A flat property market is not a neutral market. When transaction volumes fall and buyers become choosier, the gap between a well-presented, well-documented property and a problematic one widens dramatically — even when headline prices appear unchanged. This is precisely the challenge at the heart of Flat Market Valuations in 2026: How Surveyors Should Assess Risk When Prices Are Stagnant but Buyers Are More Selective.

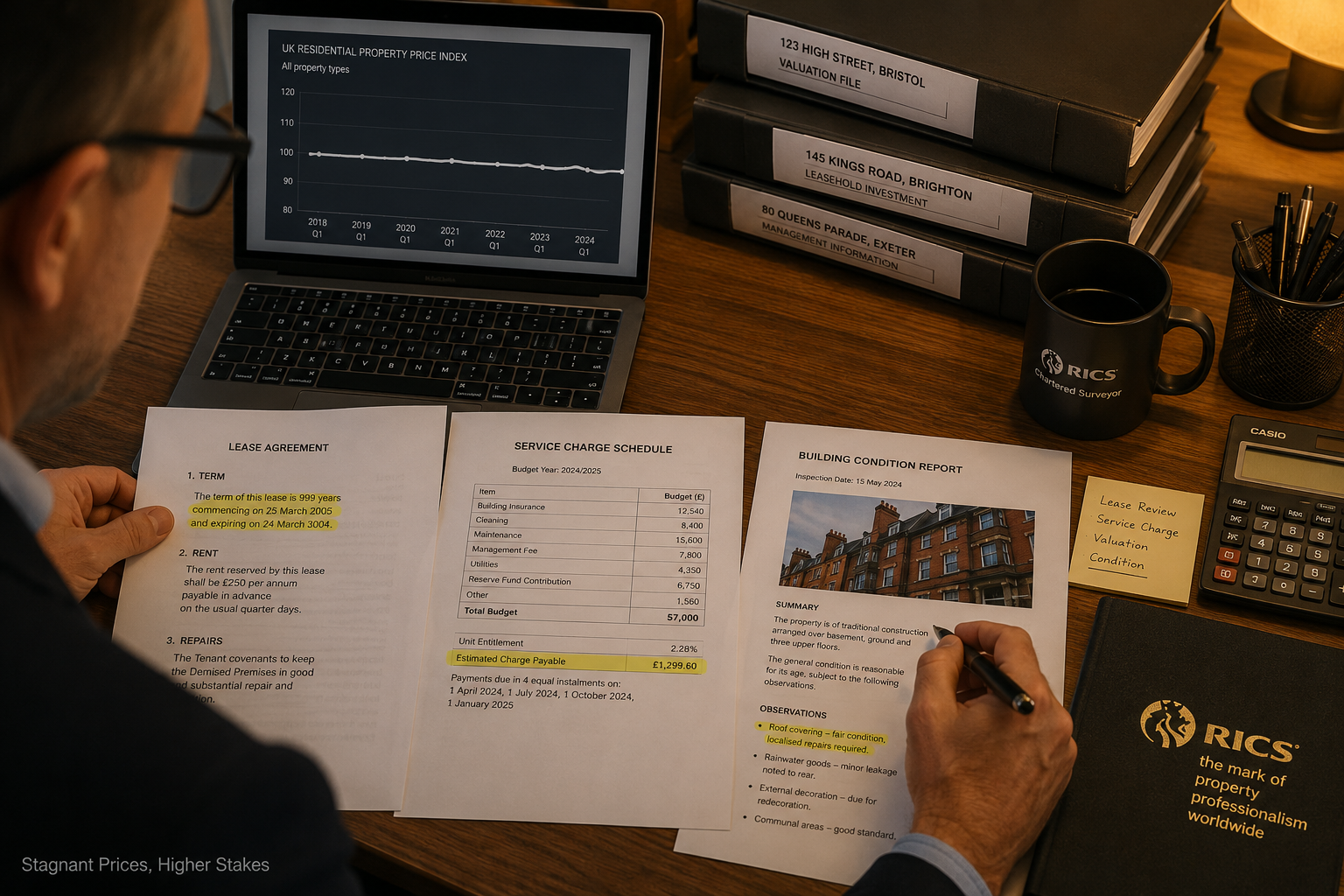

In 2026, UK residential property prices have broadly plateaued across many regions. Yet within that stillness, enormous variation exists. Buyers are spending longer on due diligence, walking away from properties with structural concerns, onerous lease terms, or high service charge exposure. Lenders are scrutinising valuations more carefully. For surveyors, this environment demands sharper risk assessment, clearer client communication, and a more granular approach to comparable evidence.

Key Takeaways 📌

- Flat markets amplify property-specific risk — condition, tenure, and local demand matter far more than in rising markets.

- Comparable evidence must be treated critically — stale or thin comparables can produce misleading valuations.

- Lease terms, service charges, and cladding issues are now primary valuation drivers in many segments.

- Surveyors must communicate value adjustments clearly to both buyers and lenders to avoid disputes and negligence claims.

- A thorough survey is more important than ever in a slow-moving market where buyers have less margin for error.

Why Flat Markets Are Deceptively Risky for Valuers

The instinct in a stable market is to assume stability. Prices haven't fallen, so the risk must be contained — right? Not quite. Flat markets create their own category of valuation risk, and it is one that is easy to underestimate.

When prices are rising, a minor defect or an awkward lease clause is often absorbed by general market momentum. Buyers accept imperfections because they fear missing out. In 2026, that dynamic has reversed. Buyers are patient, well-informed, and increasingly unwilling to absorb risk they cannot quantify.

💬 "A flat market doesn't mean all properties are equally flat. It means the market has stopped hiding problems."

For surveyors, this creates a clear professional obligation: every valuation must stand on its own merits, not on the assumption that rising sentiment will paper over the cracks. The following factors are now carrying disproportionate weight in flat market valuations.

Condition and Defect Exposure

In a rising market, a buyer might accept a property needing £30,000 of roof repairs because they expect to recoup it in capital growth within two years. In a flat market, that same buyer either renegotiates aggressively or walks away entirely.

Surveyors must therefore be more precise about quantifying defect costs and flagging them explicitly in reports. A vague reference to "some roof coverings showing signs of wear" is no longer adequate. Clients and lenders need to understand the likely cost range and the urgency of the work.

A Level 3 Building Survey is particularly valuable in this environment, as it provides the depth of investigation needed to uncover hidden defects that a more selective buyer pool will inevitably discover during their own due diligence.

Local Demand Divergence

National price indices mask enormous local variation. In 2026, some micro-markets — particularly commuter towns with good transport links and strong schools — remain competitive. Others, especially areas with high concentrations of leasehold flats or properties affected by fire safety remediation requirements, are seeing very slow transaction volumes.

Surveyors must resist the temptation to apply regional averages. Hyper-local comparable evidence, ideally from the same street or development, is essential. Where comparable evidence is thin, that thinness itself is a risk factor that should be noted in the valuation report.

Assessing Lease Terms, Service Charges, and Tenure Risk

For leasehold properties — which make up a significant proportion of the UK's urban housing stock — the flat market has exposed tenure-related risks that were previously masked by buyer competition.

Lease Length and Ground Rent

A lease with fewer than 80 years remaining triggers the marriage value calculation under current legislation, making lease extensions more expensive. In a flat market, buyers are far less willing to absorb this cost speculatively. Surveyors must:

- Calculate the unexpired lease term precisely and flag its impact on mortgageability.

- Assess ground rent clauses — particularly doubling ground rents or those linked to RPI, which can render a property unmortgageable.

- Note any pending lease extension negotiations and their potential effect on value.

Understanding valuation factors specific to leasehold properties is critical here, as these elements can reduce an otherwise comparable property's value by tens of thousands of pounds.

Service Charge Exposure

High or unpredictable service charges are a growing concern for flat buyers in 2026. Where a development has deferred major works — lift replacements, external decoration, roof repairs — the risk of a large special levy falls on the current owner or buyer.

| Risk Factor | Low Risk | Medium Risk | High Risk |

|---|---|---|---|

| Annual service charge | Under £2,500 | £2,500–£5,000 | Over £5,000 |

| Reserve fund adequacy | Well-funded | Partially funded | Minimal/none |

| Pending major works | None identified | Minor works | Structural/cladding |

| Lease remaining | 90+ years | 80–90 years | Under 80 years |

Surveyors should request three years of service charge accounts and the most recent Section 20 consultation notices before forming a view on value. Where accounts are unavailable or incomplete, this should be flagged as a material uncertainty.

Cladding and Fire Safety

The legacy of fire safety remediation continues to affect valuations in 2026, particularly for flats in buildings over 11 metres. Properties without an EWS1 form — or with a B2 or C2 rating — remain difficult or impossible to mortgage through mainstream lenders.

Surveyors must be explicit about:

- Whether an EWS1 form exists and its rating.

- Whether remediation works are planned, in progress, or completed.

- The likely impact on value and marketability if remediation is outstanding.

This is not a peripheral concern — it is often the single largest value driver for affected properties.

How Flat Market Valuations in 2026 Require a New Approach to Comparable Evidence

The mechanics of valuation — finding comparable sales and adjusting for differences — remain the same. But the quality and interpretation of comparable evidence must be held to a higher standard in a flat, selective market.

The Problem with Stale Comparables

In a rising market, a comparable from 12 months ago can be used with a modest upward adjustment. In a flat or uneven market, a 12-month-old comparable may reflect a different buyer sentiment entirely. Properties that sold quickly in late 2024 may have benefited from a brief window of activity that no longer exists.

Surveyors should:

- Prioritise comparables from the last three to six months wherever possible.

- Discount comparables from periods of unusual activity — post-stamp-duty-holiday surges, for example.

- Note the time on market for comparable properties, as extended marketing periods signal weaker demand.

Adjusting for Condition Differences

In a selective market, condition adjustments carry more weight. A comparable property that sold in excellent decorative order is not directly comparable to a property requiring significant updating — even if they are on the same street.

Surveyors should document their condition adjustments clearly and be prepared to justify them to lenders. A comprehensive condition survey report provides the evidence base needed to support these adjustments robustly.

Thin Markets and Material Uncertainty

Where fewer than three or four comparable transactions exist within a reasonable search radius and time period, the valuation is operating in a thin market. RICS guidance permits the use of a "material uncertainty" caveat in such circumstances, and surveyors should not hesitate to use it where appropriate.

A material uncertainty declaration does not mean the valuation is wrong — it means the evidence base is limited and the valuer has been transparent about that limitation. In a flat market, this transparency protects both the surveyor and the client.

Communicating Value Adjustments to Clients and Lenders

One of the most underappreciated skills in flat market conditions is explaining value adjustments in plain language. Clients who expected a valuation to match the asking price — and lenders who need to justify their lending decision — both need clear, logical explanations.

What Clients Need to Understand

Buyers often conflate the asking price with market value. In a flat market, these can diverge significantly, especially where:

- The seller's price is based on an outdated peak valuation.

- The property has defects that the seller has not disclosed or priced in.

- The local market has softened relative to the broader regional trend.

Surveyors should explain value adjustments in terms of specific, quantifiable factors rather than vague market references. For example:

"The valuation reflects a downward adjustment of approximately £18,000 from the agreed price. This accounts for the estimated cost of replacing the flat roof over the rear extension (£8,000–£12,000), the below-average lease length of 74 years, and the absence of an EWS1 form for the building's external wall system."

This level of specificity helps clients make informed decisions and reduces the risk of post-transaction disputes. Understanding why hiring a residential surveyor could save you thousands becomes especially clear when a valuation uncovers issues like these.

What Lenders Need to See

Mortgage lenders in 2026 are applying greater scrutiny to valuations, particularly for properties with:

- Fire safety concerns.

- Short leases or problematic ground rent clauses.

- High service charge exposure.

- Evidence of structural movement or significant defect.

Lenders need the valuation report to clearly separate the gross value from the adjusted value, with each deduction explained and evidenced. Where a surveyor recommends a retention — withholding part of the mortgage advance until specific works are completed — the rationale should be documented in detail.

For surveyors working across the South East and London, understanding local market conditions in areas like Surrey and Sussex is essential to providing lenders with credible, locally-grounded evidence.

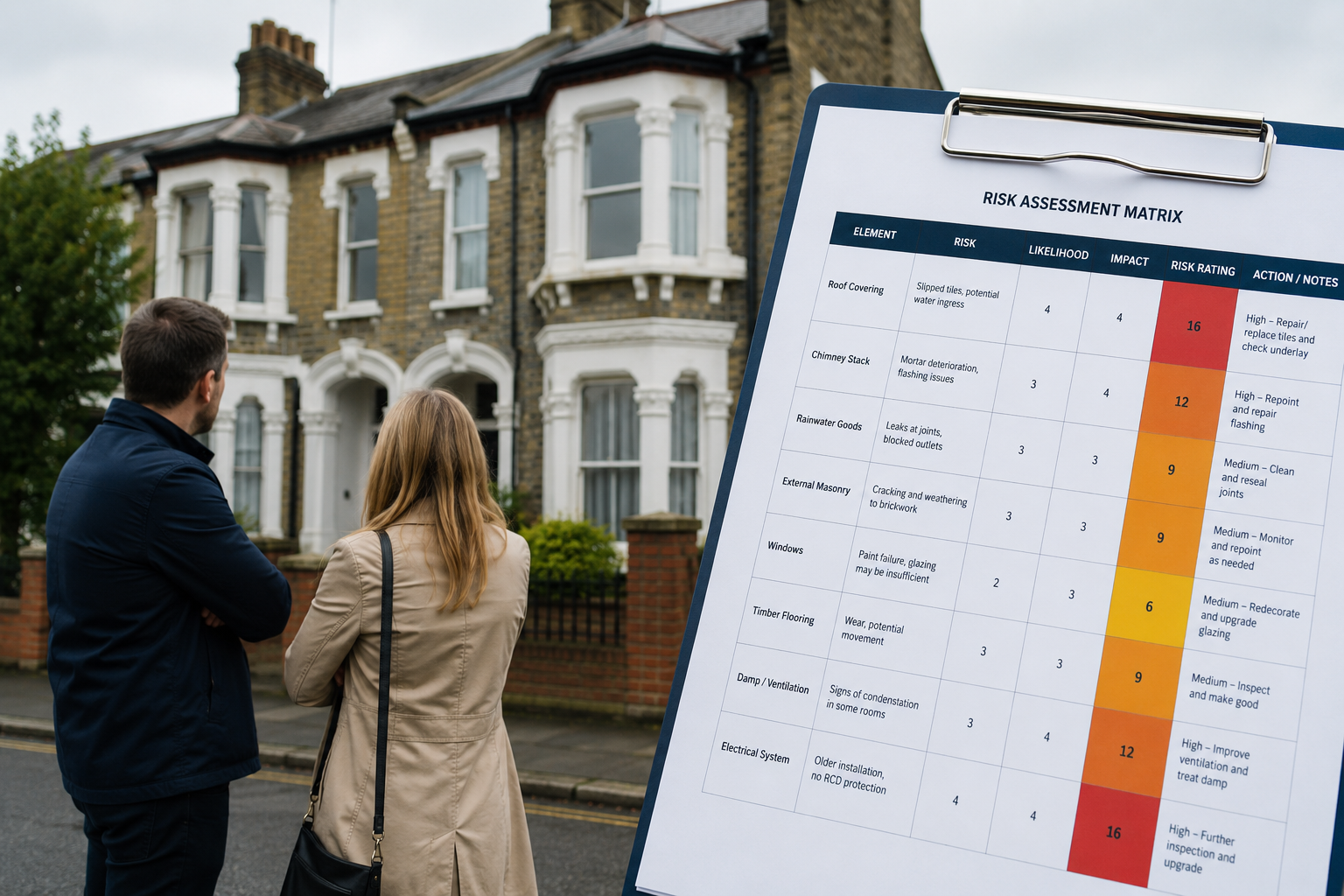

Practical Risk Assessment Framework for Flat Market Valuations in 2026

The following framework helps surveyors structure their risk assessment systematically in slow-moving or uneven markets.

Step 1: Establish the True Comparable Base 🔍

- Search a 6-month window first; extend to 12 months only if necessary.

- Exclude outlier sales (distressed sales, probate sales at undervalue, or sales between connected parties).

- Note the marketing period for each comparable.

Step 2: Assess Property-Specific Risk Factors ⚠️

Use a structured checklist:

- Structural condition (roof, walls, foundations, drainage)

- Tenure (freehold, leasehold, shared ownership)

- Lease length and ground rent terms

- Service charge history and reserve fund adequacy

- Fire safety documentation (EWS1 status)

- Planning or building regulations compliance

- Environmental risks (flood, subsidence, contamination)

For properties where subsidence is a concern, a specialist subsidence survey may be required before a reliable valuation can be formed.

Step 3: Apply and Document Adjustments 📋

Each adjustment should be:

- Specific — tied to a named defect or risk factor.

- Quantified — expressed as a monetary figure or percentage range.

- Evidenced — supported by contractor estimates, comparable data, or specialist reports.

Step 4: Consider Marketability, Not Just Value 🏠

A property can have a technically supportable valuation figure and still be effectively unmarketable. Surveyors should comment on likely time to sell and the depth of the buyer pool for properties with significant risk factors.

A property that will attract only cash buyers — because lenders will not lend on it — has a different effective value than one that is fully mortgageable, even if the headline figure appears similar.

Step 5: Apply the Appropriate Survey Level 📊

Not every property requires the same level of investigation. However, in a flat market where buyers are more selective, the case for a more thorough survey is stronger than ever.

- Level 2 surveys are appropriate for newer, standard-construction properties in good condition. See the complete guide to Level 2 Home Surveys for more detail.

- Level 3 Building Surveys are essential for older properties, non-standard construction, or any property where defects are suspected. The guide to Level 3 House Surveys explains when this level of investigation is warranted.

The Surveyor's Role in Protecting All Parties

In a flat, selective market, the surveyor's role extends beyond producing a number. It encompasses:

- Protecting buyers from overpaying for properties with hidden or underpriced risk.

- Protecting lenders from advancing against inadequate security.

- Protecting sellers from transactions that collapse late in the process due to undisclosed issues.

- Protecting the surveyor from negligence claims by producing well-reasoned, well-documented reports.

The professional and legal obligations of a RICS-registered valuer do not change with market conditions. But the practical application of those obligations demands greater care, greater specificity, and greater transparency in 2026 than in more buoyant periods.

Conclusion: Actionable Steps for Surveyors in a Flat Market

The core message of Flat Market Valuations in 2026 is straightforward: when buyers are more selective, surveyors must be more rigorous. A flat market does not forgive vague comparables, undocumented adjustments, or missed defects. The following steps will help surveyors deliver high-quality, defensible valuations in this environment.

✅ Actionable Next Steps for Surveyors:

- Refresh your comparable evidence standards — commit to a six-month search window as the default, not the exception.

- Build a structured defect quantification process — every significant defect should carry an estimated remediation cost range.

- Develop a tenure risk checklist — lease length, ground rent, service charges, and EWS1 status should be assessed on every leasehold instruction.

- Improve your client communication templates — plain-language explanations of value adjustments reduce disputes and build trust.

- Know when to recommend a higher survey level — a do I need a home survey conversation with clients should always address the complexity of the specific property.

- Use material uncertainty declarations appropriately — thin markets require transparent caveats, not false precision.

- Stay current on local market conditions — national indices are a starting point, not a substitute for local knowledge.

Flat markets reveal the quality of professional practice. Surveyors who invest in rigour, transparency, and clear communication will not only protect their clients — they will build the kind of reputation that generates referrals long after market conditions change.