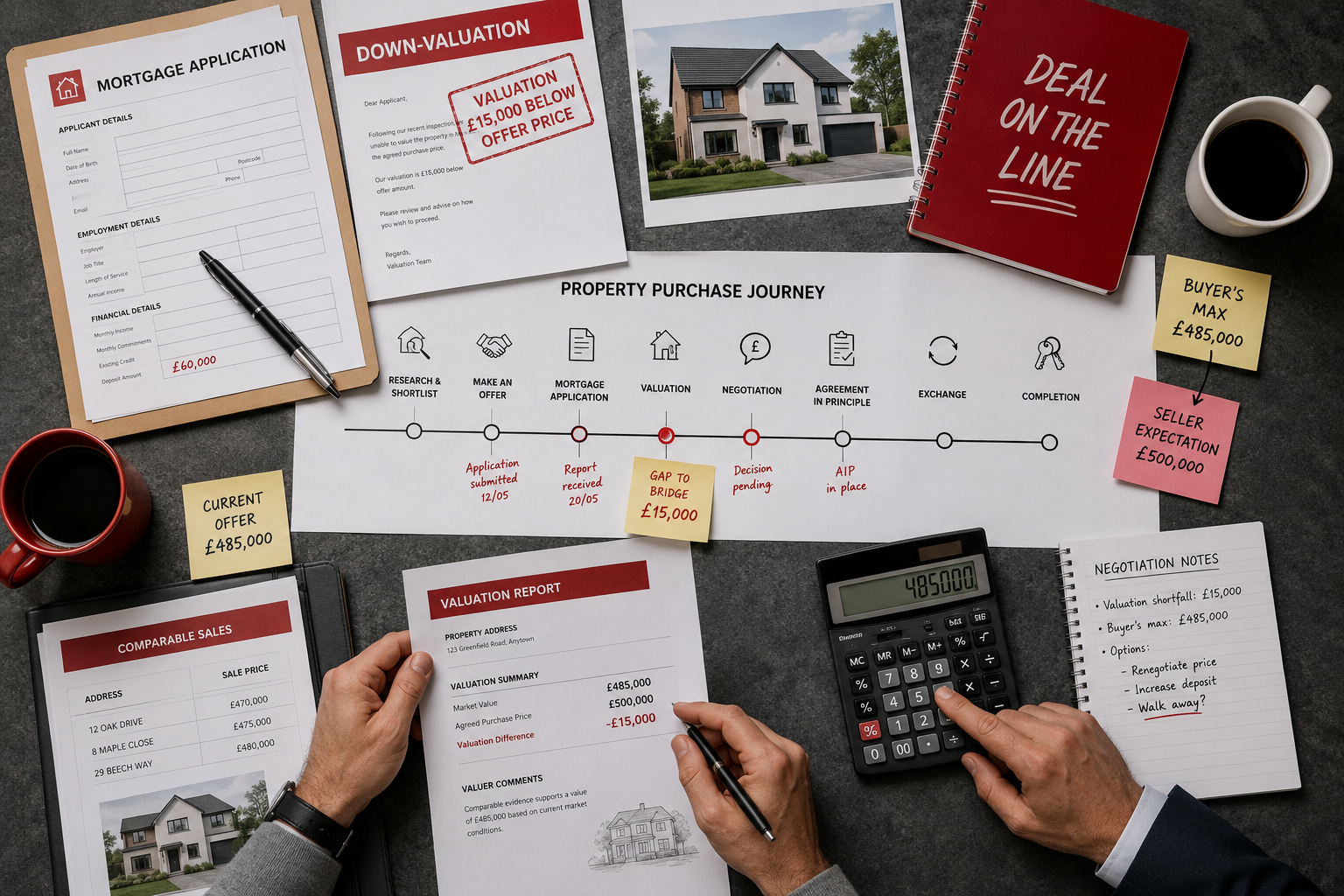

Nearly 400,000 UK homes were down-valued in a single year, with the average reduction sitting at £7,500 per transaction — enough to collapse a purchase, trigger a renegotiation, or expose a surveyor to a formal complaint [1]. For valuation surveyors, that figure is not an abstract statistic. It represents hundreds of thousands of moments where professional opinion collides with commercial expectation, emotional investment, and, increasingly, regulatory scrutiny.

This article addresses the challenge of Valuation Surveyors and Mortgage Down-Valuations: How to Evidence and Defend Opinions When Transactions are Under Pressure from the practitioner's perspective. It explains how to build a defensible valuation file, manage challenges from borrowers and estate agents, satisfy lender compliance requirements, and withstand the ultimate test — court or tribunal examination.

Key Takeaways

- Down-valuations are common and legally defensible when supported by robust, documented comparable evidence aligned with RICS standards.

- The most frequent causes of down-valuations include overpricing, limited comparable data, poor property condition, and lagging market evidence.

- Surveyors must document their reasoning clearly enough to satisfy lenders, regulators, and potential court scrutiny.

- Formal reconsideration-of-value processes exist and must be handled systematically, not reactively.

- Energy performance ratings and automated valuation model outputs are increasingly relevant factors in valuation disputes.

Why Down-Valuations Happen and Why They Are Contested

Understanding the root causes of a down-valuation is the first step toward defending one. The most common triggers fall into four broad categories.

1. Overambitious agreed prices

Estate agents are incentivised to achieve the highest possible sale price. When a buyer and seller agree a figure that exceeds what the market evidence supports, the mortgage valuation will reflect the evidence — not the enthusiasm [2]. This is not a surveyor error; it is the system working correctly.

2. Thin or lagging comparable evidence

In rapidly rising markets, recent transaction data often lags behind current asking prices. Registered sale prices — the gold standard for comparable evidence — can be three to six months behind the market at the point of inspection [7]. Surveyors must acknowledge this lag explicitly in their reports rather than silently adjusting upward without justification.

3. Property condition and defects

Properties requiring significant structural repair, modernisation, or with non-standard construction are routinely valued below agreed prices [2]. A buyer may factor in their own renovation plans; a lender's valuation must reflect the property as it stands on the day of inspection, not as it might look after works are completed.

4. Automated Valuation Model (AVM) conflicts

Some lenders use AVMs for lower loan-to-value applications. These models cannot assess condition, local micro-market nuances, or subjective factors such as aspect, noise, or layout [3]. When an AVM figure conflicts with a surveyor's opinion, the surveyor's documented reasoning becomes the critical differentiator.

"A valuation is not a negotiation. It is a professional opinion formed on evidence, and the surveyor's duty runs to the lender — not to the transaction."

Understanding these causes matters because each one requires a different evidential response. A surveyor defending a condition-related down-valuation needs photographic evidence and condition notes. One defending a comparable-data gap needs a transparent explanation of the evidence hierarchy used and why available comparables were weighted as they were.

Building a Defensible Evidence File: The Core of Valuation Surveyors and Mortgage Down-Valuations

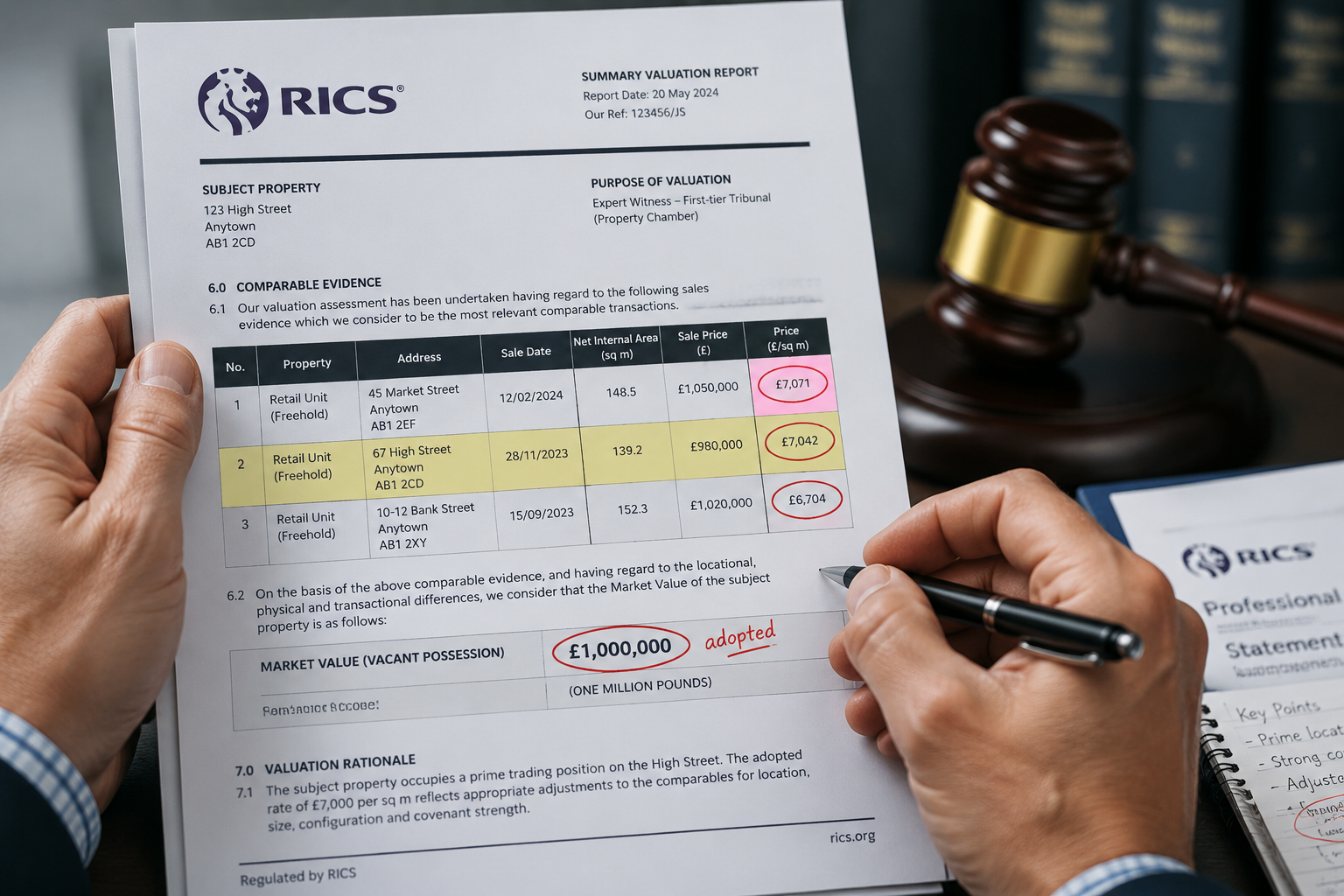

The single most important protection a surveyor has when a down-valuation is challenged is a well-constructed, contemporaneous evidence file. RICS surveyors are required to base valuations on comparable evidence and prevailing market conditions, maintaining accuracy and objectivity throughout [4]. That obligation is not satisfied by selecting three comparables and recording a figure — it requires a documented analytical process.

Selecting and Weighting Comparable Evidence

A robust comparable analysis should include:

| Factor | Best Practice |

|---|---|

| Number of comparables | Minimum three; ideally five or more |

| Recency | Prefer sales within the last six months; note any older evidence and explain its use |

| Proximity | Within the same street, block, or immediate neighbourhood first |

| Property similarity | Match tenure, size (GIA/GEA), condition, and specification as closely as possible |

| Source | Land Registry, EPC register, agent confirmation, auction results |

Each comparable should be individually analysed, not simply listed. The surveyor should note adjustments made for differences in size, condition, floor level, or tenure, and explain the weighting applied. If a comparable is excluded, the reason should be recorded.

Documenting Market Conditions

Where market evidence is thin or the agreed price reflects a rising market, surveyors should include a brief but explicit market commentary. This might reference:

- Local price trend data from recognised indices

- Time-adjusted analysis where older comparables are used

- Commentary on supply/demand conditions in the specific sub-market

- Any known factors affecting local values (regeneration, infrastructure, planning decisions)

This documentation protects the surveyor if the market subsequently moves and a complainant argues the valuation was too conservative.

Condition and Repair Evidence

For properties where condition is a material factor, the file should include:

- Dated photographs of all defects referenced in the valuation

- Notes on the estimated cost or impact of repairs, referenced to recognised cost data

- Any specialist reports obtained or recommended

- A clear narrative linking the condition findings to the valuation figure

This is particularly relevant for shared ownership valuations and Help to Buy valuations, where lender requirements and scheme rules add an additional layer of scrutiny to the evidence base.

Energy Performance and EPC Ratings

Under current RICS Red Book standards, surveyors must consider EPC ratings as a valuation factor [3]. Properties with poor energy ratings — particularly those facing mandatory upgrade requirements — may attract a measurable discount in certain markets. This consideration should be explicitly noted in the valuation narrative, with reference to the current EPC rating and any known legislative requirements affecting the property type.

Handling Challenges: Borrowers, Agents, and the Reconsideration Process

When a down-valuation is issued, the surveyor will almost inevitably face a challenge. Understanding the formal and informal dimensions of that challenge is essential for both professional protection and practical resolution.

The Informal Challenge: Agent and Borrower Pressure

Estate agents and borrowers frequently contact surveyors directly after a down-valuation. The approach is often to present additional comparables, argue that the surveyor "missed" recent sales, or suggest that the valuation will kill the deal. Surveyors should respond to these approaches professionally and systematically.

Key principles for managing informal challenges:

- Acknowledge receipt of any additional evidence promptly and in writing

- Assess new comparables against the same criteria applied to the original analysis

- Do not revise a valuation simply because of commercial pressure — only revise if new evidence genuinely supports a different opinion

- Document all communications, including verbal discussions where possible

- Maintain the distinction between the lender client and the borrower/agent

The surveyor's duty of care runs primarily to the lender. Borrowers may have a secondary claim in certain circumstances, but the valuation must not be influenced by the borrower's desire to complete the transaction [4].

The Formal Reconsideration of Value

Most lenders operate a formal reconsideration of value (ROV) process. Regulatory guidance — including principles articulated by financial regulators — emphasises that ROV procedures must be based on credible evidence, not commercial pressure, and must follow documented procedures for addressing deficiencies in the original valuation [6].

A well-managed ROV response should:

- Acknowledge the request formally and record the date received

- Review each piece of new evidence submitted against defined criteria

- Prepare a written response addressing each point raised

- Either maintain the original opinion with reasons, or revise it with a clear explanation of what new evidence changed the analysis

- Retain the full correspondence and analysis in the valuation file

Buyers and borrowers have the right to request a reconsideration if they believe a valuation is inaccurate, and surveyors should treat this process as an opportunity to demonstrate professional rigour rather than a threat [5]. For those seeking broader context on what different survey types cover, the guide to understanding home surveys provides useful background on the distinctions between mortgage valuations and more detailed inspection reports.

When Agents Submit Their Own Comparables

Agents frequently submit comparable evidence in support of a challenge. Surveyors should apply the same analytical framework to agent-supplied comparables as to their own research. Common issues with agent-supplied evidence include:

- Properties under offer rather than completed sales

- Comparables from different sub-markets presented as equivalent

- Asking prices rather than achieved prices

- Properties with materially different specifications or conditions

Each of these issues should be addressed explicitly in the ROV response. If the agent's comparables are valid and genuinely support a higher figure, the surveyor should say so and revise accordingly. Professional credibility depends on consistency of method, not consistency of outcome.

Satisfying Lenders, Regulators, and Court Scrutiny

The ultimate test of a valuation opinion is whether it can withstand examination by a lender's compliance team, a professional standards body, or — in the most serious cases — a court or tribunal. Valuation Surveyors and Mortgage Down-Valuations: How to Evidence and Defend Opinions When Transactions are Under Pressure is ultimately a question of whether the surveyor's reasoning is transparent, reproducible, and grounded in evidence.

Lender Compliance Requirements

Lenders increasingly require surveyors on their panels to meet specific documentation standards. These typically include:

- A minimum number of comparable transactions with source references

- Explicit commentary on market conditions

- Condition ratings aligned with lender-specific scales

- Clear identification of any special assumptions or departures from standard methodology

Surveyors should familiarise themselves with the specific panel requirements of each lender they work for, as these requirements vary and non-compliance can result in panel removal regardless of the quality of the underlying valuation.

RICS Professional Standards

RICS Red Book Global Standards set the framework for all residential mortgage valuations. Key obligations include:

- Valuation must be based on Market Value as defined in the Red Book

- The basis of value, inspection scope, and any limitations must be disclosed

- Comparable evidence must be identified and its application explained

- The valuer must be competent for the property type and location

Surveyors facing a complaint to RICS should be able to demonstrate that their valuation file meets these standards. The RICS dispute resolution service and the Financial Ombudsman Service both examine valuation complaints, and a well-documented file is the primary defence in both forums.

Expert Witness and Court Scrutiny

In litigation — whether a professional negligence claim by a lender or a dispute between buyer and seller — the surveyor may be required to act as an expert witness or to have their valuation examined by one. The expert witness services framework requires that expert evidence be independent, objective, and based on the facts known at the date of valuation.

Courts apply a "bracket of reasonableness" test to valuation disputes. A valuation that falls within the range that a competent surveyor could reasonably have reached on the available evidence will generally be defensible, even if it differs from the ultimate market outcome. The critical question is whether the surveyor's method was sound and their evidence base adequate — not whether the figure turned out to be correct in hindsight.

The Role of Valuation Factors Documentation

Maintaining a clear record of all valuation factors considered — location, condition, tenure, comparable evidence, market conditions, and special features — is not merely good practice. It is the foundation of any defensible position. Surveyors who can produce a contemporaneous, structured record of their reasoning are significantly better placed in any dispute than those relying on memory or reconstructed notes.

For complex or high-value transactions, some surveyors commission additional specialist input — drainage surveys, structural assessments, or environmental reports — before finalising their opinion. Resources such as drainage survey guidance and structural engineering assessments can provide the technical underpinning that strengthens a valuation opinion where condition is a significant factor.

Practical Steps When a Transaction Is Under Pressure

When a down-valuation threatens to collapse a transaction, surveyors face simultaneous pressure from multiple directions. The following framework helps manage that pressure without compromising professional standards.

Step 1: Secure the file immediately

Before responding to any challenge, ensure the valuation file is complete, dated, and locked. Add nothing retrospectively without clearly dating and labelling it as a post-valuation addition.

Step 2: Identify the nature of the challenge

Is the challenge based on new evidence, a procedural complaint, or simply commercial pressure? The response to each is different. New evidence requires analysis. A procedural complaint requires a compliance review. Commercial pressure requires a polite but firm restatement of professional obligations.

Step 3: Engage the lender's compliance team early

If a challenge is escalating, notify the lender's panel management or compliance team proactively. Lenders generally prefer early notification over being surprised by a formal complaint.

Step 4: Respond in writing to all substantive challenges

Every substantive point raised in a challenge should receive a written response. Oral assurances are not sufficient and create no record.

Step 5: Consider whether a desktop review or re-inspection is warranted

If significant new evidence has been submitted or material facts about the property were not available at the time of inspection, a formal desktop review or re-inspection may be appropriate. This should be conducted under the same standards as the original valuation and documented accordingly.

For surveyors working across the London market, regional knowledge is a significant factor in comparable selection. Practitioners based in areas such as West London or South East London will be familiar with the micro-market variations that can make a material difference to comparable weighting — and that local expertise, properly documented, is itself a defence against challenge.

Conclusion

Valuation Surveyors and Mortgage Down-Valuations: How to Evidence and Defend Opinions When Transactions are Under Pressure is one of the most practically demanding challenges in residential surveying practice. The professional and legal stakes are real: complaints to RICS, lender panel removal, and professional negligence claims are all possible consequences of a poorly documented or indefensible valuation.

The good news is that the framework for protection is clear. Build a comprehensive, contemporaneous evidence file. Apply a consistent, documented methodology to comparable selection and weighting. Engage with formal reconsideration processes systematically rather than reactively. Communicate clearly with lenders, and maintain the distinction between professional duty and commercial pressure.

Actionable next steps for practising surveyors:

- Review your current valuation file template against RICS Red Book requirements and lender panel standards — identify any documentation gaps.

- Establish a written protocol for handling ROV requests, including response timelines and escalation triggers.

- Ensure all condition-related down-valuations include dated photographic evidence and a clear narrative linking findings to the valuation figure.

- Familiarise yourself with EPC and energy performance requirements under current RICS standards, and incorporate these into standard report commentary.

- Where complex property types or high-value transactions are involved, consider whether specialist input — structural, environmental, or legal — is warranted before finalising your opinion.

A down-valuation that is properly evidenced and professionally defended is not a liability. It is a demonstration of exactly the rigour that the profession, lenders, and ultimately the public depend upon.

References

[1] What To Do If A Property Is Down Valued – https://england.landlordsguild.com/article/what-to-do-if-a-property-is-down-valued/?utm_source=openai

[2] Why Was My Property Downvalued – https://realsurveying.co.uk/why-was-my-property-downvalued/?utm_source=openai

[3] Home Down Valuation Advice – https://www.ayrshiremortgages.com/mortgages/mortgage-advice/home-down-valuation-advice/?utm_source=openai

[4] Down Valuation Fact Or Fiction – https://ww3.rics.org/uk/en/journals/property-journal/-down-valuation—fact-or-fiction-.html?utm_source=openai

[5] What Happens If I Disagree With A Valuation – https://www.reallymoving.com/surveyors/guides/what-happens-if-i-disagree-with-a-valuation?utm_source=openai

[6] Interagency Guidance On Reconsiderations Of Value Of Residential Real Estate Valuations – https://www.federalreserve.gov/frrs/guidance/interagency-guidance-on-reconsiderations-of-value-of-residential-real-estate-valuations.htm?utm_source=openai

[7] Mortgage Down Valuation – https://www.whathouse.com/mortgages-and-homes/mortgage-down-valuation/?utm_source=openai

[8] What To Do If A Home Valuation Is Lower Than The Offer – https://www.zoopla.co.uk/discover/selling/what-to-do-if-a-home-valuation-is-lower-than-the-offer/?utm_source=openai

[9] Down Valuations – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/down-valuations/?utm_source=openai