Builder confidence in March 2026 registered at just 38 points—a figure that represents nearly two years of continuous negativity below the critical 50-point threshold. This persistent weakness signals a fundamental shift in market dynamics that building surveyors and property professionals cannot afford to ignore. Understanding Building Survey Market Sentiment in Early 2026: Navigating Regional Price Divergence and Buyer Uncertainty has become essential for accurate property valuations, client advisement, and strategic planning in an increasingly fragmented marketplace.

The early months of 2026 have revealed a property market characterized by stark regional disparities, aggressive pricing strategies, and deeply uncertain buyer behavior. For chartered surveyors conducting RICS building surveys and property valuations, these conditions demand heightened attention to local market dynamics and a nuanced understanding of how sentiment translates into actual transaction values.

Key Takeaways

- Builder confidence remains below breakeven: The Housing Market Index (HMI) scored 38 in March 2026, marking 24 consecutive months below the 50-point threshold that separates positive from negative sentiment [4]

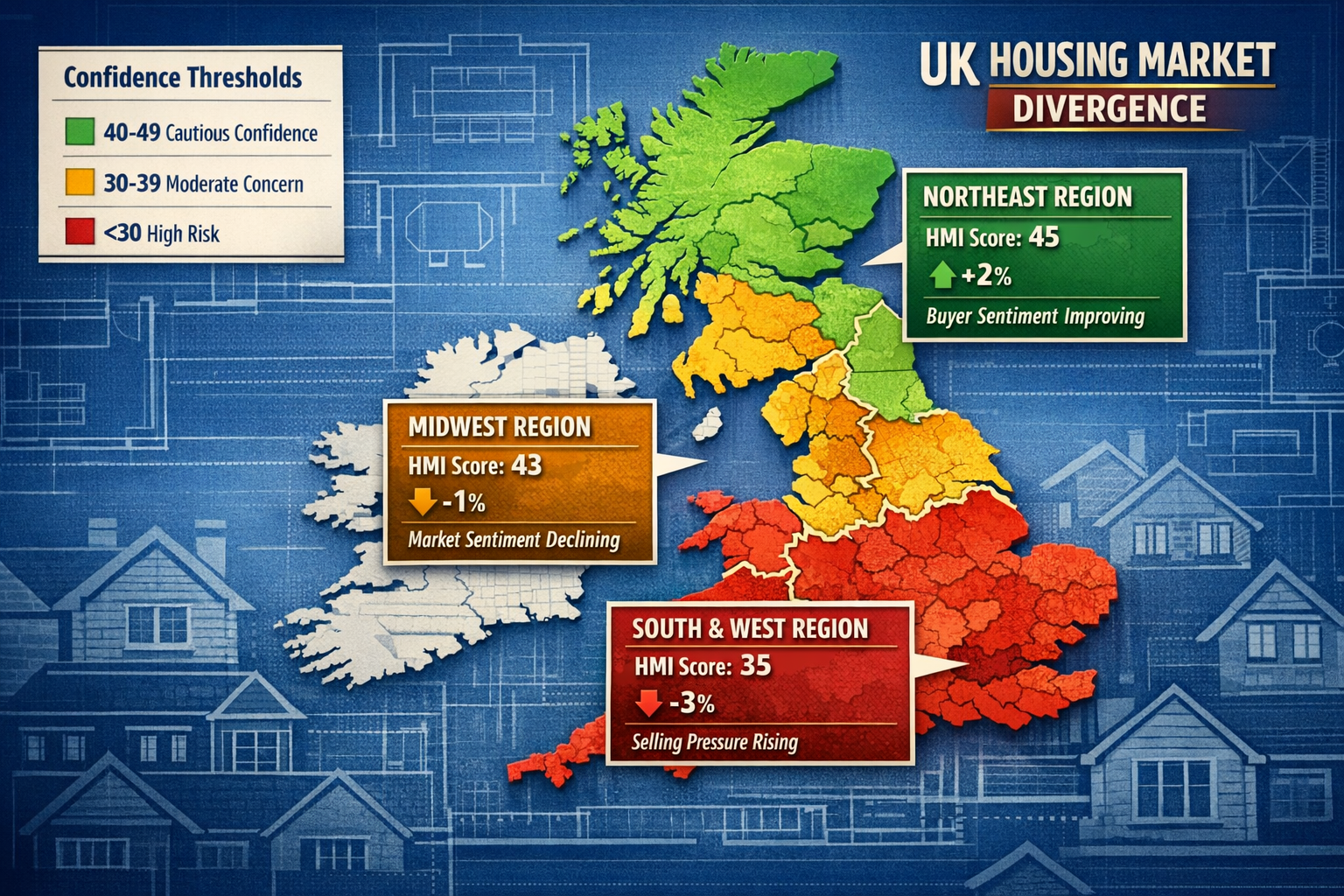

- Regional divergence reaches 10-point spread: The Northeast leads at 45 while the South and West lag at 35, creating significant valuation challenges across different UK regions [3]

- Price reductions persist: 37% of builders cut prices in March, maintaining an average 6% discount, while 64% deployed sales incentives for the 12th consecutive month [4]

- Buyer traffic collapsed: The prospective buyer traffic index dropped to just 23 points, representing one of the lowest demand signals on record [1]

- Short-term outlook weakens: Near-term confidence balance fell to -18%, though 12-month outlook remains stable at +33%, indicating surveyors must balance immediate caution with medium-term optimism

Understanding Building Survey Market Sentiment in Early 2026

The Building Survey Market Sentiment in Early 2026 landscape presents unprecedented challenges for property professionals. The National Association of Home Builders' Housing Market Index, a critical barometer of industry confidence, has consistently signaled distress throughout the first quarter of 2026. This sustained negativity affects how surveyors approach homebuyer surveys and valuation assessments.

The Confidence Crisis Explained

Builder sentiment of 38 indicates that significantly more builders view market conditions as poor rather than good [5]. This pessimism stems from multiple converging factors:

- Elevated mortgage rates continue to suppress buyer purchasing power

- High home prices relative to income ratios create affordability barriers

- Construction cost pressures from materials, labor, and regulatory compliance

- Economic uncertainty affecting consumer confidence and spending decisions

For building surveyors, this negative sentiment translates into tangible valuation considerations. When conducting structural surveys, professionals must account for the reality that distressed market conditions often reveal themselves in negotiated price reductions, extended marketing periods, and increased buyer scrutiny of property defects.

Component Breakdown: What the Numbers Really Mean

The HMI comprises three critical sub-indices that surveyors should monitor closely:

Current sales conditions: This component measures present-day transaction activity and pricing power. In early 2026, this metric reflects the immediate pressure builders face to convert inventory into sales.

Future sales expectations: This forward-looking measure fell to 49 in January—the first time below breakeven since September 2025 [1]. This decline signals diminished optimism about the next six months, suggesting surveyors should adopt conservative valuation approaches for properties requiring extended marketing periods.

Prospective buyer traffic: At just 23 points, this represents a critical weakness in demand signals [1]. Low traffic indicates fewer qualified buyers actively searching, which directly impacts achievable sale prices and negotiation dynamics. When preparing what surveyors check during inspections, this context helps frame realistic market value assessments.

Navigating Regional Price Divergence Across UK Markets

Perhaps the most significant challenge for building surveyors in 2026 is the regional price divergence that has created a patchwork of distinct market conditions. The 10-point spread between the most and least optimistic regions represents substantial valuation complexity [3].

Regional Performance Breakdown

| Region | HMI Score (Jan 2026) | Market Characterization | Surveyor Implications |

|---|---|---|---|

| Northeast | 45 | Approaching neutral | More stable valuations, moderate buyer confidence |

| Midwest | 43 | Cautiously negative | Mixed signals require careful local analysis |

| South | 35 | Deeply negative | Significant price pressure, extended marketing |

| West | 35 | Deeply negative | High discount rates, aggressive incentives |

This regional variation means that surveyors operating across multiple markets must adjust their valuation methodologies and market commentary accordingly. A chartered surveyor in London faces dramatically different conditions than colleagues in Essex or Sussex.

Why Regional Divergence Matters for Valuations

The stark regional differences stem from localized factors including:

✅ Employment market strength: Regions with robust job growth maintain better housing demand

✅ Inventory levels: Areas with oversupply face greater price pressure

✅ Migration patterns: Population inflows support pricing while outflows create weakness

✅ Local regulatory environment: Planning restrictions and development policies affect supply responses

✅ Economic base diversity: Regions dependent on struggling industries show weaker sentiment

For surveyors preparing comprehensive reports, these regional factors must inform market value opinions. A property in the Northeast warrants different pricing assumptions than an identical property in the South, even when physical condition and location quality appear comparable.

London's Sharp Cooling: A Case Study

London, traditionally a bellwether for UK property markets, has experienced particularly sharp cooling in early 2026. The capital's market shows:

- Reduced international buyer activity due to global economic uncertainty

- Price sensitivity among domestic buyers facing affordability constraints

- Increased inventory levels as sellers adjust to new market realities

- Growing gap between asking and achieved prices

Surveyors conducting valuations in areas like Fulham, Putney, or Battersea must carefully analyze recent comparable sales, adjusting for the accelerated market softening. Understanding how long house surveys take becomes particularly important when market conditions change rapidly, as delayed surveys may reflect outdated market assumptions.

Building Survey Market Sentiment: Buyer Uncertainty and Its Impact

The third pillar of Building Survey Market Sentiment in Early 2026: Navigating Regional Price Divergence and Buyer Uncertainty centers on unprecedented buyer hesitation. Consumer confidence has been cited as the primary obstacle for buyers for four consecutive months in early 2026 [2].

The Buyer Confidence Crisis

Buyer uncertainty manifests in several measurable ways:

Extended decision timelines: Prospective buyers are taking longer to commit to purchases, conducting more extensive due diligence, and frequently requesting multiple surveys or re-inspections before proceeding.

Increased negotiation leverage: With 37% of builders cutting prices and 64% offering incentives [4], buyers have gained significant negotiating power. This shift means survey findings carry greater weight in price negotiations.

Higher scrutiny of defects: Buyers are using survey findings more aggressively to demand price reductions or repairs. Even minor defects identified in Level 2 surveys become negotiation points in the current environment.

Financing challenges: Despite widespread mortgage rate buydowns—with 80% of builders offering rates in the 4-5% range [2]—buyers remain cautious about long-term affordability and potential rate increases.

Price Reduction Patterns and Surveyor Response

The persistence of price reductions provides crucial context for valuation work:

- 37% of builders reduced prices in March 2026, up slightly from 36% in February [4]

- Average discount remained at 6%, up from 5% in December 2025 [4]

- Sales incentives reached near 12-month highs at 64% of builders [4]

These statistics indicate that builders are maintaining consistent discounting strategies rather than testing higher price points. For surveyors, this suggests:

🏠 Market value opinions should reflect realistic achievable prices, not aspirational asking prices

🏠 Comparable sales analysis must account for incentives that don't appear in headline prices

🏠 Marketing period assumptions should be extended given the challenging demand environment

🏠 Risk factors should be clearly articulated in survey reports to manage client expectations

Demand Expectations: Reality vs. Perception

Interestingly, just over 51% of builders reported in January that demand was on track with their expectations—double the share from December [2]. However, this improvement likely reflects adjusted expectations rather than genuine demand recovery. Builders have recalibrated their forecasts downward, making current activity appear more acceptable by comparison.

For building surveyors, this distinction matters. When assessing market conditions for RICS home surveys, professionals should distinguish between:

- Absolute demand levels (which remain weak)

- Relative performance against lowered expectations (which appears improved)

This nuance prevents overly optimistic market commentary that could mislead clients about genuine market strength.

Practical Implications for Building Surveyors

The combination of weak sentiment, regional divergence, and buyer uncertainty creates specific challenges and opportunities for building surveyors in 2026.

Valuation Methodology Adjustments

Enhanced comparable analysis: With market conditions varying significantly by micro-location, surveyors must expand their comparable search radius while carefully adjusting for regional sentiment differences. A sale in a high-confidence area cannot directly inform valuations in a low-confidence region without substantial adjustment.

Incentive normalization: When builders offer mortgage rate buydowns worth thousands of pounds, headline sale prices don't reflect true market value. Surveyors must calculate the present value of these incentives and adjust comparable sales accordingly.

Time-on-market weighting: Properties that sold quickly in early 2026 likely represent either exceptional value or highly desirable characteristics. Conversely, extended marketing periods signal pricing above market clearing levels. This temporal dimension requires more sophisticated comparable analysis.

Condition premium recalibration: In uncertain markets, buyers place higher premiums on move-in-ready properties and discount those requiring work more severely. The valuation gap between excellent and poor condition widens during periods of buyer uncertainty.

Client Communication Strategies

Effective surveyors in 2026 must master the art of communicating market uncertainty:

Provide context: Explain that current sentiment levels represent historic lows and that market conditions are unusually challenging. This context helps clients understand why valuations may seem conservative.

Quantify regional factors: Use specific regional HMI data to explain why a property in one area commands different pricing assumptions than similar properties elsewhere.

Discuss negotiation leverage: Help buyers understand that current conditions favor purchasers, and survey findings can be powerful negotiation tools. For sellers, explain that addressing defects before marketing may prevent larger price reductions later.

Set realistic timelines: With buyer traffic at historic lows, properties will likely take longer to sell. Incorporate this reality into advice about survey timing and transaction planning.

Risk Management Considerations

The uncertain environment creates potential liability issues for surveyors:

⚠️ Market value disclaimers: Given rapid market changes, include clear statements about valuation date relevance and the potential for market shifts

⚠️ Assumption documentation: Clearly document all market assumptions, regional data sources, and sentiment indicators used in forming opinions

⚠️ Limitation of scope clarity: Ensure clients understand what the survey does and doesn't cover, particularly regarding future market performance

⚠️ Professional indemnity review: Verify that insurance coverage adequately addresses valuation disputes in volatile market conditions

Looking Forward: Short-Term Caution, Medium-Term Stability

While near-term confidence remains weak, with the short-term balance at -18%, the 12-month outlook holds at +33%, suggesting industry professionals expect eventual stabilization. This divergence between immediate pessimism and medium-term optimism creates a complex planning environment.

Factors That Could Improve Sentiment

Several developments could shift market sentiment positively:

📈 Mortgage rate stabilization or decline: If rates settle into a predictable range, buyer confidence may gradually recover

📈 Income growth outpacing home prices: Improved affordability ratios would expand the buyer pool

📈 Regulatory relief: Reduced compliance costs could ease builder cost pressures

📈 Economic confidence improvement: Broader economic stability would support housing demand

Persistent Headwinds

Conversely, several challenges show no signs of abating:

📉 Construction cost pressures: Materials, labor, and land costs remain elevated [4]

📉 Tariff uncertainty: Trade policy unpredictability affects materials pricing

📉 Labor shortages: Skilled trades remain in short supply across regions

📉 Buildable lot scarcity: Limited development-ready land constrains supply responses

Building surveyors must balance these competing forces when advising clients on property decisions and investment timing.

Conclusion

Building Survey Market Sentiment in Early 2026: Navigating Regional Price Divergence and Buyer Uncertainty represents one of the most challenging environments for property professionals in recent memory. With builder confidence persistently below breakeven, a 10-point regional divergence in sentiment, and buyer traffic at historic lows, surveyors must adapt their methodologies and client communication approaches to reflect these realities.

The key to successful surveying practice in this environment lies in granular regional analysis, transparent communication of market uncertainties, and conservative valuation approaches that protect clients from overpaying in a softening market. Surveyors who master these skills will not only navigate current challenges but position themselves as trusted advisors when market conditions eventually stabilize.

Actionable Next Steps

For building surveyors and property professionals:

- Update regional market data monthly: Track HMI scores, local sales velocity, and price reduction patterns in your operating areas

- Enhance comparable analysis protocols: Implement systematic adjustments for incentives, regional sentiment, and time-on-market factors

- Strengthen client communication: Develop clear explanations of market conditions that help clients make informed decisions

- Review professional practices: Ensure valuation methodologies, report templates, and disclaimers adequately address current market volatility

- Invest in continuing education: Stay current on RICS guidance regarding valuations in uncertain markets and regional analysis techniques

The surveyors who thrive in 2026 will be those who acknowledge market challenges honestly, provide data-driven analysis that accounts for regional variation, and help clients navigate uncertainty with confidence. By understanding the nuanced interplay between sentiment, regional divergence, and buyer behavior, building surveyors can deliver exceptional value even in the most challenging market conditions.

For property buyers and sellers seeking professional guidance, engaging experienced chartered surveyors who understand these market dynamics has never been more important. The right survey, conducted by professionals who grasp current sentiment realities, can save thousands of pounds and prevent costly purchasing mistakes in this uncertain environment.

References

[1] Builder Sentiment Loses Ground At Start Of 2026 – https://www.nahb.org/news-and-economics/press-releases/2026/01/builder-sentiment-loses-ground-at-start-of-2026

[2] Early 2026 Housing Trends Rates Improve Incentives Expand Confidence Lags,59489 – https://riograndeguardian.com/premium/stacker/stories/early-2026-housing-trends-rates-improve-incentives-expand-confidence-lags,59489

[3] Builders Kick Off 2026 In A Downbeat Mood – https://www.realestatenews.com/2026/01/16/builders-kick-off-2026-in-a-downbeat-mood

[4] Builder Sentiment Inches Higher But Affordability Concerns Persist – https://www.nahb.org/news-and-economics/press-releases/2026/03/builder-sentiment-inches-higher-but-affordability-concerns-persist