A levy that was once dismissed as political fantasy is now law. Chancellor Rachel Reeves confirmed in the 26 November 2025 Budget that a High Value Council Tax Surcharge — widely referred to as the mansion tax — will apply to all residential properties valued above £2 million, with collection beginning in April 2028. For owners and buyers in Notting Hill, Holland Park, Kensington, and the wider prime central London market, the clock is already ticking.

The prime central London mansion tax 2026 high value council tax surcharge is not a distant concern. It is reshaping acquisition strategies, influencing pricing conversations, and — critically — making independent professional valuations more important than they have been in a generation.

Key Takeaways 📌

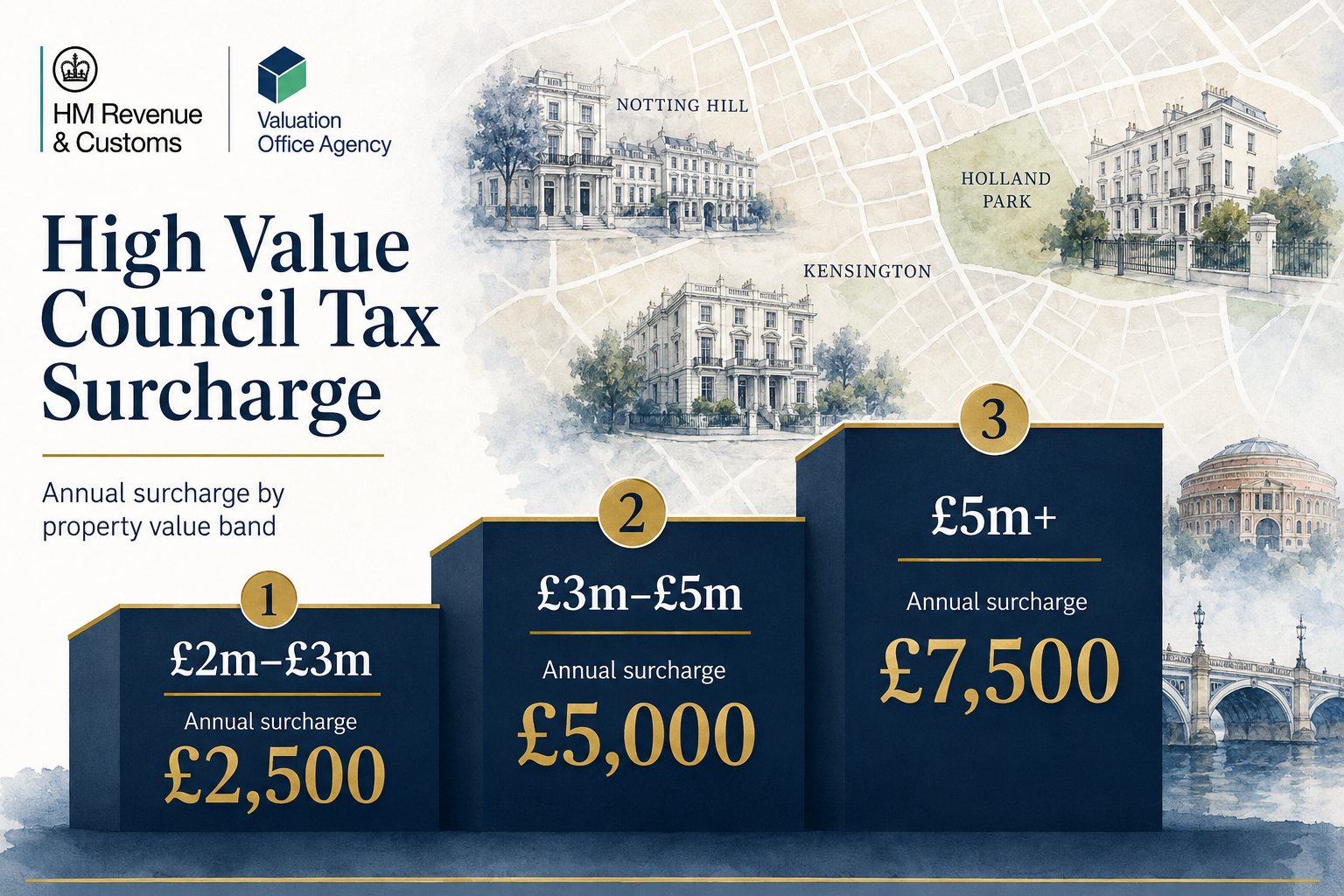

- The High Value Council Tax Surcharge applies to properties valued over £2 million, with annual charges of £2,500 to £7,500 depending on value band.

- Collection begins April 2028, but the tax is already influencing buyer and seller behaviour right now in 2026.

- Valuations will be carried out by the Valuation Office Agency (VOA) — but owners near the £2m threshold should not rely solely on a government assessment.

- An independent RICS Red Book valuation could be the difference between paying the surcharge or not — a saving of thousands of pounds per year.

- Prime central London prices had already fallen 4.3% before the Budget announcement, creating a nuanced backdrop for the new charge.

Understanding the High Value Council Tax Surcharge: The Key Details

How the Surcharge Is Structured

The High Value Council Tax Surcharge is collected alongside existing council tax bills, meaning it integrates into the existing billing framework rather than creating an entirely new tax mechanism. The tiered annual charges are as follows:

| Property Value Band | Annual Surcharge |

|---|---|

| £2,000,001 – £3,000,000 | £2,500 |

| £3,000,001 – £5,000,000 | £5,000 |

| £5,000,001 and above | £7,500 |

These are not one-off charges. They recur every year, making them a permanent addition to the cost of ownership for high-value properties across prime central London and beyond.

It is worth noting that pre-Budget speculation had suggested a far more punitive structure — some analysts feared a 1% annual levy on properties above £2 million, which on a £3 million home would have meant £30,000 per year. The confirmed surcharge figures came as a significant relief to the market. Sentiment stabilised quickly following the announcement, and a number of transactions that had been placed on hold resumed shortly after, albeit constrained by the timing near the Christmas period.

Who Carries Out the Valuations?

The Valuation Office Agency — the same body responsible for council tax banding — will carry out property valuations to determine which band each home falls into. This is important context for owners, because VOA valuations are conducted at scale, using desktop-based methodologies and comparable evidence rather than detailed on-site inspections.

Why the Prime Central London Mansion Tax 2026 High Value Council Tax Surcharge Makes Independent Valuations Essential

The £2 Million Threshold Problem

"The difference between being inside or outside the surcharge threshold could be a matter of a few thousand pounds in assessed value — but the financial consequence is £2,500 every single year."

For homeowners whose properties sit near the £2 million mark, the stakes are significant. In prime central London — where Notting Hill garden-flat conversions, Holland Park lateral apartments, and Kensington mews houses frequently cluster around this value — the margin between paying nothing and paying £2,500 annually could be razor-thin.

The VOA will use its own methodology. If you believe their assessment is incorrect, you will need robust evidence to challenge it. That evidence needs to be professional, documented, and defensible — which is precisely what a RICS Red Book valuation provides.

Our RICS registered valuers at Notting Hill Surveyors carry out formal Red Book valuations that comply fully with the Royal Institution of Chartered Surveyors' global valuation standards. These reports are legally robust, independently produced, and carry the weight needed to challenge a VOA assessment if required.

Acting Now, Not in 2027

With April 2028 as the collection start date, many homeowners may feel there is no urgency. That instinct is understandable — but it is mistaken. Here is why acting in 2026 makes sense:

- Market values shift. A property worth £1.95 million today may appreciate above the threshold before the VOA conducts its assessment. Knowing your current value creates a documented baseline.

- Comparable evidence degrades. The sales data used to support a valuation challenge is strongest when recent. Commissioning a valuation now preserves contemporaneous evidence.

- Acquisition decisions are being made now. Buyers considering properties near the threshold need to factor the surcharge into their long-term ownership cost calculations before exchanging contracts.

For buyers and owners seeking specialist advice in the area, our chartered surveyors in central London are well-placed to assist with valuations and property assessments across the prime central London market.

Understanding Your Valuation Factors

Not all properties of a similar size or postcode will be valued identically. The VOA — and any independent valuer — will consider a range of factors including:

- Floor area and configuration

- Condition and specification

- Outdoor space (garden, terrace, roof terrace)

- Parking (particularly valuable in Kensington and Notting Hill)

- Lease length for leasehold properties

- Planning history and permitted development potential

Our detailed guide to valuation factors explains how each element is weighted in a formal assessment. Understanding these factors before the VOA arrives puts you in a far stronger position.

The Broader Impact on Prime Central London Transactions

A Market Already Under Pressure

The mansion tax announcement did not land in a buoyant market. At the time of the November 2025 Budget, prime central London prices had fallen 4.3% over the preceding 12 months — the widest annual decline since February 2021. This was a market already absorbing the impact of elevated mortgage rates, stamp duty changes, and shifting buyer sentiment from international purchasers navigating the non-resident stamp duty surcharge.

The prime central London mansion tax 2026 high value council tax surcharge adds a new, recurring cost layer to ownership. For owner-occupiers, this is an additional annual outgoing. For investors, it compounds the effect of the reduced CGT annual exemption (now just £3,000 per year) and — for landlords above the income threshold — the Making Tax Digital compliance requirements that became mandatory from April 2026.

The Case for Proactive Surveys Before Transacting

Whether you are buying, selling, or simply holding a prime central London property, the surcharge changes the calculus in practical ways:

For buyers 🏠

- Commission an independent valuation before offer, not after. If a property is assessed at £2.1 million by the VOA, you will pay £2,500 per year. Knowing this in advance allows for price negotiation.

- Consider a full building survey to identify any condition issues that may affect value — defects that reduce the assessed value could keep you below the threshold.

For sellers 🏷️

- A formal RICS valuation gives you an evidence-based asking price, and demonstrates to buyers that the property has been professionally assessed — reducing the risk of post-survey renegotiation.

- Properties near the £2 million mark may benefit from a comprehensive condition survey report to demonstrate that the property's condition supports its value positioning.

For existing owners 📋

- If you believe your property may be mis-banded by the VOA, a Red Book valuation provides the independent evidence needed to mount a formal challenge.

- Leasehold owners should also consider whether a lease extension valuation is relevant — a short lease materially affects value and could influence which band a property falls into.

Outer London Is Not Immune

It is tempting to view the surcharge as a prime central London issue exclusively. However, a meaningful proportion of properties in outer London — particularly in areas such as Barnes, Chelsea, and parts of west London — also exceed the £2 million threshold. Owners in these locations face identical obligations. Our chartered surveyors in west London and chartered surveyors in Chelsea are available to assist owners across the wider high-value London market.

Conclusion: Take Control of Your Valuation Position Now

The prime central London mansion tax 2026 high value council tax surcharge is a permanent feature of the ownership landscape for high-value properties. With collection beginning in April 2028, there is a window of opportunity — but it is narrowing.

Here are the actionable steps we recommend for every prime central London homeowner:

- ✅ Commission an independent RICS Red Book valuation if your property is near the £2 million threshold — do not wait for the VOA to make the first move.

- ✅ Review your property's condition with a professional building survey — defects affect value, and value determines your band.

- ✅ Seek specialist advice before transacting — buyers and sellers should factor the surcharge into negotiations and due diligence.

- ✅ Consider lease extension if you hold a leasehold property with a shorter lease — this directly affects your assessed value.

- ✅ Document your position now — contemporaneous valuation evidence is strongest when produced well ahead of any dispute.

At Notting Hill Surveyors, we are a RICS chartered firm with deep expertise across Notting Hill, Holland Park, Kensington, and the wider prime central London market. We provide Red Book valuations, building surveys, and specialist property advice tailored to high-value residential owners navigating exactly this kind of policy change.

📞 Contact us today to discuss how we can help you understand your valuation position and protect your interests ahead of April 2028.