}

Fewer than 1% of Scottish properties will be directly affected by the new council tax bands introduced in the 2026 Scottish Budget — yet those properties sit at the epicentre of one of the most significant valuation shifts the country's prime market has seen in decades. The valuation impacts of 2026 Budget on prime Scottish properties, specifically the surveyor adjustments required for homes above the £2M threshold, demand a methodologically distinct response from RICS-accredited professionals working north of the border. This article examines what those adjustments look like in practice, how Scotland's approach diverges from England's, and what property owners and advisors should do before April 2028.

Key Takeaways

- Scotland's 2026 Budget introduces two new council tax bands — Band I (£1M–£2M) and Band J (above £2M) — effective from 1 April 2028.

- A £5 million government budget has been allocated for targeted revaluation of affected properties, moving away from 1991 valuations.

- Surveyors must now incorporate tax-liability adjustments into comparable evidence analysis for properties above the £2M threshold.

- Scotland's band-based model differs structurally from England's surcharge approach, requiring jurisdiction-specific valuation methodology.

- Affected owners have a window until 2028 to commission accurate, RICS-compliant valuations and plan accordingly.

Understanding the New Council Tax Bands and Their Valuation Trigger

The Scottish Budget 2026–2027, published by the Scottish Government in January 2026, confirmed two entirely new council tax bands for high-value residential properties [5]. Band I will apply to properties valued between £1 million and £2 million; Band J will capture all properties valued above £2 million. Both bands take effect from 1 April 2028, giving a defined implementation window of roughly two years [1].

The structural significance of this change cannot be overstated. Scotland's current council tax system is still anchored to 1991 capital values — a baseline that has never been comprehensively updated in the intervening 35 years. The new bands require current market valuations, not historical estimates. To fund this revaluation exercise, the Scottish Government has allocated £5 million specifically for targeted assessments of the affected stock [1].

Why Current Valuations Are Now Non-Negotiable

Under the old system, a property worth £2.5 million in today's market might have been banded using a 1991 valuation that bore little relation to its present worth. The new framework eliminates that ambiguity for the top tier of the market. Assessors will need to establish whether a property sits above or below the £1M and £2M thresholds using contemporary evidence.

This creates an immediate professional obligation for surveyors. Any valuation report prepared for a property in the £900,000 to £3 million range should now explicitly address the council tax band risk, particularly where the assessed value might straddle a threshold. For context on what a thorough valuation process involves, the RICS Help to Buy Valuation guide offers a useful framework for understanding how RICS-compliant assessments are structured.

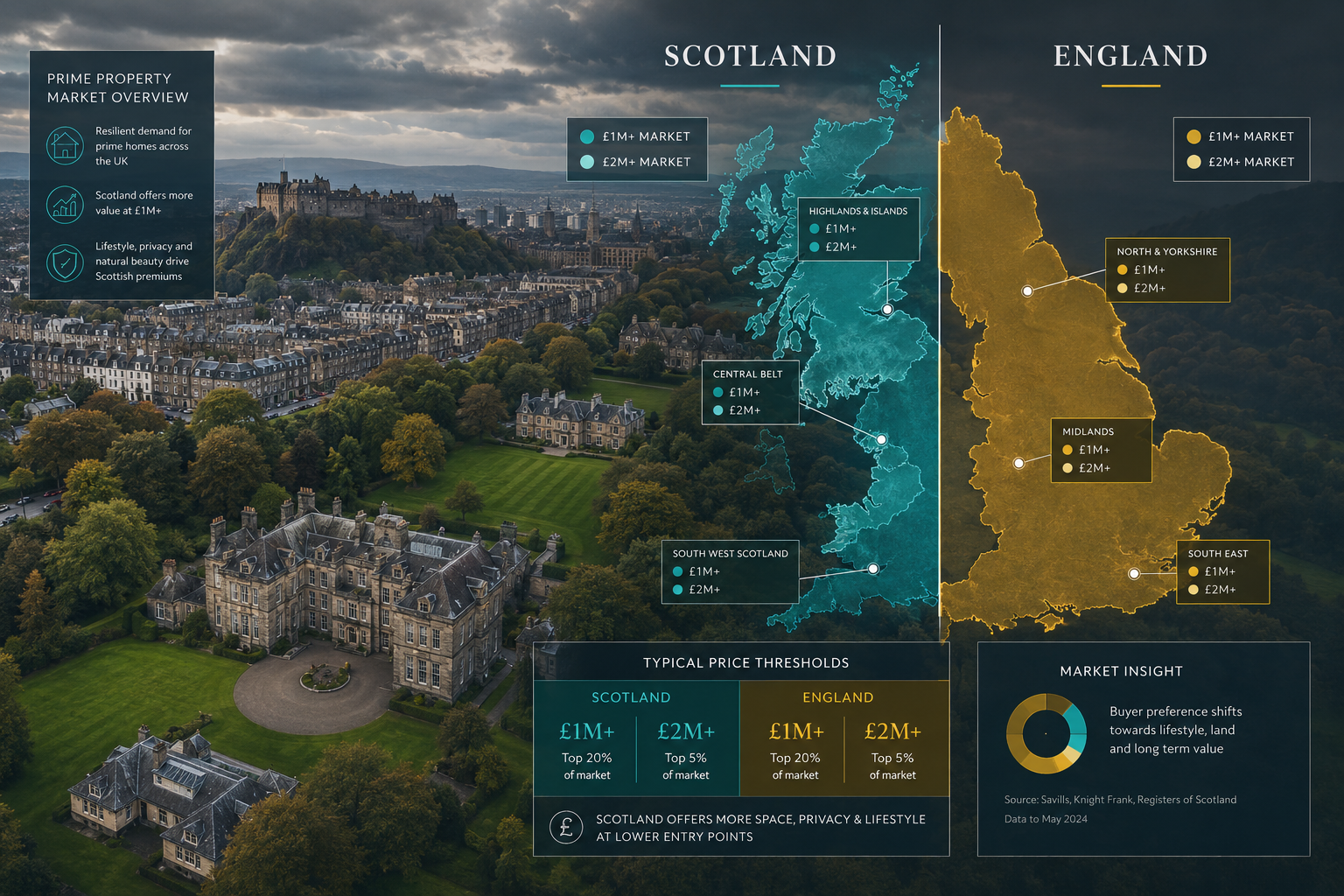

How Scotland's Approach Differs From England's Mansion Tax Model

A critical point of distinction for surveyors advising clients on cross-border portfolios is that Scotland and England have taken fundamentally different legislative routes to taxing high-value property [1].

The UK Government's November 2025 Budget introduced a council tax surcharge on properties in England valued above £2 million, effective from 2028. This is a flat additional charge layered onto an existing band, not a new band in its own right.

Scotland, by contrast, has created two entirely new bands within the council tax hierarchy. This is not merely a semantic difference — it has direct implications for how surveyors model tax-adjusted valuations.

| Feature | Scotland (2026 Budget) | England (2025 Budget) |

|---|---|---|

| Mechanism | New bands (Band I and Band J) | Surcharge on existing top band |

| Lower threshold | £1,000,000 | £2,000,000 |

| Upper threshold | No cap stated for Band J | No cap |

| Valuation basis | Current market value | Current market value |

| Effective date | 1 April 2028 | 2028 |

| Revenue estimate | £12M–£16M annually | Not directly comparable |

Source: Scottish Parliament Research Briefing [1]; Scottish Government Budget Document [5]

Because Scotland's model introduces a graduated structure with an intermediate band, surveyors must model two potential tax-step effects rather than one. A property valued at £1.8 million faces Band I liability; the same property, if evidence supports a valuation above £2 million, faces Band J. The difference in annual council tax liability between those two outcomes could be material, depending on the multiplier each local council sets.

Valuation Impacts of 2026 Budget on Prime Scottish Properties: Surveyor Adjustments Over £2M Threshold in Practice

The valuation impacts of 2026 Budget on prime Scottish properties require surveyors to revisit several core elements of their methodology. The following adjustments are now considered best practice for assessments above or approaching the £2M threshold.

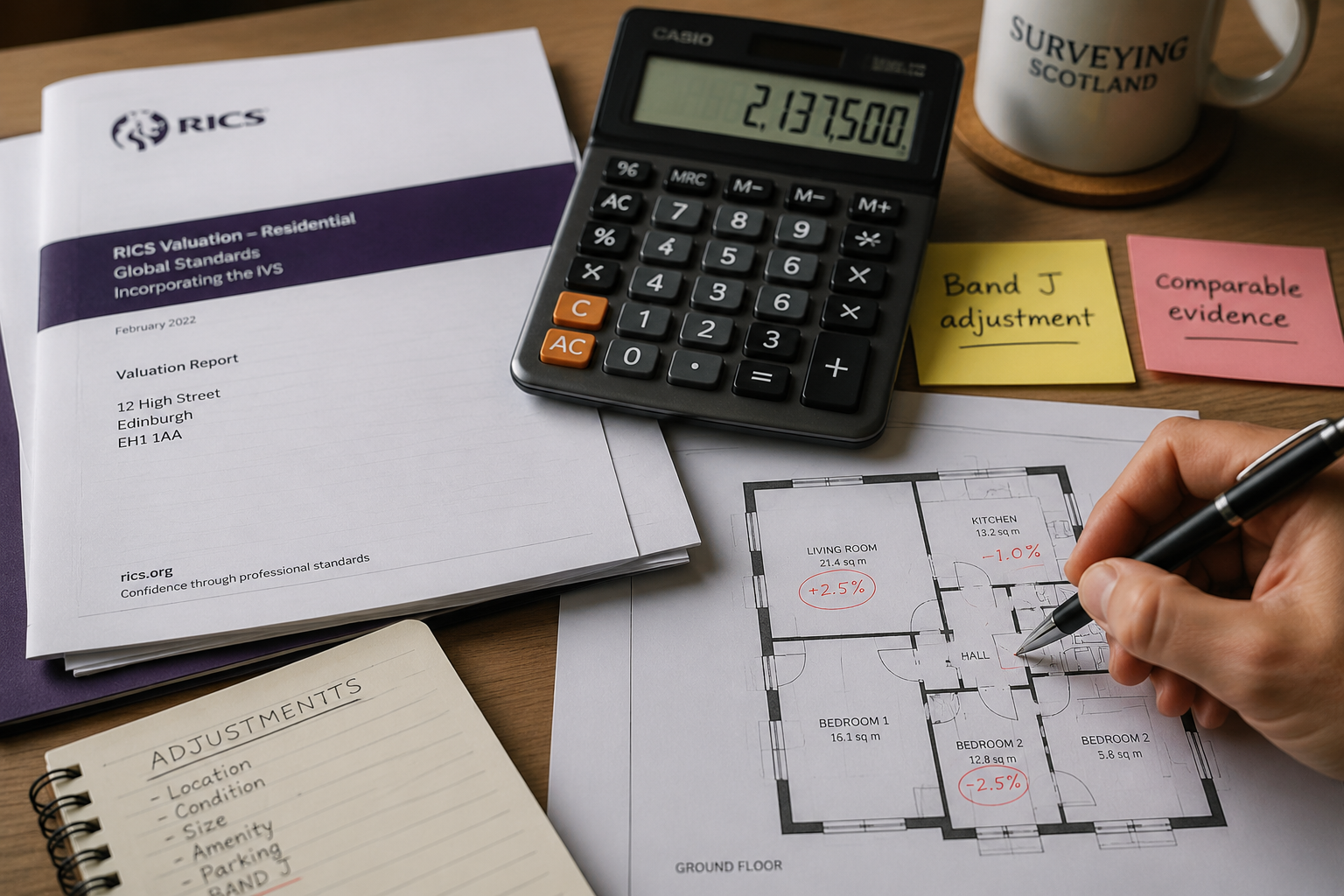

1. Tax-Adjusted Comparable Evidence

Traditional comparable analysis selects recent transactions of similar properties and adjusts for differences in size, condition, location, and specification. Post-budget, surveyors must add a further adjustment layer: tax liability at the point of sale.

If a comparable transaction completed before the 2026 Budget announcement, the buyer did not price in Band J liability. A surveyor using that transaction as evidence today must apply a downward adjustment to reflect the additional annual cost a new buyer would now factor in. Industry guidance suggests this adjustment should be calculated by capitalising the expected annual tax increment at an appropriate yield, then deducting that figure from the gross comparable value [3].

2. Threshold Sensitivity Analysis

For properties where the valuation sits within approximately 10% of either the £1M or £2M boundary, surveyors are advised to prepare a sensitivity analysis that presents values under two scenarios: above and below the threshold. This gives clients and lenders a transparent view of the tax risk embedded in the valuation [4].

This approach aligns with RICS Red Book guidance on the disclosure of material uncertainty, which requires valuers to flag conditions that could cause a reasonable variation in the reported figure.

3. Adjusting the Capitalisation Rate for Prime Scottish Stock

Prime Scottish properties — particularly Edinburgh New Town townhouses, Perthshire country estates, and high-specification Highland retreats — often trade on relatively thin yields compared to comparable English stock. The introduction of Band J creates an additional holding cost that rational buyers will price into their offers.

Surveyors should review their capitalisation rates for properties above £2M and consider whether a modest upward adjustment (reflecting increased holding costs) is warranted. This will typically translate into a modest downward pressure on capital values, the quantum of which will vary by property type and buyer profile [3] [4].

4. Regional Market Volatility Considerations

Not all Scottish regions will feel this change equally. Edinburgh's prime residential market, the Perthshire estate market, and select coastal and rural markets in Argyll and Sutherland contain the highest concentrations of properties above the £1M threshold. Surveyors operating in these areas should monitor transaction volumes closely through 2026 and 2027 for early signs of buyer hesitation or pricing adjustments [4].

For those seeking a deeper understanding of what a comprehensive survey report covers in high-value contexts, the Level 3 Building Survey guide explains the depth of inspection that RICS Level 3 assessments provide — relevant for prime properties where structural and condition factors interact with valuation.

Revenue Projections and What They Signal About Affected Property Numbers

The Scottish Government's own estimates project that the new bands will raise between £12 million and £16 million annually [1]. Cross-referencing this against typical council tax multipliers, the implied number of affected properties is small but concentrated.

Fewer than 1% of Scotland's approximately 2.7 million dwellings are expected to fall into Band I or Band J [2]. That equates to roughly 27,000 properties at the outer limit — though the number above £2M is considerably smaller. The targeted £5 million revaluation budget reinforces this: it is designed for a defined, manageable cohort of high-value homes, not a wholesale rebanding exercise.

"The new bands represent a structural shift in how Scotland taxes wealth held in residential property — and that shift has direct consequences for how surveyors must evidence and report value at the top of the market."

For property owners who hold high-value Scottish assets within an estate, it is worth noting that the revaluation exercise may also affect probate valuations where properties straddle the new thresholds. Accurate, RICS-compliant probate figures will be essential to avoid disputes with revenue authorities.

Valuation Impacts of 2026 Budget on Prime Scottish Properties: Surveyor Adjustments Over £2M Threshold — RICS Standards and Professional Obligations

RICS members operating in Scotland are bound by the RICS Valuation — Global Standards (Red Book Global) and its UK national supplement. The 2026 Budget changes create several specific professional obligations worth noting.

Material Uncertainty and Disclosure

Where the tax environment creates genuine uncertainty about market depth or pricing at the £2M+ level, RICS guidance requires surveyors to consider whether a material uncertainty clause should be included in the valuation report. This is not an admission of professional failure; it is a transparent acknowledgement that external market conditions — including pending legislative changes — create a range of possible outcomes.

Instruction Scope and Assumptions

Surveyors should review their standard instructions for prime Scottish properties to ensure the scope explicitly addresses the council tax band implications. Special assumptions may be needed where a property is currently banded under the 1991 system but will clearly fall into Band I or Band J under the updated valuations.

Lender Requirements

Mortgage lenders with exposure to Scottish prime property are beginning to request explicit commentary on Band I and Band J risk in valuation reports. Surveyors should anticipate this requirement and address it proactively, even where it is not yet a formal panel requirement.

For those newer to the professional landscape of property surveys, a useful primer on what a property surveyor does and their professional responsibilities provides helpful context on the scope of a surveyor's role.

Practical Steps for Property Owners Above the £2M Threshold

Owners of Scottish properties approaching or exceeding £2 million have a defined window before April 2028 to act. The following steps are recommended:

- Commission a current market valuation from a RICS-accredited surveyor with demonstrable experience in the Scottish prime market. Avoid relying on automated valuation models, which are not calibrated for the new tax environment.

- Understand your threshold position — if your property is close to £1M or £2M, a sensitivity analysis is essential. A difference of £50,000 in assessed value could mean a materially different annual tax bill.

- Review your insurance reinstatement figure — council tax band changes do not directly affect rebuild costs, but a revaluation exercise is a logical moment to also review insurance reinstatement valuations to ensure adequate coverage.

- Engage a tax advisor alongside your surveyor. The council tax implications interact with other holding costs and should be modelled as part of a broader financial review.

- Monitor local council multiplier decisions — the actual annual increase in council tax will depend on the multiplier each Scottish local authority sets for Band I and Band J. These have not yet been confirmed and will vary by region.

For buyers currently in the process of acquiring a high-value Scottish property, a Level 3 Building Survey provides the most comprehensive structural and condition assessment available, and should be considered standard practice at this price point.

Conclusion

The valuation impacts of 2026 Budget on prime Scottish properties are real, measurable, and require a methodologically rigorous response from RICS-accredited surveyors. The introduction of Band I and Band J council tax bands — effective from 1 April 2028 — marks Scotland's first substantive departure from 1991 valuations for high-value residential property. With a £5 million revaluation programme underway and revenue projections of up to £16 million annually, the policy is well-funded and clearly signalled.

Surveyors adjusting for properties above the £2M threshold must now integrate tax-adjusted comparable evidence, threshold sensitivity analysis, and updated capitalisation rates into their standard methodology. Scotland's band-based model is structurally distinct from England's surcharge approach, and cross-border comparisons must be applied with care.

Actionable next steps:

- If you own or advise on a Scottish property valued between £900,000 and £3 million, commission a current RICS-compliant valuation before 2027 to establish your threshold position.

- Ensure your surveyor explicitly addresses Band I and Band J risk in their report, including any material uncertainty disclosure.

- Review insurance reinstatement and probate valuations in parallel with any council tax revaluation exercise.

- Monitor Scottish local authority announcements on Band I and Band J multipliers as they are confirmed ahead of 2028.

The window is open. Property owners and their advisors who act early will be best placed to navigate the tax and valuation landscape that takes effect in 2028.

References

[1] The Commitment To Ensure Most Scottish Taxpayers Pay Less Income Tax Than They Would In The Rest Of – https://www.parliament.scot/chamber-and-committees/research-prepared-for-parliament/research-briefings/2026/1/16/sb-2604/taxation/income-tax/the-commitment-to-ensure-most-scottish-taxpayers-pay-less-income-tax-than-they-would-in-the-rest-of

[2] Scottish Budget 2026 2027 – https://www.stanleywright.co.uk/scottish-budget-2026-2027/

[3] Valuation Impacts Of 2026 Budgets 2 Million Property Taxes Surveyor Strategies For High End Market Adjustments – https://wimbledonsurveyors.com/valuation-impacts-of-2026-budgets-2-million-property-taxes-surveyor-strategies-for-high-end-market-adjustments/

[4] Valuation Adjustments For High Value Properties Over 2m Navigating 2026 Budget Tax Changes And Market Stability – https://princesurveyors.co.uk/blog/valuation-adjustments-for-high-value-properties-over-2m-navigating-2026-budget-tax-changes-and-market-stability/

[5] Scottish Budget 2026 2027 – https://www.gov.scot/binaries/content/documents/govscot/publications/corporate-report/2026/01/scottish-budget-2026-2027/documents/scottish-budget-2026-2027/scottish-budget-2026-2027/govscot%3Adocument/scottish-budget-2026-2027.pdf

[6] Post Budget 2026 Valuation Challenges Surveyor Strategies For High Value Properties Over 2 Million – https://nottinghillsurveyors.com/blog/post-budget-2026-valuation-challenges-surveyor-strategies-for-high-value-properties-over-2-million