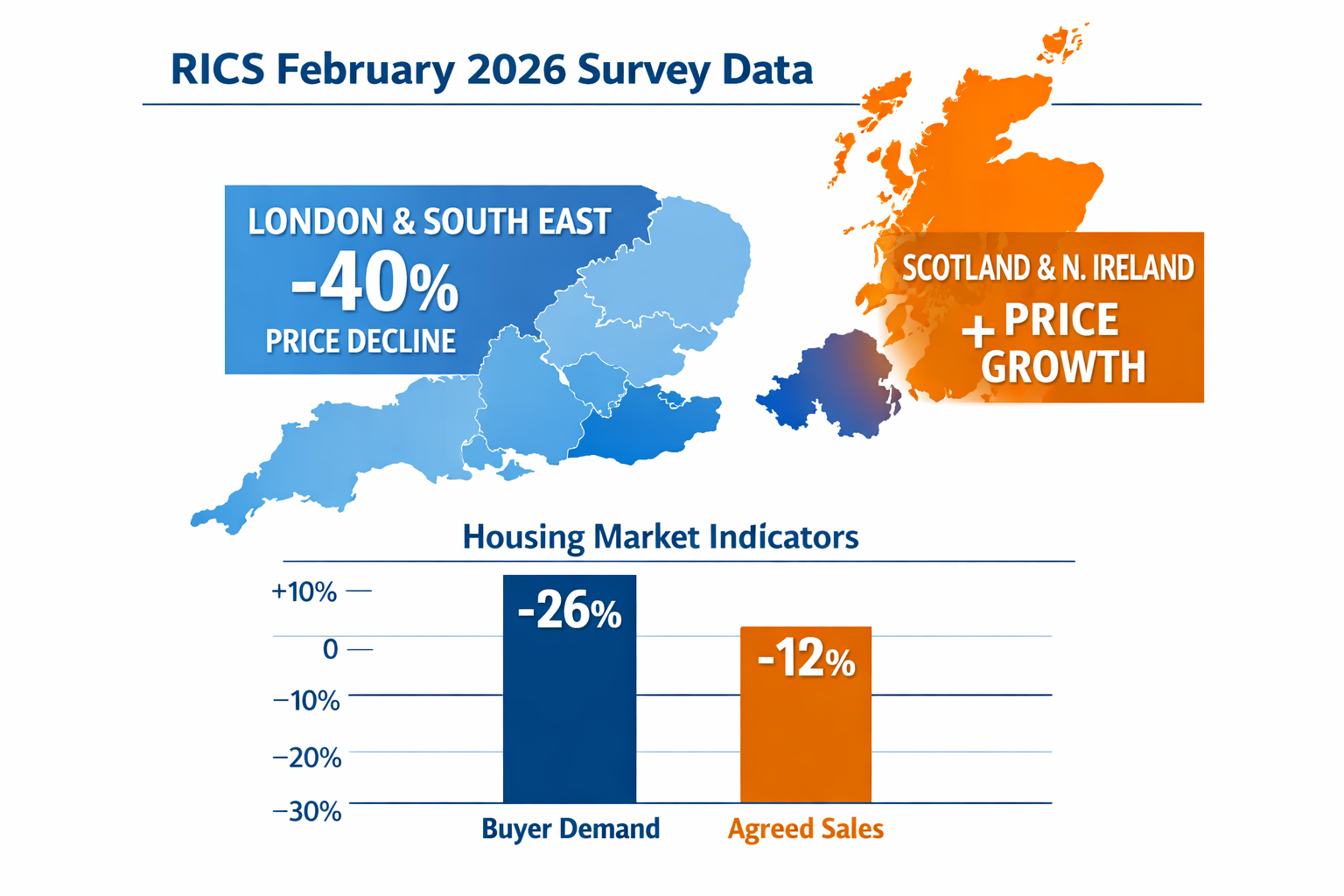

Buyer enquiries across the UK residential market collapsed to a net balance of -26% in February 2026 — the sharpest single-month deterioration since late 2025 — forcing surveyors and valuers to fundamentally reassess how they price property in a market defined by hesitation rather than momentum. The RICS February 2026 UK Residential Market Survey paints a picture of a housing sector caught between stubborn interest rate pessimism, geopolitical uncertainty, and pronounced regional divergence. Understanding the valuation adjustments for the cautious Spring 2026 housing market is no longer optional for professionals; it is a core competency [1][2].

This article unpacks the RICS February data in detail, examines what regional price flatness means for valuation methodology, and provides actionable strategies for surveyors, buyers, sellers, and investors navigating this subdued environment.

Key Takeaways 📌

- Buyer demand fell sharply to -26% net balance in February 2026, down from -15% in January, signalling a meaningful cooling of purchaser activity [1].

- National house prices are broadly flat at -12% net balance, but regional divergence is stark — London sits at -40% while Northern Ireland and Scotland trend upward [2].

- Short-term price expectations weakened to -18%, yet twelve-month expectations remain positive at +33%, suggesting the market correction may be temporary [3].

- Rental supply is tightening, with landlord instructions at -27% and rental price expectations rising to +20%, creating a bifurcated market between ownership and renting [1].

- Valuation professionals must adopt more granular, data-driven adjustment models that account for regional divergence, interest rate sensitivity, and subdued transaction volumes.

Decoding the RICS February 2026 Data: What the Numbers Really Mean

The RICS UK Residential Market Survey is one of the most closely watched barometers of sentiment in the British property sector. The February 2026 edition delivered a cluster of readings that, taken together, describe a market in a holding pattern rather than freefall — but one that demands careful recalibration from valuation professionals.

Buyer Demand and Agreed Sales

The headline buyer enquiries net balance of -26% in February represents a significant deterioration from -15% in January [1]. This is not merely a seasonal blip. Surveyors across multiple regions cited persistent concerns about the trajectory of interest rates, with many buyers choosing to delay commitments until greater clarity emerges on Bank of England policy [3].

Agreed sales, meanwhile, registered a net balance of -12%, marginally weaker than January's -9%, though notably less negative than the readings recorded across much of the second half of 2025 [2]. This distinction matters for valuers: while fewer deals are being struck, the pipeline has not collapsed entirely.

💬 "Near-term sales expectations posted the weakest reading since November 2025 at -2% net balance — a signal that surveyor pessimism over the immediate three-month outlook is hardening." [3]

Twelve-month sales expectations, however, remain moderately positive at +17% net balance — though this is a notable retreat from the +35% recorded in the previous survey [4]. The implication is clear: professionals broadly believe the market will recover, but the timeline has been pushed back.

New Instructions and Market Appraisals

New instructions (fresh listings entering the market) held broadly stable at +2% net balance, suggesting that sellers are not flooding the market in panic [1][2]. Market appraisals posted -5% net balance, pointing to a steady but uninspired pipeline of new stock [1]. For valuers, this relative stability in supply is a useful anchor — comparable evidence is available, even if transaction volumes are subdued.

Regional Price Flatness and the Valuation Adjustments for Cautious Spring 2026 Housing Market

Perhaps the most operationally significant finding in the RICS February 2026 survey is the pronounced regional divergence in price trends. National headline prices sit at a net balance of -12% — broadly flat to marginally negative — but this average obscures enormous variation beneath the surface [1][2].

The Regional Breakdown 🗺️

| Region | Price Net Balance | Direction |

|---|---|---|

| London | -40% | ⬇️ Significant downward pressure |

| East Anglia | -26% | ⬇️ Moderate downward pressure |

| South East | -24% | ⬇️ Moderate downward pressure |

| National Average | -12% | ➡️ Broadly flat |

| North West England | Positive | ⬆️ Upward trend |

| Scotland | Positive | ⬆️ Upward trend |

| Northern Ireland | Positive | ⬆️ Strongest upward trend |

Source: RICS UK Residential Market Survey, February 2026 [1][3]

This divergence has direct implications for how RICS valuations are conducted. A valuer applying a uniform national adjustment to comparable evidence risks producing a figure that is materially misleading — either over-stating value in London and the South East, or under-stating it in Northern Ireland and Scotland.

London: The Sharpest Adjustment Required

London's net balance of -40% is the steepest downward reading of any UK region and demands particular attention [1]. Critically, London's twelve-month price expectations have cooled dramatically — from +56% in January to just +7% in February [3]. This is not a rounding error; it represents a fundamental shift in surveyor confidence about the capital's near-term trajectory.

For professionals conducting a Red Book valuation in London, the February data reinforces the need to apply meaningful downward adjustments when using comparables from late 2025 or early 2026, particularly in markets such as prime central London where affordability constraints are most acute.

Short-Term vs. Long-Term Price Expectations

Short-term (three-month) price expectations weakened substantially to -18% net balance in February, down sharply from -6% in January [3]. This is the metric that should most directly influence how valuers treat time adjustments on comparable evidence.

Twelve-month price expectations remain positive at +33% net balance — but even this has moderated from +43% in January [1][3]. The message for valuers: apply caution to short-term adjustments, but avoid over-correcting in a way that suppresses values below their medium-term equilibrium.

Understanding the full scope of RICS reinstatement cost valuation and related methodologies becomes especially important when market signals are mixed and time-sensitive adjustments carry greater weight.

Practical Valuation Adjustment Strategies for Spring 2026

The valuation adjustments for the cautious Spring 2026 housing market identified through RICS February insights require surveyors to move beyond standard comparable analysis. The following strategies reflect best practice in a subdued, regionally fragmented market.

1. Apply Granular Time Adjustments to Comparable Evidence

With short-term price expectations at -18% nationally and London cooling sharply, comparables from even three to six months ago may overstate current market value. Surveyors should:

- Weight recent evidence more heavily, particularly transactions completed in January–February 2026.

- Apply explicit downward time adjustments in London, East Anglia, and the South East where price pressure is most acute.

- Document adjustment rationale clearly in valuation reports, referencing the RICS February survey data as supporting evidence [2].

2. Increase Reliance on Active Market Evidence

With agreed sales at -12% net balance and transaction volumes subdued, the pool of truly comparable evidence is smaller than in a buoyant market [2]. This makes it essential to:

- Broaden the geographic search radius for comparables while applying appropriate location adjustments.

- Use asking price data alongside achieved prices, noting the spread between the two as an indicator of negotiation pressure.

- Cross-reference with RICS building surveys findings where condition-related adjustments are required — a property with significant defects in a flat market faces compounded downward pressure.

3. Adopt a Cautious Approach to Special Assumptions

In a market where buyer demand has fallen to -26% and near-term sales expectations are negative, special assumptions about marketing periods or buyer appetite should be treated conservatively [1][3]. Surveyors should:

- Extend assumed marketing periods in London and the South East.

- Reflect the reduced pool of active buyers in any forced sale or restricted marketing scenario.

- Consider the impact of interest rate sensitivity on the buyer pool, particularly for higher-value properties.

4. Differentiate by Property Type and Tenure

The rental market data adds another layer of complexity. Landlord instructions are deeply negative at -27%, while tenant demand holds stable at +2% and rental price expectations have turned positive at +20% [1]. For investment property valuations, this supply-demand imbalance in the rental sector may support yields even where capital values are flat.

Professionals handling Help to Buy valuations or Right to Buy valuations need to be especially precise — these schemes involve statutory frameworks where an incorrect valuation carries legal and financial consequences for all parties.

5. Scrutinise Non-Standard Properties More Carefully

In a cautious market, buyers become more selective. Properties with non-standard construction, significant defects, or unusual characteristics face greater price resistance than in a rising market. A specific defect survey can help quantify the cost of remediation, providing a defensible basis for downward adjustments in the valuation report.

💬 "In flat or falling markets, the margin between a well-supported valuation and an unsupported one widens considerably — and so does the professional liability exposure for surveyors who fail to reflect current conditions."

6. Communicate Uncertainty Transparently

The RICS February 2026 data reflects a market in genuine flux. Twelve-month expectations remain positive, but the speed at which London's outlook shifted — from +56% to +7% in a single month — underlines how rapidly conditions can change [3][4]. Valuation reports issued in Spring 2026 should:

- Include explicit references to market conditions at the date of valuation.

- Note the sensitivity of the valuation to changes in interest rates or buyer demand.

- Recommend review if the property is not transacted within a defined period (typically three months in current conditions).

The Rental Market Dimension: A Parallel Pressure Point

While the ownership market navigates buyer hesitancy, the rental sector is experiencing its own form of stress. The combination of stable tenant demand (+2%) and deeply negative landlord instructions (-27%) points to a structural supply shortage that is likely to intensify rental price growth [1].

For valuers assessing investment properties or undertaking non-domicile tax valuations for overseas landlords, this dynamic is material. Rental income projections used in investment valuations should reflect the positive +20% rental price expectation rather than assuming static income streams.

The disconnect between the ownership and rental markets also has broader implications for housing policy and affordability — but from a pure valuation standpoint, it creates a bifurcated evidence base that requires careful handling.

What Buyers, Sellers, and Investors Should Do Now

The RICS February 2026 data is not a signal to panic — but it is a clear prompt to act with greater diligence. Here is what each stakeholder group should prioritise:

🏠 For Buyers

- Commission an independent survey before proceeding. In a flat market with subdued demand, sellers may be less willing to reduce prices post-survey, making pre-offer due diligence more valuable. See our guide on understanding the importance of a survey and home report.

- Negotiate on the basis of current market evidence, not 2025 peak comparables.

- Factor in interest rate risk when stress-testing affordability.

🏡 For Sellers

- Price realistically from the outset. With buyer demand at -26% and near-term expectations negative, overpriced properties will simply sit on the market [1][3].

- Obtain a current RICS valuation to ensure the asking price reflects February 2026 conditions rather than last year's sentiment.

- Consider the regional context carefully — a London seller faces a very different market than one in Northern Ireland or Scotland.

💼 For Investors

- Assess rental yield potential alongside capital value. The rental supply shortage and positive rental price expectations create opportunities even where capital appreciation is muted [1].

- Conduct thorough due diligence on condition. In a buyer's market, condition-related defects carry greater weight in price negotiations.

Conclusion: Navigating Valuation in a Cautious Spring Market

The valuation adjustments for the cautious Spring 2026 housing market demanded by the RICS February insights are not cosmetic tweaks — they represent a substantive recalibration of how property is priced in a period of genuine uncertainty. Buyer demand at -26%, London prices under severe pressure at -40%, and near-term expectations at their weakest since November 2025 collectively define a market that rewards precision and punishes complacency [1][2][3].

The encouraging counterpoint is that twelve-month sales and price expectations remain positive, suggesting the current softness is cyclical rather than structural. The professionals and market participants who use this window to sharpen their analytical frameworks — applying granular time adjustments, differentiating by region, and communicating uncertainty transparently — will be best positioned when conditions improve.

✅ Actionable Next Steps

- Commission a current-date RICS valuation if buying, selling, or refinancing in 2026 — do not rely on valuations from 2025.

- Request a detailed comparable analysis from your surveyor that explicitly references the February 2026 RICS data.

- Explore the full range of survey options to understand property condition before committing — compare options at our survey comparison guide.

- Speak to a chartered surveyor about regional adjustment methodology if your property is in London, East Anglia, or the South East.

- Review investment property income assumptions in light of the rental market data, particularly the +20% rental price expectation.

References

[1] Buyer Demand Slips Amid Doubts For A Housing Market Recovery Rics – https://www.mortgagesolutions.co.uk/mortgage-news/2026/03/12/buyer-demand-slips-amid-doubts-for-a-housing-market-recovery-rics/

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] Buyer Demand Dips Amid Interest Rate Pessimism Rics Finds – https://todaysconveyancer.co.uk/buyer-demand-dips-amid-interest-rate-pessimism-rics-finds/

[4] Uk Rics Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[5] Valuation Challenges In Weak Buyer Demand Rics February 2026 Survey Analysis And Surveyor Strategies – https://nottinghillsurveyors.com/blog/valuation-challenges-in-weak-buyer-demand-rics-february-2026-survey-analysis-and-surveyor-strategies