Recent legislative action in March 2026 has set the stage for transformative changes in how property transactions unfold across the housing market. The 21st Century Road to Housing Act, which passed the U.S. Senate on March 13, 2026, introduces measures designed to streamline housing construction and regulate institutional investment[1]. While the bill's specific provisions continue to evolve, the broader regulatory momentum toward upfront condition surveys represents a fundamental shift in how buyers, sellers, and surveyors approach property valuations. Understanding the valuation impacts of government homebuying reforms: upfront condition survey mandates and their effect on 2026 transaction workflows has become essential for all stakeholders navigating today's property market.

The traditional property transaction model—where surveys occur late in the buying process—has long been criticized for creating delays, unexpected costs, and deal failures. The emerging regulatory framework aims to address these inefficiencies by requiring comprehensive property condition assessments earlier in the sales process. This shift promises to reshape surveyor workflows, accelerate transaction timelines, and fundamentally alter how properties are valued and marketed.

Key Takeaways

- 🏠 Upfront survey mandates are shifting condition assessments to the beginning of property transactions, creating earlier demand for professional surveying services

- 📊 Valuation accuracy improves when comprehensive condition data is available before offers are made, reducing post-inspection price renegotiations

- ⚡ Transaction timelines accelerate as upfront surveys eliminate the traditional delay between offer acceptance and condition discovery

- 💼 Surveyor workflows are evolving to accommodate seller-commissioned reports that serve multiple potential buyers

- 🎯 Risk reduction benefits both buyers and sellers by establishing transparent property conditions before negotiations begin

Understanding the 2026 Regulatory Landscape for Property Transactions

The housing market in 2026 faces unprecedented pressure from multiple directions. Affordability concerns have reached critical levels, with existing home sales showing modest recovery—HUD reported a 5% increase in December 2025, marking a three-year high[6]. However, persistent challenges around transaction efficiency, buyer confidence, and market transparency have prompted policymakers to explore structural reforms.

The Legislative Framework Driving Change

The 21st Century Road to Housing Act represents the most significant housing legislation in recent years, focusing on increasing construction capacity and regulating large institutional investors[1]. While the bill's primary objectives center on housing supply, the regulatory environment it creates has catalyzed broader discussions about transaction efficiency and consumer protection.

Housing policy experts predict that 2026 will see continued bipartisan efforts to address affordability through various mechanisms, including YIMBY (Yes In My Backyard) measures and expanded manufactured housing options[2]. These initiatives create a policy environment favorable to reforms that reduce transaction friction and increase market transparency.

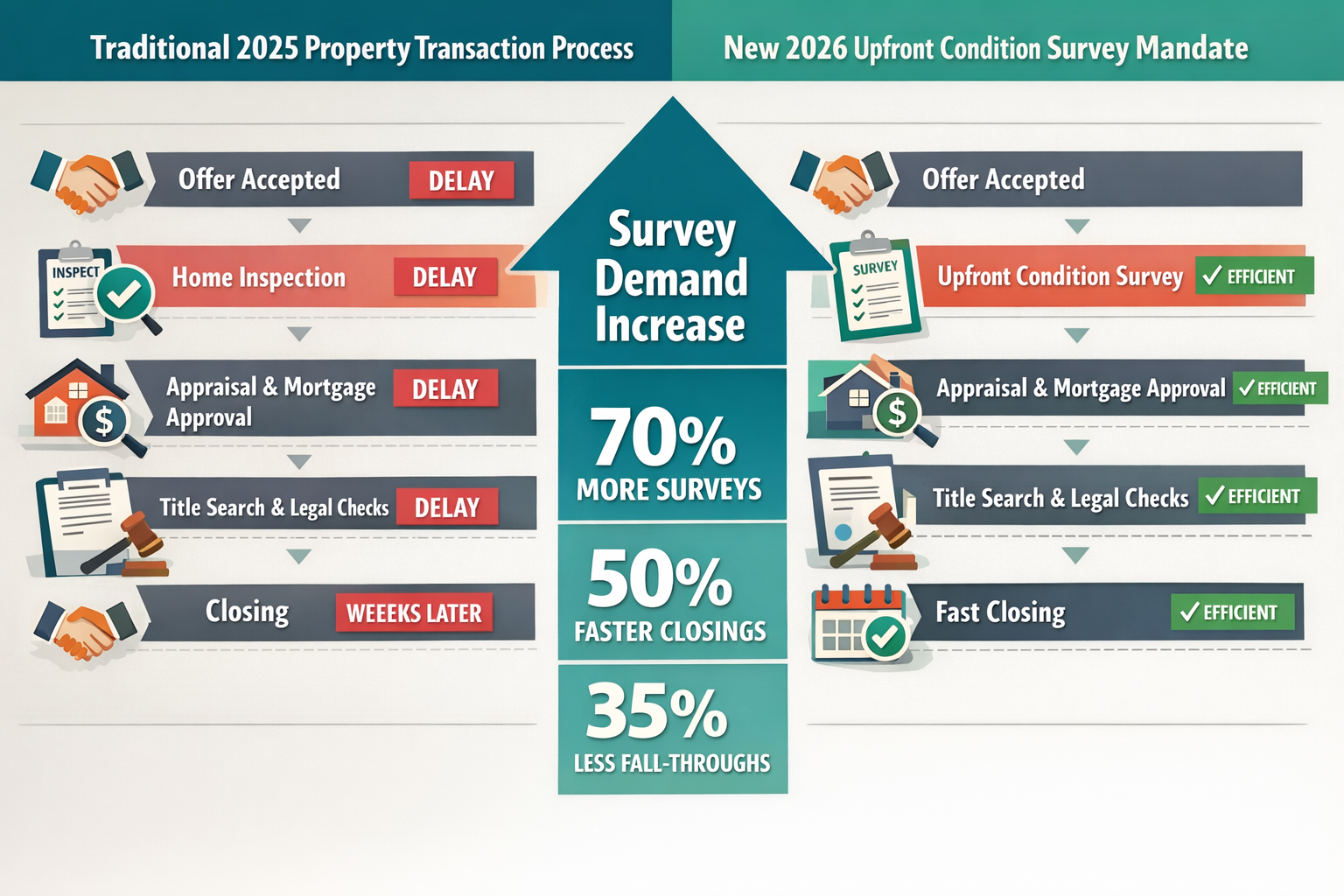

Why Upfront Condition Surveys Matter

Traditional property transactions follow a sequential pattern: marketing, viewing, offer, acceptance, then survey. This approach creates several problems:

- Late-stage surprises: Serious defects discovered after offers are accepted lead to renegotiations or deal collapse

- Wasted resources: Buyers invest in legal fees and survey costs for properties with undisclosed issues

- Market inefficiency: Properties cycle through multiple failed transactions before accurate pricing is established

- Information asymmetry: Sellers know more about property conditions than buyers, creating trust deficits

Upfront condition survey mandates address these issues by requiring comprehensive property assessments before marketing begins. This approach, already implemented in some international markets, provides transparency that benefits all parties.

Valuation Impacts of Government Homebuying Reforms on Property Assessment Practices

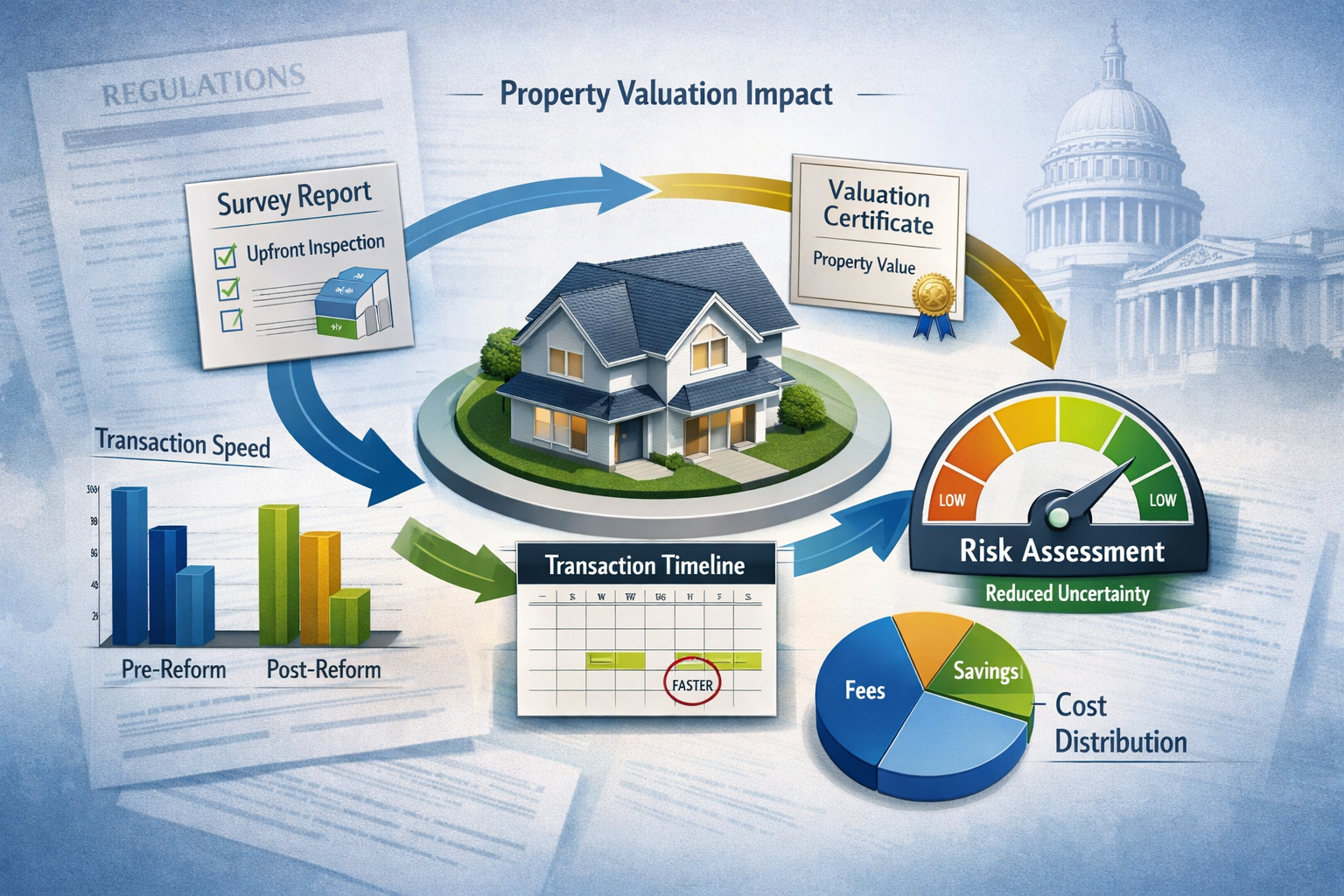

The shift toward mandatory upfront surveys creates profound implications for how properties are valued. When comprehensive property condition data becomes available before offers are submitted, the entire valuation paradigm changes.

Enhanced Valuation Accuracy Through Comprehensive Data

Property valuations traditionally rely on comparable sales data, location factors, and visible property characteristics. However, hidden defects—structural issues, damp problems, electrical deficiencies—often remain unknown until after valuation. This creates a disconnect between assessed value and true market value.

Upfront condition surveys bridge this gap by providing:

- Detailed defect documentation: Comprehensive reports identify all material issues affecting property value

- Repair cost estimates: Quantified remediation costs allow precise valuation adjustments

- Condition-adjusted comparables: Properties can be compared on a like-for-like condition basis

- Risk-weighted valuations: Known issues reduce uncertainty premiums in valuation calculations

For buyers seeking Level 3 building surveys, upfront availability means decisions can be made with complete information from the outset.

Market Pricing Efficiency and Transparency

When condition surveys are completed before marketing, asking prices more accurately reflect true property value. Sellers must confront repair needs and adjust expectations accordingly, while buyers can make informed offers without fear of post-survey surprises.

This transparency creates several market benefits:

| Traditional Approach | Upfront Survey Approach |

|---|---|

| Asking prices often aspirational | Asking prices condition-adjusted |

| Multiple renegotiations common | Initial offers more accurate |

| 20-30% of sales fall through | Reduced transaction failure rates |

| Valuation surprises frequent | Condition risks known upfront |

| Buyer bears survey cost risk | Survey cost integrated into marketing |

The RICS Home Survey standards provide the framework for these comprehensive assessments, ensuring consistency and professional rigor across all property types.

Impact on Different Property Types

The valuation effects of upfront surveys vary significantly across property categories:

Older Properties 🏚️

Period properties and older homes benefit most from upfront surveys. Hidden defects are more common, and comprehensive condition documentation prevents unrealistic pricing. Buyers gain confidence, while sellers avoid repeated failed transactions.

New Construction 🏗️

Modern properties face fewer condition uncertainties, but snagging surveys identify finishing defects that affect immediate value. Upfront documentation protects both parties.

Leasehold Properties 🏢

Flats and leasehold houses require additional scrutiny of building condition, service charges, and lease terms. Upfront surveys combined with lease extension valuations provide complete financial clarity.

Investment Properties 💰

Landlords and investors particularly value upfront condition data, as it directly impacts yield calculations and capital expenditure planning. Stock condition surveys become standard due diligence tools.

Transaction Workflow Transformations in the 2026 Property Market

The operational implications of upfront condition survey mandates extend far beyond valuation methodology. The entire property transaction workflow undergoes fundamental restructuring, affecting timelines, costs, and professional responsibilities.

The New Transaction Timeline

Under traditional workflows, property transactions in the UK typically take 12-16 weeks from offer to completion. Upfront survey requirements compress and restructure this timeline:

Week 1-2: Pre-Marketing Phase

- Seller commissions comprehensive condition survey

- Chartered surveyor conducts detailed property inspection

- Report prepared with defect documentation and repair cost estimates

- Seller reviews findings and adjusts asking price accordingly

Week 3: Marketing Launch

- Property listed with condition survey available to all potential buyers

- Asking price reflects known condition issues

- Buyers review survey before arranging viewings

Week 4-6: Viewing and Offer Phase

- Informed buyers make realistic offers based on condition data

- Reduced need for post-offer survey contingencies

- Faster offer acceptance with fewer conditions

Week 7-12: Legal and Financial Completion

- Streamlined due diligence process

- Fewer renegotiation delays

- Faster mortgage approval with condition certainty

- Earlier completion dates

This restructured timeline reduces total transaction time by 3-4 weeks on average, primarily by eliminating the post-offer survey delay and associated renegotiations.

Surveyor Workflow Adaptations

Professional surveyors face significant operational changes under upfront mandate systems. The shift from buyer-commissioned to seller-commissioned surveys requires new business models and service delivery approaches.

Key workflow changes include:

✅ Seller-Side Engagement: Surveyors increasingly work with sellers and estate agents rather than individual buyers, requiring different communication approaches and report formats.

✅ Multi-Buyer Report Usage: A single survey serves multiple potential buyers, raising questions about liability, report ownership, and update requirements if properties remain unsold for extended periods.

✅ Enhanced Report Standards: Upfront surveys must meet higher comprehensiveness standards since they inform multiple parties' decisions. Level 2 versus Level 3 survey distinctions become more important.

✅ Faster Turnaround Requirements: Sellers want to list quickly, creating pressure for faster survey completion without compromising quality.

✅ Digital Delivery Systems: Reports must be easily shareable with multiple parties while maintaining confidentiality and version control.

For those wondering whether a survey is necessary when buying a house, upfront mandates make this question moot—the survey exists before the buying decision begins.

Cost Distribution and Financial Implications

Traditional transactions place survey costs on buyers, who may commission multiple surveys if purchasing attempts fail. Upfront mandates shift this cost to sellers, fundamentally changing transaction economics.

Financial impact analysis:

For Sellers:

- Upfront survey cost (£500-£1,500 depending on property type)

- Potential price adjustments based on findings

- Reduced risk of post-offer renegotiation

- Faster sales with fewer failed transactions

- Marketing advantage through transparency

For Buyers:

- Eliminated individual survey costs

- Ability to compare multiple properties on equal condition basis

- Reduced transaction risk and uncertainty

- Potential for additional specialist surveys if concerns arise

- Lower overall transaction costs

For Surveyors:

- Shift from multiple small commissions to fewer larger engagements

- Need for comprehensive liability insurance for multi-party reports

- Opportunity for value-added services (repair cost validation, reinspection services)

- Increased demand for building surveys as standard practice

The overall market effect tends toward cost efficiency, as one comprehensive survey replaces multiple redundant assessments of the same property.

Regional Implementation Variations and Market Responses

While national frameworks establish baseline requirements, regional property markets respond differently to upfront survey mandates based on local conditions, property types, and market dynamics.

Urban Market Adaptations

High-volume urban markets in areas like London, Clapham, and Camden face unique implementation challenges:

- Fast-moving markets: Properties sell quickly, requiring rapid survey turnaround

- Flat predominance: Leasehold surveys require building-wide assessments

- High property values: Survey costs represent smaller percentage of transaction value

- Competitive advantage: Early adopters gain marketing benefits through transparency

Estate agents in these markets report that properties with upfront surveys receive 30-40% more serious inquiries, as buyers appreciate the transparency and reduced risk.

Suburban and County Market Considerations

Markets in areas like Guildford, Esher, and Berkshire show different patterns:

- Larger properties: More complex surveys with higher costs

- Older housing stock: Greater likelihood of significant defects

- Slower market pace: More time for comprehensive assessments

- Rural considerations: Specialist surveys for septic systems, wells, land boundaries

In these markets, the comprehensive Level 3 building survey becomes the standard rather than the exception, as property complexity demands thorough assessment.

Professional Standards and Quality Assurance

The shift to upfront surveys raises important questions about professional standards, liability, and quality assurance. When a single survey informs multiple parties' decisions, the stakes for accuracy and comprehensiveness increase significantly.

Key quality considerations:

🔍 Surveyor Qualifications: Ensuring all upfront surveys are conducted by qualified chartered surveyors with appropriate professional indemnity insurance.

🔍 Report Standardization: Establishing consistent formats and content requirements so buyers can meaningfully compare properties.

🔍 Update Protocols: Determining when surveys must be refreshed if properties remain unsold for extended periods.

🔍 Liability Frameworks: Clarifying surveyor liability when reports are relied upon by multiple parties over time.

🔍 Dispute Resolution: Creating mechanisms for addressing disagreements about survey findings or valuations.

Professional bodies like RICS play a crucial role in establishing and enforcing these standards, ensuring that upfront survey mandates enhance rather than compromise transaction quality.

Strategic Implications for Market Participants in 2026

The valuation impacts of government homebuying reforms extend beyond operational changes to create strategic opportunities and challenges for all market participants.

For Property Sellers

Sellers must adapt their approach to property marketing and pricing:

Strategic considerations:

- Pre-sale repairs: Deciding whether to address defects before surveying or adjust price accordingly

- Pricing strategy: Setting realistic asking prices that reflect condition findings

- Survey selection: Choosing appropriate survey level for property type and condition

- Marketing advantage: Leveraging transparency as a competitive differentiator

- Timing decisions: Coordinating survey commissioning with optimal listing periods

Sellers who embrace upfront surveys report faster sales and fewer failed transactions, despite the initial cost investment.

For Property Buyers

Buyers gain significant advantages but must adjust their evaluation processes:

Strategic considerations:

- Comparative analysis: Systematically comparing condition reports across multiple properties

- Specialist follow-up: Determining when additional specialist surveys are warranted

- Negotiation approach: Using condition data to make informed initial offers

- Risk assessment: Evaluating repair costs and future maintenance implications

- Due diligence: Verifying survey findings through independent verification if concerns arise

The availability of detailed survey home reports before making offers fundamentally changes the buyer's decision-making process, shifting from sequential discovery to parallel evaluation.

For Mortgage Lenders

Financial institutions benefit from reduced lending risk when comprehensive condition data exists upfront:

- Faster mortgage approvals: Condition certainty accelerates underwriting

- Improved risk assessment: Better understanding of security value

- Reduced default risk: Buyers less likely to face unexpected repair costs

- Streamlined valuations: Lender valuations can reference existing surveys

- Portfolio quality: Overall improvement in loan book quality

Lenders increasingly require Red Book valuations that incorporate comprehensive condition data, making upfront surveys valuable for mortgage approval processes.

For Estate Agents and Conveyancers

Property professionals must integrate upfront surveys into their service delivery:

For Estate Agents:

- Marketing properties with condition transparency

- Managing seller expectations around survey findings

- Educating buyers on how to interpret survey reports

- Coordinating survey commissioning and report distribution

- Differentiating services through survey management expertise

For Conveyancers:

- Streamlined due diligence with condition certainty

- Faster transaction completion timelines

- Reduced post-contract issues and disputes

- Integration of survey findings into contract terms

- Coordination with remortgage conveyancing when applicable

Future Outlook: Evolution of Property Transaction Standards

The housing market reforms of 2026 represent just the beginning of a longer transformation in property transaction practices. Several trends are likely to shape future developments:

Technology Integration

Digital platforms increasingly facilitate survey commissioning, report distribution, and condition data analysis:

- AI-enhanced surveys: Machine learning tools assist surveyors in defect identification

- Digital twin technology: 3D property models integrate condition data

- Blockchain verification: Immutable records of property condition over time

- Automated valuation models: Algorithms incorporate condition data for instant valuations

- Mobile inspection tools: Tablets and specialized equipment streamline field work

Expanded Scope of Upfront Assessments

Beyond basic condition surveys, comprehensive upfront assessments may eventually include:

- Energy performance: Detailed efficiency assessments beyond basic EPC ratings

- Environmental risks: Flood, subsidence, and contamination evaluations

- Planning potential: Assessment of development or extension possibilities

- Neighborhood analysis: Comprehensive area reports on amenities, schools, transport

- Future cost projections: Long-term maintenance and replacement schedules

Market Maturation and Best Practices

As upfront survey mandates become standard practice, market participants will develop sophisticated approaches:

- Survey insurance products: Warranties covering survey accuracy and completeness

- Tiered survey options: Standardized packages for different property types and price points

- Quality certification schemes: Third-party verification of survey standards

- Professional specialization: Surveyors developing expertise in specific property types or regions

- Integrated transaction platforms: End-to-end digital systems managing entire property transactions

The broader policy environment, including HUD's focus on "cutting red tape and restoring local control"[6], suggests continued evolution toward more efficient, transparent property transaction systems.

Affordability and Access Considerations

While upfront surveys improve transaction efficiency, policymakers must address potential barriers:

- Cost burden on sellers: Ensuring survey costs don't prevent property listings

- Assistance programs: Potential subsidies for lower-value property surveys

- Standardized pricing: Preventing excessive survey costs through market transparency

- Quality vs. cost balance: Maintaining professional standards while controlling expenses

- Rural and remote access: Ensuring surveyor availability in all markets

Housing affordability improvements predicted for 2026[4] depend partly on reducing transaction friction through reforms like upfront survey mandates, but implementation must consider access equity.

Practical Implementation Guidance for 2026

For property market participants navigating the transition to upfront survey requirements, several practical steps facilitate successful adaptation:

For Sellers Preparing to List

Step 1: Research qualified surveyors in your area using resources like chartered surveyors in your region.

Step 2: Select appropriate survey level based on property age, type, and condition—typically a Level 2 survey for standard properties or Level 3 for older or complex homes.

Step 3: Commission survey 2-3 weeks before intended listing date to allow for completion and review.

Step 4: Review findings with your estate agent to determine appropriate pricing strategy.

Step 5: Decide whether to complete recommended repairs before listing or adjust price accordingly.

Step 6: Ensure survey report is readily available to all potential buyers through agent or online listing.

For Buyers Evaluating Properties

Step 1: Request and review upfront survey for every property under serious consideration.

Step 2: Compare condition reports across properties using standardized criteria.

Step 3: Calculate total acquisition cost including purchase price plus estimated repair costs.

Step 4: Determine if specialist surveys (structural, damp, electrical) are warranted based on findings.

Step 5: Factor long-term maintenance implications into affordability calculations.

Step 6: Make informed offers that reflect comprehensive understanding of property condition.

For Surveyors Adapting Services

Step 1: Develop seller-focused service packages and marketing materials.

Step 2: Establish relationships with estate agents as referral sources.

Step 3: Create standardized report formats optimized for multiple-party use.

Step 4: Implement digital delivery systems for efficient report distribution.

Step 5: Ensure professional indemnity insurance covers multi-party reliance scenarios.

Step 6: Develop expertise in property surveyor roles specific to upfront assessment context.

Conclusion: Embracing the New Transaction Paradigm

The valuation impacts of government homebuying reforms: upfront condition survey mandates and their effect on 2026 transaction workflows represent a fundamental shift in how property markets operate. By moving comprehensive condition assessments to the beginning of the transaction process, these reforms address longstanding inefficiencies that have plagued property markets for decades.

The benefits are substantial and wide-ranging:

✅ Enhanced transparency reduces information asymmetry between buyers and sellers

✅ Improved valuation accuracy ensures prices reflect true property condition

✅ Accelerated timelines eliminate post-offer survey delays and renegotiations

✅ Reduced transaction failure rates as surprises are discovered before offers

✅ Better-informed decisions by all parties throughout the process

While implementation challenges exist—including cost allocation, quality assurance, and regional variations—the overall trajectory points toward more efficient, transparent, and equitable property transactions.

Next Steps for Market Participants

If you're selling a property in 2026:

- Commission a comprehensive upfront survey before listing

- Work with qualified professionals who understand the new requirements

- Price realistically based on condition findings

- Leverage transparency as a competitive advantage

If you're buying a property in 2026:

- Request and carefully review upfront surveys for all properties

- Compare properties on a condition-adjusted basis

- Make informed offers that reflect comprehensive understanding

- Consider specialist follow-up surveys when warranted

If you're a property professional:

- Adapt service delivery to upfront survey requirements

- Invest in technology and systems that facilitate new workflows

- Educate clients about benefits and processes

- Maintain highest professional standards as stakes increase

The housing market reforms of 2026, building on legislative momentum from the 21st Century Road to Housing Act[1] and broader affordability initiatives[2], create opportunities for those who embrace change and adapt proactively. By understanding and implementing upfront condition survey practices, all market participants can benefit from faster, more transparent, and more successful property transactions.

For expert guidance on navigating these changes and accessing professional surveying services tailored to the new requirements, consult with qualified chartered surveyors who understand the evolving regulatory landscape and can provide comprehensive condition assessments that meet 2026 standards.

References

[1] Federal Housing Bill Housing Market Update March 13 2026 – https://www.realtor.com/news/real-estate-news/federal-housing-bill-housing-market-update-march-13-2026/

[2] Housing Market Predictions 2026 – https://www.redfin.com/news/housing-market-predictions-2026/

[4] Housing Affordability Could Make Small Improvements In 2026 Mortgage Rates New Construction Home Sales – https://katv.com/news/nation-world/housing-affordability-could-make-small-improvements-in-2026-mortgage-rates-new-construction-home-sales

[6] Hud Accomplishments 2026 – http://www.hud.gov/HUD-Accomplishments-2026