Buyer demand in the UK residential market collapsed to a net balance of -26% in February 2026 — yet rental demand held firm at +10%, and near-term rental growth expectations sat at a striking +29% [7]. That divergence is not a coincidence. It is the defining feature of a lettings market shaped by geopolitical stress, constrained supply, and rising funding costs — and it demands a sharper, more disciplined approach to valuing rental properties in geopolitical uncertainty: RICS February 2026 survey tactics for cautious lettings markets are now essential reading for every practising valuer.

This article unpacks what the February 2026 RICS data actually means for rental valuations, how surveyors are adapting their methods, and what landlords and investors need to understand about yield assumptions, void periods, and scenario modelling in the current environment.

Key Takeaways 📌

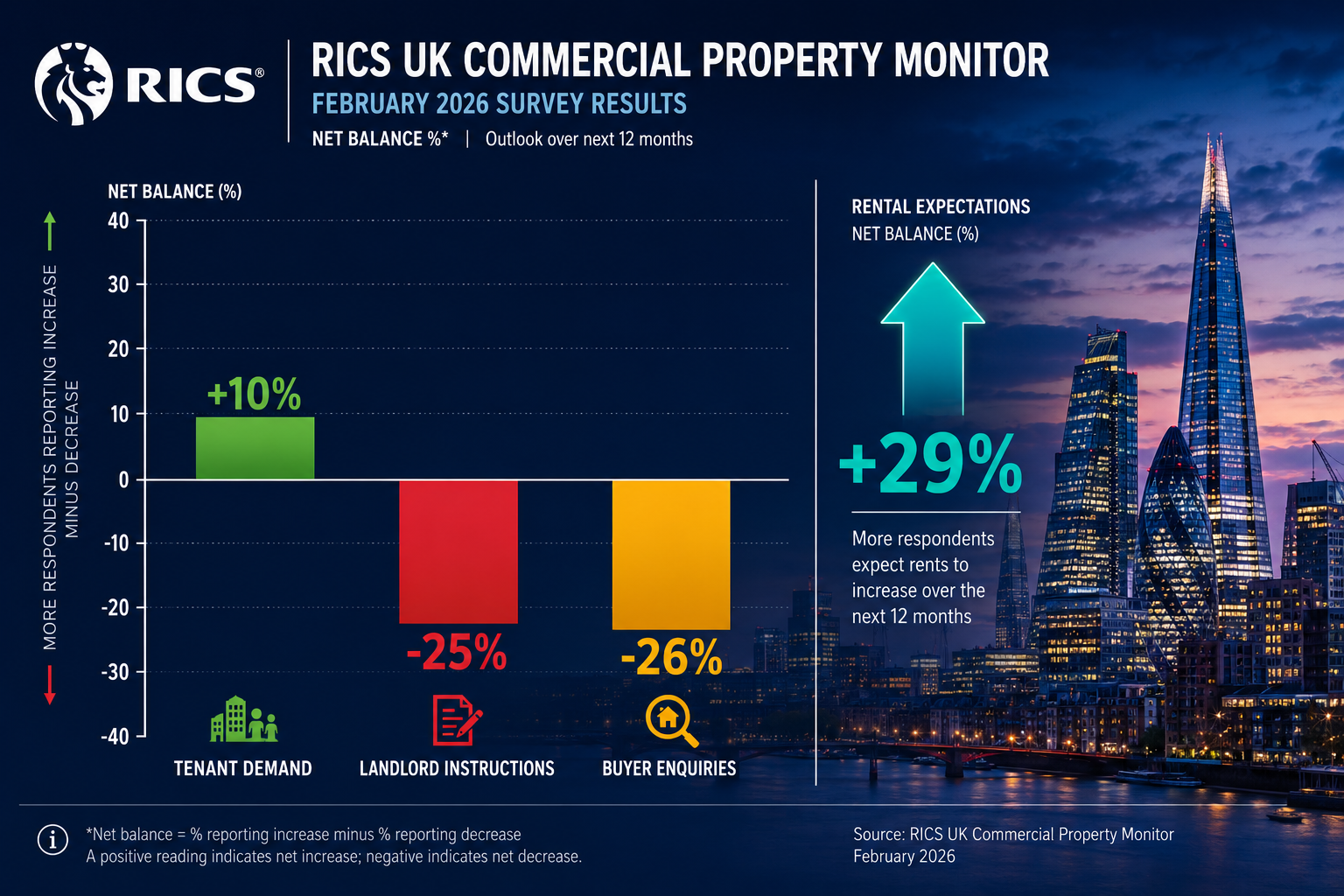

- Rental demand remains resilient (+10% net balance) even as sales activity weakens sharply, creating a supply–demand imbalance that supports rental income streams [7].

- Landlord instructions are deeply negative (-25%), meaning constrained supply underpins continued rental growth expectations of +29% in the near term [7].

- Scenario-based cash-flow modelling — testing base, stress, and upside cases — is now the recommended valuation approach in geopolitically volatile conditions [6].

- Regional divergence is critical: London and the South East face downward price pressure, while the North West, Scotland, and Northern Ireland show firmer conditions, affecting yield assumptions [1].

- Policy and regulatory risks (rent controls, landlord taxation) must be explicitly flagged in valuation reports alongside geopolitical discount assumptions [5].

Understanding the February 2026 RICS Data: What It Means for Rental Valuations

The RICS UK Residential Market Survey for February 2026 paints a bifurcated picture. On the sales side, conditions deteriorated markedly — buyer enquiries fell to a net balance of around -26%, and agreed sales followed a similar downward trajectory [7]. RICS Chief Economist Simon Rubinsohn explicitly linked this softening to a deteriorating geopolitical backdrop, noting that near-term expectations had become cautious even if 12-month sales forecasts for 2027 remained modestly positive [8].

The lettings side, however, tells a different story entirely.

The Supply–Demand Imbalance Driving Rental Values

| Indicator | Net Balance (Feb 2026) |

|---|---|

| Tenant demand | +10% |

| New landlord instructions | -25% |

| Near-term rental growth expectations | +29% |

| Buyer enquiries (sales) | -26% |

Source: RICS UK Residential Market Survey, February 2026 [7]

This imbalance — robust demand meeting severely constrained supply — is the single most important structural factor for anyone valuing rental properties in 2026. When landlord listings remain deeply negative and tenant enquiries stay positive, rental income streams are relatively insulated from the sentiment shocks that are hammering sales values [3].

💬 "Rental comparables and real-time enquiry data are more reliable anchors for valuation than volatile capital values, especially when geopolitical risks are driving sentiment swings rather than local fundamentals." — Wimbledon Surveyors [3]

For valuers, this creates both an opportunity and a responsibility. The opportunity: income-producing rental assets may be undervalued if assessed using capital-value metrics that are currently depressed by macro uncertainty. The responsibility: avoiding the trap of capitalising rent at aggressively low yields simply because demand looks strong, given that interest-rate volatility and geopolitical shocks can rapidly alter the financing environment [6].

Why Geopolitical Uncertainty Matters to Lettings Valuations

Geopolitical events affect rental valuations through several transmission channels:

- 🌍 Energy costs: Escalating conflicts (particularly in the Middle East) push up household energy bills, affecting tenant affordability and, indirectly, achievable rents.

- 💷 Mortgage rates: Following Iran-related escalation in early 2026, average 2-year fixed mortgage rates rose from approximately 4.83% to 5.90% — the highest level since mid-2024 — pushing some would-be buyers back into renting and increasing demand [2].

- 📉 Investor sentiment: Higher funding costs reduce net yields for leveraged landlords, compressing what buyers will pay for income-producing assets even when the income itself is stable.

- 🏛️ Policy responses: Governments responding to cost-of-living pressures linked to geopolitical shocks are more likely to debate rent controls or additional landlord taxation [5].

Understanding these channels is the starting point for any robust rental valuation methodology in the current environment. For further context on how RICS valuations are structured to account for market conditions, it is worth reviewing how formal Red Book standards require explicit commentary on market uncertainty.

Core Valuation Tactics: Applying RICS February 2026 Survey Data in Practice

Valuing rental properties in geopolitical uncertainty — using RICS February 2026 survey tactics for cautious lettings markets — requires moving beyond simple comparables. The following tactics represent the current best-practice consensus among leading valuation firms [3][4][5][6].

Tactic 1: Prioritise Rental Comparables Over Capital Value Sentiment

When sales sentiment is distorted by macro fear, capital values become a noisy signal for rental valuers. The February 2026 data reinforces this: price balances in London and the South East ranged from -24% to -40%, yet rental demand in many of these same areas remained positive [1][3].

Practical steps:

- Build a comparables database using actual achieved rents (not asking rents) from the past 3–6 months.

- Cross-reference against local void data and re-letting times — both of which have shortened in many mainstream markets due to constrained supply [4].

- Discount any comparable that pre-dates the current geopolitical stress period (broadly, post-Q4 2025) unless adjusted for market movement.

For those undertaking a formal rent review, this comparables-first approach is especially important: headline house-price indices will not reflect the rental market's relative resilience.

Tactic 2: Scenario-Based Cash-Flow Modelling

Single-point forecasts are inadequate in the current environment. Notting Hill Surveyors recommend testing rental valuations against at least three explicit scenarios [6]:

| Scenario | Rent Growth Assumption | Void Assumption | Yield Assumption |

|---|---|---|---|

| Base (RICS-aligned) | Modest positive (per +29% expectation) | Current local evidence | Market yield |

| Stress | Flat or modestly negative real rents | Higher voids (+2–4 weeks) | +50–75 bps premium |

| Upside | Continued demand outpacing supply | Minimal voids | Market yield or tighter |

Adapted from Notting Hill Surveyors scenario framework [6]

This approach prevents over-reliance on a single forecast in what RICS itself describes as an "interest-rate- and geopolitics-sensitive" environment [7]. The stress scenario is particularly important: if geopolitical tensions push borrowing costs higher or trigger a mild recession, real rents could stagnate even if nominal rents edge upward.

For complex income-producing assets, a commercial valuation framework — with explicit discounted cash-flow modelling — may be more appropriate than a simple yield-and-rent approach.

Tactic 3: Recalibrate Void Period Assumptions

One of the most actionable — and frequently overlooked — tactics in the current market is updating void period assumptions. Many valuation models still use legacy rules of thumb such as "one month void per year." In a market where landlord instructions are at -25% and tenant demand is at +10%, this assumption may significantly under-value income-producing rental assets [4].

Recommended approach:

- Obtain local letting agent data on average void periods for comparable properties (type, location, condition).

- Use this as the primary input, not a generic national benchmark.

- Document the source and date of void data in the valuation report — this is increasingly important in dispute contexts [5].

💬 "Over-stating voids could under-value income-producing assets in the current constrained-supply environment." — Wimbledon Surveyors [4]

Tactic 4: Apply Explicit Geopolitical Discount (or Document Why You Haven't)

Canterbury Surveyors, writing on expert-witness preparation in the context of the February 2026 RICS data, recommend a three-step approach to geopolitical risk documentation [5]:

- Cite RICS national balances on tenant demand (+10%) and landlord instructions (-25%) to establish macro conditions.

- Show regional calibration — for example, firmer conditions in the North West, Scotland, and Northern Ireland may justify tighter yield assumptions than in London [1].

- Record explicitly whether a geopolitical discount or premium has been applied, and why — including any qualitative factors such as local energy-cost exposure or tenant employment base.

This documentation discipline is not merely good practice; it is increasingly necessary for valuations that may face challenge in dispute or litigation contexts [5]. For properties subject to formal dispute processes, understanding valuation factors in depth is essential preparation.

Regional Divergence and Yield Assessment in 2026

One of the most significant findings from the February 2026 RICS survey — and one that directly affects rental valuations — is the sharp regional divergence in market conditions [1][7].

London and South East: Caution Required

Price sentiment in London and the South East is deeply negative (price balances of -24% to -40%) [1]. While rental demand remains positive, the combination of high capital values, elevated funding costs, and compressed gross yields means that:

- Yield assumptions must account for higher risk premiums in the current environment.

- Valuers should not assume that London's structural rental demand automatically justifies aggressive yield compression.

- The spread between gross and net yields is wider than in lower-cost regions, given higher service charges, management costs, and regulatory compliance burdens.

North West, Scotland, and Northern Ireland: Relative Resilience

These regions show firmer price trends and robust rental demand [1][3]. Critically, rent-to-price ratios and achievable gross yields are often more favourable outside London, meaning:

- Regional buy-to-let valuations should not mechanically import London risk premiums.

- Where local employment is stable and tenant demand is strong, yield assumptions can be more optimistic — provided they are supported by local comparable evidence.

- The RICS data for these regions provides a legitimate evidential basis for tighter yields in formal valuations [7].

For those seeking chartered surveyors in specific regional locations, working with a surveyor who has genuine local market knowledge is particularly important when regional divergence is this pronounced.

The Investor Perspective: Income Security in Uncertain Times

Higher mortgage rates (rising to approximately 5.90% after geopolitical escalation in early 2026) have a paradoxical effect on rental markets: they push marginal buyers back into renting, supporting demand, while simultaneously increasing the cost of leveraged investment [2]. For valuers, this means:

- Increased investor interest in income-secure rental assets — but at yields that reflect higher funding costs.

- Discount rates in cash-flow models should be updated to reflect the current rate environment, not the pre-escalation baseline.

- The gap between gross yield and net-of-financing yield has widened, which affects the price investors will pay for rental assets.

A stock condition survey can add significant value here by identifying capital expenditure requirements that affect net yield calculations — particularly relevant for older rental stock where energy efficiency improvements may be required.

Policy, Regulatory Risk, and Valuation Transparency

Geopolitical and economic stress does not occur in a policy vacuum. Both Notting Hill Surveyors and Canterbury Surveyors highlight that regulatory and policy risks tend to be amplified when governments are under pressure from cost-of-living and energy-price concerns [5][6].

Key Policy Risks to Flag in 2026 Rental Valuations

- 🏛️ Rent control legislation: Increasingly debated in the context of affordability pressures; any valuation of residential rental income should note this as a qualitative risk.

- 💰 Landlord taxation changes: Capital gains tax, stamp duty, and mortgage interest relief have all been subject to change in recent years; further adjustments cannot be ruled out.

- 📋 Local licensing schemes: Houses in Multiple Occupation (HMO) licensing and selective licensing schemes can materially affect net yields and should be verified at the property level.

- ⚡ Energy Performance Certificate requirements: Proposed minimum EPC standards for rental properties represent a potential capital expenditure liability that affects net income.

💬 "Non-quantifiable, policy-driven risks should be explicitly flagged in the valuer's commentary and sensitivity work." — Canterbury Surveyors [5]

These risks should appear in the valuation report's commentary section, even where they cannot be precisely quantified. Transparency about what has — and has not — been modelled is a hallmark of defensible professional practice.

For landlords navigating lease-related complexity, the FAQ on lease extensions provides useful context on how lease structure affects both rental and capital value.

Conclusion: Actionable Next Steps for Valuers and Landlords

Valuing rental properties in geopolitical uncertainty — applying RICS February 2026 survey tactics for cautious lettings markets — is not about paralysis in the face of risk. The data is clear: rental demand is resilient, supply is constrained, and near-term rental growth expectations remain positive [7]. The challenge is translating that structural strength into defensible, transparent valuations that honestly reflect the macro risks surrounding it.

Actionable Next Steps ✅

- Update your comparables database using achieved rents from the past 3–6 months, explicitly excluding pre-stress-period data unless adjusted.

- Run three-scenario cash-flow models (base, stress, upside) for every income-producing rental asset, documenting assumptions clearly.

- Recalibrate void period assumptions using current local letting agent data rather than legacy benchmarks — constrained supply justifies tighter void assumptions in many markets [4].

- Apply regional calibration to yield assumptions, avoiding the mechanical transfer of London risk premiums to regional markets where fundamentals are firmer [1].

- Document geopolitical and policy risk explicitly in valuation reports, including whether a discount has been applied and why — this is essential for dispute resilience [5].

- Update discount rates in cash-flow models to reflect the current mortgage rate environment (approximately 5.90% for 2-year fixed products as of early 2026) [2].

- Commission a stock condition survey for older rental portfolios to identify capital expenditure requirements that affect net yield calculations.

The February 2026 RICS data provides a robust evidential foundation for rental valuations — but only for valuers who use it actively, document their reasoning carefully, and resist the temptation to import sales-market pessimism into a lettings market that is, structurally, still performing [7][3].

References

[1] Latest Rics Survey Reveals Global Headwinds Are Weighing On Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/

[2] Rics Survey Iran War – https://anyhousewanted.co.uk/uk-house-prices/rics-survey-iran-war/

[3] Valuation Strategy Shifts In Q2 2026 Interpreting Rics February Survey Data Amid Geopolitical Uncertainty And Regional Divergence – https://wimbledonsurveyors.com/valuation-strategy-shifts-in-q2-2026-interpreting-rics-february-survey-data-amid-geopolitical-uncertainty-and-regional-divergence/

[4] Valuation Adjustments From February 2026 Rics Survey Countering Geopolitical Caution In Buyer Enquiries And Price Expectations – https://wimbledonsurveyors.com/valuation-adjustments-from-february-2026-rics-survey-countering-geopolitical-caution-in-buyer-enquiries-and-price-expectations/

[5] Geopolitical Uncertainty In Rics February 2026 Survey Expert Witness Preparation For Valuation Volatility Disputes – https://www.canterburysurveyors.com/blog/geopolitical-uncertainty-in-rics-february-2026-survey-expert-witness-preparation-for-valuation-volatility-disputes/

[6] Valuation Challenges In Uncertain Markets Using Rics February 2026 Data To Adjust Valuations Amid Geopolitical Volatility And Interest Rate Concerns – https://nottinghillsurveyors.com/blog/valuation-challenges-in-uncertain-markets-using-rics-february-2026-data-to-adjust-valuations-amid-geopolitical-volatility-and-interest-rate-concerns

[7] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[8] Simon Rubinsohn 43124162 Uk Residential Market Survey Activity 7437780947632189442 Dpkb – https://www.linkedin.com/posts/simon-rubinsohn-43124162_uk-residential-market-survey-activity-7437780947632189442-dpKB

[10] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf