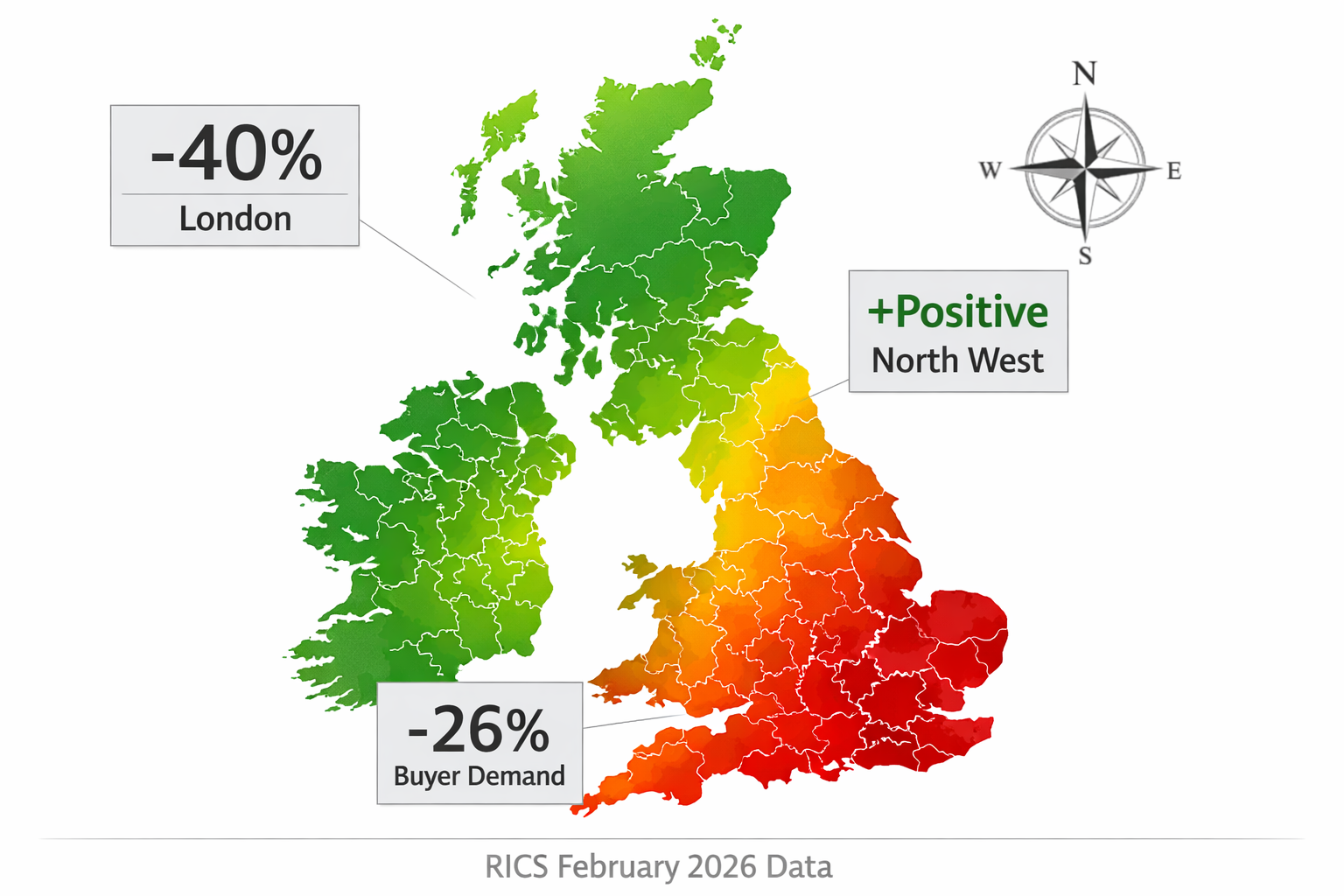

London's house price net balance crashed to -40% in February 2026 — the worst reading of any UK region — while Northern Ireland, Scotland, and the North West continued posting firmer price trends. That single data point from the RICS February 2026 UK Residential Market Survey tells a story that every buyer, seller, and building surveyor needs to understand right now. [1]

The Regional Valuation Divergences Post-RICS February 2026 Survey: Building Survey Tactics for London Stagnation vs Northern Recovery are not a temporary blip. They reflect a structural realignment of UK property markets driven by affordability ceilings, geopolitical uncertainty, and shifting demand patterns. For anyone commissioning or conducting a building survey in 2026, understanding these divergences is no longer optional — it is essential risk management. [4]

Key Takeaways 📌

- London recorded a -40% net balance for house prices in February 2026 — the sharpest downward pressure of any UK region.

- Northern regions are outperforming, with Northern Ireland, Scotland, and the North West showing resilience against national headwinds.

- Buyer demand fell sharply nationally to a net balance of -26%, driven by interest rate concerns and geopolitical instability.

- Building survey tactics must adapt to regional conditions — a London flat and a Manchester terrace carry very different risk profiles in 2026.

- 12-month London price expectations collapsed from +56% in January to just +7% in February, signalling a major confidence shift.

Understanding the RICS February 2026 Data: A Market Divided

The RICS February 2026 UK Residential Market Survey paints a picture of a market that is flat on the surface but deeply fractured underneath. [1]

The headline net balance for house prices registered -12% nationally — described by RICS as "broadly flat." But that national figure masks a dramatic North-South split that is reshaping how surveyors, lenders, and buyers should approach property transactions across different regions. [4]

The Numbers That Matter

| Region | Price Net Balance (Feb 2026) | Direction |

|---|---|---|

| London | -40% | ⬇️ Strong decline |

| South East | -24% | ⬇️ Moderate decline |

| East Anglia | -26% | ⬇️ Moderate decline |

| North West | Positive | ⬆️ Recovery |

| Scotland | Positive | ⬆️ Recovery |

| Northern Ireland | Positive | ⬆️ Recovery |

| National | -12% | ➡️ Broadly flat |

Source: RICS UK Residential Market Survey, February 2026 [4]

What Is Driving the Divergence?

Several forces are converging to create these regional valuation divergences:

- 🏦 Interest rate anxiety: Geopolitical instability — including Middle East conflict escalation and rising oil prices — is increasing the likelihood that mortgage rates will "remain higher for longer." [4] This hits high-value Southern markets hardest, where buyers are more leveraged.

- 💷 Affordability ceilings: London and the South East have simply run out of headroom. Average prices relative to incomes in these regions leave little room for further growth when borrowing costs remain elevated.

- 🏗️ Northern value proposition: Cities like Manchester, Leeds, and Liverpool offer comparatively strong rental yields and lower entry prices, attracting both owner-occupiers and investors who have retreated from London.

- 📉 Buyer demand collapse: New buyer enquiries nationally posted a net balance of -26% in February, down sharply from -15% in January. [1] London felt this most acutely.

"12-month price expectations in London dropped from +56% in January to just +7% in February 2026 — one of the most dramatic single-month collapses in surveyor confidence on record." [4]

Regional Valuation Divergences Post-RICS February 2026 Survey: What Building Surveyors Are Seeing on the Ground

The RICS data is not just an abstract market commentary. It has direct, practical implications for how building surveys should be scoped, priced, and interpreted depending on where a property sits on the UK map.

London: Surveying in a Stagnant Market

In a stagnating market, the risk profile of a property purchase changes fundamentally. When prices are rising, minor defects are often absorbed by capital growth. When prices are flat or falling, every defect becomes a negotiating lever — and every overlooked issue becomes a potential financial trap.

Building surveyors operating in London in 2026 are adapting their approach in several key ways:

1. Heightened focus on latent defects

In a flat market, buyers cannot rely on future price appreciation to offset repair costs. Surveyors are spending more time investigating concealed issues — particularly in London's ageing Victorian and Edwardian housing stock. Damp, timber decay, and aging drainage systems are priority inspection areas. A damp survey commissioned alongside a full building survey is increasingly common practice.

2. Stricter valuation cross-referencing

With London's 12-month price expectations having collapsed from +56% to just +7% in a single month [4], surveyors are being more conservative in their comparable evidence selection. Properties that appeared well-priced in January 2026 may now be overpriced relative to revised market expectations.

3. Subsidence and structural risk assessment

London's clay soils make subsidence surveys particularly relevant, especially as prolonged dry periods stress foundations. In a falling market, a property with subsidence risk carries compounded downside: the defect cost plus the market decline.

4. Leasehold and service charge scrutiny

London's predominantly leasehold flat market adds another layer of complexity. Surveyors are flagging service charge escalation risks and major works liabilities with greater urgency — costs that buyers in a rising market might have accepted are now deal-breakers.

For buyers purchasing in specific London areas, working with locally experienced professionals matters enormously. Chartered surveyors in Central London and chartered surveyors in South East London bring area-specific knowledge of typical defect patterns and local comparable evidence that a generalist surveyor may lack.

Northern Recovery Zones: Surveying in an Ascending Market

The Northern recovery presents a different but equally important set of survey challenges. In markets where prices are rising, buyers face the opposite problem: the fear of missing out can override due diligence.

Key tactical adjustments for Northern market surveys include:

1. Rapid turnaround without cutting corners

In competitive Northern markets, buyers face pressure to exchange quickly. Surveyors must balance speed with thoroughness. Knowing how long a Level 2 survey takes helps buyers plan realistic timelines without sacrificing quality.

2. Non-standard construction awareness

Many Northern towns contain significant stocks of non-standard construction properties — including steel-framed, concrete panel, and timber-framed homes — that require specialist assessment. A standard visual inspection is insufficient for these property types.

3. Avoiding overpayment in recovery momentum

Even in recovering markets, individual properties can be overpriced relative to their condition. A full RICS building survey provides the evidence base to negotiate effectively — or walk away from a property whose condition does not justify the asking price.

4. Rental market dynamics

With landlord instructions nationally at a firmly negative net balance of -27% and 20% of survey participants expecting rents to rise [1], buy-to-let investors are active in Northern recovery zones. For these buyers, a stock condition survey can provide a comprehensive baseline for portfolio management.

Practical Building Survey Tactics for Navigating Regional Valuation Divergences Post-RICS February 2026 Survey

Whether buying in a stagnant London market or a recovering Northern city, the following tactical framework helps buyers and their advisors make better decisions in 2026's divergent landscape.

🔍 Tactic 1: Match Survey Level to Market Risk

Not all surveys are equal, and not all markets require the same level of scrutiny. Use this guide:

| Market Condition | Recommended Survey Level | Rationale |

|---|---|---|

| London flat market (high-value, ageing stock) | Level 3 Full Building Survey | Maximum defect identification in a no-margin-for-error market |

| Northern recovery (older terraced stock) | Level 3 Full Building Survey | Non-standard construction and older fabric require depth |

| Northern recovery (modern post-2000 property) | Level 2 RICS Home Survey | Lower risk profile, faster turnaround |

| Any market (new build) | Snagging survey + Level 2 | Builder defects require specialist identification |

Understanding the differences between survey types is the starting point for every property purchase decision.

🔍 Tactic 2: Use Survey Findings as a Valuation Tool

In a divergent market, a building survey is not just a safety check — it is a valuation instrument. Survey findings can and should be used to:

- Renegotiate the purchase price based on costed remedial works

- Identify value traps — properties priced as if defect-free when they are not

- Support mortgage applications where lenders require evidence of structural integrity

In London's stagnant market, where agreed sales posted a net balance of -12% in February [1], sellers are more willing to negotiate. A detailed survey report provides the factual basis for those conversations.

🔍 Tactic 3: Understand Regional Valuation Factors

Valuation is not a single national formula. The factors that influence property valuation vary significantly by region. In London, proximity to transport links, leasehold terms, and service charge history carry disproportionate weight. In Northern markets, proximity to employment centres, school catchment areas, and regeneration pipeline matter more.

Buyers should commission a RICS-specific defect survey when a particular concern — such as suspected subsidence, damp, or structural movement — needs targeted investigation before committing to a purchase.

🔍 Tactic 4: Factor in the Macro Environment

Near-term price expectations nationally fell to -18% in February from -6% in January [1] — a significant deterioration. This means:

- Buyers in London should not assume a floor has been reached. Further price softening is possible, making thorough due diligence even more critical.

- Buyers in Northern recovery zones should not assume the recovery is immune to national headwinds. Geopolitical uncertainty and elevated mortgage rates affect all markets eventually.

- Sellers everywhere should price realistically and present properties in the best possible condition to avoid extended time on market.

🔍 Tactic 5: Do Not Overlook the Rental Market

With landlord instructions at -27% nationally [1], rental supply is tightening even as tenant demand remains stable. For investors, this creates opportunity — but only where the underlying property condition supports the rental yield. A dilapidations survey is essential for any investor acquiring tenanted or previously tenanted property to establish the true condition baseline and avoid inheriting costly repair liabilities.

Choosing the Right Surveyor for a Divergent Market

The regional valuation divergences post-RICS February 2026 survey demand locally knowledgeable professionals. A surveyor who primarily works in Central London may not be best placed to assess a terrace in Salford — and vice versa.

Key selection criteria for 2026:

✅ RICS accreditation — Non-negotiable. Only RICS-regulated surveyors provide reports that lenders and courts will accept.

✅ Local market experience — Ask specifically about recent comparable transactions and typical defect patterns in the target area.

✅ Clear reporting — Survey reports should clearly distinguish between urgent defects, significant issues, and advisory items, with cost guidance where possible.

✅ Independence — Avoid surveyors recommended exclusively by estate agents. Independence ensures objectivity.

For London buyers, chartered surveyors in West London and chartered surveyors in South West London offer the local expertise needed to navigate the capital's complex and currently pressured market.

Conclusion: Actionable Next Steps for Buyers and Surveyors in 2026

The RICS February 2026 data has delivered a clear verdict: the UK property market is not one market — it is several, moving in different directions simultaneously. Regional valuation divergences post-RICS February 2026 survey are not a footnote; they are the defining feature of the current landscape.

Here are the actionable next steps for anyone involved in a property transaction right now:

-

Commission the right survey level for your specific market and property type. Do not default to the cheapest option in a market where defect costs can exceed the price saving.

-

Use survey findings actively in price negotiations — especially in London's stagnant market where sellers have reduced leverage.

-

Engage a locally experienced RICS-accredited surveyor who understands the specific valuation dynamics of the target region.

-

Factor in the macro environment — elevated mortgage rates, geopolitical uncertainty, and softening near-term expectations mean due diligence is more important than ever.

-

Do not conflate national headlines with local reality — a -12% national net balance tells you almost nothing about what is happening on a specific street in Manchester or Mayfair.

The divergence between London stagnation and Northern recovery is an opportunity for informed buyers and a trap for the unprepared. The right building survey, conducted by the right professional, is the tool that separates the two.

References

[1] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[2] Valuation Impacts Of February 2026 RICS Survey Strategies For Regional Price Divergence In UK Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets

[3] UK Residential Market Survey February 2026 – https://www.navah-consulting.co.uk/news/uk-residential-market-survey-february-2026

[4] UK Residential Market Survey February 2026 (PDF) – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[5] UK Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf

[6] Regional Valuation Divergences In 2026 Recovery RICS Tactics For North South Price Shifts In Building Surveys – https://nottinghillsurveyors.com/blog/regional-valuation-divergences-in-2026-recovery-rics-tactics-for-north-south-price-shifts-in-building-surveys