The UK property market in 2026 is telling two very different stories. While surveyors in Scotland and the North West are applying upward valuation adjustments to reflect strengthening prices, their counterparts in London and the South East face the challenge of justifying substantial downward corrections. This dramatic regional divergence, revealed in the Royal Institution of Chartered Surveyors (RICS) January 2026 survey, demands a fundamental rethinking of how chartered surveyors approach property valuations across the United Kingdom.

The Valuation Adjustments for Widening Regional Disparities: RICS January 2026 Survey Insights for Surveyors reveal a market in transition, where national averages mask profound local variations. Understanding these patterns isn't just academic—it's essential for delivering accurate, defensible valuations that protect clients and maintain professional standards.

Key Takeaways

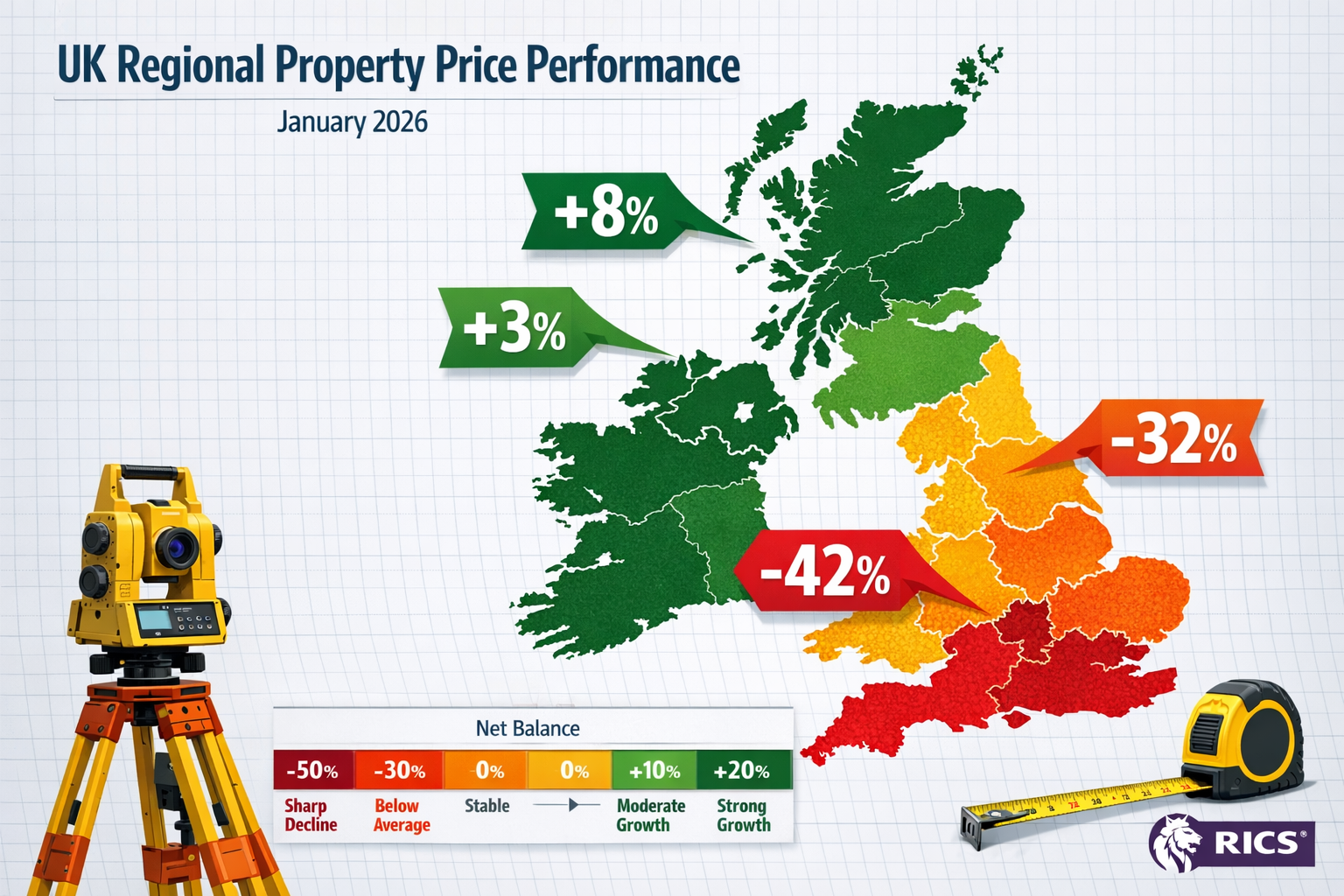

- 📊 National prices stabilizing at -10% net balance, improving from -19% in October 2025, but regional performance varies dramatically from +10% in Scotland to -42% in London

- 🏴 Scotland, Northern Ireland, and North West England lead recovery with positive price trajectories requiring upward valuation adjustments

- 📉 London and South East markets remain significantly negative, with affordability challenges necessitating substantial downward comparable adjustments

- 🔮 43% of surveyors anticipate higher prices within 12 months, the most optimistic outlook since February 2025, creating timing considerations for valuation dates

- 🏘️ Rental market tightening with tenant demand rising and landlord supply falling, requiring upward yield adjustments for investment property valuations

Understanding the Regional Divide in UK Property Markets

The January 2026 RICS survey data reveals a property market experiencing its most pronounced regional divergence in recent memory. The national net balance of -10% represents a significant improvement from the -19% recorded in October 2025[1], suggesting the market may be approaching a turning point. However, this headline figure conceals dramatic variations that require surveyors to adopt region-specific valuation methodologies.

Northern Regions Leading the Recovery

Scotland and Northern Ireland continue to record upward price trends, representing the strongest performing regions in the UK market[1]. The North West and North of England are similarly showing upward price trajectories, indicating these regions have effectively decoupled from the softer southern markets[1]. For property surveyors operating in these areas, this necessitates careful consideration of positive market momentum when selecting and adjusting comparable sales evidence.

The implications for valuation practice are significant. When conducting a RICS Home Survey in Manchester or Glasgow, surveyors must recognize that comparable sales from even six months ago may understate current market values. Time adjustments become critical, with recent transactions carrying greater weight than historical data that predates the recovery phase.

Southern England's Persistent Challenges

In stark contrast, London registered a significantly negative price performance at -42% as of December 2025, with the South East at -32%[4]. The South West and East Anglia continue to lag the national average, necessitating substantial downward valuation adjustments in these traditionally affluent regions[1]. These markets remain "more negative than the headline average," reflecting persistent affordability challenges that fundamentally impact comparable property analysis[2].

For surveyors conducting RICS building surveys in these regions, the challenge lies in distinguishing between temporary market softness and structural price corrections. The extended period of negative sentiment suggests that valuations based on 2024 peak prices would be inappropriate without significant downward adjustment.

The East Anglia Stabilization Story

East Anglia presents an interesting middle ground, showing early signs of stabilization. Market intelligence from firms operating across Hertfordshire, Essex, and Cambridgeshire indicates that while "transaction levels remain below historic norms," confidence is gradually improving and pricing appears to be finding more consistent footing[3]. However, the same sources note that "over-ambitious pricing is still being challenged, often leading to extended marketing periods or price adjustments"[3].

This observation carries important implications for valuation practice. Surveyors must apply strict comparables discipline in regions experiencing recovery, rejecting asking prices or initial listing data in favor of actual achieved sale prices. The gap between optimistic vendor expectations and market reality remains significant in these transitional markets.

Valuation Adjustments for Widening Regional Disparities: Survey-Driven Methodologies

The Valuation Adjustments for Widening Regional Disparities: RICS January 2026 Survey Insights for Surveyors demand a systematic approach to regional market analysis. Surveyors cannot rely on national trends or historical regional relationships—each local market requires independent assessment based on current evidence.

Implementing Location Coefficient Adjustments

Traditional valuation methodology recognizes location as a primary value driver, but the current market requires dynamic location coefficients that reflect rapidly changing regional performance. A property in the North West may now command a premium relative to comparable properties in the South East—a reversal of historical patterns that many valuation models fail to capture.

When conducting Level 3 building surveys, surveyors should document the regional market context explicitly. This includes:

- Regional net balance figures from the RICS survey as market condition evidence

- Comparative regional performance showing divergence from national trends

- Local market intelligence from active estate agents and recent transaction data

- Affordability metrics specific to the region, including price-to-income ratios

Time Adjustment Strategies in Volatile Markets

The divergence between 3-month sales expectations (+4%) and 12-month expectations (+35%) reveals a market where timing matters enormously[1]. This represents the strongest 12-month reading since December 2024, yet short-term caution persists. For surveyors, this creates a tension between current market conditions and anticipated future performance.

Best practice dictates that valuations reflect market conditions at the valuation date, not projected future values. However, surveyors must be transparent about market trajectory when advising clients. A property valued in January 2026 in a recovering northern market may see appreciation by year-end, while a London property may face continued softness.

When applying time adjustments to comparable sales, consider:

- Transaction date proximity: Recent sales (within 3 months) require minimal adjustment in stable markets but may need significant adjustment in rapidly changing regions

- Market phase identification: Is the local market in decline, stabilization, or recovery?

- Seasonal factors: Traditional spring market dynamics may be disrupted by regional divergence

- Transaction type: Forced sales or distressed transactions require additional scrutiny

Comparable Selection in Divergent Markets

The widening regional disparities make comparable selection more challenging but also more critical. Surveyors conducting homebuyer surveys must expand their comparable search criteria while simultaneously applying stricter relevance filters.

Geographic proximity remains important, but micro-market variations within regions have intensified. A property in inner London may perform differently from outer London suburbs, while coastal areas in the South West show different patterns from inland towns. Chartered surveyors in Surrey face different market conditions than those in Sussex, despite their geographic proximity.

The RICS survey data suggests that property type and condition have become more significant differentiators. Strong demand for comprehensive property surveys, particularly for older or altered properties in regions like Hertfordshire, Essex, and Cambridgeshire[3], indicates that buyers are increasingly sensitive to defect risk. This heightened scrutiny means that properties in excellent condition may command premiums over those requiring work—a spread that may have widened compared to historical norms.

Regional Case Studies: Applying RICS January 2026 Insights

To illustrate how Valuation Adjustments for Widening Regional Disparities: RICS January 2026 Survey Insights for Surveyors translate into practical valuation decisions, consider these representative scenarios across different UK regions.

Case Study 1: North West England Recovery Market

Property: Three-bedroom semi-detached house in Greater Manchester

Valuation Date: January 2026

Regional Context: North West showing upward price trajectory[1]

A surveyor conducting a valuation for mortgage purposes identifies three comparable sales:

- Comparable A: Sold December 2025 for £285,000

- Comparable B: Sold September 2025 for £275,000

- Comparable C: Sold June 2025 for £270,000

Adjustment Strategy: Given the North West's positive momentum, the surveyor applies a +2% time adjustment to Comparable B (4 months old) and +4% adjustment to Comparable C (7 months old), reflecting the regional recovery trajectory. This yields adjusted values of £280,500 and £280,800 respectively, closely aligned with the most recent sale at £285,000.

The surveyor's report explicitly references the RICS January 2026 survey data showing regional outperformance, providing documentary support for the positive time adjustments. The final valuation of £285,000 reflects current market conditions without speculating on future appreciation, despite the optimistic 12-month outlook.

Case Study 2: London Market Correction

Property: Two-bedroom flat in South London

Valuation Date: January 2026

Regional Context: London at -42% net balance[4]

Comparable sales present a challenging picture:

- Comparable A: Sold January 2026 for £425,000 (current month)

- Comparable B: Sold August 2025 for £465,000

- Comparable C: Sold March 2025 for £485,000

Adjustment Strategy: The surveyor recognizes that using the older comparables without adjustment would overstate current value. The London market's persistent negative performance justifies downward time adjustments of approximately -8% for Comparable B and -12% for Comparable C, yielding adjusted values of £427,800 and £427,200 respectively.

However, the surveyor also notes that the market appears to be stabilizing (improving from -19% nationally in October)[1]. Rather than extrapolating continued decline, the valuation relies most heavily on the recent January sale at £425,000, with the adjusted older comparables providing supporting evidence.

The report for this chartered surveyor in Fulham explicitly acknowledges the "significantly negative price performance" in London while noting "early signs of market stabilization" to provide context for lending decisions. The final valuation of £425,000 reflects current depressed conditions without assuming further deterioration.

Case Study 3: East Anglia Transitional Market

Property: Four-bedroom detached house in Cambridgeshire

Valuation Date: January 2026

Regional Context: East Anglia showing stabilization with pricing finding "more consistent footing"[3]

The surveyor identifies a challenge: the property was initially marketed at £625,000 in October 2025 but failed to sell. It was subsequently reduced to £595,000 in December 2025 and is now under offer at £580,000.

Comparable sales in the immediate area are limited:

- Comparable A: Similar property sold November 2025 for £590,000

- Comparable B: Slightly larger property sold September 2025 for £615,000

Adjustment Strategy: The surveyor recognizes the "over-ambitious pricing being challenged" pattern described in regional market intelligence[3]. The initial asking price of £625,000 is dismissed as unrealistic, reflecting vendor expectations rather than market reality.

After applying size adjustments and modest negative time adjustments to reflect the stabilizing (but not yet recovering) market, the surveyor concludes that £585,000 represents fair market value—closely aligned with the negotiated offer price and the November comparable. The report explicitly notes that "transaction levels remain below historic norms" and that extended marketing periods are common, providing context for the price negotiation history.

This chartered surveyor in Essex approach demonstrates the importance of distinguishing between asking prices and achieved sales in transitional markets.

Forward-Looking Considerations for Surveyors

The 43% of respondents anticipating higher prices over the next 12 months[1] represents the most positive price outlook since February 2025. This optimism, combined with 12-month sales expectations surging to +35%[1], creates both opportunities and challenges for valuation professionals.

Balancing Current Conditions with Future Expectations

Professional valuation standards require that valuations reflect market conditions at the valuation date, not anticipated future performance. However, surveyors have a duty to inform clients about market trajectory, particularly when advising on purchase timing or investment decisions.

For clients considering purchases in recovering northern markets, surveyors might note that current valuations reflect present conditions but that regional performance trends suggest potential for appreciation. Conversely, for London and South East purchases, surveyors should highlight that while stabilization appears underway, the market remains significantly below previous peaks.

This distinction is particularly important for Help to Buy valuations, where government equity stakes create long-term implications. A property purchased in a recovering market may generate different equity share outcomes than one in a persistently soft market.

Rental Market Dynamics and Investment Valuations

The RICS survey reveals that tenant demand is edging higher after two quarters of flat or negative readings, while landlord instructions remain firmly negative[1]. This supply-demand imbalance means rental prices are expected to continue rising in the near term, requiring surveyors to adjust implied rental yields upward, particularly for investment property valuations.

For commercial building surveys and residential investment valuations, this creates a counterintuitive scenario: capital values may be soft in southern regions, but rental yields are improving due to rising rents. The investment case for buy-to-let properties may actually be strengthening in markets where capital values have corrected significantly.

Surveyors conducting investment valuations should:

- Update rental comparables frequently, as the market is moving quickly

- Apply lower yield percentages (higher multiples) to reflect improving rental market conditions

- Consider regional rental market variations, as tenant demand patterns may differ from sales market trends

- Document landlord supply constraints as a factor supporting rental growth projections

Defect Sensitivity and Condition Adjustments

The "strong demand for RICS Home Surveys (Level 2 and Level 3)" in regions like Hertfordshire, Essex, and Cambridgeshire, particularly for older or altered properties[3], reflects heightened buyer sensitivity to property condition. This trend has valuation implications beyond the survey fee itself.

Properties requiring significant remedial work may face wider discounts than historical norms would suggest. Buyers in a cautious market are less willing to take on defect risk, particularly given the affordability challenges that persist in many regions. When conducting comprehensive condition survey reports, surveyors should consider whether identified defects would have a proportionally larger impact on value in the current market.

Conversely, properties in excellent condition with recent improvements may command premiums over standard comparables. The "flight to quality" phenomenon common in uncertain markets appears to be manifesting in the current UK property landscape.

Practical Implementation for Survey Professionals

For surveyors seeking to implement the Valuation Adjustments for Widening Regional Disparities: RICS January 2026 Survey Insights for Surveyors in daily practice, several concrete steps can improve valuation accuracy and defensibility.

Developing Regional Market Intelligence Systems

Successful valuation practice in 2026 requires systematic regional market monitoring beyond what any single survey provides. Surveyors should:

- Subscribe to RICS monthly survey updates and maintain a database of regional net balance figures over time

- Establish relationships with active local estate agents in each market area to supplement quantitative data with qualitative insights

- Track days on market and price reduction frequency as leading indicators of market direction

- Monitor mortgage approval rates and lending criteria by region, as credit availability affects achievable prices

- Maintain comparable sales databases with detailed adjustment notes to build institutional knowledge

Chartered surveyors in West London operating across multiple boroughs need particularly robust systems to track micro-market variations within the broader London market.

Documentation Standards for Regional Adjustments

Given the unusual market conditions and significant regional variations, documentation standards become critical for professional defensibility. Valuation reports should explicitly:

- State the regional market context with reference to RICS survey data or equivalent market intelligence

- Justify time adjustments with reference to regional price trends, not just national averages

- Explain comparable selection criteria and why certain potential comparables were rejected

- Quantify and justify all adjustments with transparent methodology

- Distinguish between market value and market conditions commentary to avoid confusion about the valuation figure itself

This enhanced documentation serves multiple purposes: it protects the surveyor professionally, provides transparency for clients and lenders, and creates a knowledge base for future valuations in the same area.

Continuing Professional Development Focus Areas

The rapidly evolving regional landscape demands that surveyors invest in targeted continuing professional development (CPD). Priority areas for 2026 include:

- Advanced comparable analysis techniques for volatile and divergent markets

- Regional economic analysis to understand the fundamental drivers behind regional performance differences

- Rental market valuation as the investment landscape shifts

- Communication skills for explaining complex regional variations to clients unfamiliar with market dynamics

- Technology tools for market analysis, comparable searching, and adjustment calculations

Professional bodies including RICS offer specialized training on valuation types and methodologies that address current market challenges.

Conclusion

The Valuation Adjustments for Widening Regional Disparities: RICS January 2026 Survey Insights for Surveyors reveal a UK property market undergoing its most significant regional divergence in recent memory. With Scotland and the North West showing positive momentum while London languishes at -42%, surveyors can no longer rely on national trends or historical regional relationships to guide valuation decisions.

The path forward requires rigorous regional market analysis, disciplined comparable selection, and transparent adjustment methodologies that reflect current market realities rather than outdated assumptions. Surveyors must balance the improving national sentiment—with 43% expecting higher prices within 12 months—against persistent regional weaknesses that show no signs of rapid resolution.

Actionable Next Steps for Surveyors

- Audit your current valuation methodology to ensure regional market conditions are explicitly considered in every valuation

- Establish systematic regional monitoring using RICS survey data, local market intelligence, and transaction analysis

- Review recent valuations in light of January 2026 survey insights to identify any systematic biases or outdated assumptions

- Enhance documentation standards to provide transparent justification for regional adjustments

- Invest in CPD focused on advanced valuation techniques for divergent markets

- Communicate proactively with clients about regional market dynamics and their implications for property decisions

The UK property market of 2026 demands more from surveyors than ever before. Those who rise to meet this challenge with rigorous analysis, transparent methodology, and clear communication will not only protect their professional standing but provide genuine value to clients navigating an increasingly complex market landscape.

For professional surveying services that incorporate the latest RICS market intelligence and regional analysis, explore our comprehensive survey offerings or contact our team of experienced chartered surveyors serving locations across the UK.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[3] Uk Residential Market Survey January 2026 – https://www.navah-consulting.co.uk/news/uk-residential-market-survey-january-2026

[4] Uk Residential Survey Dec 2025 Confidence Rebound – https://www.rics.org/news-insights/uk-residential-survey-dec-2025-confidence-rebound