Moving an EPC rating from F to C can add approximately 16% to a property's sale price — yet the majority of residential valuations in 2026 still treat energy performance as a footnote rather than a core valuation driver [1]. That gap between market reality and valuation practice is closing fast, and surveyors who fail to bridge it risk producing reports that neither lenders nor buyers can rely on.

Valuing Homes with EPC‑Led Retrofit Potential: How Surveyors Should Reflect Upgrade Costs and Future Savings is no longer a niche topic for green mortgage specialists. It sits at the heart of mainstream residential valuation as the UK property market bifurcates along energy-efficiency lines. This article sets out a practical, Red Book–compliant framework for reflecting retrofit potential in residential valuations — going well beyond simple EPC band commentary to address costed upgrade works, anticipated bill savings, and emerging lender requirements.

Key Takeaways 📌

- EPC ratings are now a primary price driver, with poor-rated homes facing measurable discounts and energy-efficient homes commanding premiums of up to £40,000 [1].

- Surveyors should present three linked value figures: as-is value, as-improved value, and EPC-led potential — especially where retrofit is credible and costed.

- A residual valuation approach — deducting reasonable retrofit costs from post-works market value — provides a defensible, Red Book–compatible methodology.

- Net-present-value (NPV) of energy bill savings offers a quantifiable basis for value adjustments when comparable sales evidence is thin.

- Green mortgage criteria from major lenders are now directly influencing achievable prices, making EPC status a loan-term variable as well as a market variable [7].

Why EPC Ratings Have Become a Central Valuation Variable

For much of the past decade, EPC ratings appeared in survey reports as a compliance note — useful for buyers, but rarely influencing the final figure. That era is over.

By 2026, a clear market bifurcation has emerged. Energy-efficient homes sell faster and achieve stronger prices, while low-rated stock faces longer marketing periods and buyer-driven discounts [7]. Engel & Völkers' analysis of European residential markets confirms that properties with excellent energy ratings achieve significantly higher sales prices than comparable unrenovated buildings, while low-rated homes "often have to accept noticeable discounts" as buyers factor in future retrofit costs [2].

The numbers are striking:

| EPC Improvement | Estimated Value Uplift |

|---|---|

| G → A | Up to £40,000 (Halifax/Santander data) [1] |

| F → C | ~16% increase in sale price [1] |

| D → B | Meaningful premium in most markets [4] |

Rightmove's Green Homes Report underpins much of this evidence, and while the original dataset runs to mid-2022, its findings continue to inform valuation commentary in 2025–26 [1]. Critically, 70% of buyers now believe correctly fitted energy efficiency measures (EEMs) positively affect market value [1] — a buyer sentiment shift that surveyors cannot ignore when assessing market evidence.

The Regulatory Pressure Behind the Numbers

Government policy is amplifying market forces. Proposed minimum EPC requirements for rental properties and the broader trajectory toward net zero mean that low-rated homes carry regulatory obsolescence risk — a factor that Red Book guidance requires valuers to consider when assessing market value. A property that may require £20,000–£30,000 of mandatory works within five years is not the same asset as one that already meets future standards [8].

Understanding what surveyors do in this context means recognising that energy performance assessment is now an integral part of condition reporting, not an add-on.

A Practical Valuation Framework for EPC‑Led Retrofit Potential

Valuing Homes with EPC‑Led Retrofit Potential: How Surveyors Should Reflect Upgrade Costs and Future Savings requires a structured, three-tier approach. The framework below is compatible with RICS Red Book (Global Standards) requirements and reflects emerging best practice from lender and valuation commentary in 2026 [3].

Tier 1: As-Is Market Value

The starting point is the conventional market value based on current condition and EPC rating. This figure should:

- Reference comparable sales evidence adjusted for EPC band where data allows

- Explicitly note the current EPC rating and band as a market-facing characteristic

- Flag any mandatory compliance risk (e.g., properties below EPC E for rental use)

- Avoid double-counting — if comparables already reflect poor energy performance, no further deduction is needed

💡 Pull Quote: "The as-is value is not the end of the analysis — it is the baseline from which retrofit potential is measured."

Tier 2: As-Improved Value (Post-Retrofit)

Where a credible retrofit plan exists or can be reasonably modelled, surveyors should estimate the market value assuming works are completed to achieve a target EPC band (typically C or above). This involves:

- Identifying the target EPC band — usually EPC C as a minimum, given lender and regulatory benchmarks

- Modelling post-works comparables — selecting sales evidence from similar properties already at the target band

- Adjusting for location and property type — energy efficiency premiums vary by market; a £40,000 premium in London may be £8,000–£12,000 in a lower-value market [1]

- Noting assumptions clearly — the as-improved value must be presented as conditional on works being completed to a specified standard

For properties where a Level 3 building survey has already identified structural or fabric issues, the as-improved value must account for remediation works before retrofit measures are applied.

Tier 3: EPC‑Led Retrofit Potential (Residual Approach)

The third figure bridges Tiers 1 and 2 using a residual valuation methodology:

EPC-Led Retrofit Potential = As-Improved Value − Reasonable Retrofit Costs − Developer's Profit/Risk Allowance

This approach, recommended in March 2026 valuation briefings for RICS-registered surveyors [3], provides a defensible basis for valuing properties where:

- Current condition is poor but retrofit is financially viable

- The buyer is likely to undertake works (e.g., a developer, landlord, or owner-occupier with a green mortgage)

- Market comparables at the current EPC band are thin or distorted

Typical Retrofit Cost Ranges (2026 UK Market)

| Measure | Estimated Cost Range |

|---|---|

| Loft insulation | £300 – £600 |

| Cavity wall insulation | £500 – £1,500 |

| Solid wall insulation (external) | £8,000 – £22,000 |

| Air source heat pump | £7,000 – £15,000 |

| Triple glazing (full house) | £6,000 – £15,000 |

| Solar PV (4kW system) | £5,000 – £9,000 |

| Full deep retrofit (EPC F→C) | £15,000 – £45,000 |

Note: Costs vary significantly by property type, size, and region. Surveyors should use local contractor evidence where available.

Avoiding the Double-Count Trap ⚠️

A critical discipline in this framework is avoiding double-counting. If a buyer has already negotiated a price reduction reflecting poor EPC performance, applying a further retrofit cost deduction in the valuation overstates the discount. Surveyors must assess whether:

- The agreed price already reflects EPC-related obsolescence

- Comparable evidence used has been adjusted for EPC differences

- Any retrofit grant funding (e.g., Great British Insulation Scheme, ECO4) reduces the net cost to the buyer

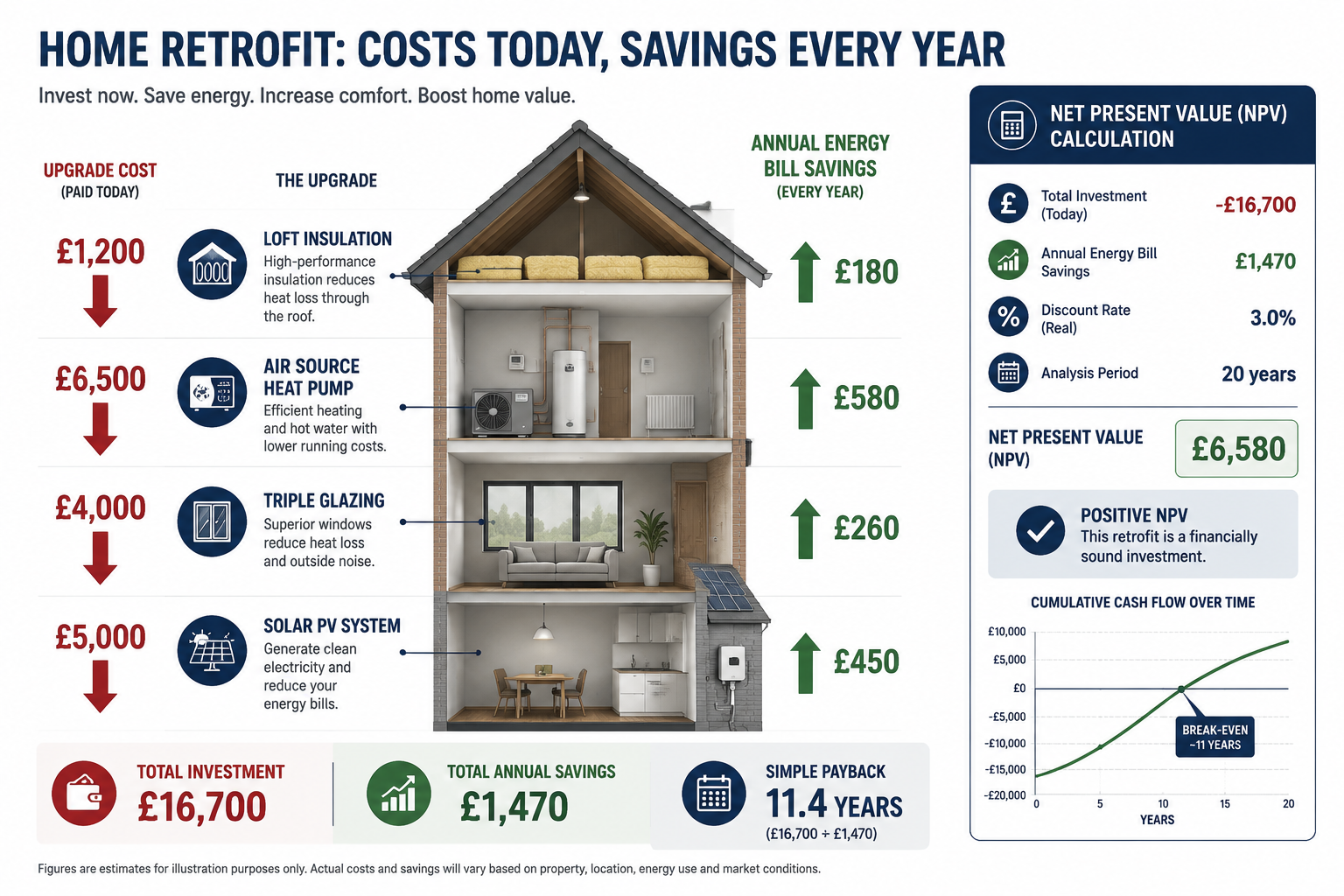

Quantifying Energy Savings: From Bill Reductions to Value Uplift

One of the most powerful — and underused — tools in Valuing Homes with EPC‑Led Retrofit Potential: How Surveyors Should Reflect Upgrade Costs and Future Savings is the net-present-value (NPV) of anticipated energy bill savings. This approach is particularly useful where comparable sales evidence is limited or where a valuer needs to support an uplift figure.

The Savings Differential

New-build data for 2026 show that A–B rated three-bedroom homes typically carry combined heating and electricity bills of around £800–£1,200 per year [5]. By contrast, existing stock at EPC D–F can cost £2,500–£4,500 annually to run, depending on fuel type and property size [6]. That differential — potentially £1,500–£3,000 per year — is a real financial benefit that buyers increasingly price into offers.

NPV Calculation: A Worked Example

Assume a semi-detached house currently rated EPC E with annual energy costs of £3,200. Post-retrofit to EPC C, costs fall to £1,400 — a saving of £1,800/year.

Using a simple NPV model over 15 years at a 5% discount rate:

NPV of savings ≈ £18,600

This figure does not automatically translate into a £18,600 value uplift — purchaser behaviour, discount rates, and market sentiment all moderate the relationship. However, it provides a quantified, transparent basis for commentary on energy-related value adjustments, which is increasingly expected in green mortgage assessments and retrofit-oriented valuation reports [9].

💡 Pull Quote: "Translating annual bill savings into a net-present-value figure gives surveyors a defensible, data-driven anchor for EPC-related value commentary."

Green Mortgages: When EPC Affects Loan Terms

Green mortgage products from major lenders now offer preferential rates for EPC A and B properties — typically 0.1%–0.4% below standard rates. This directly affects purchaser affordability and, by extension, achievable price [7]. Surveyors should note where:

- A property qualifies (or would qualify post-retrofit) for green mortgage products

- The rate differential materially affects buyer demand in the subject market

- A lender's minimum EPC requirement (commonly EPC C for new lending on buy-to-let) affects the pool of eligible buyers

For buyers exploring financing options, understanding the home report cost and process is a useful starting point before engaging with green mortgage providers.

Referencing Savings in Valuation Reports

Surveyors are not energy assessors, and reports should be clear about the basis of any savings figures cited. Best practice in 2026 includes:

- Referencing the existing EPC's recommended improvements and their estimated cost/saving ranges

- Citing published energy cost benchmarks (e.g., Ofgem price cap data, EST typical bill figures) rather than bespoke calculations

- Noting uncertainty — actual savings depend on occupant behaviour, future energy prices, and works quality

- Distinguishing between energy cost savings and carbon savings — both are relevant but serve different audiences

Practical Guidance for Red Book–Compliant EPC Valuation Reporting

What Must Appear in the Report

A Red Book–compliant valuation addressing EPC-led retrofit potential should include:

- ✅ Current EPC rating and band (or note if no valid EPC exists)

- ✅ Identification of key energy efficiency measures recommended in the EPC

- ✅ Estimated cost range for works to achieve target band (sourced and referenced)

- ✅ As-is market value with EPC-related adjustments to comparables explained

- ✅ As-improved value (conditional, with assumptions stated)

- ✅ Commentary on green mortgage eligibility and lender requirements

- ✅ NPV of savings (indicative, with caveats) where comparables are thin

- ✅ Statement on double-count risk and how it has been addressed

Choosing the Right Survey Type

The depth of EPC-related commentary appropriate in a valuation report depends partly on the survey level commissioned. A Level 2 HomeBuyer Survey will flag EPC issues and recommend further investigation, while a Level 3 Building Survey provides the fabric-level detail needed to cost retrofit works accurately. For properties where EPC-led value is a significant factor — typically older stock below EPC D — a Level 3 survey is strongly advisable before committing to a residual valuation approach.

Buyers unsure which survey level suits their property can use the what survey do you need tool to identify the right starting point.

Soft Markets and EPC Potential

In flat or softening markets, EPC-driven retrofit potential can justify values at the upper end of the comparable range — but only where three conditions are met [3]:

- A clear, costed retrofit plan exists (or can be credibly modelled)

- Works would lift the property to at least EPC C

- The cost-to-benefit ratio is demonstrable using local sales evidence

Where these conditions are not met, surveyors should resist pressure to inflate values on the basis of speculative retrofit potential. The residual approach provides discipline: if retrofit costs consume the entire uplift, the EPC-led potential adds no value above the as-is figure.

Damp, Structural Issues, and Retrofit Sequencing

A frequently overlooked issue is retrofit sequencing. Installing insulation or a heat pump in a property with unresolved damp or structural defects can cause significant harm — trapping moisture, voiding warranties, and reducing the effectiveness of measures. Surveyors should flag where damp surveys or structural surveys are needed before retrofit costs can be reliably estimated. Failing to sequence works correctly can turn a £20,000 retrofit into a £35,000 remediation project.

Conclusion: Actionable Next Steps for Surveyors in 2026

The property market in 2026 is pricing energy performance with increasing precision. Valuing Homes with EPC‑Led Retrofit Potential: How Surveyors Should Reflect Upgrade Costs and Future Savings is no longer optional guidance — it is the standard that lenders, buyers, and regulators are beginning to expect.

Here are the key actions surveyors should take now:

- Adopt the three-tier framework (as-is, as-improved, EPC-led potential) as standard practice for properties below EPC C.

- Build a local cost database for common retrofit measures — contractor quotes, grant availability, and regional variations all affect the residual calculation.

- Integrate NPV of savings commentary into reports where comparable evidence is thin, with clear caveats on assumptions.

- Check green mortgage eligibility criteria for major lenders before finalising valuation figures — loan-term differences affect achievable prices.

- Recommend appropriate survey depth — Level 3 surveys are essential where fabric condition affects retrofit cost estimates.

- Address damp and structural issues first — flag sequencing risks explicitly to avoid underestimating total upgrade costs.

- Avoid double-counting — always assess whether agreed prices or comparable adjustments already reflect EPC-related discounts.

The surveyors who master this framework will produce valuations that are more accurate, more defensible, and more useful to every party in the transaction. Those who continue to treat EPC ratings as a footnote will find their reports increasingly challenged by lenders, buyers, and the market itself.

References

[1] Retrofit Increases House Value – https://www.refurbandretrofit.com/retrofit-increases-house-value/

[2] Energy Efficient Real Estate – https://www.engelvoelkers.com/de/en/resources/energy-efficient-real-estate

[3] Energy Efficiency Retrofit Valuations In Flat Markets Assessing Epc Improvements When Buyer Demand Softens – https://princesurveyors.co.uk/blog/energy-efficiency-retrofit-valuations-in-flat-markets-assessing-epc-improvements-when-buyer-demand-softens/

[4] The Impact Of Epc Ratings On Property Value And Marketability – https://propertybox.io/blog/the-impact-of-epc-ratings-on-property-value-and-marketability/

[5] The 2026 New Home Features That Deliver Real Value – https://www.newhomesforsale.co.uk/resources/buying-advice/the-2026-new-home-features-that-deliver-real-value/

[6] Future Proofing Your Yield The 2026 Energy Retrofit Guide For Bedfordshire Landlords – https://www.country-properties.co.uk/guides/landlords/future-proofing-your-yield-the-2026-energy-retrofit-guide-for-bedfordshire-landlords/

[7] Energy Efficiency And Property Value The Role Of Epc Ratings In 2026 – https://cucumbereco.co.uk/blog/energy-efficiency-and-property-value-the-role-of-epc-ratings-in-2026

[8] Epc Ratings Energy Efficiency 2026 All You Need To Know – https://www.cartermay.co.uk/epc-ratings-energy-efficiency-2026-all-you-need-to-know/

[9] S0378778826000897 – https://www.sciencedirect.com/science/article/pii/S0378778826000897

[10] New Epc System 4 Metrics Explained – https://myepcupgrade.co.uk/new-epc-system-4-metrics-explained/