The UK property market has transformed dramatically, creating unprecedented opportunities for first-time buyers. After years of stretched affordability and limited housing stock, 2026 marks a pivotal shift: 40% of homes nationwide can now be purchased with monthly mortgage payments lower than local rents[1], mortgage rates have dipped below 4% for the first time in years[2], and available housing inventory sits 6% above year-ago levels[1]. For aspiring homeowners, understanding how to properly prepare valuations in this evolving landscape can mean the difference between securing an excellent deal and overpaying in a market that finally favors buyers. Preparing Valuations for First-Time Buyers in 2026: Leveraging Improved Affordability and Supply Trends requires strategic insight into current market dynamics, professional valuation protocols, and timing considerations that maximize purchasing power.

Key Takeaways

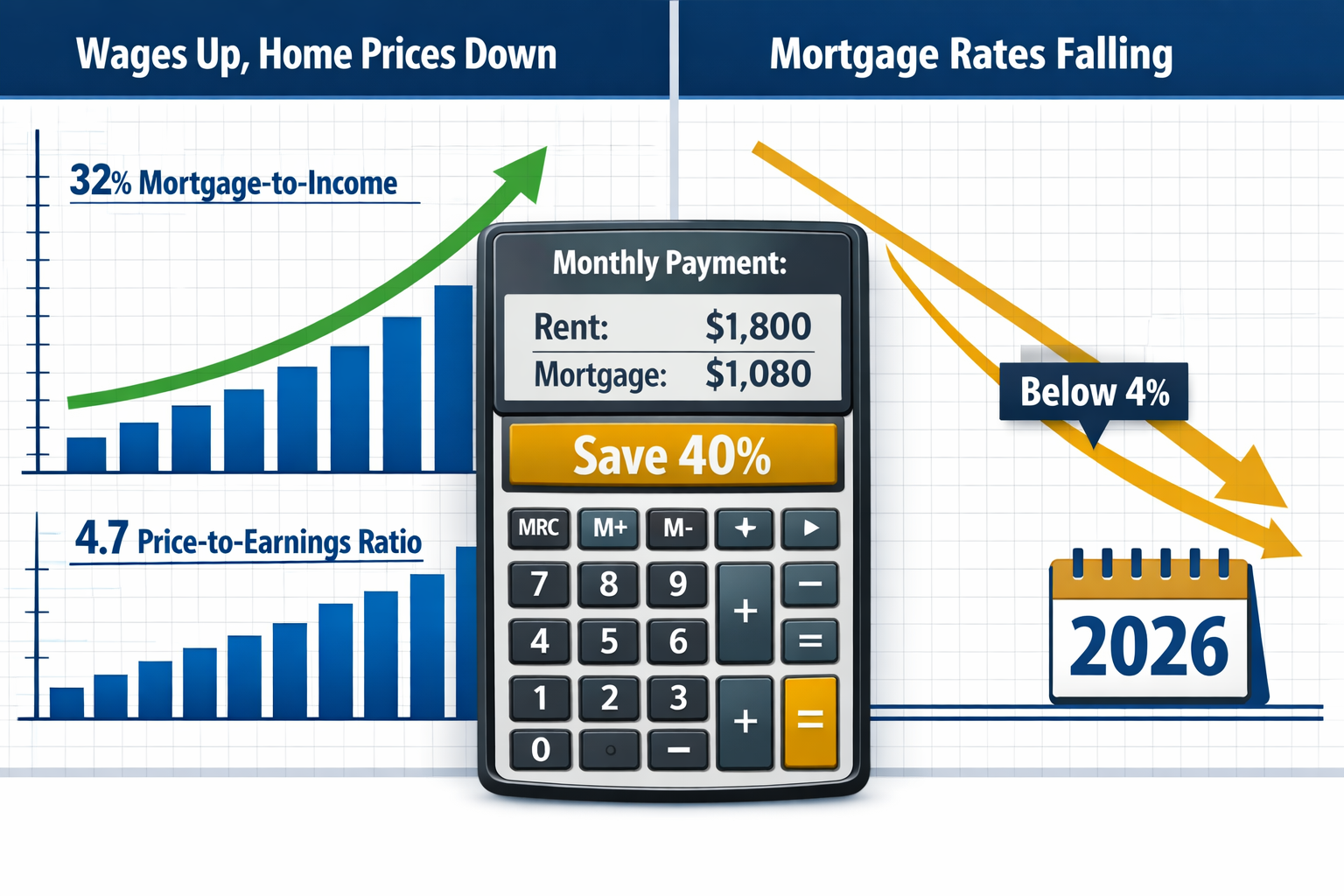

- Affordability has normalized significantly: First-time buyer mortgage repayments now represent approximately 32% of take-home pay, close to the long-term average of 30%, with the house price-to-earnings ratio improving to 4.7[1]

- Increased housing supply creates buyer leverage: Available stock is 6% higher than last year, providing greater selection and stronger negotiating positions for first-time purchasers[1]

- Professional valuations protect against overpayment: With asking prices showing volatility and regional variations, independent RICS valuations ensure buyers understand true market value before committing

- Mortgage rate improvements expand budgets: Five-year fixed rates below 4% combined with three consecutive years of wage growth outpacing house price inflation have fundamentally strengthened real purchasing power[1][2]

- Regional market dynamics require localized analysis: Northern regions continue outperforming southern markets, making location-specific valuation expertise essential for optimal investment decisions[2]

Understanding the 2026 Market Landscape for First-Time Buyers

The property market in 2026 presents a fundamentally different environment compared to the challenging conditions of recent years. Average UK house prices reached a new high of £301,151 in February 2026, with monthly growth of 0.3% and annual growth strengthening to 1.3%[2]. While these figures might initially suggest continued unaffordability, the underlying economics tell a more optimistic story for first-time buyers.

The Affordability Revolution

Three critical factors have converged to create what experts describe as a "normalized" affordability environment:

Wage Growth Outpacing Property Inflation 📈

For three consecutive years, average earnings growth has exceeded house price inflation[1]. This fundamental shift has reversed the decades-long trend of property values racing ahead of income growth. The practical impact is substantial: buyers today have genuinely greater purchasing power relative to property prices than at any point since before the 2020 pandemic.

Mortgage Rate Improvements

Five-year fixed mortgage rates have fallen below 4% for the first time in several years[2], with further rate cuts expected from the Bank of England in coming months. This represents a dramatic improvement from the 6%+ rates that characterized much of 2023-2024. For a typical first-time buyer purchasing a £250,000 property with a 10% deposit, the difference between a 6% rate and a 3.8% rate amounts to approximately £250 per month—or £15,000 over five years.

Improved Price-to-Earnings Ratios

The house price-to-earnings ratio has improved to 4.7, just below the 20-year average[1]. This metric provides crucial context: while absolute house prices remain high, they've become more aligned with what households can realistically afford based on current income levels.

Supply Dynamics Favor Buyers

Perhaps the most significant development for first-time buyers is the 6% increase in available housing stock compared to year-ago levels[1]. This inventory expansion creates several advantages:

- Greater selection and choice across property types, locations, and price points

- Reduced bidding war intensity that characterized the pandemic-era market

- Enhanced negotiating leverage when making offers below asking prices

- More time for due diligence including comprehensive property valuations and surveys

The combination of improved affordability metrics and increased supply creates what market analysts describe as a "buyer's market"—conditions that haven't existed consistently since before 2020.

Preparing Valuations for First-Time Buyers in 2026: Essential Protocols and Strategies

Professional property valuation represents one of the most critical yet frequently underestimated steps in the first-time buyer journey. In 2026's dynamic market environment, understanding valuation protocols and leveraging professional expertise can protect buyers from overpaying while identifying genuine opportunities.

Why Independent Valuations Matter More Than Ever

Despite improved market conditions, several factors make professional valuations particularly important in 2026:

Asking Price Volatility

Rightmove recorded a 2.8% jump in asking prices between December and February 2026, representing the strongest start to a year since 2020[1]. However, February asking prices held flat month-over-month after January's record jump, indicating seller uncertainty about sustainable pricing levels. This volatility means asking prices may not accurately reflect true market value.

Regional Performance Disparities

Northern regions continue to outperform southern markets with stronger price growth concentrated in the north of England and Scotland, while higher-priced southern regions remain softer[2]. A property in Manchester may warrant a different valuation approach than a comparable property in Surrey, despite similar asking prices.

Lender Requirements

Mortgage lenders require professional valuations to ensure the property provides adequate security for the loan. However, lender valuations serve the lender's interests—not the buyer's. Independent valuations provide buyers with comprehensive information about property condition, market positioning, and fair value.

Key Valuation Methods for First-Time Buyers

Professional chartered surveyors employ several valuation approaches, each providing different insights:

| Valuation Method | Description | Best Used For |

|---|---|---|

| Comparative Market Analysis | Evaluates recent sales of similar properties in the same area | Standard residential purchases in established neighborhoods |

| Income Approach | Calculates value based on potential rental income | Buy-to-let or properties with rental potential |

| Cost Approach | Estimates replacement cost minus depreciation | New builds or unique properties with limited comparables |

| Residual Method | Determines value based on development potential | Properties requiring significant renovation |

For most first-time buyers, the comparative market analysis provides the most relevant insights, examining recent sales data, current market conditions, and property-specific features to determine fair market value.

The RICS Valuation Standard

Working with RICS (Royal Institution of Chartered Surveyors) qualified professionals ensures valuations follow rigorous professional standards. RICS valuations consider:

- Physical property characteristics: Size, layout, condition, construction quality

- Location factors: Neighborhood desirability, transport links, local amenities

- Market conditions: Current supply-demand dynamics, recent transaction data

- Legal considerations: Tenure type, planning restrictions, easements

- Economic factors: Local employment trends, demographic shifts, development plans

For first-time buyers exploring government assistance schemes, specialized valuations may be required. Help to Buy valuations follow specific protocols to ensure properties meet scheme requirements, while RICS shared ownership valuations address the unique considerations of part-buy, part-rent arrangements.

Integrating Valuations with Comprehensive Surveys

Smart first-time buyers recognize that valuation and condition assessment work hand-in-hand. While valuations determine market worth, comprehensive surveys identify potential defects, maintenance issues, and hidden costs that impact long-term value.

Understanding what survey you need depends on property age, type, and condition. The survey landscape includes:

- RICS Level 2 HomebuYer Survey: Suitable for conventional properties in reasonable condition

- RICS Level 3 Building Survey: Comprehensive inspection for older, altered, or unusual properties

- Specific Defect Reports: Targeted investigation of particular concerns identified during initial viewings

Many first-time buyers benefit from reviewing a full structural survey sample to understand the depth of information professional surveys provide. This knowledge helps buyers make informed decisions about which survey level matches their property and risk tolerance.

Leveraging Valuation Data for Negotiation

Professional valuations provide powerful negotiation leverage in 2026's buyer-favorable market. When a valuation reveals asking price exceeds fair market value by 5-10%, buyers can:

✅ Present objective evidence supporting a lower offer

✅ Negotiate repairs or price reductions based on condition issues

✅ Request seller contributions toward closing costs or repairs

✅ Walk away confidently from overpriced properties knowing alternatives exist

With housing stock 6% above year-ago levels[1], buyers have genuine alternatives—strengthening their negotiating position considerably compared to the seller's market conditions of 2020-2022.

Preparing Valuations for First-Time Buyers in 2026: Timing Considerations and Market Entry Strategies

Strategic timing plays a crucial role in maximizing the benefits of improved affordability and supply trends. Understanding market cycles, seasonal patterns, and economic indicators helps first-time buyers optimize their market entry.

Current Market Momentum and Future Outlook

Sales activity in February 2026 ran at one of the strongest levels of the past decade[1], indicating renewed market confidence after the prolonged Budget uncertainty of late 2025. This activity surge reflects several positive developments:

- Resolution of political and economic uncertainty

- Improved mortgage product availability and pricing

- Pent-up demand from buyers who delayed purchases during 2024-2025

- Realistic seller pricing expectations following market adjustments

Expert house price forecasts for 2026 show modest but consistent growth expectations:

- Nationwide: 2-4% growth

- Halifax: 1-3% growth

- Savills: 2% growth

- Zoopla: 1.5% growth[3]

These conservative forecasts suggest a stable, sustainable market rather than the volatile boom-bust cycles that characterized previous decades.

Seasonal Considerations for First-Time Buyers

Property markets exhibit predictable seasonal patterns that savvy first-time buyers can leverage:

Spring Market (March-May) 🌸

- Highest inventory levels as sellers list properties

- Increased competition from other buyers

- Best selection of available properties

- Traditionally strongest price growth period

Summer Market (June-August) ☀️

- Sustained activity but slightly reduced urgency

- Family buyers prioritize school calendar considerations

- Good negotiating opportunities as summer progresses

- Completion timelines may extend due to holidays

Autumn Market (September-November) 🍂

- Second peak activity period after summer slowdown

- Motivated sellers who didn't achieve summer sales

- Shorter daylight hours can make properties less appealing

- Opportunity for advantageous negotiations

Winter Market (December-February) ❄️

- Lowest inventory and buyer activity levels

- Highly motivated sellers remaining on market

- Strongest negotiating leverage for buyers

- Potential delays due to holiday periods

In 2026's buyer-favorable market with 6% higher inventory[1], first-time buyers have flexibility to be selective about timing rather than feeling pressured to act immediately regardless of season.

Regional Strategy: Where to Focus Valuation Efforts

The persistent north-south divide in UK property performance requires location-specific valuation strategies. Northern regions continue outperforming southern markets[2], creating different opportunity profiles:

Northern England and Scotland 🏴

- Stronger price growth momentum

- Better affordability relative to local wages

- Emerging regeneration areas offering value appreciation potential

- Lower absolute entry prices for first-time buyers

Southern England 🏛️

- Softer price growth but greater absolute values

- Potential for better long-term capital appreciation

- Higher quality employment opportunities in many areas

- Stretched affordability despite improvements

Midlands and Wales 🏴

- Balanced markets between northern growth and southern softness

- Strong fundamentals with improving infrastructure

- Competitive pricing with good quality housing stock

- Attractive for remote workers seeking value

First-time buyers should prioritize locations based on:

- Employment opportunities and career trajectory

- Lifestyle preferences and community characteristics

- Commuting requirements and transport infrastructure

- Long-term appreciation potential based on development plans

- Affordability metrics relative to household income

Working with chartered surveyors with local market expertise ensures valuations reflect area-specific dynamics rather than generic national trends.

Government Schemes and Valuation Requirements

Several government initiatives continue supporting first-time buyers in 2026, each with specific valuation requirements:

Help to Buy Equity Loan Scheme

While the scheme closed to new applications in October 2022 for most of England, existing participants may still require valuations for staircasing or final redemption. Help to Buy valuations must follow specific protocols to determine fair market value for equity calculations.

Shared Ownership Programs

These schemes allow buyers to purchase a share (typically 25-75%) of a property and pay rent on the remaining portion. RICS shared ownership valuations ensure fair pricing for both initial purchase and subsequent staircasing transactions.

Right to Buy Schemes

Council and housing association tenants may qualify for significant discounts when purchasing their rented homes. RICS Right to Buy valuations determine market value before discount application, ensuring both buyer and seller receive fair treatment.

Mortgage Valuation vs. Independent Valuation

Understanding the distinction between lender-required mortgage valuations and independent buyer valuations is crucial:

Mortgage Valuation (Lender's Interest)

- ❌ Basic assessment to protect lender's security

- ❌ May not identify significant defects

- ❌ Often desktop-only without property visit

- ❌ Limited detail and explanation

- ❌ Serves lender, not buyer

Independent Valuation (Buyer's Interest)

- ✅ Comprehensive market value assessment

- ✅ Detailed property inspection

- ✅ Identification of value-affecting factors

- ✅ Negotiation leverage and decision-making support

- ✅ Buyer's interests prioritized

In 2026's improved but still complex market, the relatively modest cost of an independent valuation (typically £300-800 depending on property value and location) provides substantial protection against overpaying on what will likely be the largest purchase of a first-time buyer's life.

Practical Steps: Executing Your Valuation Strategy

Implementing an effective valuation strategy requires systematic preparation and professional engagement:

Step 1: Financial Preparation and Budget Clarity

Before commissioning valuations, establish clear financial parameters:

- Mortgage agreement in principle confirming borrowing capacity

- Deposit funds readily accessible and documented

- Additional costs budget for surveys, valuations, legal fees, and moving expenses

- Monthly payment comfort level considering the 32% mortgage-to-income guideline[1]

Step 2: Property Research and Shortlisting

Leverage the 6% increase in available stock[1] to create a robust shortlist:

- Research multiple properties in target areas

- Attend viewings with detailed checklists

- Document property features, condition, and concerns

- Compare asking prices against recent sales data

- Identify 2-3 serious candidates before commissioning valuations

Step 3: Commission Professional Valuations

Engage RICS-qualified surveyors for comprehensive assessments:

- Schedule valuations for shortlisted properties

- Provide surveyors with complete property information

- Request detailed written reports with comparable evidence

- Ask questions about methodology and findings

- Consider combining valuation with comprehensive survey services

Step 4: Analyze and Compare Results

Review valuation reports systematically:

- Compare valuation figures against asking prices

- Identify properties offering best value relative to market

- Note condition issues affecting value or requiring remediation

- Calculate total cost of ownership including identified repairs

- Prioritize properties based on value, condition, and suitability

Step 5: Strategic Offer Formulation

Use valuation evidence to craft compelling offers:

- Base offers on valuation evidence rather than asking prices

- Include valuation report excerpts in offer justification

- Negotiate repairs, price reductions, or seller contributions

- Remain prepared to walk away from overpriced properties

- Leverage inventory levels to maintain negotiating strength

Step 6: Due Diligence and Completion

Following offer acceptance, complete remaining due diligence:

- Commission comprehensive building survey if not already completed

- Review legal documentation and title searches

- Confirm mortgage approval and finalize lending arrangements

- Coordinate completion timeline with all parties

- Plan move logistics and immediate property requirements

Common Valuation Pitfalls to Avoid

First-time buyers should be aware of frequent mistakes that can undermine valuation benefits:

❌ Relying Solely on Online Estimates

Automated valuation models (AVMs) from property portals provide rough guidance but lack the nuance of professional assessments. They cannot account for property-specific condition, recent improvements, or micro-location factors.

❌ Skipping Independent Valuations to Save Money

The £300-800 cost of professional valuation is negligible compared to the potential cost of overpaying by 5-10% on a £300,000 property (£15,000-30,000). This represents false economy with substantial downside risk.

❌ Ignoring Regional Market Dynamics

Applying national market trends to local decisions overlooks the significant regional variations characterizing the 2026 market[2]. Northern and southern markets require different analytical approaches.

❌ Confusing Asking Price with Market Value

The 2.8% jump in asking prices between December and February[1] reflects seller optimism rather than necessarily justified market value. Independent valuations provide objective reality checks.

❌ Overlooking Condition Issues

Cosmetic presentation can mask significant defects affecting long-term value. Professional valuations identify these issues before they become expensive surprises.

❌ Rushing Due to Market FOMO

Despite increased activity levels, the 6% higher inventory[1] means buyers have options. Rushing valuation and survey processes to avoid "missing out" often leads to poor decisions.

Conclusion: Maximizing First-Time Buyer Success in 2026

Preparing Valuations for First-Time Buyers in 2026: Leveraging Improved Affordability and Supply Trends represents a fundamental shift from the challenging market conditions that characterized recent years. With 40% of homes now purchasable with mortgage payments below local rents[1], mortgage rates below 4%[2], and housing stock 6% above year-ago levels[1], the structural conditions favor well-prepared first-time buyers.

Professional valuation services provide the foundation for confident, informed decision-making in this improved but still complex market. By understanding true market value, identifying condition issues, and leveraging objective evidence in negotiations, first-time buyers can maximize their purchasing power and secure properties that represent genuine long-term value.

Your Next Steps

To capitalize on 2026's improved market conditions:

- Secure mortgage agreement in principle to clarify your budget and demonstrate seriousness to sellers

- Engage RICS-qualified surveyors early in your property search for valuation and survey expertise

- Research target locations thoroughly, understanding regional performance dynamics and future development plans

- Create systematic property evaluation criteria incorporating both valuation metrics and personal requirements

- Maintain negotiating discipline by being prepared to walk away from overpriced properties

- Plan comprehensively for all costs including surveys, valuations, legal fees, and post-purchase expenses

The combination of normalized affordability metrics, increased housing supply, and professional valuation expertise creates an unprecedented opportunity window for first-time buyers. Those who approach the market strategically—armed with professional valuations, comprehensive surveys, and realistic expectations—are positioned to secure excellent value in properties that will serve as solid foundations for long-term financial security.

The 2026 market rewards patience, preparation, and professional guidance. By leveraging improved affordability and supply trends through rigorous valuation protocols, first-time buyers can confidently navigate property purchase and achieve successful homeownership outcomes.

References

[1] Uk Property March 2026 – https://www.garrington.co.uk/market-review/uk-property-march-2026/

[2] Uk House Prices Hit New High As Market Gathers Pace In Early 2026 – https://propertysoup.co.uk/uk-house-prices-hit-new-high-as-market-gathers-pace-in-early-2026/

[3] Whats Outlook Uk House Prices 2026 – https://global.morningstar.com/en-gb/personal-finance/whats-outlook-uk-house-prices-2026