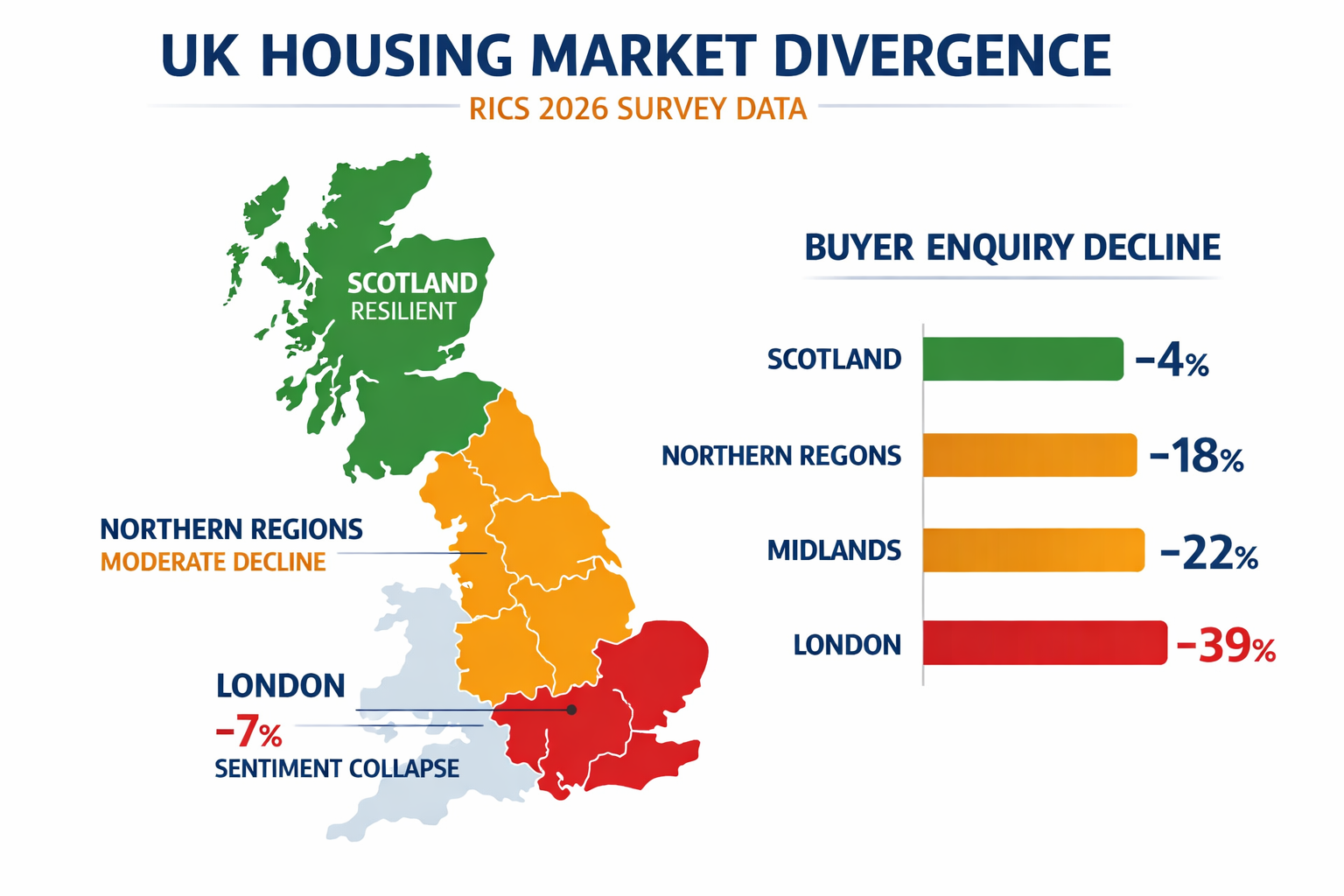

London buyer sentiment has collapsed to just +7% according to RICS February 2026 data — a figure that should stop every building surveyor in their tracks. Nationally, buyer enquiries have fallen by -26%, and the regional divergence between markets is now so pronounced that a single national risk framework is no longer fit for purpose. Building Survey Risk Assessment in Spring 2026's Cautious Market: Adjusting for -26% Buyer Enquiry Decline and Regional Price Divergence is no longer a theoretical concern — it is the operational reality facing every surveyor, buyer, and lender this season [2].

The market has not crashed. But it has changed its psychology. Buyers are hesitant, sellers are stubborn, and the gap between asking price and achievable price is widening in ways that make defect prioritisation and risk communication more consequential than ever.

Key Takeaways 📋

- Buyer enquiries have dropped -26% nationally in spring 2026, creating a more cautious transaction environment where survey findings carry greater weight in negotiations.

- Regional price divergence is now the dominant risk factor, with London sentiment at +7% while some northern and Scottish markets show relative resilience [2].

- Level 3 Building Surveys are increasingly essential in volatile markets, providing the depth of defect analysis needed to protect buyers and inform renegotiations [4].

- Interest rate volatility and material cost pressures are compounding structural risk assessments, requiring surveyors to adjust their frameworks beyond physical condition alone [3].

- Defect prioritisation and risk communication must be recalibrated for cautious buyer psychology — findings that might have been noted as "monitor" in 2024 may now be deal-breakers in 2026.

Understanding the Spring 2026 Market Landscape

The spring 2026 housing market is defined by caution, not collapse. The RICS February 2026 survey identified regional divergence in price trends as the most operationally significant finding for property professionals, requiring localised valuation adjustments rather than uniform national approaches [2]. This is not a uniform downturn — it is a fractured market where postcode-level analysis has become essential.

What the -26% Buyer Enquiry Decline Actually Means

A -26% drop in buyer enquiries does not mean one-in-four transactions has disappeared. It means the pool of motivated, financially committed buyers has thinned considerably. Those who remain in the market are:

- 🔍 More forensic in their due diligence

- 💬 More likely to use survey findings as negotiation leverage

- ⏳ Less willing to proceed past significant defects without price reductions

- 🏦 Subject to tighter lending conditions linked to interest rate volatility [3]

For building surveyors, this shift in buyer psychology changes the stakes of every report. A category 3 defect (requiring urgent attention) in a 2023 market might have been absorbed into the transaction. In spring 2026, the same defect may cause a buyer to withdraw entirely — or demand a reduction that the seller refuses, killing the deal.

"In a cautious market, the building survey is no longer just a health check — it is the primary risk management document for the entire transaction."

The Macro Pressures Behind the Numbers

The demand weakness is not isolated to the UK. The 2026 U.S. Homebuilder Executive Outlook Survey reveals a market navigating demand uncertainty with caution rather than exuberance, with developers reassessing risk exposure across the board [1]. In Canada, pre-construction condominium sales in Toronto fell to multi-decade lows in 2025, with condominium starts projected to remain particularly weak through 2026 [3]. Developers are focusing on completing projects already underway rather than starting new ones — a signal of reduced confidence that echoes across international markets [3].

Closer to home, interest rate volatility and potential tariffs on building materials are adding cost pressures that constrain project viability and require surveyors to adjust their risk frameworks beyond simple physical condition assessments [3]. An older roof that would cost £8,000 to replace in 2023 may now cost £12,000+ due to material inflation — a figure that changes its risk classification entirely.

For buyers seeking a Level 3 Building Survey, these macro factors must now be integrated into how defects are costed and communicated.

How Regional Price Divergence Reshapes Building Survey Risk Assessment in Spring 2026's Cautious Market

Regional divergence is the defining characteristic of spring 2026 property risk. The RICS February 2026 data makes clear that a London buyer and a buyer in the East Midlands are operating in fundamentally different risk environments — and their building surveys should reflect that [2].

A Regional Risk Breakdown

| Region | Market Sentiment | Price Trend | Survey Risk Priority |

|---|---|---|---|

| London | +7% (very weak) | Flat to declining | Highest — defects carry maximum negotiation weight |

| South East | Moderate weakness | Slight softening | High — buyer caution elevated |

| North West | Relative resilience | Modest growth | Medium — standard risk framework applies |

| Scotland | Positive | Stable to rising | Lower — but structural risks unchanged |

| East Midlands | Mixed | Flat | Medium-high — oversupply in some segments |

This divergence means that a chartered surveyor operating across multiple regions cannot apply a single risk communication template. The same damp issue in a London flat carries different transactional consequences than the same issue in a Manchester terrace — not because the defect is different, but because the buyer's alternatives and negotiating position are different.

Localised Valuation Adjustments Are Now Non-Negotiable

The RICS February 2026 survey is explicit: regional divergence in price trends requires localised valuation adjustments rather than uniform national approaches [2]. For building surveyors, this translates into several practical changes:

1. Comparable Evidence Must Be Hyper-Local

Using national averages for repair cost estimates or residual value calculations is no longer defensible. Surveyors must source local contractor quotes and local transaction data.

2. Risk Ratings Must Reflect Market Liquidity

In low-liquidity markets (like London at +7% sentiment), a category 2 defect (defects requiring repair or replacement but not urgent) should be communicated with greater emphasis on the cost and timeline implications, because the buyer has fewer alternative properties and lenders are more cautious.

3. Resale Market Context Must Be Included

The 2026 resale market will show signs of recovery but remain below long-term averages [3]. Surveyors should note where a property's condition places it relative to local market expectations — a below-average condition property in a flat market faces compounded risk.

For properties in Central London, Surrey, or South East London, the combination of weak sentiment and high property values makes comprehensive survey coverage essential — the financial stakes of missing a significant defect are simply too high.

Adjusting Defect Prioritisation and Risk Communication for Cautious Buyer Psychology

Building Survey Risk Assessment in Spring 2026's Cautious Market: Adjusting for -26% Buyer Enquiry Decline and Regional Price Divergence ultimately comes down to one practical question: how should surveyors change what they write, and how they say it?

Rethinking the Three-Tier Defect Framework

The standard RICS three-category condition rating system (1 = no repair needed, 2 = repair/replacement needed, 3 = urgent action required) remains valid. But the narrative context around each rating must evolve for spring 2026 conditions.

Category 3 Defects in a -26% Enquiry Market:

These are now potential transaction killers. Surveyors should:

- Provide specific cost range estimates, not just descriptions

- Note whether the defect is likely to affect mortgage lending

- Flag whether the issue is common to the property type/age (contextualising risk)

- Consider whether a structural engineer report or specialist investigation is warranted before exchange

Category 2 Defects — The New Battleground:

In a buoyant market, category 2 defects are often accepted and budgeted for. In spring 2026, they are increasingly used as negotiation tools. Surveyors should:

- Be precise about repair timelines (immediate vs. within 3 years vs. within 10 years)

- Note the consequence of non-repair (e.g., damp penetration leading to structural damage)

- Avoid vague language like "monitor" without specifying what monitoring involves

The Elevated Importance of Level 3 Surveys

Comprehensive Level 3 Building Surveys are becoming particularly valuable in volatile spring 2026 markets, providing the most thorough assessment of physical condition to mitigate valuation risk [4]. Unlike a Level 2 Homebuyer Survey, a Level 3 survey:

- ✅ Inspects roof spaces, sub-floor voids, and all accessible areas

- ✅ Provides detailed descriptions of construction and materials

- ✅ Includes specific repair recommendations and cost guidance

- ✅ Assesses the implications of defects on value and insurability

For buyers considering older, larger, or non-standard properties — exactly the type most common in London and the South East — the Level 2 vs Level 3 survey comparison almost always resolves in favour of the more comprehensive option in the current market.

Subsidence, Roofs, and High-Risk Defect Categories in 2026

Two defect categories deserve special attention in spring 2026 risk assessments:

Subsidence: With ground movement risks increasing due to climate-related soil shrinkage, subsidence surveys are more frequently warranted as a follow-up to building survey findings. In a weak market, undisclosed subsidence risk is a significant liability for both buyer and surveyor.

Roof Condition: Material cost inflation means that a roof requiring replacement is now a substantially larger financial risk than in previous years. Roof surveys as specialist follow-ups should be recommended more readily when there is any ambiguity about remaining life expectancy.

Communicating Risk to Cautious Buyers: Practical Language Guidance

The tone and structure of survey reports must match the psychological state of spring 2026 buyers. Key principles:

| Old Approach | Spring 2026 Approach |

|---|---|

| "Monitor the damp" | "Damp at X location requires investigation within 6 months; untreated, it risks timber decay" |

| "Typical for age" | "Typical for age, but note: repair costs in current market are 30-40% higher than 2022 estimates" |

| "Seek specialist advice" | "Recommend specialist structural engineer report before exchange; lender may require this" |

| "Negotiate on price" | "Based on current market conditions in [region], this defect supports a price reduction of £X-£Y" |

Practical Framework: Adjusting Survey Risk Assessments for Spring 2026

A Five-Point Adjustment Protocol

Given the market conditions described above, the following five-point protocol is recommended for building surveyors operating in spring 2026:

-

Regional Context Statement — Include a brief market context paragraph at the start of every report, noting local sentiment, price trend, and buyer demand conditions. This frames all subsequent risk ratings appropriately.

-

Cost-Adjusted Defect Ratings — All repair cost estimates should reflect 2026 material and labour costs, not historical benchmarks. Flag where costs have increased significantly.

-

Mortgage Risk Flags — Explicitly note which defects are likely to trigger lender conditions or retention of funds. In a tight lending environment, this is critical information for buyers.

-

Negotiation Guidance Section — Consider adding a brief section summarising the key findings most likely to support price renegotiation, with realistic ranges based on local comparable data.

-

Follow-Up Survey Recommendations — Be specific about which specialist surveys are recommended and why. In a cautious market, buyers appreciate clear guidance rather than open-ended suggestions.

Commercial Property Considerations

The risk adjustment principles above apply equally to commercial transactions. Commercial building surveys in spring 2026 face additional pressures from weakened occupier demand and rising vacancy rates in some sectors. Surveyors undertaking RICS commercial building surveys should pay particular attention to:

- Deferred maintenance that sellers may have accumulated during low-activity periods

- Mechanical and electrical systems that may be at end of useful life

- Compliance issues that have become more stringent since 2022

Conclusion: Actionable Next Steps for Spring 2026 🏠

The -26% decline in buyer enquiries and the sharp regional price divergence of spring 2026 are not temporary noise — they represent a structural shift in how property risk must be assessed and communicated. Building Survey Risk Assessment in Spring 2026's Cautious Market: Adjusting for -26% Buyer Enquiry Decline and Regional Price Divergence demands that surveyors, buyers, and their advisors move beyond standardised templates and embrace a more contextualised, market-aware approach.

Actionable next steps:

- 🔎 Buyers: Commission a Level 3 Building Survey for any property that is older than 20 years, non-standard in construction, or located in a high-value/low-sentiment market like London.

- 📍 Buyers in regional markets: Ensure your surveyor has genuine local expertise — the compare survey types tool can help identify the right level of inspection for your property.

- 🏗️ Surveyors: Update cost benchmarks, integrate regional market context into reports, and sharpen defect communication language to reflect cautious buyer psychology.

- 🏢 Commercial buyers: Prioritise comprehensive pre-acquisition surveys given weakened market liquidity and elevated deferred maintenance risk.

- 📊 All parties: Treat the building survey as the primary risk management document in spring 2026 transactions — not a formality, but a genuine decision-making tool.

The market will recover. But the buyers, surveyors, and advisors who navigate spring 2026 successfully will be those who took the cautious signals seriously and adjusted their approach accordingly.

References

[1] Survey Reveals Demand Uncertainty Is Changing 2026 Homebuilding Strategy – https://www.housingwire.com/articles/survey-reveals-demand-uncertainty-is-changing-2026-homebuilding-strategy/

[2] Valuation Adjustments For Cautious Spring 2026 Housing Market Rics February Insights On Buyer Demand Dips And Regional Price Flatness – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-cautious-spring-2026-housing-market-rics-february-insights-on-buyer-demand-dips-and-regional-price-flatness

[3] Housing Market Outlook – https://www.cmhc-schl.gc.ca/professionals/housing-markets-data-and-research/market-reports/housing-market/housing-market-outlook

[4] Macroeconomic Uncertainty And Spring 2026 Valuations How Building Surveyors Adjust For Interest Rate Volatility And Geopolitical Risk – https://nottinghillsurveyors.com/blog/macroeconomic-uncertainty-and-spring-2026-valuations-how-building-surveyors-adjust-for-interest-rate-volatility-and-geopolitical-risk