London's property market has entered uncharted territory in 2026. House price expectations have plummeted from +56% to just +7% year-on-year, according to recent RICS data [4]. This dramatic shift in buyer sentiment has created a complex landscape where traditional property valuation methods no longer tell the complete story. For prospective buyers navigating London's flat market, understanding how to conduct a thorough building survey risk assessment for London's stalled market: identifying value traps in flat price zones has never been more critical.

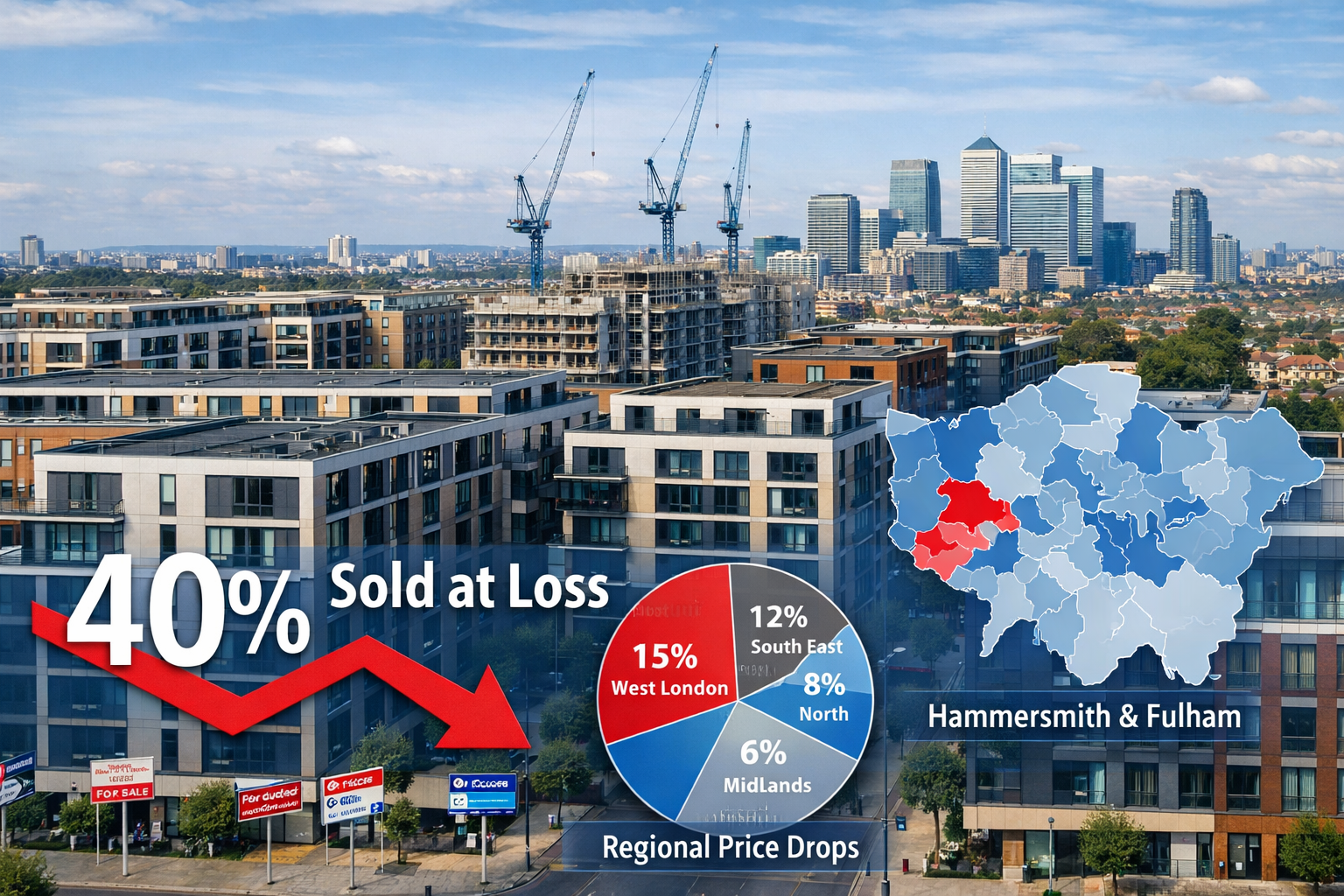

The capital's flat prices have fallen 7% since early 2023, with some boroughs experiencing far steeper declines [3]. Behind these headline figures lies a more troubling reality: approximately 40% of owners who purchased new build flats in the past 20 years sold at a loss in 2025 [3]. When inflation adjustment is factored in, real-term losses reach 25–30% over just five years for many London flat owners [3].

This article provides a comprehensive framework for identifying structural defects, financial liabilities, and market positioning risks that can turn what appears to be a bargain into a long-term financial burden.

Key Takeaways

- London flat prices have declined 7% since early 2023, with 40% of new build flat purchases from the past 20 years resulting in losses when sold in 2025 [3]

- Building survey risk assessments must now incorporate market stagnation factors including service charge escalation, lease terms, and regional depreciation patterns

- Hammersmith and Fulham saw two-thirds of new build flat owners sell at losses, highlighting critical geographic risk concentration [3]

- Professional Level 3 building surveys identify hidden defects that compound value loss in flat price zones where capital appreciation has stalled

- Construction cost inflation exceeding sales prices on 50% of London land signals ongoing supply constraints that create pockets of opportunity alongside widespread risk [5]

Understanding London's Stalled Flat Market in 2026

The Structural Shift in London Property Dynamics

The London property market has undergone a fundamental transformation between 2023 and 2026. The 83% appreciation seen between 2009–2015 now feels like ancient history as the market grapples with multiple headwinds simultaneously [3]. Interest rate increases, the ending of Help to Buy schemes, and escalating service charges have created a perfect storm for flat owners.

According to RICS survey data from February 2026, approximately 40% of UK respondents view the property market to be in a downturn, with another quarter perceiving it to be at the bottom of the cycle [4]. This pessimism is particularly acute in the London flat market, where the combination of high entry prices and stagnant or declining values has trapped many owners.

The average UK house price exceeded £300,000 for the first time in January 2026, with the median house price-to-earnings ratio in Southeast England at approximately 9.3 times earnings [6]. This affordability crisis has reduced transaction momentum, creating a market where properties linger unsold while sellers resist price reductions.

Regional Variation in Depreciation Patterns

Not all London boroughs have experienced equal depreciation. Hammersmith and Fulham experienced the sharpest depreciation, with two-thirds of flat owners who previously bought new properties selling at losses in 2025, based on Land Registry data analysis [3]. This geographic concentration of value destruction highlights the importance of location-specific risk assessment.

Working with chartered surveyors in West London or chartered surveyors in Central London who understand these regional patterns becomes essential when evaluating properties in high-risk zones.

The New Build Flat Crisis

Perhaps the most alarming trend is the performance of new build flats. Approximately 40% of owners who purchased new build flats in the past 20 years sold at a loss in 2025, according to Hamptons estate agent analysis [3]. This statistic challenges the conventional wisdom that new properties offer better long-term value.

Several factors contribute to this phenomenon:

- Premium pricing at purchase that exceeds comparable resale values

- Rapid depreciation once the "new" premium evaporates

- Service charge escalation that outpaces wage growth

- Build quality issues that emerge after warranty periods expire

- Oversupply in specific developments creating internal competition

Building Survey Risk Assessment for London's Stalled Market: Core Methodology

The Enhanced Level 3 Building Survey Approach

In a stalled market, a comprehensive Level 3 building survey becomes the cornerstone of risk mitigation. Traditional surveys focus primarily on structural defects, but building survey risk assessment for London's stalled market: identifying value traps in flat price zones requires an expanded scope that incorporates financial and market positioning analysis.

A thorough RICS building survey in 2026 should examine:

Structural and Building Fabric Issues:

- Foundation movement and subsidence indicators

- Roof condition and remaining lifespan

- Damp penetration and condensation patterns

- Window and door condition (particularly in new builds)

- External envelope integrity

- Internal structural alterations and their compliance

Service and Systems Analysis:

- Heating system age and efficiency

- Electrical installation condition and certification

- Plumbing and drainage functionality

- Ventilation adequacy

- Fire safety compliance (especially in multi-unit buildings)

Lease and Legal Considerations:

- Remaining lease term and extension costs

- Ground rent terms and escalation clauses

- Service charge history and projected increases

- Building insurance arrangements

- Planned major works and reserve fund status

- Cladding issues and remediation liabilities

Critical Red Flags in Flat Price Zones

When conducting building survey risk assessment for London's stalled market: identifying value traps in flat price zones, certain warning signs should trigger immediate concern:

🚩 Service Charge Escalation: Properties with service charges increasing above 5% annually compound value erosion. David Fell, lead analyst at Hamptons, identifies service charge increases as the primary driver of real-term losses [3].

🚩 Short Leases: Flats with less than 80 years remaining on the lease face exponential extension costs. The marriage value calculation kicks in below this threshold, significantly increasing the financial burden.

🚩 Cladding and Fire Safety Issues: Post-Grenfell regulations have created substantial remediation liabilities. Properties with unresolved cladding issues may be unmortgageable and face six-figure repair bills.

🚩 High Ground Rent: Ground rents doubling every 10-15 years create a financial time bomb that erodes capital value and mortgage availability.

🚩 Poor Build Quality: New builds showing premature defects (within 5-10 years) suggest systemic construction issues that will accelerate depreciation.

What Professional Surveyors Look For

Understanding what surveyors look for in a house survey helps buyers appreciate the depth of analysis required. In London's stalled market, chartered surveyors apply heightened scrutiny to:

| Assessment Area | Standard Survey Focus | Enhanced Stalled Market Focus |

|---|---|---|

| Structural Integrity | Visible defects | Historical movement patterns, repair quality, ongoing settlement |

| Services | Basic functionality | Replacement costs, efficiency ratings, upgrade requirements |

| External Envelope | Weather tightness | Thermal performance, maintenance liability, shared responsibility issues |

| Legal/Lease | Basic terms review | Full financial modeling, comparative analysis, exit strategy viability |

| Market Position | Not typically included | Comparable sales analysis, time on market, price reduction history |

Identifying Value Traps in Flat Price Zones: Practical Assessment Framework

Geographic Risk Mapping

The first step in building survey risk assessment for London's stalled market: identifying value traps in flat price zones involves understanding geographic risk concentration. Certain London areas exhibit higher vulnerability to value traps:

High-Risk Characteristics:

- Boroughs with above-average new build concentration

- Areas with multiple large-scale developments completed 2015-2020

- Locations with declining rental yields

- Neighborhoods experiencing demographic shifts

- Transport infrastructure promise that failed to materialize

Lower-Risk Characteristics:

- Established neighborhoods with diverse housing stock

- Areas with strong local employment centers

- Locations with proven long-term capital growth

- Neighborhoods with tight supply constraints

- Transport-connected zones with completed infrastructure

Engaging chartered surveyors in North West London or other area specialists provides crucial local market intelligence that generic surveys cannot capture.

Financial Liability Assessment

Beyond physical defects, financial liabilities represent the most insidious value traps. A comprehensive assessment must quantify:

Service Charge Analysis:

- Historical annual increases (5-year trend)

- Comparison with similar developments

- Management company efficiency and transparency

- Planned major works and reserve fund adequacy

- Shared facility costs (gyms, concierge, gardens)

Lease Extension Calculations:

- Current lease length

- Marriage value implications

- Freeholder responsiveness and reasonableness

- Statutory vs. negotiated route costs

- Impact on mortgage availability

Remediation Liabilities:

- Cladding and fire safety compliance status

- Building Safety Fund application status

- Shared cost allocation mechanisms

- Timeline for completion

- Impact on insurance and mortgageability

The Rental Yield Reality Check

With London's average monthly rent standing at £2,067 as of February 2026, down 0.5% month-on-month but up 2.0% year-on-year [2], rental yield analysis provides crucial context for investment viability.

Projected rental value growth for 2026 is just 2–3%, broadly matching forecast construction cost inflation [6]. This creates stability but limited uplift for investors. Properties with rental yields below 4% in current market conditions face significant capital appreciation pressure to deliver acceptable total returns.

The large volume of long-term tenancies ending ahead of the Renters' Rights Act implementation on 1 May 2026 [2] has created temporary market distortions. Landlords serving Section 21 notices on sub-market rent properties to reset rental values means some properties may show artificially low current rental income that doesn't reflect market potential.

Construction Quality and Defect Patterns

Only 5% of planned homes were built in the first half of 2025, indicating severe construction pipeline bottlenecks [5]. This supply constraint should theoretically support values, but it also reflects a market where approximately 50% of London land is not viable for development because construction costs exceed potential sales prices [5].

This economic reality has several implications for building survey risk assessment:

- Developers cutting corners: When margins compress, build quality often suffers

- Incomplete developments: Stalled projects leave early buyers in limbo

- Reduced competition: Fewer new builds may support older flat values

- Maintenance backlog: Existing stock deteriorates faster when renovation economics don't work

A detailed Level 3 building survey example demonstrates the depth of investigation required to uncover these issues before commitment.

Regulatory Changes and Their Impact on Survey Requirements

The Renters' Rights Act 2026

The implementation of the Renters' Rights Act on 1 May 2026 fundamentally alters landlord risk management. Possession processes will become slower and more complex under the new legislative framework [2], making tenant quality, referencing, and rent/legal expenses protection policies essential.

For buyers considering buy-to-let investments, this regulatory shift demands enhanced due diligence on:

- Property condition: Higher standards required to attract quality tenants

- Maintenance accessibility: Properties requiring frequent access become problematic

- Tenant appeal: Features that attract stable, long-term tenants gain premium value

- Dispute potential: Properties with ambiguous lease terms or shared responsibility issues create conflict risk

Building Safety and Cladding Regulations

The ongoing evolution of building safety regulations continues to create valuation uncertainty. Properties with unresolved cladding issues face:

- Mortgage restrictions: Many lenders refuse to finance affected properties

- Insurance challenges: Premiums increase dramatically or coverage becomes unavailable

- Remediation costs: Six-figure bills that may fall on leaseholders

- Extended timelines: Years-long resolution processes that freeze transactions

A thorough survey must include specialist assessment of external wall systems and fire safety compliance status. This often requires additional commercial building surveys expertise when dealing with mixed-use developments.

Strategic Decision Framework: When to Walk Away

The Value Trap Decision Matrix

Not every property in a flat price zone represents a value trap. The following framework helps distinguish genuine opportunity from disguised liability:

GREEN LIGHT INDICATORS ✅

- Property priced 15%+ below 2019 peak with no structural defects

- Service charges below £2,000 annually with stable 10-year history

- Lease exceeding 100 years with reasonable ground rent

- No cladding issues or confirmed remediation completion

- Strong rental yield (5%+) with demonstrated tenant demand

- Location in area with employment growth and infrastructure investment

- Evidence of comparable sales at similar price levels

AMBER LIGHT INDICATORS ⚠️

- Property priced at or near 2019 peak with minor defects

- Service charges £2,000-£4,000 annually with moderate increases

- Lease 80-100 years requiring extension within 5 years

- Cladding issues with confirmed funding and timeline

- Moderate rental yield (4-5%) in stable market

- Location in transitional area with mixed signals

- Limited comparable sales requiring price discovery

RED LIGHT INDICATORS 🛑

- Property priced above 2019 peak with any defects

- Service charges exceeding £4,000 annually with accelerating increases

- Lease below 80 years with uncooperative freeholder

- Unresolved cladding issues without funding pathway

- Poor rental yield (below 4%) with declining demand

- Location in area with documented value destruction

- No comparable sales suggesting market failure

The Exit Strategy Test

Before committing to any property in a stalled market, apply the exit strategy test:

"If I needed to sell this property in 3-5 years, what would make it attractive to the next buyer?"

Properties that fail this test—those with accumulating liabilities, deteriorating condition, or adverse market positioning—represent value traps regardless of current price. The survey should explicitly assess resale viability, not just current condition.

Professional Survey Selection and Instruction

Choosing the Right Survey Level

While homebuyer surveys provide basic assessment, building survey risk assessment for London's stalled market: identifying value traps in flat price zones demands the comprehensive approach of a Level 3 survey.

Understanding what is a Level 3 home survey and whether a Level 3 survey is worth it becomes crucial when the property represents a significant financial commitment in an uncertain market.

The additional cost of a Level 3 survey (typically £800-£1,500 for a London flat) pales in comparison to the potential losses from undiscovered defects or financial liabilities. In a market where 40% of new build flat purchases resulted in losses [3], this investment provides essential protection.

Specialist Assessments to Consider

Depending on property characteristics, supplementary specialist surveys may be warranted:

- Drainage surveys: For properties with historical drainage issues or ground floor flats

- Roof surveys: For top floor flats or properties with shared roof responsibility

- Cladding and fire safety assessment: For any flat in buildings above 11 meters

- Lease analysis: Legal review of onerous terms and financial obligations

- Specific defect reports: Detailed investigation of particular concerns identified in initial survey

Timeline and Process Management

Understanding how long house surveys take helps manage transaction timelines. A comprehensive Level 3 survey typically requires:

- Instruction to site visit: 5-10 working days

- Site inspection: 3-6 hours for a typical flat

- Report preparation: 7-14 working days

- Specialist follow-ups: Additional 2-4 weeks if required

In a stalled market where properties remain available for extended periods, buyers have negotiating leverage to ensure adequate survey time without risking the purchase to competing offers.

Negotiation Strategy Based on Survey Findings

Using Survey Results to Renegotiate Price

A comprehensive survey revealing significant defects or financial liabilities provides powerful negotiation leverage. In London's current market, where approximately 40% of respondents view the property market to be in a downturn [4], sellers face pressure to accommodate reasonable price adjustments.

Effective negotiation approach:

- Quantify all identified issues: Convert defects to repair costs with contractor quotes

- Highlight market context: Reference comparable sales and time on market

- Present total liability picture: Combine structural defects with financial obligations

- Propose fair adjustment: Request reduction reflecting genuine cost to remedy

- Maintain transaction momentum: Frame negotiation as path to completion, not deal-breaking

For properties in flat price zones, even modest price reductions (5-10%) can transform a marginal purchase into a viable investment by creating equity buffer against further market stagnation.

When to Walk Away

Some survey findings should trigger immediate withdrawal:

- Structural movement requiring underpinning (£15,000-£50,000+ cost)

- Major damp or water ingress affecting multiple rooms (£10,000-£30,000+)

- Electrical rewiring requirement throughout property (£5,000-£15,000)

- Unresolved cladding issues with no funding pathway (potentially £50,000-£150,000 per flat)

- Service charge arrears or management company insolvency

- Lease disputes or freeholder legal action

The sunk cost of survey fees (£1,000-£2,000) represents excellent value when it prevents a six-figure mistake.

Conclusion: Navigating London's Stalled Market with Confidence

London's property market in 2026 presents unprecedented challenges for flat buyers. With prices down 7% since early 2023 [3], house price expectations plummeting from +56% to +7% year-on-year [4], and 40% of new build flat purchases from the past 20 years resulting in losses [3], the risks have never been higher.

However, market stagnation also creates genuine opportunities for informed buyers who conduct rigorous building survey risk assessment for London's stalled market: identifying value traps in flat price zones. The key differentiator between successful purchases and value traps lies in the quality and comprehensiveness of pre-purchase due diligence.

Actionable Next Steps

For prospective buyers:

- Engage qualified professionals early: Contact RICS registered valuers and chartered surveyors before making offers

- Commission comprehensive Level 3 surveys: Don't compromise on survey quality to save modest costs

- Conduct independent financial analysis: Model service charges, lease extension costs, and rental yields

- Research geographic risk factors: Understand borough-specific depreciation patterns

- Maintain negotiating leverage: Use survey findings to achieve fair pricing

- Plan exit strategy: Only purchase properties with clear resale viability

For current owners considering sale:

- Obtain pre-sale survey: Identify and remedy defects before marketing

- Compile comprehensive documentation: Service charge history, building works, warranties

- Price realistically: Accept market reality rather than chasing 2019 peak values

- Highlight positive factors: Demonstrate stable service charges, long lease, no cladding issues

For investors evaluating opportunities:

- Focus on rental yield fundamentals: With growth projections at just 2-3% [6], income becomes crucial

- Understand regulatory changes: Factor Renters' Rights Act implications into risk assessment

- Diversify geographic exposure: Avoid concentration in high-risk boroughs

- Maintain liquidity reserves: Budget for unexpected remediation or market deterioration

The London flat market will eventually stabilize and recover, but timing remains uncertain. Success in this environment requires patience, rigorous analysis, and willingness to walk away from properties that fail comprehensive risk assessment. By applying the frameworks outlined in this guide and engaging qualified professionals for thorough building surveys, buyers can navigate flat price zones with confidence and identify genuine value amid widespread traps.

The £1,000-£2,000 investment in professional survey services represents the most cost-effective insurance policy available in today's uncertain market. When 40% of new build flat purchases resulted in losses [3] and real-term losses reach 25-30% over five years [3], comprehensive due diligence isn't optional—it's essential.

References

[1] Housing Market Outlook 2026 – https://www.ameripriseadvisors.com/matthew.c.london/insights/housing-market-outlook-2026/

[2] London Rental Market Feb 2026 A Market Reset Before Rra – https://www.baseps.co.uk/blog-posts/london-rental-market-feb-2026-a-market-reset-before-rra

[3] House Price Crash – https://hoa.org.uk/news/house-price-crash/

[4] Uk Economy Property Update February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-economy-property-update-february-2026.pdf

[5] Watch – https://www.youtube.com/watch?v=M-F411s-YJs

[6] The London Southeast Residential Market In 2026 Stability Regulation And The Rebalancing Of Risk – https://www.quantem.co.uk/2026/02/25/the-london-southeast-residential-market-in-2026-stability-regulation-and-the-rebalancing-of-risk/