UK house prices rose for the eighth consecutive month in early 2026, yet transaction volumes remain roughly 12% below the five-year pre-pandemic average — a gap that tells a far more nuanced story than any single headline figure. For residential valuers, that tension between price momentum and subdued activity is precisely where professional judgement becomes most critical. Understanding how UK surveyors should adapt residential valuations to early 2026 market recovery signals is not just a technical exercise; it is a matter of professional duty, lender confidence, and client protection.

Key Takeaways 📋

- Early 2026 recovery signals are cautious and uneven — valuers must resist extrapolating short-term price momentum into forward assumptions.

- RICS UK Residential Market Survey data points to improving buyer enquiries but persistently low stock levels, distorting comparable evidence.

- Risk premiums should be recalibrated region by region, not applied as a blanket national adjustment.

- Comparable selection, demand weighting, and special assumptions all require explicit documentation under RICS Red Book Global Standards.

- Surveyors operating in recovering micro-markets — from Central London to commuter belts — face different adjustment challenges and must apply local intelligence rigorously.

Reading the 2026 Recovery Signals Correctly

The RICS UK Residential Market Survey for Q1 2026 paints a picture of cautious optimism. New buyer enquiries are net positive for the third consecutive quarter. Agreed sales are edging upward. Yet the same survey flags that new instructions from vendors remain suppressed, creating an artificial tightening of supply that is flattering asking prices without necessarily reflecting genuine market depth.

💬 "A recovering market is not the same as a recovered market. Valuers who conflate the two expose lenders and buyers to significant risk."

This distinction matters enormously when selecting and weighting comparable evidence. In a clear upswing, recent transactions carry strong evidential weight. In an early recovery phase, those same transactions may reflect a supply-constrained spike rather than a durable shift in market value. UK surveyors should therefore:

- Date-weight comparables carefully — transactions from Q4 2025 may reflect a different market sentiment than Q1 2026 sales.

- Scrutinise days-on-market data — rapidly falling days-on-market in low-stock environments can signal demand without confirming sustainable value.

- Cross-reference listing price trajectories — are vendors achieving asking price, above, or below? The spread reveals true market confidence.

Understanding the full range of factors that influence residential valuations is essential before applying any market-level adjustment.

How UK Surveyors Should Adapt Residential Valuations to Early 2026 Market Recovery Signals: Methodology Adjustments

Recalibrating Demand Assumptions

One of the most common errors in a recovering market is treating improved buyer sentiment as confirmed demand. The RICS survey measures net balance of surveyor opinion — it tells us direction, not magnitude. Valuers should treat positive net balances as a prompt to investigate, not to automatically adjust values upward.

Practical steps for demand recalibration:

| Signal | What It Suggests | Valuation Response |

|---|---|---|

| Rising buyer enquiries | Latent demand returning | Monitor, do not auto-adjust upward |

| Low vendor instructions | Supply constraint flattering prices | Apply caution to recent sale comparables |

| Mortgage approvals rising | Finance availability improving | Positive signal — note in report |

| Transaction volumes below average | Market not yet normalised | Weight older comparables less aggressively |

| Price-to-income ratios stabilising | Affordability floor forming | Supports base value assumptions |

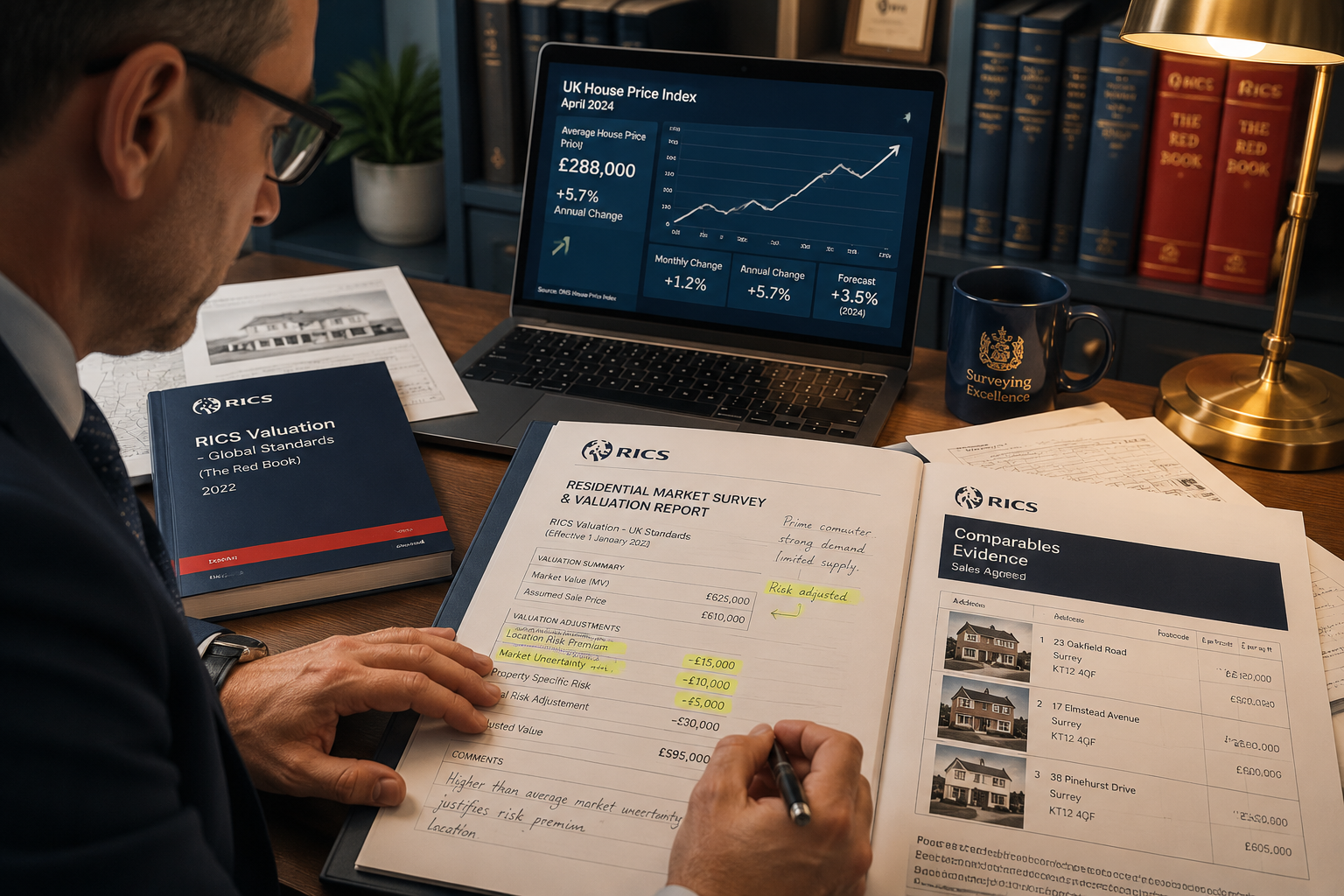

For RICS Red Book valuations, all material assumptions about market conditions must be explicitly stated. In early 2026, that means documenting the recovery phase context — not just the comparable evidence — within the valuation report.

Adjusting Risk Premiums in a Transitional Market

Risk premiums embedded in residential valuations typically reflect uncertainty about future marketability. In a clear downturn, premiums widen. In a clear upswing, they compress. In an early recovery, the appropriate position sits somewhere between — and that position varies significantly by:

- Geography 🗺️ — Prime Central London is recovering faster than some northern commuter markets.

- Property type 🏠 — Detached family homes with gardens are outperforming flats in many areas.

- Price band 💷 — Sub-£500,000 properties are seeing stronger demand than upper-prime stock.

- Energy efficiency ⚡ — EPC-rated properties are attracting measurable premiums as buyer awareness grows.

Surveyors working across Central London will encounter different risk dynamics than colleagues operating in South West London or outer commuter zones. A blanket national risk premium adjustment is not defensible under RICS standards.

Transaction Volume Adjustments: Why Thin Markets Require Greater Care

When transaction volumes are depressed — as they remain in early 2026 relative to historical norms — the evidential base for comparable analysis narrows. This creates several practical challenges:

- Temporal gaps between comparable transactions increase, reducing their reliability.

- Atypical sales (distressed disposals, probate sales, developer incentive purchases) carry disproportionate weight in thin datasets.

- Off-market transactions become more common, reducing transparency.

The professional response is not to avoid valuation — it is to expand the comparable search radius thoughtfully, apply explicit adjustments for differences in location and condition, and increase the prominence of the market commentary section within the report.

For properties where condition significantly affects value, a RICS-specific defect survey can provide the structural evidence needed to justify condition-based adjustments in thin comparable environments.

Regional Nuances: Applying Local Intelligence to National Recovery Data

National recovery signals are useful as a directional indicator. They are not a substitute for local market intelligence. The RICS survey data aggregates surveyor opinion across England, Scotland, Wales, and Northern Ireland — markets that are recovering at meaningfully different speeds in 2026.

London and South East

The London market is showing the clearest early recovery signals, driven by:

- Returning international buyer activity in prime zones

- Improved mortgage product availability for high-value purchases

- Rental market pressure pushing tenants toward ownership

Surveyors operating in areas like North London or South East London should note that recovery is not uniform even within boroughs. Transport links, school catchments, and regeneration proximity create micro-market variations that national data simply cannot capture.

Commuter Belt and Home Counties

Markets in areas such as Guildford, Leatherhead, and St Albans are benefiting from a partial reversal of the post-pandemic dispersal trend, with some buyers returning to commuter zones as hybrid working patterns stabilise. However, affordability constraints remain acute in these markets, and price growth is more modest than inner-London comparables suggest.

Surveyors covering Guildford and Leatherhead should apply particular scrutiny to the relationship between local wage growth and achievable sale prices before accepting recent comparables at face value.

How UK Surveyors Should Adapt Residential Valuations to Early 2026 Market Recovery Signals: Documentation and Compliance

RICS Red Book Compliance in a Volatile Base Period

The RICS Red Book Global Standards (as updated) require valuers to clearly state the market conditions prevailing at the date of valuation. In early 2026, this means:

- Identifying the recovery phase explicitly in the market commentary section.

- Noting the limitations of comparable evidence where transaction volumes are below historical norms.

- Stating any special assumptions applied — for example, if a valuation assumes market conditions normalise within a defined period.

- Documenting the basis of value used (Market Value, Market Rent, etc.) and confirming it remains appropriate given current conditions.

💬 "Transparency in methodology is the valuer's primary defence — both professionally and legally — when market conditions are in transition."

Avoiding the 'Anchoring' Trap

Behavioural research consistently shows that valuers — like all professionals — are susceptible to anchoring bias, where an initial data point (such as a vendor's asking price or a lender's loan amount) disproportionately influences the final valuation figure. In an early recovery market, anchoring to recent high comparables is a particular risk.

Mitigation strategies include:

- Completing the comparable analysis before reviewing the instruction price where possible.

- Peer review of valuations in locations where recovery signals are strongest.

- Using RICS valuation services that incorporate structured review processes.

- Maintaining a written audit trail of how each comparable was weighted and why.

Special Valuation Scenarios in a Recovery Market

Several valuation types carry heightened complexity during market transitions:

🏠 Right to Buy Valuations

Under Right to Buy schemes, the valuation date is fixed and the market must be assessed as it stands. In early 2026, this means surveyors cannot assume further recovery — the valuation must reflect current market conditions, not anticipated ones.

🤝 Shared Ownership Valuations

Shared ownership valuations are particularly sensitive to market phase. The staircasing price must reflect genuine market value at the date of valuation. In a recovering market with thin comparables, this requires especially careful comparable selection and explicit market commentary.

💰 Capital Gains Tax Valuations

For CGT valuations, the retrospective or current date of valuation must be clearly established. Where the valuation date falls within the recovery period, the surveyor must document the specific market conditions prevailing at that date — not conditions as they may have evolved since.

Practical Checklist: Adapting Valuations to 2026 Recovery Conditions ✅

Use this checklist to ensure valuations reflect current market nuance:

- Review latest RICS UK Residential Market Survey before each valuation instruction

- Select comparables from within the past 3 months where possible; extend cautiously with explicit adjustments

- Document transaction volume context — note if local market is thin

- Apply geography-specific risk assessment — do not use national averages as local proxies

- Check EPC ratings of comparables and subject property — energy efficiency premiums are measurable in 2026

- State market conditions explicitly in the report narrative

- Avoid anchoring — complete comparable analysis independently of instruction price

- Peer review valuations in high-recovery-signal locations

- Confirm basis of value is appropriate for the instruction type

- Flag any special assumptions clearly and obtain client acknowledgement

The Surveyor's Role in Protecting Market Integrity

Understanding what a chartered surveyor does extends well beyond measuring rooms and checking roof tiles. In a transitional market, the residential valuer acts as a critical check on market exuberance — protecting buyers from overpaying, lenders from over-exposure, and the broader market from the kind of speculative inflation that preceded previous corrections.

The early 2026 recovery signals are genuinely encouraging. Mortgage approvals are rising. Buyer sentiment is improving. The RICS survey net balance is positive. But cautious optimism is not the same as certainty, and professional valuations must reflect that distinction with precision and transparency.

Surveyors who adapt their methodology thoughtfully — calibrating demand assumptions, adjusting risk premiums regionally, and documenting their reasoning rigorously — will not only produce more defensible valuations. They will also build the kind of professional reputation that sustains a practice through whatever market phase comes next.

Conclusion: Actionable Next Steps for UK Residential Valuers in 2026

The question of how UK surveyors should adapt residential valuations to early 2026 market recovery signals does not have a single answer — it has a structured process. Here are the concrete next steps every residential valuer should take now:

- Subscribe to and regularly review the RICS UK Residential Market Survey — treat it as a live market intelligence tool, not a quarterly formality.

- Build a regional comparable database that distinguishes between thin-market and active-market evidence, with explicit weighting notes.

- Update your report templates to include a dedicated market conditions narrative section that addresses the current recovery phase.

- Engage in CPD focused on behavioural biases in valuation — anchoring and availability bias are heightened risks in transitional markets.

- Collaborate with colleagues in your area to cross-check local market intelligence, particularly in micro-markets where transaction volumes remain low.

- Review your PI insurance position — in a transitional market, the risk of challenge to valuations increases, and adequate cover is non-negotiable.

The 2026 recovery is real — but it is early, uneven, and fragile. The surveyors who serve their clients best will be those who resist the temptation to follow the headline and instead apply the rigorous, evidence-based methodology that defines the profession at its best.