during Q2-Q3 peak season

Social Media Presence: Instagram and Facebook content showing survey process, team members, and property insights builds trust with younger first-time buyers

Financial Planning and Investment for Growth

Capital Requirements for Scaling

Preparing for First-Time Buyer Market Surge and Building Survey Demand: Scaling Surveyor Operations for Q2-Q3 2026 Recovery requires strategic investment:

Technology Infrastructure: £15,000-£30,000 for integrated software platforms, mobile devices, and inspection equipment

Marketing and Lead Generation: £20,000-£40,000 for Q2-Q3 digital campaigns and partnership development

Workforce Expansion: £50,000-£100,000 for associate surveyor recruitment, training, and initial compensation

Working Capital: 60-90 day cash reserves to manage payment timing gaps during rapid growth

Revenue Projections and ROI

Conservative growth scenario for mid-sized surveying firm:

Current State (Q1 2026):

- 5 full-time surveyors

- 200 surveys/month

- Average fee: £600

- Monthly revenue: £120,000

Scaled Operations (Q2-Q3 2026):

- 5 full-time + 3 associate surveyors

- 320 surveys/month (60% increase)

- Average fee: £650 (premium for faster service)

- Monthly revenue: £208,000

- Incremental monthly revenue: £88,000

Investment Payback: With approximately £100,000 total investment, payback period is 6-8 weeks of scaled operations, with continued elevated revenue through Q3 2026.

Preparing for Post-Recovery Market Conditions

Sustainable Operations Beyond the Surge

While Q2-Q3 2026 represents peak demand, sustainable firms plan for market normalization:

Flexible Cost Structure: Maintain core permanent team with associate network for surge capacity rather than over-hiring permanent staff

Diversified Service Mix: Develop complementary services for slower periods:

- Commercial building surveys

- Party wall services

- Structural surveys and monitoring

- Dilapidations surveys

Client Retention Programs: First-time buyers become future clients for:

- Renovation project surveys

- Pre-sale condition assessments

- Remortgage valuations

- Investment property surveys

Market Intelligence: Continuous monitoring of inventory levels, mortgage rates, and buyer sentiment enables proactive capacity adjustments

Building Long-Term Competitive Advantages

The firms that thrive post-recovery will have:

✅ Reputation for Quality: Maintained standards during rapid growth, generating positive reviews and referrals

✅ Operational Excellence: Refined processes and technology enabling efficient service delivery at scale

✅ Market Relationships: Strong partnerships with estate agents, mortgage brokers, and solicitors

✅ Brand Recognition: Established presence in key geographic markets through consistent marketing

✅ Team Development: Trained and retained talented surveyors who can handle complex properties independently

Conclusion: Strategic Imperatives for Q2-Q3 2026 Success

The convergence of declining mortgage rates, expanding inventory, and pent-up first-time buyer demand creates an unprecedented opportunity for surveying firms in 2026. However, capitalizing on this First-Time Buyer Market Surge and Building Survey Demand: Scaling Surveyor Operations for Q2-Q3 2026 Recovery requires immediate strategic action.

Critical Success Factors:

-

Start scaling operations now rather than waiting for demand to materialize—recruitment, training, and system implementation require 8-12 weeks minimum

-

Invest in technology infrastructure that enables efficient operations at scale while maintaining quality standards

-

Develop flexible workforce models combining permanent staff with associate networks to manage seasonal variation

-

Implement robust quality assurance protocols preventing reputation damage during rapid growth

-

Position marketing specifically for first-time buyers with educational content, transparent pricing, and social proof

-

Plan for sustainable operations beyond the surge through diversified services and client retention programs

The firms that execute these strategies effectively will not only capture outsized revenue during Q2-Q3 2026 but establish market leadership positions that persist through subsequent market cycles.

Next Steps for Surveying Firms:

📊 Conduct capacity analysis: Calculate current maximum survey volume and identify bottlenecks limiting growth

🤝 Develop associate network: Begin recruiting qualified surveyors for overflow work before peak demand arrives

💻 Evaluate technology gaps: Audit current systems and implement integrated platforms for scheduling, reporting, and client communication

📈 Launch marketing campaigns: Begin educational content and digital advertising targeting first-time buyers in key markets

🎯 Establish quality protocols: Document inspection standards, review processes, and training requirements for consistency

The Q2-Q3 2026 recovery window is approaching rapidly. Surveying firms that begin preparation now will be positioned to capture this historic opportunity while those who delay will watch competitors gain market share during the most significant first-time buyer surge in recent years.

For firms seeking to understand the full scope of services required by first-time buyers, explore our comprehensive guides on what surveyors do and whether home surveys are necessary. The time to scale operations is now—the recovery waits for no one.

References

[1] Is The 2026 Housing Market Finally Opening Doors For First Time Buyers – https://www.kavout.com/market-lens/is-the-2026-housing-market-finally-opening-doors-for-first-time-buyers

[2] Housing Market Outlook – https://www.freedommortgage.com/learn/market-updates/housing-market-outlook

[3] Austin Housing Market Forecast 2026 2027 – https://neuhausre.com/austin-housing-market-forecast-2026-2027/

[4] Watch – https://www.youtube.com/watch?v=Tb2aeEGMhyY

[5] Why Buyers Are Returning To The 2026 Housing Market – https://levelmtg.com/news/why-buyers-are-returning-to-the-2026-housing-market/

[6] Housing Market Forecast 2026 2029 – https://www.noradarealestate.com/blog/housing-market-forecast-2026-2029/