The UK property market stands at a pivotal moment in 2026. After years of elevated borrowing costs that dampened buyer enthusiasm and constrained transaction volumes, mortgage rates are finally retreating from their peaks. This shift is fundamentally reshaping how professional surveyors approach property valuations, requiring sophisticated adjustment techniques to accurately reflect changing market dynamics. Understanding the impact of mortgage rate cuts on 2026 property valuations and the surveyor adjustment techniques employed has become essential for property owners, investors, and industry professionals navigating this evolving landscape.

As mortgage rates decline toward the 5.5%-6.3% range throughout 2026, the ripple effects extend far beyond monthly payment calculations. Chartered surveyors must recalibrate their valuation methodologies to account for improved affordability, expanding buyer pools, and shifting market sentiment. The impact of mortgage rate cuts on 2026 property valuations requires surveyors to employ nuanced adjustment techniques that balance historical data with forward-looking market indicators.

Key Takeaways

- Mortgage rates are forecast to decline to 5.5%-6.3% in 2026, creating the first meaningful affordability improvement since 2020 and expanding the qualified buyer pool by approximately 5.5 million households [5]

- Property valuations require sophisticated time and market condition adjustments as surveyors account for the lag between comparable sales data and current market dynamics influenced by rate changes

- Buy-to-let valuations face unique recalibration challenges as lower mortgage costs improve rental yields and investment returns, requiring distinct adjustment techniques from residential owner-occupied properties

- Monthly mortgage payments could decrease by £300-400 for typical properties, offsetting modest 1-2% house price growth and improving overall market accessibility [1][2]

- Professional surveyor expertise becomes critical in 2026 as standard automated valuation models struggle to capture the nuanced impact of transitioning rate environments on property values

Understanding the 2026 Mortgage Rate Landscape

Forecast Predictions and Market Expectations

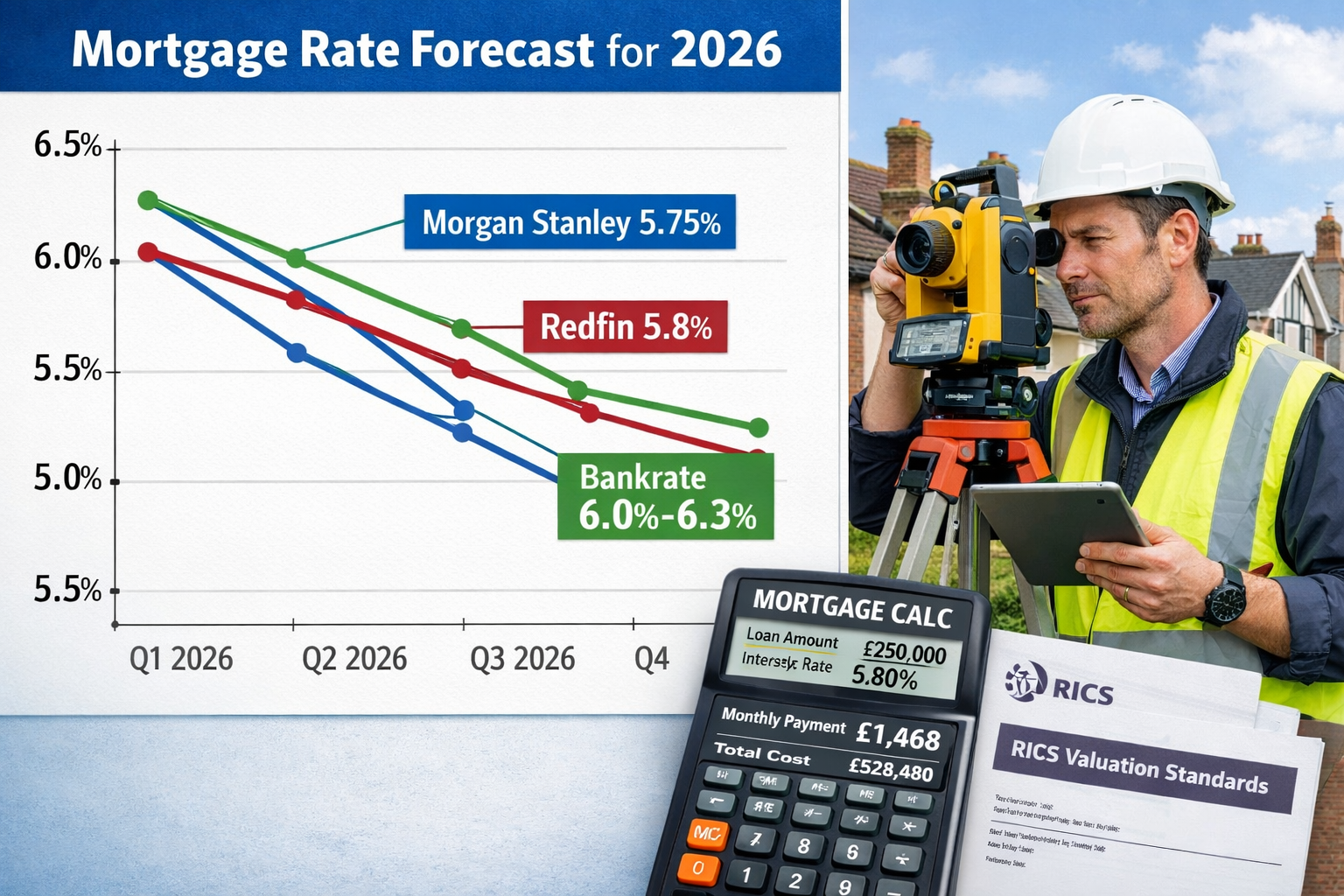

The mortgage rate environment in 2026 represents a significant departure from the elevated rates that characterized 2023-2025. Multiple authoritative forecasts converge on a similar outlook: rates will decline but remain above the ultra-low pandemic-era levels that many homeowners still enjoy.

Morgan Stanley predicts that 30-year fixed mortgage rates could decline to 5.50%-5.75% in the first half of 2026, driven by the 10-year Treasury yield declining to approximately 3.75% by mid-2026, though rates are expected to rise again in the second half of the year [1]. This forecast suggests a volatile but generally improving rate environment.

Redfin's head of economics research offers a more conservative outlook, expecting 30-year mortgage rates to average 6.3% throughout 2026, down from the 2025 average of 6.6%. Their analysis suggests rates will dip into the low-6% range but are unlikely to fall significantly below 6% for any extended period [2].

Bankrate's senior industry analyst Ted Rossman provides perhaps the most optimistic projection, predicting the 30-year fixed rate could fall below 6% for the first time since summer 2022, potentially reaching as low as 5.5%, though rates will likely fluctuate around the 6% mark throughout the year [3].

Zillow Research takes the most cautious stance, stating that mortgage rates are unlikely to fall below 6% in 2026, though borrowers have already experienced some relief during 2025 [4].

Key Rate Forecast Comparison

| Source | 2026 Rate Forecast | Key Assumptions |

|---|---|---|

| Morgan Stanley | 5.50%-5.75% (H1 2026) | 10-year Treasury at 3.75%, rates rise H2 |

| Redfin | 6.3% average | Gradual decline from 6.6% in 2025 |

| Bankrate | 5.5%-6.0% range | Potential dip below 6% temporarily |

| Zillow | Above 6.0% | Conservative outlook, limited decline |

Impact on Affordability and Buyer Demand

The practical implications of these rate reductions are substantial. For a £1 million property, monthly payment savings could reach approximately £358 per month if rates decline to 5.50% from 6.20% (monthly cost declining from approximately £4,900 to £4,542) [1].

Perhaps more significantly, research from the National Association of Home Builders demonstrates that a one percentage-point drop in mortgage rates can expand the pool of qualified homebuyers by approximately 5.5 million households, including about 1.6 million renters who could become first-time buyers [5]. This expansion in buyer demand creates fundamental shifts in market dynamics that professional surveyors must account for in their valuation methodologies.

Impact of Mortgage Rate Cuts on 2026 Property Valuations: Core Adjustment Techniques

Time Adjustment Factors in Declining Rate Environments

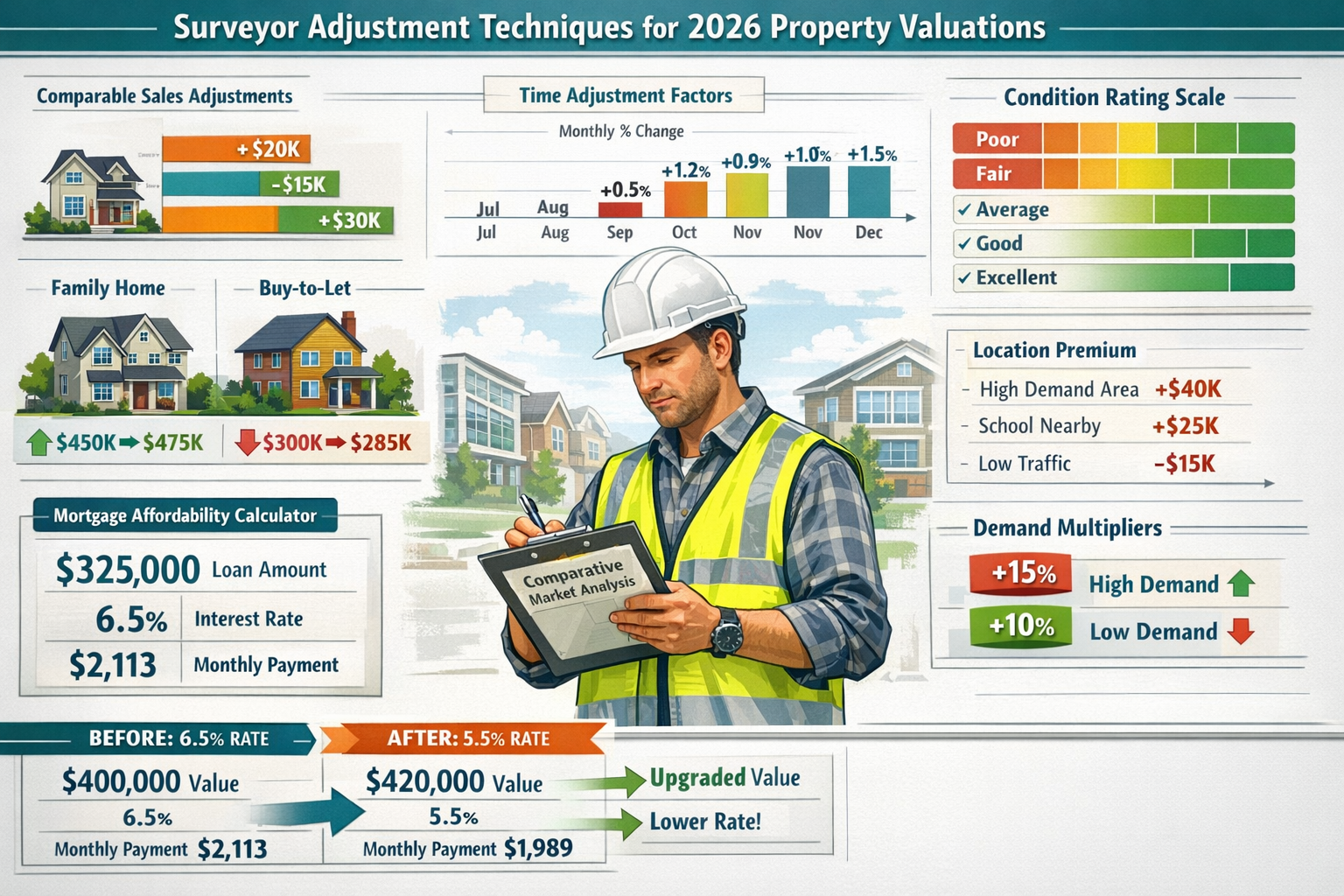

One of the most critical challenges surveyors face when assessing the impact of mortgage rate cuts on 2026 property valuations involves time adjustments to comparable sales data. Traditional valuation methodologies rely heavily on recent comparable transactions, typically within the previous 3-6 months. However, in a rapidly changing rate environment, even recent sales may not accurately reflect current market conditions.

Professional surveyors employ several sophisticated time adjustment techniques:

📊 Monthly Market Movement Analysis: Surveyors track month-over-month changes in transaction volumes, average sale prices, and time-on-market metrics to establish baseline adjustment percentages. In 2026, as rates decline, properties sold even 3-4 months ago may have transacted in a materially different affordability environment.

📈 Rate-Indexed Adjustment Factors: Advanced practitioners develop adjustment matrices that correlate specific mortgage rate levels with buyer demand intensity. For example, a comparable sale that occurred when rates were at 6.5% may require a positive adjustment of 2-3% when current rates have fallen to 5.8%, reflecting increased competition and buyer purchasing power.

🏘️ Micro-Market Velocity Tracking: Different property segments respond to rate changes at varying speeds. First-time buyer properties typically see more immediate impacts from rate reductions, while luxury properties may lag by several months. Comprehensive condition survey reports must account for these segment-specific dynamics.

Demand Multiplier Adjustments

The expansion of the qualified buyer pool creates what surveyors term "demand multiplier effects." When 5.5 million additional households suddenly qualify for mortgages due to rate reductions, the competitive dynamics for available properties shift dramatically.

Surveyors incorporate demand adjustments through:

- Buyer-to-Listing Ratios: Tracking the ratio of active buyers to available properties in specific postcodes and price bands

- Offer Competition Metrics: Analyzing the average number of offers per property and percentage of properties receiving multiple bids

- Days-on-Market Trends: Monitoring how quickly properties sell as an indicator of demand intensity

In areas experiencing strong demand multiplier effects, surveyors may apply positive adjustments of 3-5% to comparable sales that occurred before rate reductions took effect, particularly for properties in the £300,000-£600,000 range where the expanded buyer pool concentrates.

Affordability-Based Valuation Recalibration

Traditional valuation approaches focus primarily on comparable sales, with less emphasis on buyer affordability metrics. However, the impact of mortgage rate cuts on 2026 property valuations necessitates incorporating affordability analysis directly into valuation frameworks.

Modern surveyor techniques include:

✅ Payment-to-Income Modeling: Calculating what percentage of median household income is required for mortgage payments at current rates, then adjusting valuations when this ratio improves significantly

✅ Qualification Threshold Analysis: Identifying how many additional buyers can qualify for specific property price points as rates decline

✅ Comparative Payment Analysis: Comparing monthly payment requirements for subject properties against rental equivalents, with improving buy-versus-rent economics supporting higher valuations

For Level 3 building surveys, these affordability considerations become particularly important when advising clients on maximum prudent purchase prices in the evolving rate environment.

Surveyor Adjustment Techniques for Residential and Buy-to-Let Properties

Residential Owner-Occupied Valuation Adjustments

The impact of mortgage rate cuts on 2026 property valuations manifests differently across property types and ownership categories. For residential owner-occupied properties, surveyors focus primarily on end-user affordability and lifestyle value.

Key residential adjustment considerations include:

🏠 First-Time Buyer Premium: Properties appealing to first-time buyers (typically £250,000-£450,000 in most UK markets) see disproportionate demand increases as rate reductions enable entry into homeownership. Surveyors may apply 2-4% positive adjustments to comparable sales in this segment when rates have declined materially since the comparable transaction.

🏡 Family Home Stability: Larger family homes (3-4 bedrooms) in good school catchment areas demonstrate more stable valuation patterns, with 1-2% adjustments typically sufficient to account for rate-driven demand changes.

🌳 Location Premium Recalibration: Lower rates enable buyers to stretch budgets geographically, potentially reducing location premiums for prime areas as buyers can now afford properties in previously unattainable postcodes. This requires surveyors to reassess traditional location adjustment percentages.

Buy-to-Let Investment Property Adjustments

Buy-to-let (BTL) properties require fundamentally different adjustment techniques when assessing the impact of mortgage rate cuts on 2026 property valuations. Investment properties are valued based on income generation potential and investment returns rather than purely on owner-occupier demand.

BTL-specific surveyor adjustments include:

💰 Yield Recalibration: As mortgage rates decline, the gap between rental yields and borrowing costs widens, improving cash flow for leveraged investors. A property generating 5% rental yield becomes significantly more attractive when mortgage rates drop from 6.5% to 5.5%, potentially supporting 3-5% valuation increases independent of owner-occupier market movements.

📊 Investment Return Modeling: Professional surveyors conducting commercial property valuations apply discounted cash flow analysis, with discount rates adjusted downward as borrowing costs decline, mechanically increasing net present values.

🔄 Investor Demand Surge Factors: Lower rates attract new BTL investors who were previously priced out of the market. Surveyors track investor inquiry volumes, BTL mortgage application data, and portfolio landlord activity to gauge demand intensity.

Comparative Adjustment Framework:

| Property Type | Rate Impact Sensitivity | Typical Adjustment Range | Primary Drivers |

|---|---|---|---|

| First-Time Buyer Homes | High | 2-4% | Affordability expansion, demand surge |

| Family Homes | Moderate | 1-2% | Stable demand, incremental improvement |

| Luxury Properties | Low | 0-1% | Cash buyers dominant, rate-insensitive |

| BTL Single Units | High | 3-5% | Yield improvement, investor returns |

| BTL Portfolios | Very High | 4-6% | Leverage benefits, institutional interest |

Geographic Variation in Rate Impact

The impact of mortgage rate cuts on 2026 property valuations varies significantly by location. Chartered surveyors in London face different market dynamics than those in regional markets.

Geographic adjustment considerations:

- London and Southeast: Higher average property prices mean rate reductions create larger absolute payment savings, but cash buyers represent a higher proportion of transactions, moderating rate sensitivity

- Regional Markets: Greater reliance on mortgage financing means rate reductions have more pronounced demand impacts, potentially requiring larger upward adjustments

- Commuter Zones: Areas within reasonable commuting distance to major employment centers see amplified benefits as lower rates enable buyers to afford larger properties in these locations

Chartered surveyors in areas like Hertfordshire, Oxfordshire, and Berkshire must carefully calibrate adjustments to reflect local market dynamics while incorporating broader rate-driven trends.

Market Dynamics and Supply-Demand Rebalancing in 2026

Inventory Unlocking and the Lock-In Effect

One of the most significant factors influencing the impact of mortgage rate cuts on 2026 property valuations is the gradual unlocking of housing inventory as rates decline. During 2023-2025, many homeowners with pandemic-era mortgages below 3% were effectively "locked in" to their current properties, unwilling to sell and take on new mortgages at 6-7%.

As rates decline toward 5.5-6% in 2026, this lock-in effect gradually diminishes, though it doesn't disappear entirely. Housing supply and demand are expected to balance out in 2026, with modest increases in for-sale inventories as lower mortgage rates incentivize homeowners to list properties [1].

Surveyor implications:

- Increasing Comparable Inventory: More recent sales data becomes available, improving the reliability of comparable sales analysis

- Reduced Scarcity Premiums: Markets that experienced severe inventory constraints in 2024-2025 may see scarcity premiums moderate as supply increases

- Transaction Volume Normalization: Higher transaction volumes provide better market evidence, though surveyors must distinguish between rate-driven demand and underlying market strength

Price Growth Expectations and Valuation Ceilings

Despite improving affordability from rate reductions, home prices are expected to grow only 1-2% in 2026 across major forecasts. Morgan Stanley predicts 2% appreciation, while Redfin and Zillow forecast approximately 1-1.2% growth, compared to roughly flat prices in 2025 [1][2][4].

This modest growth environment creates unique challenges for surveyors assessing the impact of mortgage rate cuts on 2026 property valuations:

📉 Price Resistance Indicators: Nearly 60% of houses sold in 2025 came with at least one price cut, indicating significant price resistance despite continued appreciation [6]. Surveyors must recognize that while demand may increase with lower rates, buyers remain price-sensitive.

⚖️ Offsetting Forces: The National Association of Home Builders chief economist notes that mortgage rate decreases will offset the modest home price growth, improving overall affordability [5]. This suggests valuations should reflect improved transaction feasibility rather than dramatic price appreciation.

🎯 Realistic Valuation Ranges: Professional surveyors provide valuation ranges rather than point estimates, acknowledging uncertainty in how rate benefits translate to actual transaction prices in a price-resistant market.

Monthly Payment Dynamics

A critical insight for 2026 is that monthly mortgage payment reductions are expected to occur for the first time since 2020 [5]. This represents a fundamental shift in market psychology and buyer behavior.

For practical illustration:

- £400,000 property at 6.5% rate: Monthly payment approximately £2,020

- £400,000 property at 5.5% rate: Monthly payment approximately £1,815

- Monthly savings: £205 (approximately 10% reduction)

This £205 monthly saving translates to roughly £2,460 annually, which over a typical 5-year ownership period represents £12,300 in reduced costs. Surveyors incorporate these affordability improvements into demand assessments and valuation adjustments.

Professional Surveyor Expertise and Valuation Standards in 2026

RICS Valuation Standards and Rate Environment Considerations

The Royal Institution of Chartered Surveyors (RICS) provides comprehensive valuation standards that RICS registered valuers must follow. In 2026, these standards take on heightened importance as surveyors navigate the impact of mortgage rate cuts on property valuations.

Key RICS principles applicable to rate-driven market changes:

✅ Market Value Definition: RICS defines market value as "the estimated amount for which an asset should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion."

This definition requires surveyors to assess what buyers can and will pay in current market conditions, directly incorporating affordability improvements from rate reductions.

✅ Basis of Value Transparency: Surveyors must clearly state the basis of valuation and any special assumptions, particularly important when rate environments are changing rapidly and future rate movements remain uncertain.

✅ Comparable Evidence Hierarchy: RICS standards prioritize recent, similar, and proximate comparable sales. In transitioning rate environments, surveyors must carefully document how they've adjusted older comparables to reflect current conditions.

Distinguishing Between Valuation Types

Different valuation purposes require different approaches to incorporating the impact of mortgage rate cuts on 2026 property valuations:

Mortgage Lending Valuations: Conservative approach focusing on sustainable long-term value rather than short-term rate-driven demand spikes. Lenders want assurance that property values will hold even if rates subsequently rise.

Purchase Valuations: More responsive to current market conditions and buyer demand, reflecting what properties can realistically achieve in current transactions. Homebuyer surveys typically incorporate more current market sentiment.

Investment Valuations: Heavily focused on income generation and returns, with lease extension valuations and shared ownership valuations requiring specialized adjustment techniques for rate changes.

Taxation Valuations: Capital gains tax valuations require specific date-of-valuation assessments, with rate environment at that specific point in time being critical.

Technology and Data Analytics in Modern Surveying

Professional surveyors in 2026 leverage advanced technology to better assess the impact of mortgage rate cuts on property valuations:

🖥️ Real-Time Market Data Platforms: Access to daily transaction data, mortgage application volumes, and buyer inquiry metrics enables more responsive valuations

📱 Automated Valuation Model (AVM) Integration: While AVMs alone cannot capture nuanced rate impacts, professional surveyors use them as starting points, then apply expert judgment and manual adjustments

🚁 Enhanced Property Assessment Tools: Drone surveys and digital measurement technologies improve property assessment accuracy, ensuring valuations reflect true property characteristics alongside market conditions

📊 Predictive Analytics: Machine learning models help identify leading indicators of how rate changes flow through to transaction prices in different market segments

Practical Application: Case Studies and Examples

Case Study 1: First-Time Buyer Property in Outer London

Property: 2-bedroom flat in Ealing, £425,000 asking price

Comparable Sales: Three similar properties sold 4-6 months ago at £410,000-£420,000 when mortgage rates averaged 6.4%

Current Environment: Rates have declined to 5.7%, expanding first-time buyer pool significantly

Surveyor Adjustments Applied:

- Time adjustment: +1.5% (£6,150-6,300) for improving market conditions

- Demand multiplier: +2% (£8,200-8,400) for increased buyer competition in first-time buyer segment

- Condition variation: -1% (£4,100-4,200) for slightly inferior condition versus best comparable

Adjusted Valuation Range: £420,000-£430,000

Conclusion: Current asking price of £425,000 sits appropriately within adjusted valuation range, reflecting improved affordability and demand from rate reductions.

Case Study 2: Buy-to-Let Investment Property

Property: 3-bedroom house in Kingston, £550,000, rental income £2,200/month

Investment Metrics at Different Rates:

| Mortgage Rate | Monthly Payment | Net Monthly Cash Flow | Gross Yield | Net Yield |

|---|---|---|---|---|

| 6.5% | £2,780 | -£580 | 4.8% | Negative |

| 5.5% | £2,500 | -£300 | 4.8% | Negative |

| 5.5% (80% LTV) | £2,000 | +£200 | 4.8% | 0.4% |

Surveyor Analysis: While gross yield remains constant at 4.8%, the improved cash flow position at lower rates makes the property significantly more attractive to leveraged investors. Comparable BTL sales from 6 months ago at £530,000-£540,000 require upward adjustment.

Adjustments Applied:

- Investment return improvement: +3% (£15,900-16,200) for enhanced cash flow potential

- Investor demand increase: +1.5% (£7,950-8,100) for growing BTL market activity

- Market conditions: +0.5% (£2,650-2,700) for general improvement

Adjusted Valuation Range: £556,000-£567,000

Case Study 3: Family Home in Commuter Belt

Property: 4-bedroom detached house in Hertfordshire, £750,000

Market Context: Strong commuter location, good schools, traditionally popular with families upgrading from London

Rate Impact Analysis: Lower rates enable London-based families to afford the move while maintaining acceptable monthly payments despite higher property prices

Surveyor Considerations:

- Comparable sales from 5 months ago averaged £735,000 when rates were 6.3%

- Current rates at 5.8% improve affordability by approximately £250/month

- Increased viewing activity and faster sales times indicate strengthening demand

Adjustments Applied:

- Time/market improvement: +1.5% (£11,025)

- Location premium maintenance: 0% (commuter premium stable)

- Property condition: +0.5% (£3,675) for recent improvements

Adjusted Valuation Range: £745,000-£760,000

Conclusion: Property well-positioned in current market, with rate reductions supporting traditional price premiums for quality family homes in commuter locations.

Challenges and Limitations in Rate-Driven Valuation Adjustments

Uncertainty in Rate Trajectory

One of the primary challenges surveyors face when assessing the impact of mortgage rate cuts on 2026 property valuations is uncertainty about future rate movements. While forecasts predict rates in the 5.5-6.3% range, Morgan Stanley specifically notes that rates are expected to rise again in the second half of 2026 [1].

This creates valuation dilemmas:

⚠️ Short-Term vs. Long-Term Value: Should valuations reflect peak affordability at the lowest point in the rate cycle, or more sustainable values accounting for potential rate increases?

⚠️ Buyer Behavior Uncertainty: Will buyers rush to purchase when rates hit lows, creating temporary demand spikes and price premiums that prove unsustainable?

⚠️ Market Timing Risks: Properties valued in Q2 2026 when rates are at 5.5% may face different market conditions by Q4 2026 if rates have risen back to 6.2%

Professional surveyors address these uncertainties through scenario analysis and valuation ranges rather than precise point estimates, clearly documenting assumptions about rate environments.

Data Lag and Comparable Sales Timing

Property transaction data inherently lags current market conditions. A sale that completes today may have had the price agreed 8-12 weeks ago, when rate environments were different. This data lag complicates the assessment of impact of mortgage rate cuts on 2026 property valuations.

Surveyor techniques to address data lag:

📅 Agreement Date vs. Completion Date Analysis: Tracking when prices were agreed rather than when sales completed provides more accurate market timing

📈 Leading Indicator Integration: Monitoring asking prices, offer acceptance rates, and time-on-market metrics that respond more quickly than completed sales data

🔍 Buyer Sentiment Surveys: Incorporating qualitative data about buyer confidence and urgency alongside quantitative transaction data

Segment-Specific Variation

Not all properties benefit equally from rate reductions. Luxury properties with prices above £2 million see limited impact, as these buyers often use cash or have minimal rate sensitivity. Conversely, entry-level properties see disproportionate demand increases.

This variation requires surveyors to develop segment-specific adjustment frameworks rather than applying uniform rate-impact adjustments across all property types. Valuation factors must be carefully calibrated to property characteristics and target buyer profiles.

Strategic Implications for Property Stakeholders

For Property Buyers

Understanding the impact of mortgage rate cuts on 2026 property valuations helps buyers make informed decisions:

✅ Timing Considerations: Buyers benefit from improved affordability but face increased competition from expanded buyer pools

✅ Negotiation Leverage: In markets where supply increases faster than demand, buyers may retain negotiation power despite rate improvements

✅ Professional Survey Importance: Obtaining a comprehensive Level 3 building survey becomes even more critical when paying rate-driven premium prices

✅ Long-Term Value Assessment: Buyers should focus on properties that offer value independent of temporary rate advantages, ensuring sustainable investment

For Property Sellers

Sellers navigating 2026 markets should understand:

📈 Realistic Pricing: While rate reductions improve affordability, the market remains price-sensitive, with 60% of 2025 sales requiring price reductions [6]

⏰ Market Timing: Sellers may benefit from listing when rates are at cyclical lows and buyer demand peaks

📋 Property Presentation: With increased competition from rising inventory, property condition and presentation become more critical differentiators

🎯 Professional Valuation: Obtaining an accurate valuation report helps set realistic asking prices that reflect current market conditions

For Property Investors

BTL and property investors face unique strategic considerations:

💼 Acquisition Timing: Lower rates create favorable acquisition windows, particularly for leveraged purchases where rate reductions directly improve returns

📊 Portfolio Revaluation: Existing portfolios may see valuation increases from improved yield spreads, potentially enabling refinancing or equity release

🏘️ Market Selection: Geographic markets with strong rental demand and limited supply offer best risk-adjusted returns in improving rate environments

⚖️ Leverage Optimization: Lower rates enable higher leverage while maintaining positive cash flow, though investors must consider refinancing risks if rates subsequently rise

Conclusion

The impact of mortgage rate cuts on 2026 property valuations represents one of the most significant market shifts in recent years, fundamentally altering affordability dynamics and buyer demand across UK property markets. As mortgage rates decline toward the 5.5-6.3% range, professional surveyors must employ sophisticated adjustment techniques that account for expanding buyer pools, improving investment returns, and changing market psychology.

Key conclusions include:

🎯 Rate reductions create measurable valuation impacts ranging from 1-2% for stable family homes to 4-6% for highly rate-sensitive segments like first-time buyer properties and buy-to-let investments

📊 Professional surveyor expertise becomes increasingly critical as standard valuation approaches struggle to capture the nuanced interplay between rate changes, demand dynamics, and sustainable property values

⚖️ Market rebalancing is underway with modest price growth of 1-2% offset by declining monthly payments, creating the first real affordability improvement since 2020

🏘️ Geographic and segment variation requires tailored approaches rather than uniform adjustment factors across all property types and locations

The surveyor adjustment techniques discussed—including time adjustments, demand multipliers, affordability recalibration, and yield-based investment analysis—provide frameworks for accurately assessing property values in this transitioning market. However, these techniques require professional judgment, local market knowledge, and careful documentation of assumptions.

Actionable Next Steps

For property buyers: Engage a qualified chartered surveyor to obtain comprehensive valuation and condition assessments before committing to purchases in this improving but competitive market.

For property sellers: Obtain professional valuation advice to set realistic asking prices that reflect current market conditions while capitalizing on improved buyer affordability.

For property investors: Conduct thorough investment analysis incorporating current rate environments and potential future rate movements, with professional valuation support for portfolio decisions.

For industry professionals: Continue developing expertise in rate-impact valuation adjustments through ongoing professional development and market monitoring.

The 2026 property market offers opportunities for well-informed participants who understand how mortgage rate cuts translate to property valuations through professional surveyor adjustment techniques. Success requires combining market knowledge, professional expertise, and realistic expectations about the pace and magnitude of market changes in this evolving landscape.

References

[1] Mortgage Rates Forecast 2025 2026 Will Mortgage Rates Go Down – https://www.morganstanley.com/insights/articles/mortgage-rates-forecast-2025-2026-will-mortgage-rates-go-down

[2] Housing Market Predictions 2026 – https://www.redfin.com/news/housing-market-predictions-2026/

[3] Mortgage Rates Forecast – https://www.bankrate.com/mortgages/mortgage-rates-forecast/

[4] 2026 Housing Predictions 35800 – https://www.zillow.com/research/2026-housing-predictions-35800/

[5] 2026 Real Estate Outlook What Leading Housing Economists Are Watching – https://www.nar.realtor/magazine/real-estate-news/2026-real-estate-outlook-what-leading-housing-economists-are-watching

[6] Will Home Prices Finally Fall In 2026 – https://awealthofcommonsense.com/2025/12/will-home-prices-finally-fall-in-2026/