The UK residential property market has entered a critical phase as buyer enquiries plummeted to -26% net balance in February 2026, marking the sharpest monthly deterioration since late 2025 and shattering the brief optimism that characterized the early weeks of the year. This dramatic reversal presents unprecedented valuation challenges in weak buyer demand, forcing chartered surveyors to recalibrate their methodologies amid mounting uncertainty. The RICS February 2026 Survey reveals a market gripped by geopolitical tensions, persistent inflation concerns, and regional divergence so pronounced that London properties face -40% net balance while Scotland maintains relative stability—creating a complex landscape where traditional valuation approaches require immediate adaptation[2][3].

Understanding the Valuation Challenges in Weak Buyer Demand: RICS February 2026 Survey Analysis and Surveyor Strategies has become essential for professionals navigating this turbulent environment. The data paints a sobering picture: agreed sales remain subdued at -12% net balance, near-term price expectations have turned negative at -18%, and market confidence sits precariously on what RICS describes as "fragile" foundations[2]. For surveyors, these conditions demand not just technical precision but strategic insight into how weak demand fundamentally alters valuation principles.

Key Takeaways

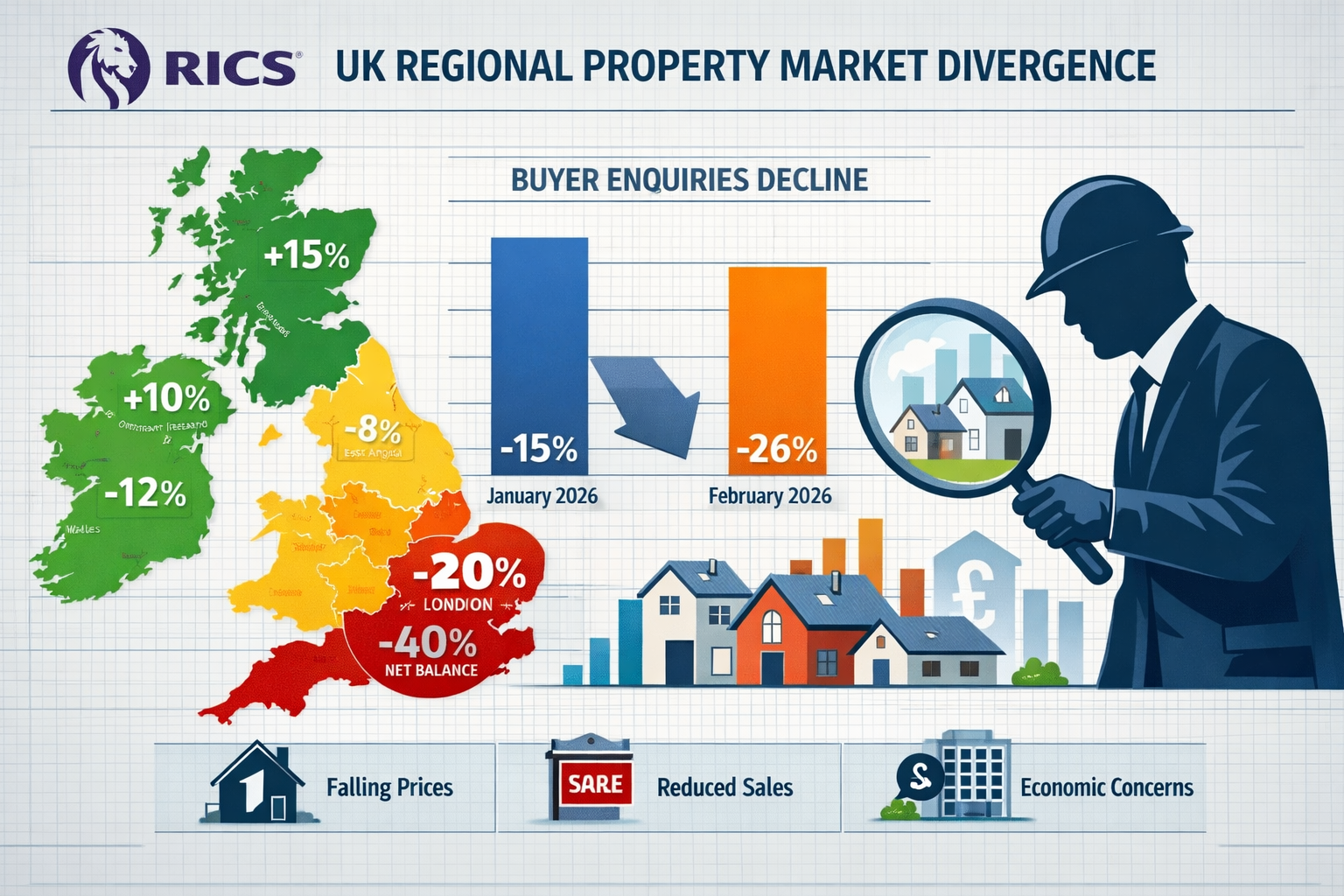

- 🔻 Buyer enquiries collapsed to -26% net balance in February 2026, down from -15% in January, creating significant valuation uncertainty across UK markets

- 🗺️ Regional divergence intensified dramatically, with London experiencing -40% net balance while Scotland and Northern Ireland maintain positive trends, requiring location-specific valuation strategies

- 📊 Near-term price expectations turned negative at -18%, the weakest since November 2025, while 12-month outlook remains cautiously positive at +33% nationally

- 🏠 Supply conditions remain stable at +2% net balance, but weak demand creates downward price pressure requiring surveyors to adjust comparable selection and weighting

- 💼 Surveyor strategies must incorporate geopolitical risk factors, mortgage rate uncertainty, and enhanced market evidence analysis to maintain valuation accuracy

Understanding the February 2026 Market Deterioration

The RICS February 2026 Survey documents a market reversal that caught many industry observers off-guard. After modest improvements in December 2025 and January 2026, the residential sector experienced what can only be described as a confidence shock. The -26% net balance for buyer enquiries represents an 11-percentage-point decline in just one month—a velocity of change that complicates valuation work considerably[2].

The Numbers Behind the Decline

The survey data reveals multiple pressure points affecting valuation accuracy:

| Metric | February 2026 | January 2026 | Change |

|---|---|---|---|

| Buyer Enquiries | -26% | -15% | ▼ 11 points |

| Agreed Sales | -12% | -10% | ▼ 2 points |

| Near-term Sales Expectations | -2% | +5% | ▼ 7 points |

| Near-term Price Expectations | -18% | -6% | ▼ 12 points |

| National House Prices | -12% | -11% | ▼ 1 point |

These figures demonstrate that the valuation challenges in weak buyer demand extend beyond simple price adjustments. The entire transaction ecosystem has weakened simultaneously, creating compounding effects on property values[2][3].

Geopolitical and Economic Drivers

RICS respondents consistently cited geopolitical escalation in the Middle East and rising oil prices as primary drivers of renewed uncertainty. These external shocks have reignited inflation concerns and reinforced expectations that mortgage rates will remain elevated for longer than previously anticipated[2]. For surveyors conducting RICS home surveys, this macroeconomic backdrop must now factor into valuation judgments, particularly when assessing future marketability.

The fragility of market confidence means that valuations completed in January 2026 may already require reconsideration if used for mortgage purposes in March or April. This temporal sensitivity represents a significant challenge for both surveyors and their clients.

Regional Divergence: The London Challenge and Beyond

Perhaps the most striking aspect of the RICS February 2026 Survey Analysis is the extreme regional divergence in market conditions. This geographic variation creates distinct valuation challenges that require surveyors to adopt location-specific strategies rather than applying national trends uniformly.

London's Steep Decline

London recorded a -40% net balance for house prices, representing the steepest downward pressure of any UK region[2]. This 40-percentage-point negative reading reflects multiple compounding factors:

- Affordability constraints reaching critical levels in the capital

- Stamp duty burdens disproportionately affecting London transactions

- Economic uncertainty impacting high-value property confidence

- International buyer withdrawal amid geopolitical tensions

For surveyors working in London, these conditions demand careful consideration when selecting comparable evidence. Properties that sold in November or December 2025 may no longer provide reliable guidance for February 2026 valuations. Understanding what surveyors do in these conditions extends beyond technical measurement to sophisticated market interpretation.

The South East and East Anglia Struggle

The South East recorded -24% net balance while East Anglia showed -26%, indicating that London's challenges have spread to surrounding commuter regions[2]. This geographic contagion effect creates valuation complications for properties positioned as "London alternatives"—their value proposition weakens when the capital itself faces sustained pressure.

Relative Stability in Scotland and Northern Ireland

In stark contrast, Scotland and Northern Ireland continue reporting firmer price trends, providing surveyors in these regions with more stable valuation environments[2]. This divergence means that national-level data provides limited guidance for local valuation decisions—a reality that underscores the importance of regional market expertise.

When conducting a Level 2 house survey in Edinburgh versus one in East London, surveyors must apply fundamentally different market context assumptions despite working within the same national regulatory framework.

Valuation Challenges in Weak Buyer Demand: Technical Considerations

The valuation challenges in weak buyer demand identified in the RICS February 2026 Survey require surveyors to revisit fundamental valuation principles and adapt methodologies to reflect market realities. Weak demand doesn't simply mean lower prices—it creates structural challenges in establishing reliable market value.

Comparable Evidence Selection

In a market characterized by -26% buyer enquiry levels, the volume and quality of comparable transactions diminishes significantly. Surveyors face several technical challenges:

Time Adjustments: With near-term price expectations at -18%, the temporal relevance of comparable evidence decays rapidly. A transaction from December 2025 may require meaningful downward adjustment when valuing a similar property in February 2026[2].

Transaction Volume: Agreed sales at -12% net balance means fewer transactions to analyze[2]. Surveyors must cast wider geographic nets or extend lookback periods, both of which introduce additional uncertainty.

Motivation Analysis: In weak demand environments, understanding seller motivation becomes critical. Distressed sales, estate disposals, or motivated relocations may not represent true market value, yet they constitute an increasing proportion of available evidence.

Market Value vs. Mortgage Lending Value

The RICS Red Book defines market value as "the estimated amount for which an asset should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction after proper marketing." When buyer enquiries fall to -26%, the concept of "proper marketing" becomes problematic—properties may require extended marketing periods or price reductions to attract the diminished buyer pool[2].

For surveyors providing RICS registered valuations for mortgage purposes, this creates tension between market value (what a property might achieve with extended marketing) and mortgage lending value (a more cautious assessment reflecting current liquidity constraints).

The Supply-Demand Imbalance

Interestingly, the February 2026 survey shows new instructions at +2% net balance, indicating supply remains relatively stable despite weak demand[2]. This imbalance typically exerts downward price pressure, but the magnitude varies by property type, location, and price bracket.

Surveyors must assess whether:

- Current supply levels are sustainable or represent pent-up selling pressure

- The property being valued faces above-average or below-average competition

- Supply characteristics (property type, condition, location) match or mismatch current demand patterns

Surveyor Strategies for Maintaining Valuation Accuracy

Given the valuation challenges in weak buyer demand documented in the RICS February 2026 Survey, chartered surveyors must employ enhanced strategies to maintain accuracy and defend their professional judgments. The following approaches represent best practices emerging from current market conditions.

Enhanced Market Research Protocols

Daily Market Monitoring: In rapidly changing conditions, weekly or monthly market reviews prove insufficient. Surveyors should establish daily monitoring of:

- New listing volumes and pricing strategies

- Price reduction frequency and magnitude

- Days-on-market trends for comparable properties

- Mortgage rate movements and availability

Agent Intelligence Networks: Cultivating relationships with multiple estate agents provides qualitative insights that supplement quantitative data. Agents can identify buyer hesitation patterns, negotiation dynamics, and emerging price resistance levels that haven't yet appeared in transaction data.

Regional Specialization: The extreme divergence between London (-40%) and Scotland (positive trends) demonstrates that national expertise no longer suffices[2]. Surveyors should focus on deep regional specialization, understanding local economic drivers, employment patterns, and demographic trends.

Valuation Methodology Adaptations

Increased Weighting on Recent Evidence: Traditional approaches might weight comparable evidence equally within a six-month window. Current conditions demand exponential weighting favoring the most recent transactions, potentially limiting reliance on evidence older than 60-90 days.

Explicit Uncertainty Disclosure: RICS guidance permits surveyors to include uncertainty clauses when market conditions warrant. With near-term price expectations at -18%, valuations should explicitly acknowledge the elevated uncertainty environment and potential for near-term value changes[2].

Scenario Analysis: Rather than single-point valuations, consider providing range estimates or scenario-based valuations that reflect different market trajectory assumptions. This approach provides clients with more realistic expectations while protecting the surveyor's professional position.

Client Communication Excellence

When conducting homebuyers surveys, clear communication about market conditions becomes as important as the technical valuation itself:

Market Context Education: Clients need to understand that the -26% buyer enquiry figure doesn't mean prices have fallen 26%, but rather indicates the demand-supply dynamic that influences value[2]. Providing this context prevents misunderstandings and manages expectations.

Timeline Sensitivity: Explain that valuations have shorter shelf-lives in volatile markets. A valuation completed in February may require updating if the transaction doesn't proceed promptly.

Regional Variation Clarity: Clients relocating between regions need explicit guidance on how London's -40% differs from Scotland's positive trends[2]. This prevents inappropriate cross-regional comparisons.

The Rental Market Context and Alternative Valuation Approaches

The RICS February 2026 Survey also provides insight into rental market dynamics, which offer alternative valuation perspectives during periods of weak buyer demand. Understanding the rental sector helps surveyors assess properties through investment lenses when owner-occupier demand falters.

Rental Market Resilience

The survey shows tenant demand at +2% net balance, indicating relative stability compared to the sales market's -26% buyer enquiries[2]. However, landlord instructions fell sharply to -27%, creating supply constraints that support rental values.

Rental Growth Expectations: With +20% of surveyors expecting rents to rise over the next three months, the rental market provides a counterpoint to sales market weakness[2]. For surveyors valuing investment properties or conducting commercial valuations, this rental strength supports income-based valuation approaches.

Investment Valuation Approaches

When buyer demand weakens substantially, investment valuation methodologies gain relevance even for properties traditionally valued on an owner-occupier basis:

Yield Compression Analysis: If rental values remain stable or grow while capital values face pressure, gross and net yields increase. Surveyors should calculate current yields and compare them to historical norms and alternative investment returns.

Income Capitalization: For properties with established rental income, capitalization approaches may provide more stable value indicators than comparable sales methods during demand shocks.

Development Potential: In weak markets, properties with planning permission potential or conversion opportunities may hold value better than standard residential stock.

Future Outlook: 12-Month Expectations vs. Near-Term Reality

The RICS February 2026 Survey Analysis reveals a fascinating dichotomy between near-term pessimism and longer-term cautious optimism—a tension that creates both challenges and opportunities for surveyors.

The Expectations Gap

Near-term price expectations: -18% net balance (indicating expected decline)

12-month price expectations: +33% net balance (indicating expected growth)[2]

This 51-percentage-point gap between three-month and twelve-month expectations suggests surveyors anticipate a difficult spring followed by recovery. However, London's 12-month outlook cooled dramatically to just +7%, down from +56% previously, indicating diminished confidence in the capital's recovery trajectory[2].

Strategic Implications for Valuations

This expectations gap creates valuation dilemmas:

Short-Term Transactions: Properties requiring quick sales face the full force of current weak demand and should be valued accordingly, potentially incorporating forced-sale considerations.

Patient Sellers: Properties where sellers can wait for market improvement might justify valuations that reflect 12-month expectations rather than immediate conditions—though this requires careful justification and explicit disclosure.

Development Projects: Properties requiring building surveys for development purposes should be valued with particular attention to delivery timelines. Projects completing in Q4 2026 face different market conditions than those finishing in Q2 2026.

The First-Time Buyer Factor

Tim Green FRICS noted that the first-time buyer segment represents the likely recovery driver, with increased property listings providing early positive signs, though "Spring has not quite arrived yet"[2]. For surveyors, this suggests:

- Entry-level properties may stabilize before higher price brackets

- Locations with strong first-time buyer demographics may outperform

- Properties requiring significant renovation may face extended weakness as first-time buyers typically have limited capital

Understanding what does a party wall surveyor do becomes relevant here, as first-time buyers often purchase terraced or semi-detached properties where party wall considerations affect value.

Risk Management and Professional Standards

The valuation challenges in weak buyer demand documented in the RICS February 2026 Survey elevate professional risk for surveyors. Maintaining compliance with RICS standards while adapting to volatile conditions requires careful risk management.

RICS Red Book Compliance

The RICS Valuation – Global Standards (Red Book) provides the framework for professional valuation practice. In current market conditions, several provisions gain particular importance:

VPS 3 (Valuation Reports): Requires clear identification of the purpose of valuation and any special assumptions. In weak demand environments, surveyors should explicitly state assumptions about marketing periods, buyer motivation, and market conditions.

VPGA 10 (Matters that may Give Rise to Material Valuation Uncertainty): The February 2026 market conditions may warrant inclusion of material valuation uncertainty clauses, particularly for properties in severely affected regions like London.

Professional Indemnity Insurance: Surveyors should review their PII coverage to ensure adequate protection given elevated market volatility and potential for valuation challenges.

Documentation and Defensibility

Enhanced documentation becomes critical when valuations may be questioned months or years later:

Market Evidence Files: Maintain comprehensive records of all comparable evidence considered, including properties ultimately rejected and the reasoning for exclusion.

Methodology Justification: Document why particular approaches were selected and others rejected, especially when departing from standard practices.

Assumption Registers: Create explicit registers of all assumptions underlying the valuation, with particular attention to market condition assumptions.

When conducting Level 3 building surveys, this documentation discipline extends to physical condition assessments that may affect value in weak markets.

Conclusion

The Valuation Challenges in Weak Buyer Demand: RICS February 2026 Survey Analysis and Surveyor Strategies reveals a UK residential property market at a critical juncture. The sharp deterioration in buyer enquiries to -26% net balance, combined with extreme regional divergence and near-term price expectations turning negative at -18%, creates an environment where traditional valuation approaches require significant adaptation[2][3].

For chartered surveyors, these conditions demand enhanced professional capabilities across multiple dimensions: deeper market research, more sophisticated comparable analysis, explicit uncertainty acknowledgment, and superior client communication. The geographic variation—from London's -40% to Scotland's relative stability—means that regional expertise has never been more valuable[2].

Actionable Next Steps for Surveyors

✅ Implement daily market monitoring protocols to track rapid changes in demand, supply, and pricing dynamics in your operating regions

✅ Review and update comparable evidence databases monthly, applying appropriate temporal adjustments to reflect the -18% near-term price expectations[2]

✅ Enhance client communication frameworks to explain market context, regional variations, and valuation uncertainty explicitly

✅ Develop regional specialization rather than attempting to maintain national coverage, given the extreme divergence between markets

✅ Review professional indemnity insurance coverage and documentation practices to ensure adequate protection in volatile conditions

✅ Consider investment valuation approaches as supplements to traditional comparable methods, particularly for properties with rental income potential

✅ Establish agent intelligence networks to access qualitative market insights that supplement quantitative data

The February 2026 survey suggests that while near-term conditions remain challenging, the 12-month outlook maintains cautious optimism at +33% nationally[2]. Surveyors who successfully navigate the current weak demand environment while maintaining professional standards will be well-positioned to capitalize on the eventual recovery. The key lies in recognizing that these valuation challenges require not just technical precision but strategic market insight and adaptive methodologies.

For property professionals seeking expert guidance through these challenging conditions, partnering with experienced chartered surveyors who understand regional market dynamics and maintain rigorous professional standards remains the most effective strategy for accurate valuations and informed property decisions.

References

[1] Valuation Impacts Of February 2026 Rics Survey Strategies For Regional Price Divergence In Uk Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets

[2] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[3] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] housingtoday.co.uk – https://www.housingtoday.co.uk/news/uk-housing-market-to-stagnate-in-year-ahead-as-middle-east-conflict-raises-borrowing-costs-says-rics/5141678.article