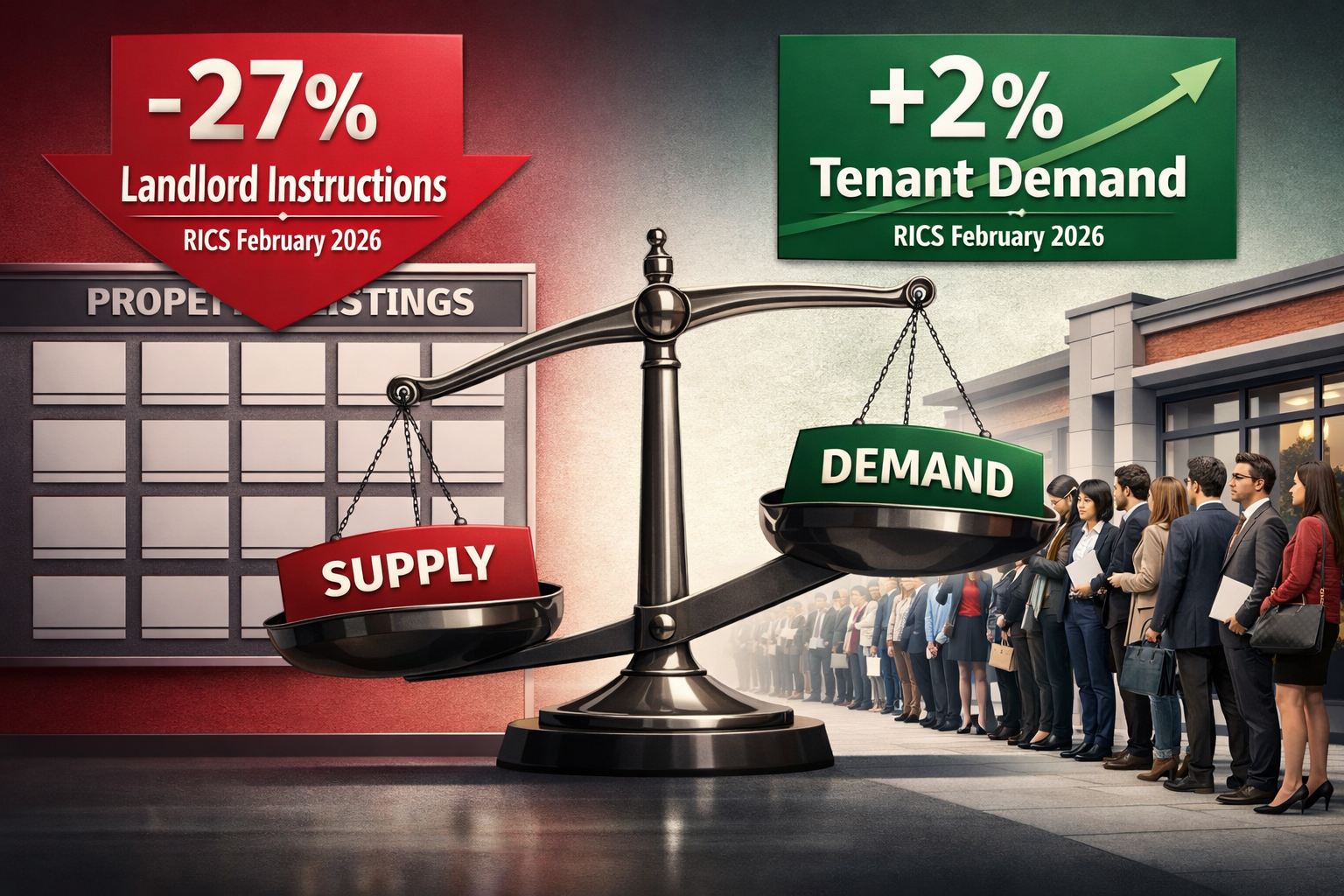

The rental property market has hit a critical inflection point: landlord instructions plummeted to a -27% net balance in February 2026, while tenant demand held steady at +2%, creating the most severe supply-demand mismatch recorded in recent RICS survey history. For valuation surveyors, this unprecedented shortage demands immediate strategic adaptation in portfolio assessments, methodology adjustments, and client advisory services.

Understanding Surveyor Strategies for Landlord Instructions Shortage: Valuations in Tight Lettings Markets per RICS February 2026 has become essential for professionals navigating this constrained environment. The February 2026 RICS UK Residential Survey reveals that one in five surveyed participants expects rents to rise over the coming quarter, directly reflecting the supply crisis. For chartered surveyors conducting rental valuations, these market dynamics require sophisticated approaches that account for limited comparable evidence, accelerated rental growth expectations, and portfolio risk assessment in an environment where fresh listings remain essentially flat.

Key Takeaways

- Landlord instructions fell to -27% net balance in February 2026, creating severe rental stock shortages while tenant demand remained stable at +2%

- 20% of survey participants forecast rent increases over the next three months, requiring surveyors to adjust valuation models for accelerated growth scenarios

- New instructions stayed neutral at +2%, indicating no immediate pipeline relief and necessitating alternative comparable evidence strategies

- Valuation methodologies must adapt to address data limitations, constrained supply dynamics, and heightened rental yield volatility

- Portfolio risk assessment becomes critical as supply-demand imbalances create divergent performance across property types and locations

Understanding the February 2026 Rental Market Crisis

The Scale of the Landlord Instruction Shortage

The RICS February 2026 data paints a stark picture of rental market dysfunction. The -27% net balance in landlord instructions represents one of the most firmly negative readings on record, signaling that significantly more landlords are withdrawing properties from the rental market than are bringing new ones forward[1][2]. This withdrawal has created what the survey describes as "an ongoing shortage of rental stock" that fundamentally alters the valuation landscape[1].

Simultaneously, tenant demand remained stable at +2% net balance over the three-month period to February, demonstrating persistent occupier appetite despite affordability pressures[1][2][3]. This stability in demand against collapsing supply creates a textbook supply-demand imbalance that drives rental inflation and complicates traditional valuation approaches.

Why New Instructions Offer No Relief

Perhaps most concerning for surveyors seeking comparable evidence is that new instructions remained neutral at +2% net balance, indicating that "fresh listings are neither rising nor falling materially at the headline level"[1][3]. This stagnation in the pipeline means valuers cannot rely on an influx of new market evidence to calibrate assessments in the coming months.

The combination of declining landlord participation, stable tenant demand, and flat new instruction pipelines creates what property valuation professionals describe as a "triple constraint" environment—limited stock, persistent demand, and no immediate relief mechanism.

Surveyor Strategies for Landlord Instructions Shortage: Valuations in Tight Lettings Markets per RICS February 2026 – Core Methodological Adaptations

Adjusting Comparable Evidence Frameworks

In markets with -27% landlord instruction balances, traditional comparable evidence becomes scarce and potentially unrepresentative. Surveyors must implement several strategic adjustments:

📊 Expanded Geographic Search Parameters

When local comparables are limited, valuers need to widen geographic boundaries while applying appropriate location adjustments. This requires deeper understanding of micro-market differentials and transport connectivity premiums.

⏰ Extended Time Horizons with Indexation

With fresh evidence scarce, surveyors may need to rely on older transactions adjusted forward using rental growth indices. The RICS data showing 20% of participants expecting rent rises provides market sentiment that can inform these adjustments[1][2][3].

🏘️ Cross-Property Type Analysis

In constrained markets, examining rental performance across property types (flats versus houses, different bedroom counts) helps establish relative value hierarchies even when direct comparables are unavailable.

📈 Yield Compression Modeling

Supply shortages typically compress yields as investors compete for limited stock. Surveyors must model how constrained supply affects capitalization rates across different property segments.

Incorporating Forward-Looking Rental Growth

The February 2026 RICS survey's finding that 20% of participants forecast rent increases over the coming quarter demands that valuers incorporate forward-looking growth assumptions into their assessments[1][2][3]. This requires:

- Scenario modeling that tests valuations under different rental growth trajectories

- Sensitivity analysis showing how portfolio values respond to 5%, 10%, or 15% rental increases

- Market cycle positioning that acknowledges where current supply constraints sit within broader rental cycles

- Risk-adjusted growth rates that account for regulatory uncertainty and potential market corrections

For professionals conducting RICS-compliant valuations, these forward-looking adjustments must be transparently documented and justified within the Red Book framework.

Data Limitation Disclosure and Uncertainty Quantification

The RICS survey flagged that February 2026 "market conditions require valuers to implement specific methodological adjustments that address both data limitations" amid broader economic volatility[4]. This necessitates:

Clear Uncertainty Statements

Valuation reports must explicitly acknowledge when comparable evidence is limited due to the -27% instruction shortage and explain how this affects confidence intervals.

Assumption Sensitivity

Surveyors should quantify how changes in key assumptions (rental growth rates, void periods, tenant demand sustainability) impact final valuations, particularly important when conducting commercial property assessments.

Market Condition Caveats

Reports should reference the specific RICS February 2026 data points to contextualize valuation decisions within documented market conditions.

Portfolio-Level Strategies for Tight Lettings Markets

Diversification Risk Assessment

In markets characterized by Surveyor Strategies for Landlord Instructions Shortage: Valuations in Tight Lettings Markets per RICS February 2026, portfolio concentration risk becomes magnified. Surveyors advising institutional clients or private landlords should:

🎯 Geographic Concentration Analysis

Assess whether portfolios are over-exposed to specific local markets where landlord exodus may be most severe. The neutral +2% new instruction balance suggests this shortage is widespread rather than localized[1][3].

🏢 Property Type Diversification

Evaluate whether portfolios maintain appropriate mix across property types, as supply constraints may affect segments differently. Building survey insights can inform which property types face greatest supply pressure.

💰 Yield Spread Monitoring

Track how yield differentials between property types and locations evolve as supply constraints create divergent performance patterns.

Tenant Quality and Covenant Strength

With stable +2% tenant demand but limited supply, tenant quality becomes a critical valuation consideration:

- Covenant strength assessment becomes more important as landlords can be more selective

- Lease length premiums may emerge as landlords seek security in uncertain markets

- Tenant retention value increases when replacement tenants are readily available but competing properties are not

Regulatory and Policy Risk Integration

The RICS survey notes "concerns persist over the building safety process" and broader regulatory pressures[5]. Surveyors must integrate these policy risks into valuations:

Building Safety Compliance

Properties with outstanding building safety issues face valuation discounts, particularly in markets where landlords are already exiting. Specific defect surveys can identify these liabilities.

Energy Performance Requirements

Anticipated EPC regulations may accelerate landlord exits, further constraining supply in certain property segments.

Rent Control Speculation

While not currently implemented, potential rent control policies create valuation uncertainty that should be addressed through scenario analysis.

Practical Implementation for Surveyors

Client Communication and Expectation Management

When explaining Surveyor Strategies for Landlord Instructions Shortage: Valuations in Tight Lettings Markets per RICS February 2026 to clients, surveyors should:

📋 Present Data Context

Share the specific RICS figures: -27% landlord instructions, +2% tenant demand, +2% new instructions, and 20% expecting rent rises[1][2][3]. This grounds conversations in objective market data.

💡 Explain Methodology Adaptations

Be transparent about how data limitations affect valuation approaches, similar to how professionals explain valuation factors in other contexts.

⚠️ Highlight Uncertainty Ranges

Provide valuation ranges rather than point estimates when comparable evidence is particularly constrained, acknowledging that tight markets create greater volatility.

Technology and Data Solutions

Modern surveying practice increasingly relies on technology to address data scarcity:

Automated Valuation Models (AVMs)

While not substitutes for professional judgment, AVMs can help identify rental trends across broader datasets when local comparables are limited.

Market Intelligence Platforms

Subscription services providing rental listing data, tenant demand metrics, and supply pipeline information help surveyors maintain market awareness despite -27% instruction shortages[1][2].

Geographic Information Systems (GIS)

Spatial analysis tools help identify comparable properties across wider geographic areas while quantifying location adjustment factors.

Professional Development and RICS Guidance

Surveyors navigating these challenging conditions should:

- Monitor RICS guidance updates as the organization responds to evolving market conditions

- Engage with peer networks to understand how colleagues are addressing similar valuation challenges

- Document methodology decisions thoroughly to support professional indemnity positions

- Consider specialist training in rental market analysis and constrained market valuation techniques

For those seeking comprehensive property assessment approaches, understanding what surveyors look for in property surveys provides foundational knowledge applicable to rental valuations.

Regional and Sector-Specific Considerations

Geographic Variation in Landlord Withdrawal

While the RICS data presents national figures, the -27% landlord instruction balance manifests differently across regions:

London and South East

Higher property values and regulatory scrutiny may drive more pronounced landlord exits, yet strong tenant demand provides valuation support.

Regional Cities

Areas with strong employment growth may see less severe instruction shortages as rental yields remain attractive to landlords.

Rural and Secondary Markets

Limited tenant pools may exacerbate supply constraints, creating valuation challenges for chartered surveyors in areas like Surrey or Sussex.

Property Type Performance Divergence

The +2% tenant demand stability masks significant variation across property types:

🏠 Family Houses

Strong demand from households seeking space, but supply constraints may be less severe as family landlords less likely to exit.

🏢 Flats and Apartments

Building safety concerns and service charge pressures may accelerate landlord withdrawals, creating acute supply shortages in this segment.

🎓 Student and HMO Properties

Specialized regulatory requirements may further constrain supply, supporting rental growth but complicating valuations.

💼 Professional Lets

High-quality properties in prime locations may see minimal supply impact as professional landlords remain committed.

Economic Context and Broader Market Forces

Interest Rate Environment

The RICS survey references "interest rate concerns" as part of the broader market uncertainty[4]. For rental valuations, this creates multiple pressures:

- Mortgage cost increases reduce landlord profitability, potentially driving further exits

- Discount rate adjustments affect investment valuations and yield expectations

- Affordability constraints may eventually dampen tenant demand, though this hasn't materialized in the +2% stable demand reading[1][2][3]

Labor and Development Constraints

The survey notes "labour shortages are less prevalent but a lack of skills will rapidly re-emerge as a barrier if development plans gather pace," with "profit margins seen as remaining under pressure through the course of this year"[5]. For surveyors, this suggests:

- Limited new supply pipeline will perpetuate rental stock shortages beyond 2026

- Development viability challenges mean market correction through new construction remains distant

- Refurbishment constraints may limit landlord ability to upgrade properties, affecting quality-adjusted rental growth

Building Safety Process Concerns

The persistent "concerns over the building safety process"[5] create specific valuation challenges:

- Cladding and fire safety issues require explicit identification and quantification in valuation reports

- Remediation cost uncertainty affects landlord exit decisions and property values

- Insurance availability impacts both landlord viability and property marketability

Surveyors conducting RICS home surveys or commercial building surveys must integrate these safety considerations into rental property assessments.

Long-Term Strategic Positioning

Anticipating Market Evolution

While February 2026 data shows -27% landlord instructions[1][2], surveyors must consider how this market may evolve:

📈 Potential Stabilization Scenarios

- Rental growth attracts new landlord entrants, gradually improving instruction balances

- Policy changes reduce regulatory burden, slowing landlord exits

- Interest rate reductions improve landlord economics

📉 Continued Constraint Scenarios

- Further regulatory tightening accelerates withdrawals beyond -27%

- Building safety costs force additional landlord exits

- Institutional investors consolidate market share, changing valuation dynamics

Building Valuation Resilience

Professional surveyors can build resilience against ongoing market constraints by:

Developing Specialist Expertise

Deep knowledge of rental market dynamics, yield analysis, and constrained market valuation becomes a competitive differentiator.

Maintaining Comprehensive Databases

Systematic collection of rental evidence, even in thin markets, builds proprietary comparable databases that support future valuations.

Cultivating Market Intelligence Networks

Relationships with letting agents, property managers, and institutional investors provide qualitative insights that supplement limited quantitative data.

Embracing Transparent Uncertainty

Rather than avoiding difficult valuations, specialists who can transparently navigate uncertainty with robust methodology gain client trust.

Conclusion

The February 2026 RICS data revealing -27% landlord instructions alongside stable +2% tenant demand and 20% expecting rent rises defines a rental market in profound supply crisis[1][2][3]. For valuation surveyors, these conditions demand immediate strategic adaptation across methodology, client communication, and professional practice.

Surveyor Strategies for Landlord Instructions Shortage: Valuations in Tight Lettings Markets per RICS February 2026 center on three pillars: methodological flexibility to address data limitations, transparent uncertainty quantification, and forward-looking rental growth integration. Professionals who master these adaptations position themselves as essential advisors in navigating constrained markets.

Actionable Next Steps

✅ Review current valuation methodologies against RICS February 2026 market conditions and identify necessary adjustments

✅ Develop scenario models incorporating the 20% rent rise expectations and various supply constraint trajectories

✅ Enhance comparable evidence databases with expanded geographic and temporal parameters to address the -27% instruction shortage

✅ Strengthen client communication frameworks to transparently explain how market constraints affect valuation confidence and methodology

✅ Monitor RICS guidance updates and engage with professional development opportunities focused on constrained market valuation

✅ Implement technology solutions that provide broader market intelligence when local comparable evidence is limited

✅ Document methodology decisions thoroughly to support professional standards and indemnity positions

The rental market crisis of 2026 presents significant challenges, but also opportunities for surveyors who adapt strategically. By implementing robust methodologies that acknowledge data limitations while providing actionable insights, valuation professionals can guide clients through this period of unprecedented supply constraint with confidence and professional integrity.

For surveyors seeking to deepen their expertise in these challenging conditions, exploring comprehensive resources on valuation types and understanding the cost of valuation services provides essential context for positioning services appropriately in tight lettings markets.

References

[1] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Rics Update On The Rental Market February 2026 – https://www.oakwoodpropertyservices.co.uk/rics-update-on-the-rental-market-february-2026/

[3] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] Valuation Challenges In Uncertain Markets Using Rics February 2026 Data To Adjust Valuations Amid Geopolitical Volatility And Interest Rate Concerns – https://nottinghillsurveyors.com/blog/valuation-challenges-in-uncertain-markets-using-rics-february-2026-data-to-adjust-valuations-amid-geopolitical-volatility-and-interest-rate-concerns

[5] Uk Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf