Nearly one in five first-time buyers in England used either a shared ownership or Help to Buy scheme to get onto the property ladder in recent years — yet the majority of them skipped an independent building survey entirely. That oversight can cost thousands. Building surveys for shared ownership and Help to Buy homes: defects, valuation gaps and advising first-time buyers is a topic that sits at the intersection of technical surveying, consumer protection, and scheme-specific legal complexity. Surveyors who understand these schemes deeply are better placed to protect inexperienced buyers from hidden risks that standard mortgage valuations simply do not cover.

Key Takeaways 📋

- New-build shared ownership and Help to Buy properties carry unique snagging and construction defects that a basic mortgage valuation will never identify.

- Valuation gaps are a real and measurable risk — particularly with Help to Buy equity loans, where independent surveyor valuations often differ from developer asking prices.

- Staircasing costs are directly tied to property value, making an accurate survey and valuation critical before any share purchase.

- First-time buyers are the most vulnerable group in these schemes and need clear, jargon-free advice from their surveyor.

- A Level 3 Building Survey is the most appropriate inspection type for older shared ownership properties; a snagging survey is essential for brand-new builds.

Understanding Shared Ownership and Help to Buy: What Surveyors Need to Know

Before picking up a damp meter or drafting a report, surveyors advising clients in these schemes must understand the legal and financial framework they are operating within.

Shared Ownership: The Basics

Under shared ownership, a buyer purchases a percentage of a property — typically between 10% and 75% — and pays rent on the remaining share to a housing association. The buyer can then staircase (purchase additional shares) over time until they own 100%.

Key scheme features that affect survey scope:

| Feature | Surveyor Implication |

|---|---|

| Leasehold title (almost always) | Lease length, service charge, and ground rent must be checked |

| Housing association as co-owner | Repair obligations may be split — check the lease carefully |

| Staircasing provisions | Future valuations will determine cost of buying additional shares |

| Resale restrictions | Some schemes restrict who can buy, affecting future market value |

Help to Buy Equity Loan: What Changed in 2021 and Beyond

The original Help to Buy Equity Loan scheme closed to new applicants in March 2023. However, tens of thousands of properties purchased under the scheme remain in circulation, and buyers are now approaching surveyors to help them understand their position when remortgaging, staircasing, or selling.

Under the scheme, the government lent buyers up to 20% (40% in London) of the property value interest-free for five years. After that, interest charges apply. For surveyors in 2026, the most common instructions involve:

- Redemption valuations — establishing current market value so the equity loan can be repaid

- Resale surveys — advising new buyers purchasing a former Help to Buy property on the open market

- Defect investigations — identifying construction issues that have emerged since the original build

💡 Pull Quote: "A mortgage valuation protects the lender. A building survey protects the buyer. In shared ownership and Help to Buy transactions, that distinction has never mattered more."

Common Defects Found in Shared Ownership and Help to Buy Properties

The vast majority of shared ownership and Help to Buy properties are new-build or near-new constructions. This creates a specific defect profile that differs significantly from older housing stock. Surveyors conducting building surveys for shared ownership and Help to Buy homes must be alert to construction quality issues that are common in volume housebuilding.

Snagging Defects: The Hidden Epidemic

Snagging defects are minor (and sometimes major) construction faults left unresolved at handover. Research by consumer groups has consistently found that the average new-build home in the UK has between 100 and 150 snagging issues at the point of completion.

Common snagging defects include:

- 🔲 Poorly fitted windows and doors — gaps in seals, misaligned frames, draughts

- 💧 Inadequate drainage falls — flat or reverse-fall gutters causing overflow and damp penetration

- 🧱 Cracked render and pointing — often caused by thermal movement in fast-built structures

- ⚡ Electrical and plumbing snags — incomplete connections, poorly secured pipework

- 🏠 Roof defects — missing or slipped tiles, inadequate felt laps, poorly sealed flashings

- 🌊 Damp and condensation — especially in ground-floor flats with inadequate sub-floor ventilation

For buyers purchasing a shared ownership flat or house that is still within the developer's warranty period (typically the NHBC Buildmark 10-year warranty), identifying these defects early is financially critical. Once the warranty expires, repair costs fall on the leaseholder — even if the defect originated during construction.

Surveyors should recommend a professional snagging survey for any new-build purchase, regardless of scheme type.

Structural and Fabric Issues in Older Shared Ownership Stock

Not all shared ownership properties are new builds. Housing associations have been operating since the 1980s, and some shared ownership homes are now 20–40 years old. These properties present a very different defect profile:

- Flat roof deterioration — common in 1980s and 1990s housing association blocks

- Spalled brickwork and failed pointing — particularly on exposed elevations

- Subsidence and settlement — especially in clay-rich areas of London and the South East

- Asbestos-containing materials — present in many pre-2000 buildings, particularly in communal areas

For these older properties, a Level 3 Building Survey is the appropriate inspection level. A HomeBuyer Report (Level 2) may miss significant structural or fabric issues that could affect the buyer's ability to staircase or sell in the future.

Communal Areas and the Shared Ownership Complication

One of the most overlooked aspects of shared ownership surveys is the communal fabric. In a leasehold flat, the buyer's service charge funds repairs to the building envelope, communal areas, and shared systems. If the roof is failing or the lift needs replacing, the leaseholder will be billed — regardless of what share of the property they own.

Surveyors should:

- Inspect communal areas as thoroughly as the individual unit

- Request sight of recent service charge accounts and any Section 20 major works notices

- Flag any visible deterioration in the building envelope that could trigger large future bills

- Consider recommending a specialist roof survey if the roof condition is unclear

Valuation Gaps, Staircasing Risks and the Surveyor's Role

This is the area where building surveys for shared ownership and Help to Buy homes: defects, valuation gaps and advising first-time buyers becomes most technically demanding — and where the surveyor's advice can have the greatest financial impact.

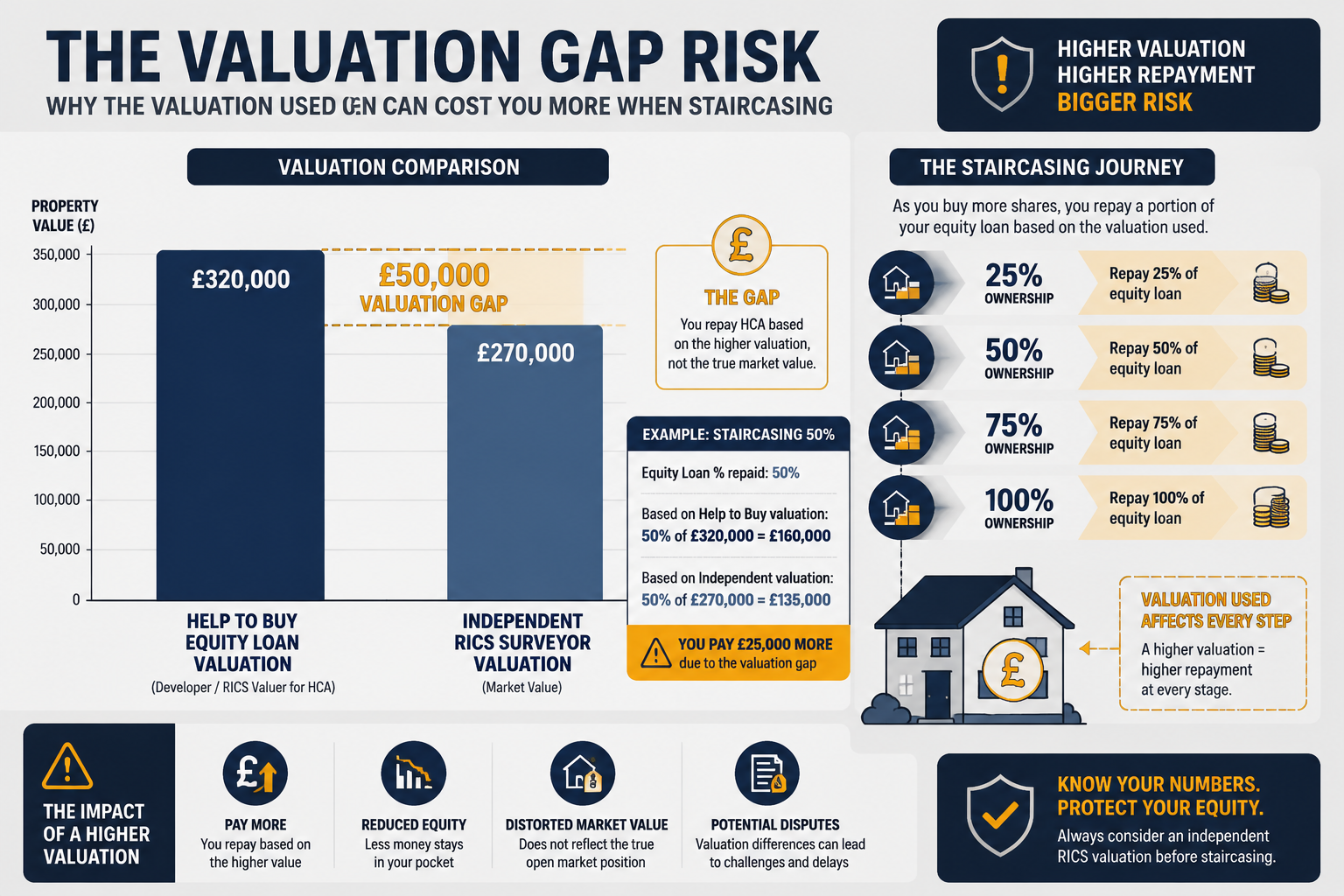

The Valuation Gap Problem

A valuation gap occurs when the price paid for a property (or the price used to calculate an equity loan) is higher than the true open market value established by an independent RICS surveyor.

In the Help to Buy context, this gap emerged because:

- Developers set asking prices based on their own valuations, which were sometimes optimistic

- The government's equity loan was calculated as a percentage of the developer's asking price

- Independent surveyors — when instructed — sometimes valued properties below the asking price

Why does this matter now? When a buyer repays their Help to Buy equity loan, the government receives the same percentage of the current market value. If the property has not increased in value as expected, or if it was overvalued at purchase, the buyer may owe more than anticipated — or find themselves in negative equity on their personal share.

Staircasing and the Valuation Cycle

Every time a shared ownership buyer staircases, the price of the additional share is calculated based on an independent RICS valuation at that point in time. This means:

- If the property has increased significantly in value, staircasing becomes more expensive

- Defects identified in a building survey can reduce the valuation, potentially making staircasing cheaper

- Unidentified defects that emerge after staircasing become the buyer's sole financial responsibility

⚠️ Important: Surveyors should make clear to clients that the staircasing valuation is a separate instruction from the building survey — but the two are closely linked. A defect-heavy survey report should prompt a conversation about how those defects might affect the staircasing valuation.

Comparable Evidence and New-Build Valuations

One of the most challenging aspects of valuing shared ownership and Help to Buy properties is the lack of comparable evidence. In a new-build development, all sales may be to scheme buyers, making it difficult to establish true open market value.

Surveyors should:

- Look beyond the development for comparable evidence from the wider area

- Adjust for the leasehold nature of the property (particularly short leases or onerous ground rents)

- Consider the impact of any identified defects on the valuation figure

- Be transparent in their report about the limitations of available comparable evidence

For clients who need a formal valuation report — whether for staircasing, remortgaging, or Help to Buy redemption — a RICS-compliant valuation report from a qualified surveyor is essential.

Advising First-Time Buyers: Communication, Clarity and Duty of Care

The technical aspects of building surveys for shared ownership and Help to Buy homes are only half the challenge. The other half is communicating findings clearly to buyers who may have no prior experience of property ownership, surveying, or leasehold law.

Why First-Time Buyers Need a Different Approach

First-time buyers in shared ownership and Help to Buy schemes are often:

- Young and financially stretched — they have used a government scheme precisely because they could not afford to buy outright

- Unfamiliar with leasehold concepts — service charges, ground rent, and staircasing are new concepts

- Emotionally invested — they have worked hard to get onto the ladder and may be reluctant to hear bad news

- Unaware of their rights — many do not know they can negotiate with developers or housing associations over defects

Surveyors have a professional and ethical duty to ensure their reports are understood, not just delivered. A technically accurate report that the client cannot interpret is of limited value.

Practical Communication Tips for Surveyors

✅ Use plain English — avoid jargon like "spalling," "efflorescence," or "interstitial condensation" without explanation

✅ Prioritise findings clearly — use a traffic light system or numbered priority list so buyers know what needs immediate attention

✅ Explain the financial implications — link defects to likely repair costs and to future staircasing or resale value

✅ Address the lease — flag any lease terms that could affect future costs or the ability to sell

✅ Recommend specialists — where issues require further investigation (e.g., structural movement, damp surveys, or asbestos surveys), say so clearly and explain why

What to Include in a Shared Ownership Survey Report

A well-structured report for a shared ownership or Help to Buy property should cover:

| Report Section | Key Content |

|---|---|

| Property description | Tenure, lease details, share being purchased |

| Structural condition | Foundations, walls, roof, floors |

| Services | Heating, plumbing, electrical (visual inspection) |

| Communal areas | Building envelope, shared services, visible defects |

| Legal/tenure matters | Lease length, ground rent, service charge history |

| Snagging schedule | Itemised list of defects with priority ratings |

| Valuation commentary | Market context, comparable evidence, scheme-specific factors |

| Recommendations | Specialist reports, negotiations, legal advice |

Buyers who want to understand the difference between survey types before commissioning an inspection can compare different types of survey to find the most appropriate level of inspection for their property.

Helping Buyers Understand Their Options After the Survey

When a survey reveals significant defects, first-time buyers often feel overwhelmed. Surveyors can add real value by explaining the practical options:

- Negotiate with the developer or housing association — defects within the warranty period should be remedied at no cost to the buyer

- Request a price reduction — if defects are significant and outside warranty, a reduction in the share price may be appropriate

- Walk away — in serious cases, buyers should understand that proceeding is not mandatory

- Commission specialist reports — for issues like subsidence or structural movement, a specialist investigation provides evidence for negotiation

For buyers who are also concerned about the leasehold aspects of their purchase — particularly in older shared ownership blocks — understanding the implications of share of freehold arrangements can also be valuable context.

Conclusion: Actionable Steps for Surveyors and Buyers in 2026

The growth of shared ownership and the legacy of Help to Buy have created a generation of homeowners who are more financially exposed than they realise. Surveyors who specialise in these schemes provide a genuinely protective service — but only if they approach each instruction with scheme-specific knowledge, technical rigour, and clear communication.

Actionable Next Steps

For surveyors:

- 🔍 Always review the lease and scheme documentation before inspection, not after

- 📋 Tailor your report structure to the scheme type — shared ownership and Help to Buy have different risk profiles

- 💬 Build in a post-report call or meeting with first-time buyer clients to explain findings in plain English

- 📊 Be explicit about valuation limitations and the link between defects and future staircasing costs

- 🏗️ Recommend a snagging survey for all new-build instructions, regardless of scheme

For first-time buyers:

- Never rely on the developer's or housing association's own inspection — commission an independent survey

- Ask your surveyor to explain what each defect means for your repair costs and future staircasing

- Check the lease length and service charge history before exchange — not after

- If defects are found, use the survey report as a negotiation tool, not just a record

The stakes in shared ownership and Help to Buy purchases are uniquely high. A thorough, well-communicated building survey is not an optional extra — it is the single most important step a first-time buyer can take to protect their investment.