The Leasehold and Freehold Reform Act 2024 has triggered the most significant recalibration of property valuation methodologies in England and Wales since the 1993 Leasehold Reform Act. With marriage value abolished, 990-year extensions now standard, and ground rent caps implemented, chartered surveyors face unprecedented challenges in adapting RICS Red Book valuation frameworks to reflect these legislative changes. Understanding Valuing Freehold vs Leasehold Reforms in 2026: Surveyor Adjustments Post-Latest Legislation Changes has become essential for property professionals navigating this transformed landscape.

The reforms, which received royal assent on May 24, 2024, fundamentally alter how surveyors assess leasehold properties, enfranchisement premiums, and freehold reversions. Key provisions implemented on January 31, 2025, removed the two-year ownership rule, while March 3, 2025, brought Right to Manage updates affecting mixed-use developments.[5] These changes create immediate valuation implications that require technical expertise and updated methodological approaches.

Key Takeaways

✅ 990-year lease extensions eliminate traditional depreciation concerns, creating "virtual freehold" status that fundamentally changes long-term valuation models

✅ Marriage value abolition reduces costs for leases under 80 years but paradoxically increases premiums for 81-150 year leases by up to 30% in some scenarios

✅ Ground rent caps at £250 (reducing to peppercorn after 40 years) significantly impact investment valuations and freehold reversion calculations

✅ Deferment rate uncertainty creates substantial valuation volatility, with even small rate changes producing dramatically different premium calculations

✅ Cost responsibility shifts eliminate leaseholder obligation to pay freeholder fees, altering transaction economics and negotiation dynamics

Understanding the Legislative Framework: Valuing Freehold vs Leasehold Reforms in 2026

The Leasehold and Freehold Reform Act 2024 represents a comprehensive overhaul of property ownership rights in England and Wales. For surveyors conducting valuations in 2026, understanding these reforms is fundamental to producing accurate, defensible assessments that comply with RICS Red Book standards.[6]

Core Legislative Changes Affecting Valuations

The Act introduces several transformative provisions that directly impact how chartered surveyors approach property valuations:

990-Year Lease Extensions: Previously, leaseholders extending their lease received 90 additional years for flats or 50 years for houses. The new standard of 990 years effectively creates perpetual ownership, eliminating the traditional "wasting asset" characteristic of short leases.[3] This change fundamentally alters depreciation calculations and removes the urgency premium previously associated with declining lease terms.

Immediate Enfranchisement Rights: The elimination of the two-year ownership requirement as of January 31, 2025, means new purchasers can immediately exercise statutory rights to extend leases or acquire freeholds.[5] This creates a more liquid market but introduces complexity for surveyors valuing properties with very short remaining terms.

Marriage Value Abolition: This component previously accounted for approximately half of the premium uplift when extending leases below 80 years.[2] Its removal represents the most significant cost reduction for affected leaseholders but creates unexpected consequences for medium-length leases.

Ground Rent Limitations: The £250 annual cap on existing leases (reducing to peppercorn after 40 years) directly impacts income capitalization calculations for freehold reversions.[5] Surveyors must now apply these caps when valuing freeholder interests, substantially reducing investment yields in many cases.

Phased Implementation Timeline

Understanding the implementation schedule is crucial for surveyors determining which valuation methodology applies to specific instructions:

| Date | Provision Implemented | Valuation Impact |

|---|---|---|

| May 24, 2024 | Royal Assent | Legislative certainty established |

| January 31, 2025 | Two-year rule removed | Immediate enfranchisement rights |

| March 3, 2025 | Right to Manage updates | 50% non-residential threshold |

| Pending | Ground rent caps | Awaiting secondary legislation |

| Pending | Commonhold framework | Future ownership model |

For surveyors working in 2026, most core provisions are now active, though some aspects await secondary legislation.[5] This creates a transitional period where valuation approaches must account for both implemented changes and anticipated future provisions.

RICS Red Book Adjustments: Valuing Freehold vs Leasehold Reforms in 2026

The RICS Valuation – Global Standards (Red Book) provides the authoritative framework for property valuations in the UK. The 2024 reforms necessitate substantial methodological adjustments that surveyors must incorporate into their practice to maintain professional compliance and accuracy.[6]

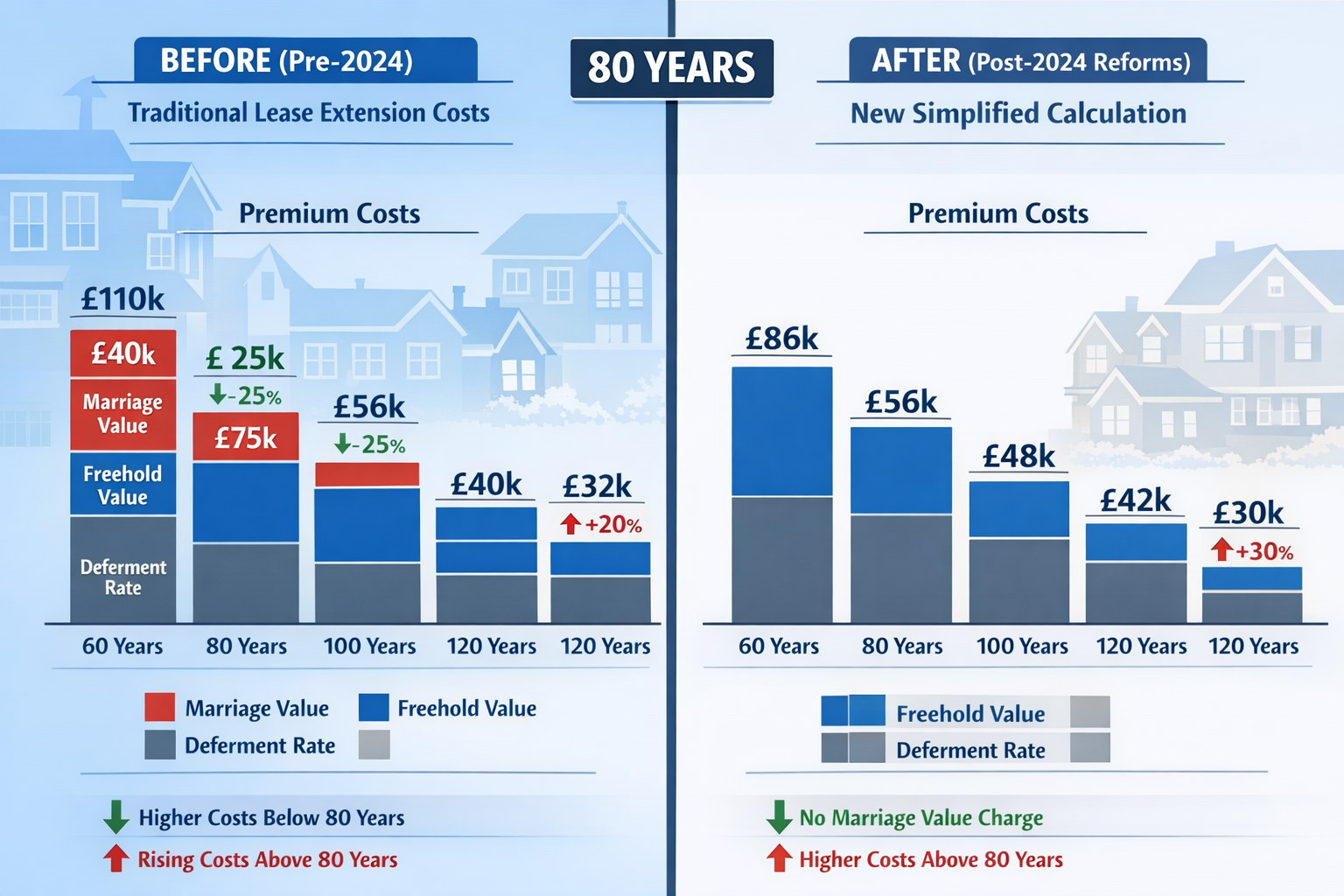

Marriage Value Removal: Calculation Methodology Changes

The abolition of marriage value represents the most technically significant change for surveyors valuing lease extensions. Previously, when a lease fell below 80 years, valuers calculated marriage value as the difference between:

- The combined value of the existing leasehold and freehold interests

- The value of the extended lease plus the diminished freehold reversion

This "marriage value" was split 50/50 between freeholder and leaseholder, often adding £20,000-£50,000 to extension premiums in prime locations.[1]

Post-Reform Calculation Framework:

Under the new regime, surveyors now calculate lease extension premiums using only:

- Diminution in freehold value: The difference between the freehold reversion value with the existing lease versus the extended 990-year lease

- Capitalised ground rent loss: The present value of ground rent income (subject to the £250 cap) that the freeholder will no longer receive

This simplified approach benefits leaseholders with sub-80-year leases but creates unexpected cost increases for those with 81-150 years remaining. Economic modeling suggests collective costs could increase by £3.14 billion if all eligible leaseholders extended simultaneously.[2]

Deferment Rate Implications

Deferment rates—the discount rate applied to future freehold reversion values—have become critically important in the reformed valuation framework. With marriage value removed, deferment rate assumptions now drive the majority of premium calculations.[2]

Current Market Rates:

- Prime central London flats: 4.75-5.0%

- Standard residential flats: 5.0-5.5%

- Houses: 4.75-5.25%

Even minor adjustments to these rates create substantial valuation differences. A 0.5% increase in the deferment rate reduces the present value of the freehold reversion, lowering the premium payable. Conversely, a decrease raises costs significantly—particularly problematic for medium-length leases.[2]

Surveyors must now carefully justify deferment rate selections with reference to:

✅ Recent tribunal decisions post-reform

✅ Property location and quality

✅ Comparable enfranchisement transactions

✅ Market evidence of freehold investment yields

Ground Rent Capitalization Under the £250 Cap

The proposed £250 annual ground rent cap (reducing to peppercorn after 40 years) fundamentally changes how surveyors capitalize ground rent income when valuing freehold reversions.[5]

Practical Application:

For a property with £500 annual ground rent:

Pre-Reform Valuation:

- Capitalize £500 at 6% yield = £8,333 present value

Post-Reform Valuation:

- Capitalize £250 at 6% yield = £4,167 present value (50% reduction)

- After 40 years: £0 present value

Surveyors must apply these caps when valuing freeholder interests for:

- Portfolio valuations for institutional investors

- Matrimonial valuations involving freehold investments

- Enfranchisement premium calculations

- RICS registered valuation reports for lending purposes

This creates downward pressure on freehold investment values, particularly for portfolios heavily dependent on ground rent income rather than reversion value.

990-Year Extension Impact on Depreciation Models

Traditional leasehold valuation incorporated depreciation curves reflecting diminishing value as lease terms shortened. The 990-year standard eliminates this consideration for extended leases, creating valuation parity with freehold properties in most scenarios.[3]

Surveyor Considerations:

When valuing properties with newly extended 990-year leases, surveyors should:

- Apply freehold comparable evidence rather than leasehold comparables

- Eliminate lease length adjustments from valuation models

- Consider remaining service charge obligations as the primary differentiator from true freehold

- Assess management quality and building condition more heavily, as these become the dominant value factors

For properties not yet extended, surveyors must now consider the immediate availability of 990-year extensions when assessing market value. Purchasers can extend from Day One, meaning short lease discounts should theoretically narrow to reflect only the extension premium cost plus transaction expenses.[3]

This creates a more efficient market but requires surveyors to maintain current knowledge of typical lease extension costs in their valuation area.

Practical Surveyor Adjustments: Valuing Freehold vs Leasehold Reforms in 2026

Implementing these legislative changes requires chartered surveyors to adapt their practical valuation approaches, data collection methods, and reporting frameworks. Understanding Valuing Freehold vs Leasehold Reforms in 2026: Surveyor Adjustments Post-Latest Legislation Changes in operational terms is essential for producing defensible valuations.

Comparative Analysis: Pre and Post-Reform Valuation Outcomes

The reforms create significantly different valuation outcomes depending on remaining lease length. Surveyors must understand these patterns to advise clients effectively:

Short Leases (Under 80 Years):

✅ Substantial cost reductions due to marriage value removal

✅ Simplified calculations with fewer contentious components

✅ Greater predictability in premium negotiations

✅ Reduced tribunal disputes over marriage value apportionment

Example Scenario:

- Property value: £500,000

- Remaining lease: 65 years

- Ground rent: £150 per annum

Pre-Reform Premium: £45,000-£55,000 (including marriage value)

Post-Reform Premium: £18,000-£24,000 (marriage value removed)

Medium Leases (81-150 Years):

⚠️ Potential cost increases of 20-30% in some scenarios

⚠️ Greater sensitivity to deferment rate assumptions

⚠️ Reduced marriage value benefit (never applicable)

⚠️ Higher present value of freehold reversion

Example Scenario:

- Property value: £500,000

- Remaining lease: 95 years

- Ground rent: £250 per annum

Pre-Reform Premium: £8,000-£12,000

Post-Reform Premium: £10,000-£16,000 (depending on deferment rate)

This counterintuitive outcome occurs because these leaseholders never benefited from marriage value removal but remain vulnerable to deferment rate changes that increase the present value of the freeholder's reversion.[2]

Service Charge Transparency and Valuation Impact

The reforms introduce enhanced service charge transparency requirements, affecting how surveyors assess leasehold properties:[3]

New Freeholder Obligations:

📋 Standardized annual service charge statements

📋 Detailed cost breakdowns by category

📋 Insurance commission disclosure

📋 Annual performance reports

📋 Transparent managing agent fee structures

For surveyors, these changes create new data sources for assessing property management quality—a factor that significantly impacts leasehold values. Properties with transparent, well-managed service charges should command premiums over those with opaque or excessive charges.

When conducting building surveys or valuations, surveyors should now request:

- Three years of service charge accounts

- Evidence of insurance commission levels

- Managing agent performance reports

- Planned maintenance schedules

- Reserve fund adequacy assessments

This information enables more accurate assessment of ongoing ownership costs, which directly impacts net present value calculations.

Right to Manage Threshold Changes

The increase in the Right to Manage threshold from 25% to 50% non-residential space opens enfranchisement opportunities for thousands of mixed-use properties previously excluded.[3]

Surveyor Implications:

For properties in town centers with ground-floor retail and upper-floor residential units, surveyors must now:

- Measure non-residential floor area accurately to determine eligibility

- Value collective enfranchisement opportunities that were previously unavailable

- Assess management transition risks when leaseholders exercise RTM rights

- Consider premium impacts of potential management changes

Properties newly eligible for collective enfranchisement or Right to Manage may experience value uplifts of 5-10% as leaseholders gain greater control over their buildings.[7]

Freehold vs Leasehold Valuation Parity Analysis

With 990-year extensions creating "virtual freehold" status, the traditional valuation gap between freehold and leasehold properties has narrowed substantially. However, several factors maintain some differential:[7]

Remaining Differentiators:

| Factor | Freehold Advantage | Leasehold Consideration |

|---|---|---|

| Service charges | None | Ongoing annual costs |

| Management control | Complete | Subject to lease terms |

| Structural alterations | Unrestricted | Requires consent |

| Subletting rights | Absolute | May be restricted |

| Mortgage availability | Widest options | Some lender restrictions |

Surveyors valuing extended leasehold properties should apply discounts of 2-5% compared to equivalent freehold properties to reflect these ongoing constraints, though this represents a significant narrowing from the historical 10-15% differential for long leases.[7]

Cost Responsibility Changes: Transaction Economics

The elimination of the leaseholder's obligation to pay the freeholder's legal and professional fees fundamentally alters enfranchisement economics.[1]

Previous Cost Structure:

- Leaseholder's premium: £30,000

- Leaseholder's legal fees: £2,000

- Leaseholder's valuation fees: £1,500

- Freeholder's legal fees (paid by leaseholder): £3,000

- Freeholder's valuation fees (paid by leaseholder): £1,500

- Total leaseholder cost: £38,000

Post-Reform Cost Structure:

- Leaseholder's premium: £30,000

- Leaseholder's legal fees: £2,000

- Leaseholder's valuation fees: £1,500

- Freeholder's costs: Borne by freeholder

- Total leaseholder cost: £33,500 (12% reduction)

This change makes enfranchisement more accessible and economically attractive, potentially increasing demand for surveyor valuation services as more leaseholders pursue extensions.[1]

Data Collection and Comparable Evidence

Surveyors must now maintain updated databases of post-reform comparable transactions to support valuation conclusions. Key data points include:

✅ Recent lease extension premiums under the new framework

✅ Tribunal decisions applying reformed methodologies

✅ Deferment rates accepted in recent settlements

✅ Ground rent capitalization rates reflecting the £250 cap

✅ 990-year extended lease sales compared to freehold equivalents

Professional surveyors should participate in industry forums and subscribe to specialist publications tracking these emerging patterns. The RICS guidance on leasehold reform provides updated technical standards as case law develops.[6]

Regional Variations and Local Market Impacts

The impact of Valuing Freehold vs Leasehold Reforms in 2026: Surveyor Adjustments Post-Latest Legislation Changes varies significantly across different UK property markets. Surveyors must understand local market dynamics to produce accurate valuations.

Prime Central London Considerations

In prime central London markets—including areas served by chartered surveyors in Chelsea, Camden, and Fulham—the reforms create distinctive valuation challenges:

High-Value Property Impacts:

🏛️ Larger absolute premium reductions for sub-80-year leases (marriage value removal saves £50,000-£150,000 in prime areas)

🏛️ Greater sensitivity to deferment rate assumptions due to high reversion values

🏛️ Institutional freeholder resistance creating more tribunal proceedings

🏛️ Portfolio valuation complexity for investment funds holding multiple freehold interests

Surveyors working in these markets must maintain detailed knowledge of recent tribunal decisions and apply deferment rates justified by prime location characteristics.

Suburban and Regional Market Dynamics

In suburban London areas like Barnes, Clapham, and Ealing, as well as regional markets in Hertfordshire, Essex, and Guildford, different patterns emerge:

Regional Characteristics:

🏘️ Lower absolute premium amounts making enfranchisement more accessible

🏘️ Greater prevalence of houses (historically more expensive to extend)

🏘️ Smaller institutional freeholder presence leading to more negotiated settlements

🏘️ Higher proportion of individual freeholders potentially more willing to negotiate

Surveyors in these markets may find greater variation in deferment rates and capitalization rates, requiring careful analysis of local comparable evidence rather than relying solely on London-centric tribunal decisions.

Mixed-Use Development Opportunities

The 50% non-residential threshold creates significant opportunities in town center locations across markets including Hammersmith, Romford, and Bromley:

Valuation Considerations:

- Measure commercial floor area precisely using RICS measurement standards

- Assess collective enfranchisement viability for newly eligible buildings

- Consider potential value uplift from leaseholder-controlled management

- Evaluate commercial tenant lease terms affecting overall building value

Properties newly eligible for collective enfranchisement may experience 5-15% value increases as leaseholders gain control over building management and future development potential.[3]

Commonhold Transition Prospects and Valuation Implications

While the 2024 reforms focus primarily on leasehold improvements, the government has signaled intention to promote commonhold as the preferred ownership model for new developments.[5] Surveyors must understand this emerging framework's valuation implications.

Commonhold Framework Overview

Commonhold represents a freehold ownership model where flat owners hold individual freehold title to their units plus shared ownership of common areas through a commonhold association. This structure eliminates:

❌ Ground rent payments

❌ Lease depreciation

❌ Freeholder/leaseholder conflicts

❌ Lease extension requirements

Valuation Advantages:

✅ Perpetual ownership without depreciation

✅ Direct control over building management

✅ Transparent cost structures

✅ Enhanced mortgage availability

✅ Simplified conveyancing

Conversion Valuation Challenges

Existing leasehold buildings may convert to commonhold if all leaseholders agree. Surveyors valuing properties in buildings considering conversion must assess:

Pre-Conversion Factors:

- Remaining lease terms and extension costs

- Current freeholder cooperation level

- Service charge transparency and fairness

- Building condition and reserve fund adequacy

Post-Conversion Factors:

- Elimination of ground rent obligations

- Removal of lease depreciation concerns

- Enhanced owner control benefits

- Potential management transition costs

Properties successfully converting to commonhold may experience 3-8% value uplifts, though this depends heavily on the previous lease terms and management quality.[5]

New-Build Valuation Considerations

The ban on new-build leasehold houses means all new houses must be sold as freehold.[3] For surveyors conducting new-build surveys, this creates:

Simplified Valuation Framework:

- No lease length considerations for houses

- Elimination of ground rent capitalization

- Direct freehold comparable evidence

- Reduced conveyancing complexity

However, new-build flats may still be sold as leasehold, requiring surveyors to carefully assess:

- Initial lease length (should be 990 years under reforms)

- Ground rent terms (should be peppercorn)

- Service charge provisions and transparency

- Management company structure and control

Professional Practice Implications for Chartered Surveyors

The reformed legislative environment creates new professional responsibilities and practice considerations for chartered surveyors conducting valuations in 2026.

Continuing Professional Development Requirements

Surveyors must maintain current knowledge of:

📚 Latest tribunal decisions applying reformed methodologies

📚 Updated RICS guidance on leasehold valuations

📚 Secondary legislation as it's implemented

📚 Market evidence of post-reform transaction patterns

📚 Deferment rate trends across different property types

Professional bodies including RICS offer specialized training on the reforms, and surveyors should complete relevant CPD modules to maintain competence.[6]

Valuation Report Updates

Valuation reports must now explicitly address the reformed framework, including:

Essential Report Components:

- Legislative context statement confirming which provisions apply

- Methodology explanation detailing marriage value treatment

- Deferment rate justification with comparable evidence

- Ground rent cap application where relevant

- Lease extension cost assessment using reformed calculations

- Freehold comparison analysis for extended leases

Reports failing to address these elements may be challenged as inadequate or non-compliant with RICS standards.[6]

Professional Indemnity Considerations

The transitional period creates elevated professional indemnity risks as valuation methodologies evolve and tribunal precedents develop. Surveyors should:

⚠️ Maintain adequate PI coverage reflecting increased complexity

⚠️ Document methodology decisions thoroughly

⚠️ Seek specialist advice on complex or high-value instructions

⚠️ Participate in peer review for significant valuations

⚠️ Monitor emerging case law continuously

Working with experienced chartered surveyors who specialize in leasehold valuations reduces risk and ensures compliance with evolving standards.

Client Advisory Responsibilities

Surveyors have enhanced advisory responsibilities under the reformed framework:

For Leaseholder Clients:

✅ Explain marriage value removal benefits (sub-80-year leases)

✅ Highlight potential cost increases (81-150 year leases)

✅ Advise on optimal extension timing

✅ Clarify 990-year extension advantages

✅ Explain cost responsibility changes

For Freeholder Clients:

✅ Assess portfolio valuation impacts

✅ Explain ground rent cap implications

✅ Advise on negotiation strategies

✅ Clarify own-cost responsibility

✅ Evaluate investment yield changes

Providing comprehensive advice helps clients make informed decisions and reduces the likelihood of disputes or dissatisfaction with valuation outcomes.

Dispute Resolution and Tribunal Considerations

The reformed framework creates new patterns in enfranchisement disputes and tribunal proceedings that surveyors must understand when providing expert evidence or negotiating settlements.

Common Dispute Areas Post-Reform

Deferment Rate Disagreements:

With marriage value removed, deferment rate assumptions now drive the majority of premium calculations. Disputes frequently center on:

- Appropriate rate for specific property types

- Impact of location on deferment rates

- Comparable evidence interpretation

- Application of tribunal precedents

Surveyors must prepare robust justifications for rate selections, supported by recent comparable evidence and tribunal decisions.[2]

Ground Rent Capitalization Disputes:

The £250 cap creates disagreements over:

- Application timing and methodology

- Capitalization rates for capped rents

- Treatment of review clauses

- Present value calculations for peppercorn conversion

Lease Length Valuation Impacts:

For properties with 81-150 year leases experiencing cost increases, disputes arise over:

- Necessity of immediate extension

- Appropriate valuation methodology

- Comparable transaction evidence

- Market value impact assessments

Expert Witness Responsibilities

Surveyors providing expert evidence in tribunal proceedings must:

🔍 Maintain independence from client interests

🔍 Apply consistent methodology across similar cases

🔍 Provide clear reasoning for all assumptions

🔍 Consider alternative approaches objectively

🔍 Comply with CPR Part 35 requirements

The reformed framework increases the importance of expert evidence quality, as fewer disputes center on easily quantifiable marriage value and more depend on professional judgment regarding rates and methodologies.

Future Legislative Developments and Surveyor Preparedness

While the 2024 reforms represent substantial change, further legislative developments remain likely. Surveyors must monitor emerging proposals to maintain valuation accuracy.

Anticipated Secondary Legislation

Several reform elements await detailed secondary legislation:[5]

Pending Provisions:

⏳ Ground rent cap implementation details (timing and transition arrangements)

⏳ Commonhold conversion procedures (valuation methodologies and dispute resolution)

⏳ Service charge regulation specifics (enforcement mechanisms and standards)

⏳ Building safety cost allocation (interaction with leasehold reforms)

Surveyors should monitor government consultations and industry responses to anticipate how these provisions will affect valuation practice.

Potential Further Reforms

The current government has indicated openness to additional reforms, potentially including:

- Complete leasehold abolition for new builds (including flats)

- Enhanced commonhold promotion measures

- Further ground rent restrictions

- Expanded enfranchisement rights

- Simplified valuation methodologies

Staying informed about policy developments enables surveyors to advise clients on optimal timing for enfranchisement actions and property transactions.

Conclusion

Valuing Freehold vs Leasehold Reforms in 2026: Surveyor Adjustments Post-Latest Legislation Changes represents a fundamental shift in property valuation practice across England and Wales. The Leasehold and Freehold Reform Act 2024 has eliminated marriage value, introduced 990-year lease extensions, capped ground rents, and transferred cost responsibilities—each change requiring substantial methodological adjustments by chartered surveyors.

The reforms create winners and losers: leaseholders with sub-80-year terms benefit from dramatic cost reductions, while those with 81-150 year leases may face unexpected premium increases due to deferment rate sensitivity. Freeholders experience diminished investment values through ground rent caps and reduced reversion values. Surveyors must navigate these complex dynamics while maintaining RICS Red Book compliance and providing clear client advice.

Actionable Next Steps

For Property Owners:

- Obtain a professional valuation from a qualified RICS surveyor to understand your specific position under the reforms

- Review your lease terms to determine optimal extension timing given the new framework

- Assess service charge transparency and consider Right to Manage opportunities if applicable

- Compare extension costs under reformed methodologies versus traditional calculations

- Consider commonhold conversion if your building meets eligibility criteria

For Property Professionals:

- Complete specialized CPD on leasehold reform valuation methodologies

- Update valuation report templates to address reformed framework requirements

- Build comparable evidence databases of post-reform transactions and tribunal decisions

- Review PI coverage to ensure adequate protection during the transitional period

- Participate in industry forums to share knowledge and best practices

For Investors:

- Reassess freehold investment portfolios considering ground rent cap impacts

- Evaluate deferment rate assumptions in existing valuation models

- Consider strategic timing for portfolio disposals or acquisitions

- Analyze geographic variations in reform impact across different markets

- Monitor secondary legislation that may further affect investment values

The reformed landscape requires expertise, current knowledge, and careful analysis. Working with experienced professionals who understand both the technical valuation requirements and the practical implications of the 2024 reforms ensures accurate property assessments and informed decision-making in this transformed market environment.

For comprehensive property valuation services that incorporate the latest legislative changes, consider consulting with specialists who maintain current expertise in leasehold reform valuations and understand the nuanced implications of Valuing Freehold vs Leasehold Reforms in 2026: Surveyor Adjustments Post-Latest Legislation Changes for your specific circumstances.

References

[1] Leasehold Reform Valuations – https://www.eddisons.com/valuations-and-advisory/valuations/leasehold-reform-valuations

[2] Leasehold And Freehold Reform Act Could Raise Costs For Many Freeholders Especially Those With 80 150 Year Leases – https://ringley.co.uk/blogs/leasehold-and-freehold-reform-act-could-raise-costs-for-many-freeholders-especially-those-with-80-150-year-leases

[3] The Leasehold Freehold Reform Act What 2026 Buyers Need To Know – https://www.gorvinsresidential.com/the-leasehold-freehold-reform-act-what-2026-buyers-need-to-know/

[4] Leasehold Reform – https://hoa.org.uk/advice/guides-for-homeowners/for-owners/leasehold-reform/

[5] Understanding The Draft 2026 Commonhold And Leasehold Reform Bill – https://www.edwinthompson.co.uk/understanding-the-draft-2026-commonhold-and-leasehold-reform-bill/

[6] Leasehold Reform In England And Wales – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards/leasehold-reform-in-england-and-wales

[7] Freehold Vs Leasehold 2026 The New Rules Of Ownership – https://www.purplebricks.co.uk/freehold-vs-leasehold-2026-the-new-rules-of-ownership

[8] Why The Government Must Consult With Professionals On Leasehold Reform – https://ifamagazine.com/why-the-government-must-consult-with-professionals-on-leasehold-reform/