By 2026, over 70% of UK mortgage lenders use some form of automated valuation model (AVM) to screen residential properties before instructing a physical inspection — yet RICS still mandates a qualified professional for the vast majority of regulated valuation purposes. That gap between algorithmic speed and professional judgement is precisely where the most important conversations in UK property are happening right now.

This article examines the landscape of PropTech and Valuation in the UK: Where AVMs, Big Data and Digital Platforms Help – and Where a Chartered Valuer Still Has to Step In — comparing what technology genuinely delivers against what it cannot yet replace, and why understanding that boundary matters for buyers, lenders, investors, and legal professionals alike.

Key Takeaways 📌

- AVMs and digital platforms have transformed speed and data access in UK property valuation, but they carry significant accuracy limitations on atypical or complex assets.

- RICS Red Book standards require human professional judgement for regulated purposes — no algorithm currently satisfies that requirement.

- Big data tools (Land Registry feeds, EPC data, digital twins) genuinely improve a chartered valuer's analysis when used correctly.

- Legal, tax, and dispute contexts — including probate, matrimonial, and ATED valuations — almost always require a RICS-registered professional.

- The smartest approach in 2026 is human-plus-machine: technology handles data aggregation; the chartered valuer applies context, liability, and professional accountability.

What PropTech Has Actually Changed in UK Property Valuation

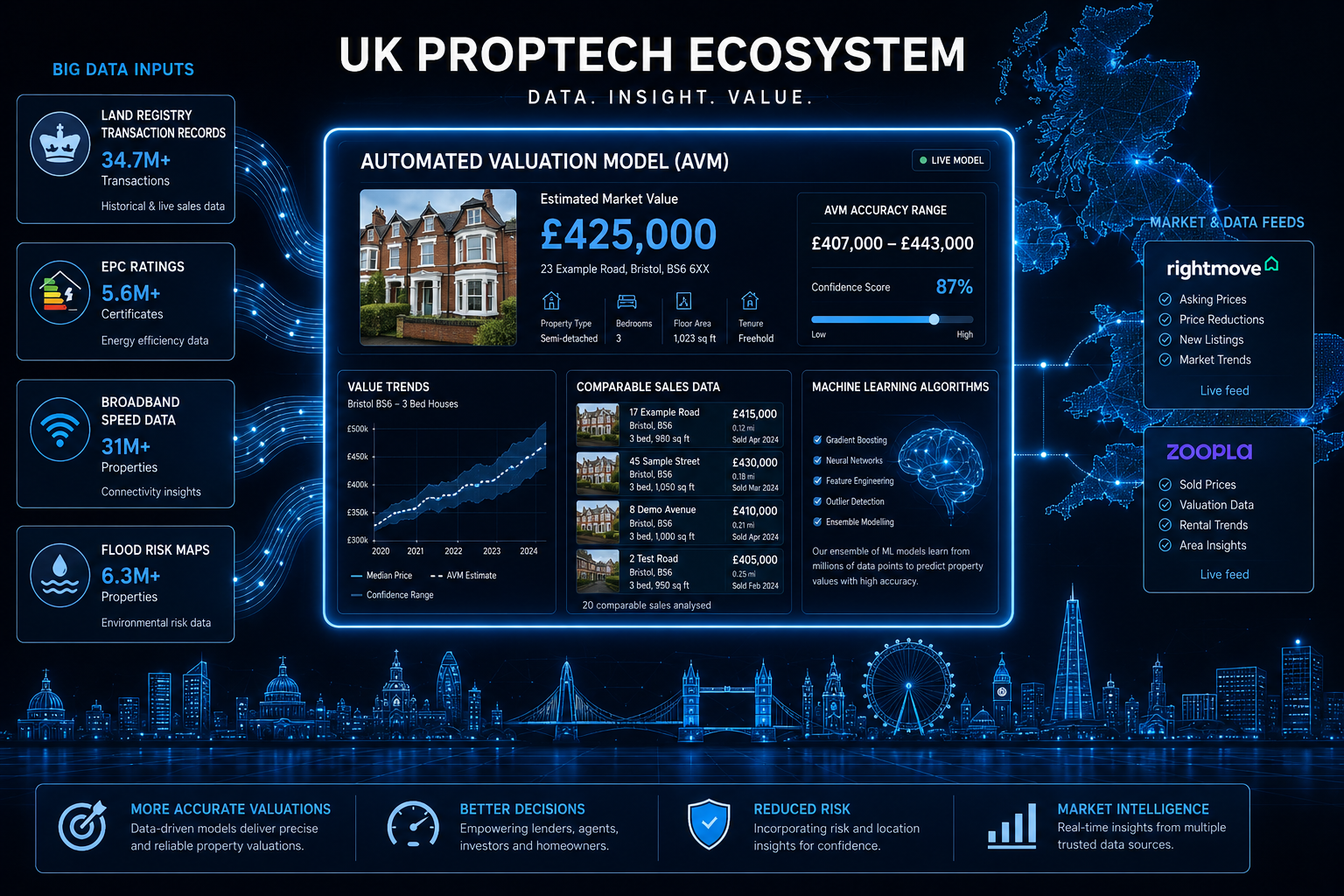

The UK PropTech sector has matured rapidly. Platforms like Rightmove Data Services, Hometrack, and Zoopla's AVM engine now process millions of data points — Land Registry transactions, EPC ratings, council tax bands, flood risk classifications, broadband speeds, and planning history — to generate near-instant property estimates.

How AVMs Work in the UK Context

An Automated Valuation Model (AVM) applies statistical regression and, increasingly, machine learning to comparable sales data. The output is typically a point estimate plus a confidence interval — for example, "£485,000 ± 8%."

Key data inputs include:

| Data Source | What It Contributes |

|---|---|

| HM Land Registry | Verified sale prices and transaction history |

| Ordnance Survey | Location, plot size, proximity metrics |

| EPC Register | Energy efficiency ratings, construction age indicators |

| Environment Agency | Flood risk and contamination flags |

| Planning Portal | Permitted development, extensions, change of use |

| ONS House Price Index | Macro-level trend adjustment |

For standard residential properties in well-transacted markets — think a two-bedroom flat in Clapham or a semi-detached in Harrow — AVMs can perform remarkably well. Confidence intervals narrow when comparable sales are plentiful and recent.

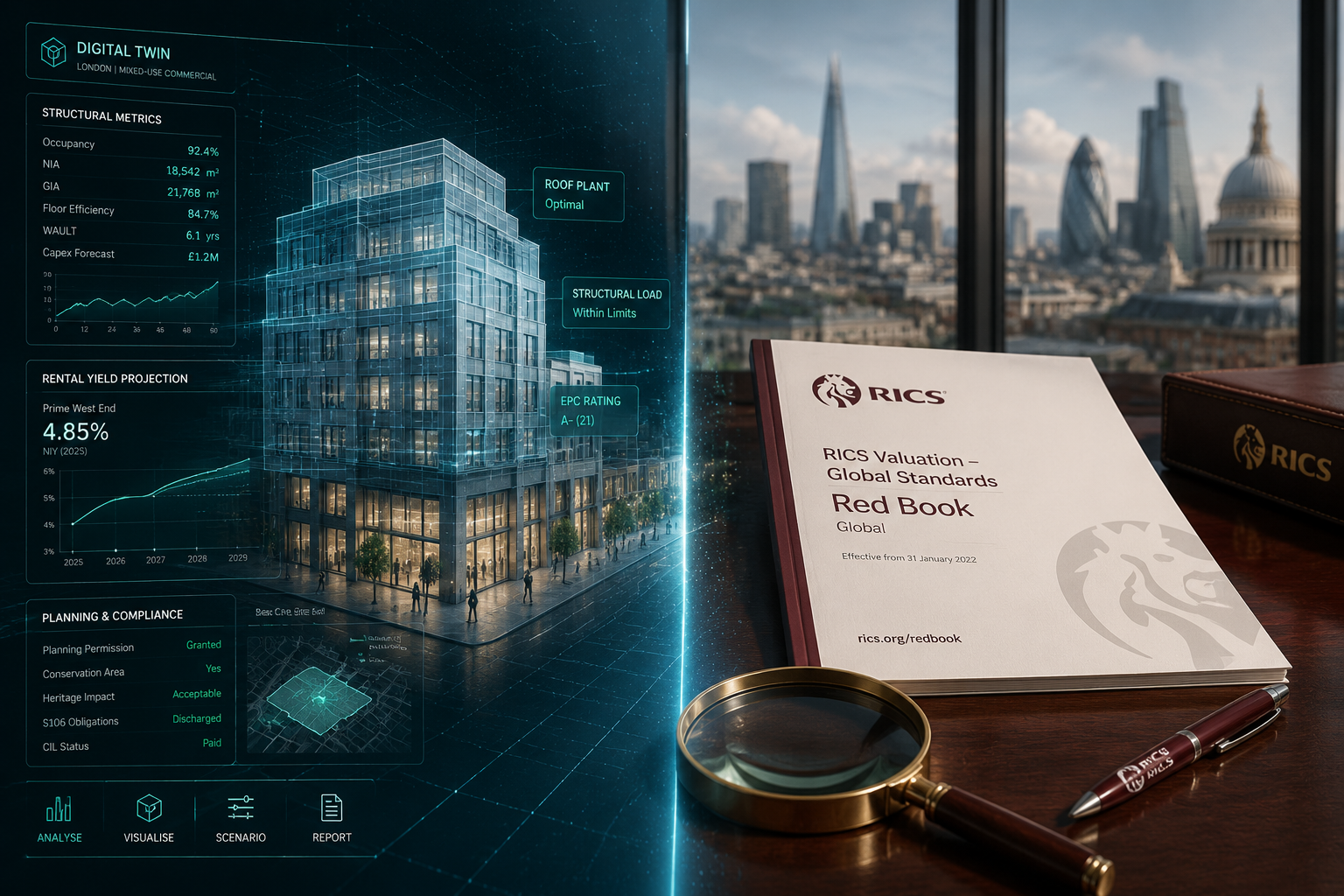

Digital Platforms Beyond AVMs

Beyond pure valuation models, PropTech now offers:

- 🏗️ Digital twins: 3D building models with embedded structural, energy, and planning data, increasingly used in commercial property analysis.

- 📊 Transaction data platforms: Tools like MSCI Real Estate and CoStar give commercial investors granular yield, void rate, and covenant strength data.

- 🔍 Lender decisioning tools: Many high-street lenders now use AVM outputs to triage loan-to-value risk before deciding whether a physical inspection is warranted.

- 🛰️ Geospatial analytics: Satellite and drone data informing site assessments, particularly for development land.

These tools have genuinely improved the speed, consistency, and data richness available to valuers. A chartered surveyor using a good transaction data platform in 2026 has access to market intelligence that would have taken weeks to compile manually a decade ago.

💬 "Technology has made the data side of valuation dramatically faster. What it hasn't done is replicate the professional judgement that turns data into a defensible opinion of value."

Where the Technology Genuinely Helps — and Its Real Limitations

Understanding PropTech and Valuation in the UK: Where AVMs, Big Data and Digital Platforms Help – and Where a Chartered Valuer Still Has to Step In requires an honest assessment of both sides.

Where PropTech Adds Real Value ✅

1. Portfolio screening and triage

Lenders and investors managing large residential portfolios use AVMs to flag properties that fall outside acceptable LTV thresholds. This is a legitimate and efficient use — the AVM isn't making a final lending decision; it's directing human attention where it's most needed.

2. Desktop valuations for low-risk remortgages

RICS guidance permits desktop and automated approaches for certain low-risk remortgage scenarios where the lender accepts the risk profile. When a property last sold two years ago in a liquid market, an AVM-assisted desktop review can be proportionate.

3. Market trend analysis

Big data platforms excel at identifying micro-market trends — price movements by postcode, yield compression in specific commercial submarkets, or the impact of a new transport link on residential values. This macro intelligence genuinely sharpens a valuer's market commentary.

4. Pre-instruction due diligence

Before commissioning a full RICS Red Book valuation, clients and advisers can use digital platforms to sense-check whether an asking price is in the right territory. This saves time and manages expectations.

5. Supporting comparable selection

Modern valuation software helps chartered surveyors identify and filter comparable transactions more efficiently, reducing the risk of cherry-picking and improving consistency.

Where AVMs Fall Short ❌

The limitations are significant and well-documented:

Atypical properties: A converted Victorian school, a listed farmhouse with agricultural restrictions, or a property with a complex leasehold structure will confuse any AVM. The model has no comparables that meaningfully match, and the confidence interval balloons to the point of uselessness.

Condition and defects: AVMs are blind to physical condition. A house with significant structural movement, Japanese knotweed in the garden, or a roof requiring immediate replacement will receive the same AVM output as an identical, pristine property next door. For anyone considering a purchase, understanding what surveyors look for in a house survey makes clear just how much condition affects value.

Leasehold complexity: Short leases, onerous ground rents, and service charge disputes all affect value in ways no algorithm currently captures reliably.

New-build premium decay: AVMs struggle to model the initial premium paid for new-build properties and how it erodes once the property is resold as second-hand.

Rapidly changing markets: In a fast-moving market — upward or downward — AVM training data lags behind reality. The model is always looking in the rear-view mirror.

When a Chartered Valuer Must Step In: Legal, Regulatory, and High-Stakes Contexts

This is the heart of the matter. PropTech and Valuation in the UK: Where AVMs, Big Data and Digital Platforms Help – and Where a Chartered Valuer Still Has to Step In is not merely an academic question — it has direct legal and financial consequences.

RICS Red Book: The Gold Standard

The RICS Valuation – Global Standards (the "Red Book") sets out the framework within which regulated valuations must be conducted. It requires:

- A qualified RICS Registered Valuer to sign off the report

- An inspection appropriate to the purpose and risk

- Independence and objectivity — the valuer must not have a conflict of interest

- A written report with reasoned methodology

No AVM output satisfies these requirements. A RICS-registered valuer brings not just data analysis but professional accountability — they carry personal liability for their opinion of value.

Situations That Always Require a Chartered Valuer

🏛️ Probate Valuations

When a property forms part of a deceased estate, HMRC requires a professional valuation for Inheritance Tax purposes. An AVM printout will not be accepted. A formal probate valuation must be prepared by a qualified professional who can defend the figure if HMRC challenges it.

⚖️ Matrimonial and Divorce Proceedings

Family courts require valuations that can withstand cross-examination. A matrimonial valuation must be prepared by an independent RICS valuer — and in contested cases, the valuer may be called as an expert witness. No algorithm provides that accountability.

🏢 Annual Tax on Enveloped Dwellings (ATED)

Companies owning UK residential property above certain thresholds must submit periodic valuations to HMRC. An ATED valuation requires a professional opinion that can be defended under scrutiny — the stakes include significant tax liability.

🏠 Help to Buy and Right to Buy Schemes

Government schemes have specific valuation requirements. RICS Help to Buy valuations and Right to Buy valuations must follow prescribed methodologies that AVMs are not designed to replicate.

🏗️ Commercial Property

Commercial valuations — for loan security, accounts purposes, or lease renewals — involve income capitalisation, yield analysis, and covenant assessment that go far beyond residential AVM methodology. A commercial property valuation requires specialist expertise and professional sign-off.

📋 Expert Witness and Dispute Resolution

When property value is contested in court or arbitration, only a qualified professional can provide admissible expert evidence. The expert witness role carries strict duties to the court that no automated system can fulfil.

The Liability Question

This is perhaps the most important practical point. When a valuation is wrong — and occasionally they are — someone must be accountable. A chartered valuer carries professional indemnity insurance and is regulated by RICS. An AVM output carries no such accountability. For any transaction where the financial or legal consequences of an error are significant, professional accountability is not optional.

The Human-Plus-Machine Model: Best Practice in 2026

The most effective approach to UK property valuation in 2026 is not a choice between technology and professional expertise — it is a deliberate combination of both.

A Practical Framework

| Scenario | Appropriate Approach |

|---|---|

| Lender triage on standard residential remortgage | AVM-led, with human review of outliers |

| Purchase of standard residential property | Physical survey + professional valuation |

| Probate, divorce, or tax purposes | RICS Red Book valuation, mandatory |

| Commercial investment acquisition | Full professional valuation + data platform analysis |

| Portfolio monitoring (institutional) | AVM for trend data; professional valuation for key assets |

| Atypical, listed, or complex property | Physical inspection essential; AVM data supplementary only |

Chartered valuers who embrace PropTech tools — using transaction data platforms, digital mapping, and AVM outputs as a starting point rather than a conclusion — deliver faster, better-evidenced reports. The technology handles data aggregation; the professional applies market knowledge, physical inspection findings, and reasoned judgement.

Understanding what a chartered surveyor does makes clear why that combination matters: the role encompasses not just data analysis but professional responsibility, legal compliance, and client duty of care.

Questions to Ask Before Relying on an AVM

Before accepting an automated valuation at face value, consider:

- Is the property typical? Standard properties in liquid markets suit AVMs better than unusual ones.

- How recent are the comparables? In a fast-moving market, six-month-old data may be materially misleading.

- What is the confidence interval? A wide interval signals low reliability.

- What is the purpose? Legal, tax, and lending purposes generally require professional sign-off.

- Has anyone inspected the property? Condition issues invisible to algorithms can materially affect value.

Conclusion: Technology Sharpens the Tool — It Doesn't Replace the Professional

PropTech has genuinely transformed what is possible in UK property valuation. AVMs, big data platforms, digital twins, and lender decisioning tools have made the industry faster, more data-rich, and more consistent across standard cases. That is a real and lasting improvement.

But the boundary is equally real. The moment a valuation carries legal weight — for probate, divorce, tax, lending security, or dispute resolution — a chartered valuer is not just preferable but necessary. RICS standards exist precisely because property decisions involve large sums of money, complex legal rights, and consequences that can last decades. Professional judgement, physical inspection, and personal accountability cannot be automated away.

Actionable Next Steps

- ✅ Use PropTech tools for market research, portfolio screening, and pre-instruction sense-checking.

- ✅ Commission a RICS Red Book valuation for any legal, tax, or regulated lending purpose — no exceptions.

- ✅ Instruct a physical survey when buying any property, regardless of what an AVM suggests.

- ✅ Check your valuer's credentials — confirm they are a RICS Registered Valuer before relying on their report.

- ✅ Seek specialist advice for atypical properties, commercial assets, or high-value transactions where the cost of a valuation error is significant.

The future of UK property valuation is human-plus-machine — and knowing which situations demand which is the most valuable knowledge of all.