Nearly one in five UK homes is privately rented — yet in 2026, the regulatory and tax landscape governing those properties is shifting faster than at any point since mortgage interest relief was phased out between 2017 and 2020. Reassessing buy-to-let: what 2026 landlord tax changes and market recovery mean for valuation surveys is no longer an abstract exercise for accountants. It is a live, practical question that affects how lenders underwrite mortgages, how surveyors calculate market value, and how investors decide whether to buy, hold or sell.

This article unpacks the interaction between tightening taxation, the quarterly reporting revolution of Making Tax Digital (MTD), and the cautious market recovery underway in 2026 — and explains what all of this means for the surveys and valuations that sit at the heart of every buy-to-let transaction.

Key Takeaways 📌

- MTD for Income Tax becomes mandatory from April 2026 for landlords earning over £50,000, introducing quarterly digital reporting that gives lenders and valuers fresher income data.

- Separate property tax rates from April 2027 (22% basic, 42% higher, 47% additional) will reduce net yields for unincorporated landlords, directly influencing investment valuations.

- Portfolio pruning — landlords selling weaker assets before 2027 — is already changing the mix of comparable transactions surveyors rely on.

- Market recovery in 2026 is real but fragile, with regional variation meaning surveyors must stress-test rents and capital growth assumptions more rigorously than before.

- Valuation surveys — from homebuyer reports to full building surveys — are increasingly expected to incorporate post-tax cash-flow thinking, not just gross rental multiples.

How Making Tax Digital Is Reshaping the Evidence Base for Valuations

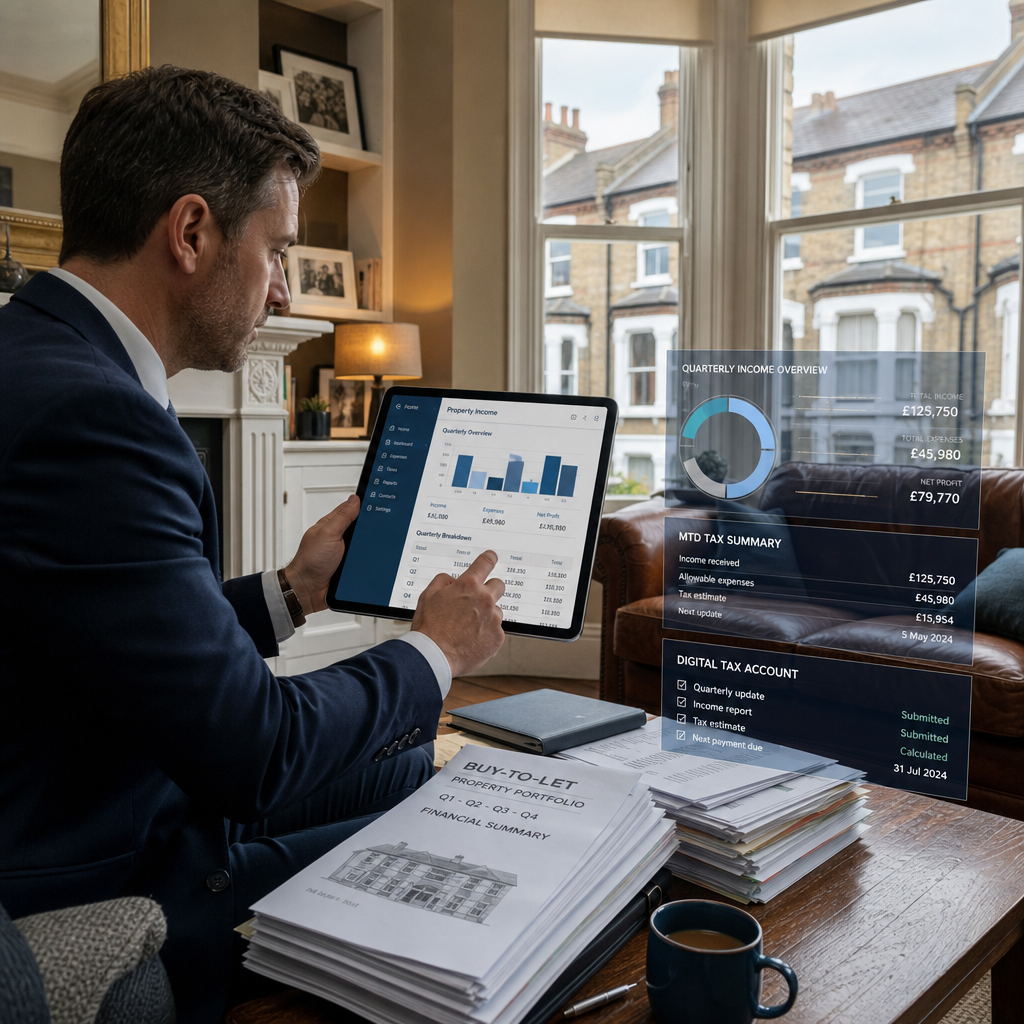

From 6 April 2026, sole-trader landlords and self-employed individuals with combined gross income above £50,000 must keep digital records and submit quarterly MTD updates to HMRC, plus an end-of-period statement and a final declaration [1][3]. The threshold falls to £30,000 from April 2027 and is expected to reach £20,000 from April 2028 [4].

For valuers and lenders, this is significant. Until now, the standard evidence for rental income has been SA302 tax calculations and tax year overviews — documents that can be 12 to 18 months out of date by the time a mortgage application lands on an underwriter's desk. MTD changes that dynamic.

"Quarterly submissions due by the 7th of August, November, February and May mean that up-to-date income evidence will, for the first time, be routinely available mid-year — not just at January's self-assessment deadline." [4]

What This Means for Interest Coverage Ratio (ICR) Stress-Testing

Buy-to-let lenders typically require rental income to cover mortgage payments at a stressed interest rate — commonly 125% to 145% of the monthly mortgage cost. Surveyors supporting these applications must assess whether the sustainable market rent (SMR) of a property meets that threshold.

With MTD data available quarterly, lenders are likely to update their affordability models more frequently. Surveyors may be asked to comment not just on current market rent but on rent trajectory — particularly relevant in regions where rents have recovered strongly in 2025–26 after a period of stagnation.

Understanding what surveyors look for in a house survey is increasingly important for landlords who want their properties to perform well in both physical inspections and financial stress-tests.

The Penalty-Points Regime and Lender Perception

HMRC is replacing the existing late-filing fine structure with a points-based system. Repeated failures to file quarterly updates on time trigger an automatic £200 penalty once a threshold of points is reached [1][2]. For professional landlords with large portfolios, persistent non-compliance could surface in accountant reports or compliance disclosures — and may begin to influence how lenders and surveyors assess the management quality and let-ability risk of a portfolio [3].

This is a subtle but real shift: valuation commentary on rental properties has traditionally focused on physical condition and location. Going forward, compliance standing may become part of the risk narrative for larger portfolio valuations.

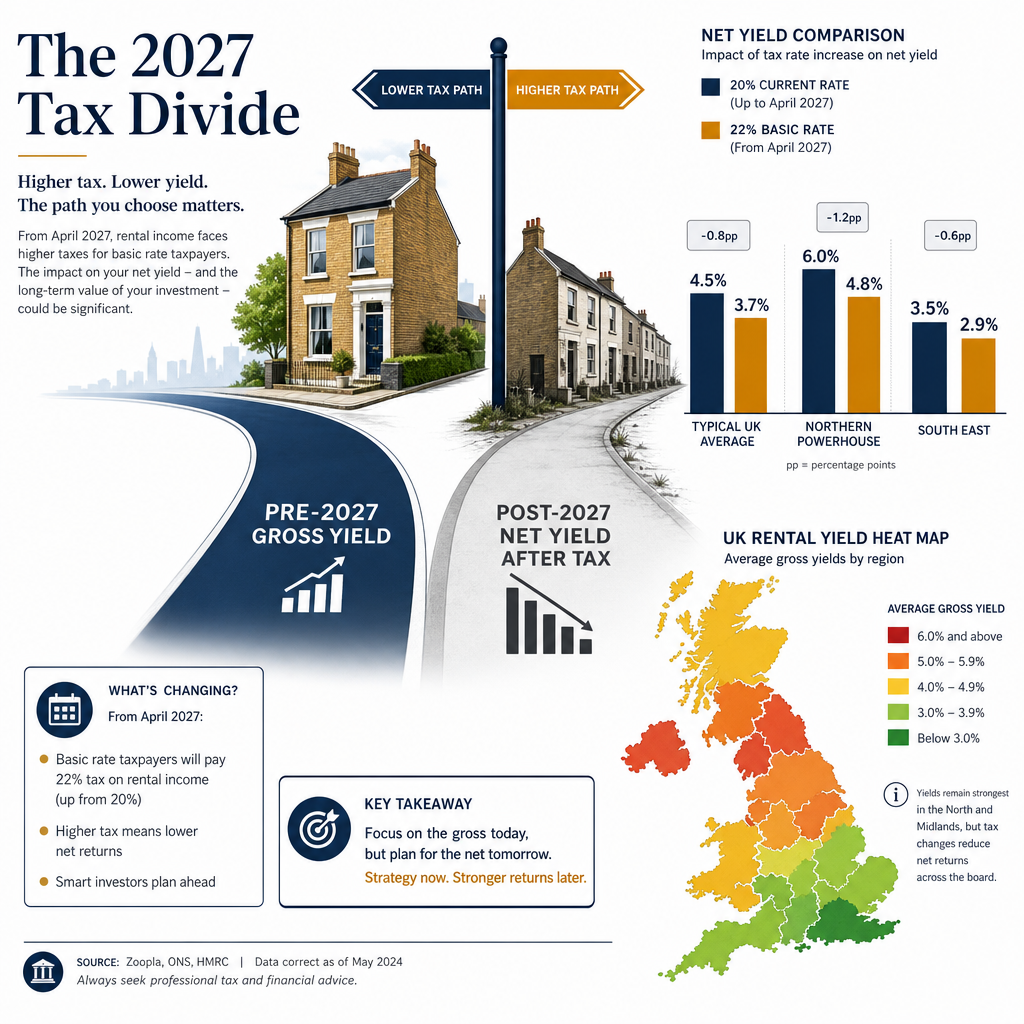

The 2027 Tax Regime: How Higher Property Tax Rates Are Already Moving Valuations

The government has legislated for separate tax rates on property income from April 2027: 22% at the basic rate, 42% at the higher rate, and 47% at the additional rate — each two percentage points above the equivalent main income tax rate [7]. Reliefs and allowances must be set against other income first, further reducing the scope to shelter rental profits [6].

This is not a future abstraction. Reassessing buy-to-let: what 2026 landlord tax changes and market recovery mean for valuation surveys requires understanding that 2026 is effectively a pricing-in year — the market is already adjusting to what 2027 will bring [9].

The Net Yield Compression Effect

Consider a higher-rate taxpaying landlord with a property generating £18,000 gross rent annually. Under current rates, income tax on rental profit might consume around 40% of net profit. From April 2027, that rises to 42% — a seemingly modest change that, compounded across a portfolio, meaningfully erodes the investment case [6][7].

| Tax Band | Current Rate | From April 2027 | Increase |

|---|---|---|---|

| Basic Rate | 20% | 22% | +2pp |

| Higher Rate | 40% | 42% | +2pp |

| Additional Rate | 45% | 47% | +2pp |

For RICS "market value" assessments, this matters because investor demand is one of the key inputs into comparable evidence. If investors are willing to pay less for buy-to-let stock due to lower post-tax returns, achieved prices in investor-dominated markets will soften — and those achieved prices become the comparables surveyors use [6][8].

Portfolio Pruning and the Comparables Problem

Industry advisers expect many landlords — especially those with highly geared or marginally profitable properties — to sell weaker-performing units before the 2027 tax rise bites, while retaining or incorporating higher-yield assets [6][8]. This selective disposal is already changing the profile of transactions coming to market.

In areas where investor-to-investor sales have historically dominated — certain London postcodes, parts of the North West and the Midlands — surveyors are now seeing more ex-rental flats and smaller terraced houses entering the resale market. These properties often require more careful condition assessment, making a Level 2 homebuyer survey or a full Level 3 building survey particularly important for buyers who may be acquiring a property that has been let for years without significant maintenance investment.

Market Recovery in 2026: Regional Variation and What It Means for Stress-Testing

The buy-to-let market in 2026 is recovering — but unevenly. After a period of price stagnation and yield compression driven by rising interest rates and regulatory pressure, moderate rent and capital value recovery is visible in some regions, while others remain subdued [2][9].

Professional advisers are telling landlords to re-run their numbers on a post-2027, higher-tax basis, which implies that surveyors doing investment valuations for larger portfolios are increasingly being asked to model values under stress-tested, post-tax cash-flows rather than purely on gross rent multiples [2][9].

Regional Snapshot: Where Recovery Is Strongest 🗺️

- Northern England & Midlands: Rental demand remains robust; yields are higher but capital growth is modest. Surveyors here are seeing stronger investor activity in 2026.

- London: Recovery is patchy. Prime zones show resilience; outer zones with high concentrations of ex-rental stock face downward pressure on values.

- South East: Rents have stabilised after sharp rises in 2023–24; capital growth expectations are cautious but positive.

- Scotland & Wales: Different regulatory environments (including rent controls in Scotland) mean valuers must apply local market knowledge carefully.

Void Risk: The Overlooked Variable

Stress-testing in buy-to-let valuations has traditionally focused on interest rate sensitivity. In 2026, void risk — the probability and cost of periods without a tenant — deserves equal attention. Rising compliance costs (including MTD administration, EPC upgrade requirements, and the Renters' Rights Act obligations) are prompting some landlords to exit the market, which in the short term tightens supply and supports rents. But in specific micro-markets, particularly purpose-built student accommodation and HMOs, oversupply and regulatory tightening are creating genuine void risk.

Surveyors assessing rental properties should consider whether the homebuyer survey or building survey they commission adequately captures condition issues that could trigger void periods — damp, heating failures, or fire safety deficiencies that would require a property to be taken off the rental market for remediation.

What Landlords and Investors Should Demand from Their Valuation Survey in 2026

Reassessing buy-to-let: what 2026 landlord tax changes and market recovery mean for valuation surveys ultimately comes down to a practical question: are the surveys being commissioned fit for purpose in a changed market?

Here is what a well-structured valuation instruction should cover in 2026:

✅ For Purchase Valuations (Lender-Instructed)

- Sustainable Market Rent (SMR) assessed against current local comparables, not historical averages

- ICR stress-test commentary at both current and stressed interest rates

- Explicit comment on void risk and local rental demand

- Condition assessment that identifies any issues likely to trigger regulatory non-compliance (EPC, HHSRS, fire safety)

✅ For Investment/Portfolio Valuations

- Post-tax yield modelling — increasingly expected by sophisticated investors and their lenders

- Commentary on comparable evidence quality, particularly where ex-rental stock is distorting the market

- Forward-looking capital growth assumptions by region, with clear sensitivity ranges

- Assessment of reinstatement cost for insurance purposes — a step often skipped on portfolio reviews but critical for accurate risk management. A reinstatement cost valuation ensures insurance cover keeps pace with build cost inflation

✅ For Landlords Considering Exit

- Full Level 3 building survey to identify latent defects before sale, avoiding price renegotiation at the point of exchange

- Lease extension valuation if the property is leasehold — short leases significantly reduce buyer pool and market value

- Dilapidations assessment if the property has been let on a commercial lease

Understanding Which Survey Type Is Right

Not every buy-to-let property requires the same level of inspection. A modern flat in a managed block may suit a Level 2 survey, while a Victorian terrace that has been let for a decade without significant works almost certainly warrants a Level 3. Use a survey comparison tool to match the survey type to the property's age, condition and complexity.

The Compliance Cost Factor: MTD Administration and Its Indirect Valuation Effects

One underappreciated consequence of MTD is its administration cost. Landlords who have historically managed their tax affairs informally — a spreadsheet and an annual accountant visit — now face the cost of MTD-compatible software, more frequent accountant engagement, and the time burden of quarterly submissions [3][4].

For small landlords with one or two properties, these costs can meaningfully erode already-thin margins. For portfolio landlords, the cost is more manageable but still real. This is accelerating the shift toward incorporation — holding properties through a limited company — which has different tax treatment and different implications for valuation surveys [8].

"A property held in a limited company is valued on the same physical basis as one held personally — but the investment value to a buyer may differ significantly, depending on how the company's tax position is structured." [8]

Surveyors asked to provide investment valuations for incorporated portfolios should understand the distinction between bricks-and-mortar market value and investment value to a specific buyer — and be clear in their reports about which basis is being applied.

Conclusion: Actionable Steps for Landlords, Buyers and Investors in 2026

The intersection of MTD compliance, the approaching 2027 tax rate increases, and a cautiously recovering market makes 2026 a pivotal year for buy-to-let decision-making. Here are the most important actions to take now:

1. Commission the right survey before any transaction. Whether buying, refinancing or selling, ensure the survey type matches the property's age and condition. Use resources like what survey do you need to identify the appropriate level of inspection.

2. Enrol in MTD-compatible software before April 2026. The quarterly reporting rhythm will reshape how income is evidenced for lenders and valuers. Being compliant from day one avoids penalty points and supports stronger mortgage applications.

3. Re-run yield calculations on a post-2027 tax basis. Any investment decision made today should be stress-tested against the 22%/42%/47% property income tax rates that take effect in April 2027. If the numbers do not work post-tax, the asset may be a disposal candidate.

4. Instruct surveyors to comment explicitly on void risk and sustainable rent. Generic valuation reports that simply state a market rent figure are no longer sufficient for sophisticated lenders or investors in 2026's environment.

5. Consider a reinstatement cost review for existing portfolio properties. Build cost inflation since 2020 means many properties are underinsured. A professional assessment protects against catastrophic financial loss.

6. Seek specialist advice before incorporating. The tax advantages of a limited company structure must be weighed against stamp duty land tax on transfer, loss of personal allowances, and different mortgage product availability — all of which affect the valuation basis of the underlying assets.

The buy-to-let market is not broken — but it is being fundamentally repriced. Landlords and investors who engage with that repricing proactively, supported by rigorous surveys and accurate valuations, are best placed to navigate what comes next.

References

[1] New Tax Rules For Buy To Let Landlords From 2026 – https://www.thornleygroves.co.uk/about-thornley-groves/insights/new-tax-rules-for-buy-to-let-landlords-from-2026/

[2] The 2026 Tax Changes Landlords Need To Prepare For – https://www.taxesdoneright.co.uk/the-2026-tax-changes-landlords-need-to-prepare-for

[3] Tax Changes For Landlords 2026 Complete Guide – https://www.djh.co.uk/latest-news/news-insights/tax-changes-for-landlords-2026-complete-guide/

[4] Making Tax Digital – https://www.nrla.org.uk/resources/tax/making-tax-digital

[6] Income Tax Increase For Landlords What The April 2027 Changes Mean For You – https://www.championgroup.co.uk/income-tax-increase-for-landlords-what-the-april-2027-changes-mean-for-you/

[7] Changes To Tax Rates For Property Savings And Dividend Income – https://www.gov.uk/government/publications/changes-to-tax-rates-for-property-savings-and-dividend-income

[8] What Are The Uk Landlord Tax Changes 2026 – https://sterlingandwells.com/blogs/what-are-the-uk-landlord-tax-changes-2026/

[9] The Landlords Guide To 2026 Legislation Tax And Compliance – https://www.doublepoint.co.uk/articles/the-landlords-guide-to-2026-legislation-tax-and-compliance/