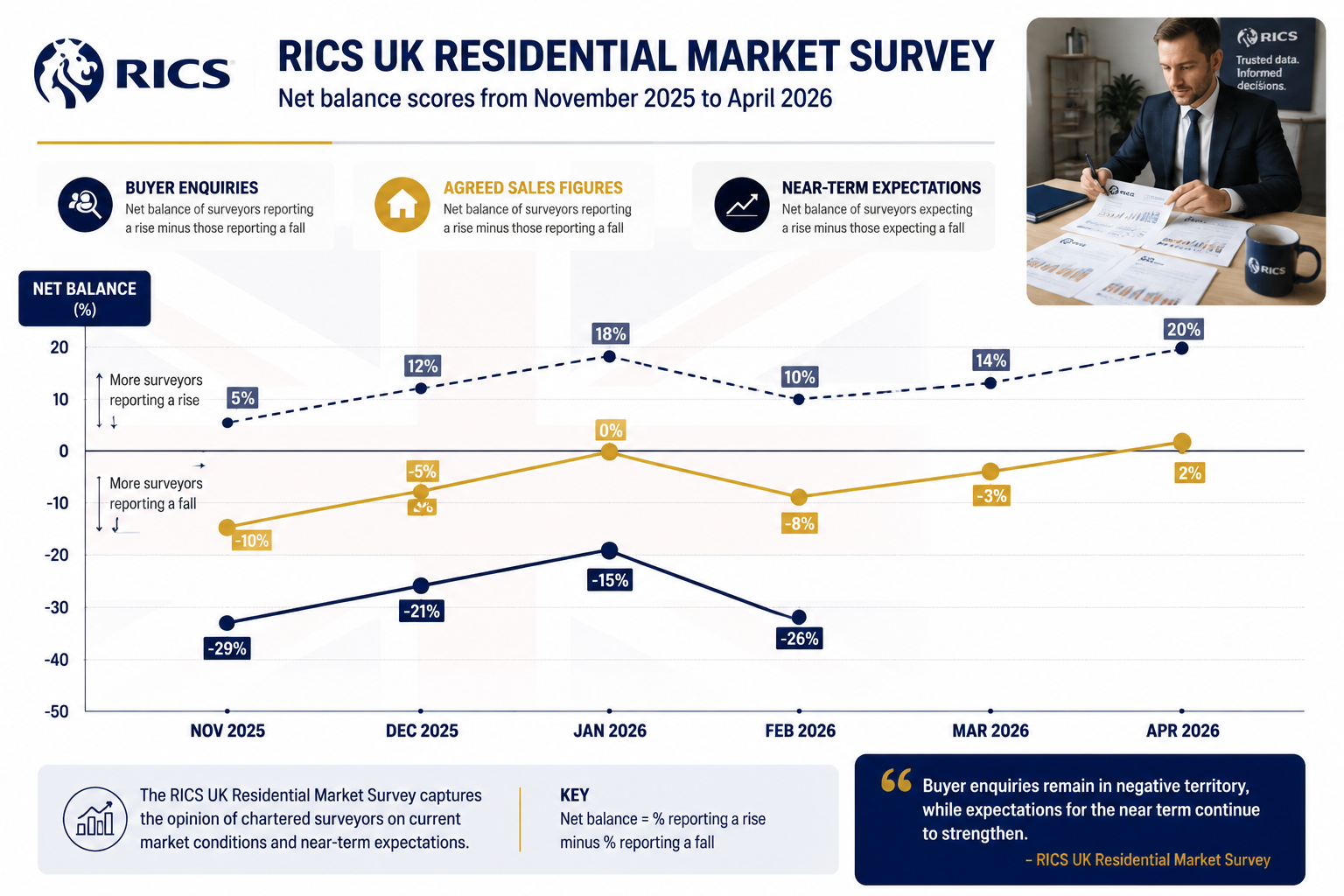

New buyer enquiries fell to a net balance of -26% in February 2026 — a sharp deterioration from -15% in January — confirming that the RICS Residential Survey Market Recovery in 2026 is far more fragile than the optimistic headlines of early January suggested [7]. For building surveyors and valuers navigating the next 12 months, that single data point tells a story: the recovery is real in parts, but it is uneven, reversible, and highly sensitive to forces largely outside the profession's control.

Understanding the RICS Residential Survey Market Recovery in 2026 — what is driving it, what is stalling it, and how it translates into practical decisions on survey instructions, inspection priorities, and valuation assumptions — is now essential reading for every RICS-regulated professional operating in the UK residential market.

Key Takeaways 📌

- January 2026 showed genuine but fragile improvement, with buyer enquiries and agreed sales reaching their least-negative readings in months — but February reversed much of that progress.

- Mortgage rates and geopolitical uncertainty are the two dominant forces shaping whether recovery momentum can be sustained through mid-2026.

- Survey instruction volumes remain below pre-2023 norms, but pockets of demand — particularly for older stock and leasehold properties — are creating targeted workload for surveyors.

- Valuers face heightened risk around comparable evidence quality, lender caution, and downward price adjustment pressure in certain regional markets.

- The next 12 months will reward surveyors who proactively adapt their inspection focus, client communication, and market commentary to reflect current conditions.

Reading the Data: What the RICS Sentiment Indicators Actually Mean for Surveyors

The January Optimism — and Why It Faded Fast

The January 2026 RICS UK Residential Market Survey offered the profession a brief moment of cautious optimism. New buyer enquiries improved to a net balance of -15%, up from -21% in December 2025 and -29% in November 2025 [1]. Agreed sales reached -9%, the least negative reading since June 2025 [1]. House price sentiment, measured over the prior three months, stood at -10%, recovering steadily from a low of -19% in October 2025 [1].

On 12-month price expectations, 43% of respondents anticipated higher prices over the year ahead as of January — the most positive outlook since February 2025 [1]. Reuters noted the survey as evidence of early recovery signs taking hold [2], and Morningstar flagged the data as consistent with a gradual market floor being established [4].

Then February arrived.

New buyer enquiries collapsed to -26% [7]. Agreed sales slipped further to -12% [7]. Near-term sales expectations fell to just -2%, described as "the weakest score since November last year" [7]. Most strikingly, 12-month sales expectations dropped from +35% in January to +17% in February — a dramatic erosion of surveyor confidence in the recovery narrative [7].

💬 "Whether this tentative improvement develops into sustained momentum will depend heavily on the trajectory of mortgage rates and broader macro confidence over the coming months."

— Simon Rubinsohn, RICS Chief Economist [1]

By March and April 2026, the RICS surveys confirmed the pattern: subdued conditions, higher mortgage rates, and geopolitical uncertainty were continuing to weigh on buyer demand and sales activity, with forward-looking indicators suggesting muted conditions were likely to persist [1].

What This Means for Survey Instruction Volumes

For building surveyors, instruction volumes track closely with agreed sales activity. When agreed sales net balances are running at -9% to -12%, the pipeline of survey commissions is thinner than it was during the 2021-2022 boom — but it is not absent.

Key insight: The surveyors who are busiest right now are not waiting for the market to recover uniformly. They are focusing on the segments where transactions are still happening:

- Older stock (pre-1960s properties) where buyers — often more experienced — still commission Level 3 Building Surveys regardless of market conditions

- Leasehold and shared ownership properties where lender requirements mandate formal valuations

- Probate and estate sales, which are transaction-driven rather than sentiment-driven

- Remortgage and refinancing activity, which actually increases when buyers delay purchases but still need to release equity

Inspection Priorities Shifting in a Subdued Market: What Surveyors Need to Prioritise

Why Market Conditions Change What You Look For

A recovering but fragile market changes the risk profile of every survey instruction. Buyers are more cautious. Lenders are more cautious. And sellers — aware that demand is soft — may have deferred maintenance, priced optimistically, or accepted offers from buyers whose financing is less secure than it appears.

This context means that the RICS Residential Survey Market Recovery in 2026 is not just a macroeconomic story. It directly affects what a competent surveyor should be emphasising in their reports.

🔍 Top Inspection Focus Areas for 2026

| Priority Area | Why It Matters Now | Survey Type Most Relevant |

|---|---|---|

| Damp and moisture ingress | Deferred maintenance during cost-of-living squeeze | Level 2 & Level 3 |

| Roof condition and coverings | Material costs rose sharply; owners delayed repairs | Level 3 Building Survey |

| Structural movement | Prolonged dry summers affecting clay soils | All survey types |

| Electrical installations | Ageing consumer units in older stock | Level 3 / Specific Defect |

| EPC and energy efficiency | Lender and regulatory pressure on ratings | All survey types |

| Cladding and fire safety | Ongoing remediation backlog | Level 2 & Level 3 |

For properties where a specific defect has already been flagged — perhaps by a mortgage valuer — a specific defect survey can provide targeted, cost-effective clarity for buyers and lenders alike.

The Energy Efficiency Dimension

Rising energy prices — themselves a product of the geopolitical uncertainty driving market weakness in early 2026 [3] — have made EPC ratings a live issue in valuations and surveys. Properties rated F or G are increasingly difficult to mortgage, and lenders are applying greater scrutiny to properties below band C. Surveyors should be flagging energy performance clearly, noting the likely cost of improvement, and cross-referencing with current lender criteria where relevant.

Older and Non-Standard Construction

In a subdued market, buyers of older properties are disproportionately represented among those still transacting. These buyers — often downsizers, cash buyers, or experienced investors — are more likely to commission a full Level 3 Building Survey and to act on its findings. Surveyors should be prepared for more complex instructions involving:

- Solid wall construction (no cavity, higher damp risk)

- Timber-framed properties (movement, beetle infestation, decay)

- Victorian and Edwardian terraces (party wall issues, original drainage)

- Properties with extensions or conversions (structural adequacy, building regulations compliance)

For buyers unsure which survey level is appropriate, a clear explanation of the difference between Level 2 and Level 3 surveys can help them make an informed decision — and helps surveyors manage scope expectations from the outset.

Valuation Strategy and Market Assumptions: Navigating the Next 12 Months

The Comparable Evidence Problem

Valuers operating in the current environment face a structural challenge: transaction volumes are low, which means comparable evidence is thin. When agreed sales net balances are running at -9% to -12% nationally [1][7], the number of recent, relevant comparables in many local markets is insufficient to support confident valuation conclusions.

This creates several practical risks:

- Stale comparables — transactions from 12-18 months ago may not reflect current market conditions

- Distorted comparables — the properties that are selling may be atypical (probate sales, distressed disposals, cash buyers accepting below-market prices)

- Lender pressure — with mortgage rates remaining elevated, lenders are applying tighter scrutiny to valuations and are more likely to challenge figures that appear optimistic

Price Expectations: Positive but Fragile

The January 2026 data showed 43% of RICS survey respondents expecting higher prices over the following 12 months [1] — a meaningful signal. But that optimism was already weakening by February, and the April survey confirmed subdued conditions persisting [1]. Valuers should treat 12-month price growth assumptions with caution, particularly in:

- High-value London markets where affordability constraints are most acute

- Commuter belt locations where hybrid working patterns continue to shift demand

- Leasehold flats where service charge inflation and cladding remediation costs are suppressing values

For leasehold properties specifically, a lease extension valuation may be required as part of the transaction process — and the current market environment makes accurate premium calculations more important than ever.

Regional Variation: Not All Markets Are Equal

The national RICS net balance figures mask significant regional divergence. Estate Agent Today noted in late 2025 that RICS had delayed its recovery forecast to spring 2026 [8] — and that delay has proven prescient. But "spring 2026" has not arrived uniformly:

- Northern England and Scotland have shown relatively more resilient transaction activity

- London and the South East face the sharpest affordability headwinds from elevated mortgage rates

- Coastal and rural markets that boomed post-pandemic are experiencing the sharpest corrections

Surveyors and valuers working across multiple regions — or those based in specific local markets — should be calibrating their assumptions to local evidence rather than relying solely on national RICS sentiment data.

Shared Ownership and Help-to-Buy Valuations

In a market where first-time buyers are squeezed by mortgage costs, shared ownership transactions remain a meaningful segment. RICS shared ownership valuations require careful attention to current market evidence, and the subdued conditions of early 2026 make it essential that valuers do not anchor to historic transaction prices that no longer reflect current buyer appetite.

What Building Surveyors and Valuers Should Watch in the Next 12 Months

The RICS Residential Survey Market Recovery in 2026 hinges on a small number of pivotal variables. Surveyors who monitor these closely will be better positioned to advise clients, calibrate their reports, and manage their own business planning.

🗓️ Key Watchpoints for H2 2026

1. Bank of England Base Rate Decisions

Every rate decision between now and December 2026 will directly affect mortgage availability and buyer confidence. A cut of 25-50 basis points could meaningfully improve the net balance scores seen in February and March. A hold — or worse, a rise — will extend the subdued conditions flagged in the April 2026 RICS survey [1].

2. Geopolitical Developments and Energy Prices

The RICS February 2026 survey explicitly cited renewed geopolitical concerns and rising oil and energy prices as intensifying inflationary pressures and keeping mortgage rates higher for longer [3]. Any de-escalation could improve consumer confidence rapidly.

3. Stamp Duty Threshold Changes

The temporary stamp duty relief that expired in March 2025 removed a significant demand stimulus. Any new government intervention — or the absence of it — will shape transaction volumes in H2 2026.

4. Lender Criteria and Product Availability

Lenders are quietly tightening criteria on certain property types (cladding-affected buildings, short leases, non-standard construction). Surveyors should stay current with lender requirements, as these directly affect whether a survey instruction converts into a completed transaction.

5. New Build Supply and Planning Reform

Government planning reform ambitions, if they translate into increased new build completions, will affect the second-hand market by providing alternative supply. This matters for valuers assessing existing stock in areas with significant new development pipelines.

Practical Steps for Surveyors Right Now

- ✅ Review your report templates to ensure condition ratings and commentary reflect current market context, not 2021-era assumptions

- ✅ Update your comparable evidence databases monthly rather than quarterly — in thin markets, even a few weeks can make a difference

- ✅ Communicate proactively with clients about the market context affecting their transaction — buyers who understand the environment make better decisions and generate fewer post-report disputes

- ✅ Consider your service mix — are you positioned to capture remortgage valuations, probate instructions, or shared ownership work during a period of subdued purchase activity?

- ✅ Stay current with RICS guidance — the profession's standards and guidance notes are updated to reflect market conditions, and compliance is non-negotiable

For surveyors who want a comprehensive framework for what to check and document, the ultimate house survey checklist provides a practical starting point that can be adapted to current market conditions.

Conclusion: Turning Market Intelligence into Professional Advantage

The RICS Residential Survey Market Recovery in 2026 is not a simple upward trajectory. It is a volatile, data-dependent process shaped by mortgage rates, geopolitical events, and regional demand patterns that can shift within a single monthly survey cycle. The January optimism, the February deterioration, and the April subdued outlook are not contradictions — they are the reality of a market finding its floor in difficult conditions.

For building surveyors and valuers, the practical response is clear:

- Calibrate your valuation assumptions to current, local comparable evidence — not national sentiment trends

- Sharpen your inspection focus on the defect categories most prevalent in the stock that is currently transacting

- Diversify your instruction mix to include segments less sensitive to purchase market sentiment

- Monitor the Bank of England, RICS monthly surveys, and lender criteria updates as your primary intelligence sources for the next 12 months

- Communicate market context clearly in your reports — clients making decisions in a fragile recovery need informed guidance, not boilerplate

The surveyors who will thrive in the next 12 months are not those waiting for a full recovery. They are those who have understood the current market well enough to serve their clients with precision and confidence right now.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Uk Housing Market Shows Early Signs Recovery Rics Survey Shows 2026 02 12 – https://www.reuters.com/world/uk/uk-housing-market-shows-early-signs-recovery-rics-survey-shows-2026-02-12/

[3] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[4] Uk Residential Housing Market Shows Signs Of Recovery – https://global.morningstar.com/en-gb/news/alliance-news/1770865507395385800/uk-residential-housing-market-shows-signs-of-recovery

[5] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[7] Buyer Demand Slips Amid Doubts For A Housing Market Recovery Rics – https://www.mortgagesolutions.co.uk/mortgage-news/2026/03/12/buyer-demand-slips-amid-doubts-for-a-housing-market-recovery-rics/

[8] Rics Housing Market Recovery Delayed Until Spring 2026 – https://www.estateagenttoday.co.uk/breaking-news/2025/12/rics-housing-market-recovery-delayed-until-spring-2026/

[9] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf