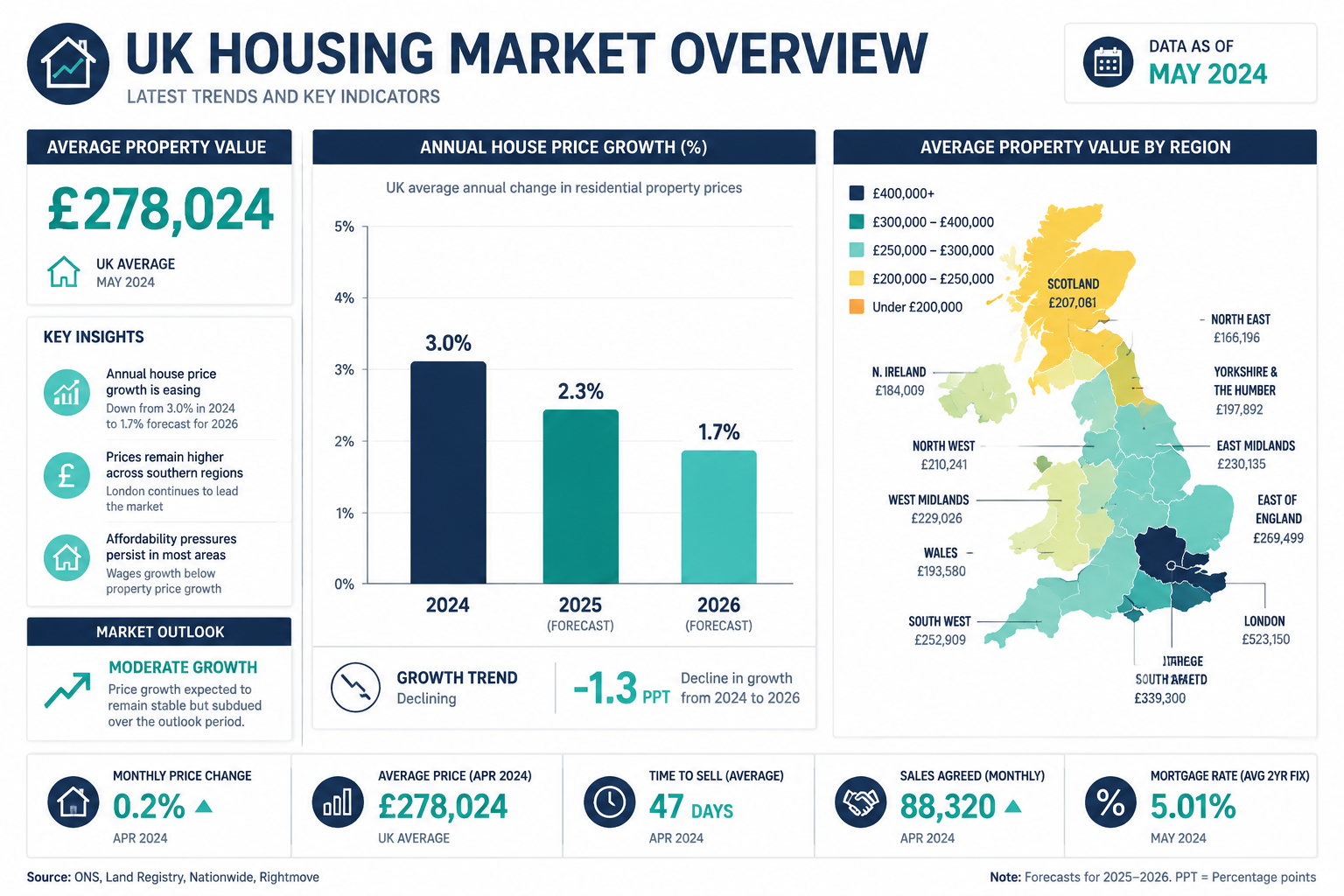

UK house prices fell 0.6% in May 2026, bringing the average property value to £278,024 — yet Rightmove and RICS forecasts still point to modest annual growth of around 2% by year-end [1]. That gap between short-term softness and medium-term recovery is precisely where first-time buyers can gain an edge. Valuing stabilizing house prices in a buyer's market: RICS tactics for first-time buyers in 2026 is not simply about knowing what a home is worth today — it is about understanding the forces shaping tomorrow's prices and using professional valuation tools to negotiate from a position of strength.

With mortgage rates averaging 5.68% on a two-year fixed deal and annual price growth slowing from 3% in April to 1.7% in May, the market has tilted toward buyers in many regions [1]. High stock levels, longer days on market, and seller motivation all create leverage — but only for buyers who understand how to read and act on credible valuations.

Key Takeaways

- UK house price growth slowed to 1.7% annually in May 2026, creating genuine negotiating room for first-time buyers.

- RICS-qualified surveyors provide independent valuations that can directly support lower offer prices and protect against overpaying.

- Regional variation is significant: London's market is expected to flatline in 2026, while other areas show more resilience.

- A professional building survey, not just a mortgage valuation, is the cornerstone of any sound buying strategy in a softening market.

- Government schemes such as Shared Ownership remain relevant tools for improving affordability when mortgage costs are elevated.

Understanding the 2026 Market: Why Stabilization Creates Buyer Leverage

The phrase "stabilizing market" can mislead. Stability does not mean stagnation — it means the frenzied bidding wars of 2021 and 2022 have given way to a more measured environment where data, not emotion, drives decisions.

Several converging factors define the 2026 landscape:

- Slowing annual growth: National price growth has dropped from 3% in April 2026 to 1.7% in May 2026 [1].

- Elevated mortgage costs: A two-year fixed rate averaging 5.68% compresses buyer budgets and reduces competition at every price point [1].

- London underperformance: London's average property price stands at £542,304, following a 1.8% decline in 2025, with expectations of flat prices throughout 2026 [2].

- Geopolitical headwinds: Instability in the Middle East has dampened consumer confidence and pushed lenders toward caution [1].

- Increased supply: More properties are sitting on the market for longer, giving buyers time to assess and negotiate.

"A buyer's market is not a gift — it is an opportunity that requires preparation. Without a credible valuation, leverage is theoretical."

For first-time buyers, this environment is genuinely different from the past decade. The question is not whether to buy, but how to buy intelligently.

What "Buyer's Market" Actually Means for Valuation

In a seller's market, asking prices are treated as floors. In a buyer's market, they become ceilings. The difference matters enormously when commissioning a valuation. A RICS-qualified surveyor operating under the Red Book Global Standards will assess market value based on comparable transactions, not aspirational asking prices. That distinction can translate directly into a lower offer — and a lower purchase price.

Valuing Stabilizing House Prices: RICS Tactics for First-Time Buyers in 2026

The Royal Institution of Chartered Surveyors (RICS) sets the professional and ethical standards for property valuation in the UK. For first-time buyers navigating a softening market, RICS guidance provides a structured framework that goes well beyond a simple price check.

The Three Pillars of RICS Valuation in a Soft Market

1. Market Value Assessment

A formal RICS valuation establishes what a property would realistically sell for between a willing buyer and a willing seller on the open market. In 2026, this figure often differs from the asking price by a meaningful margin — particularly in London and the South East, where price corrections have been most pronounced [2].

When a RICS valuation comes in below the agreed purchase price, buyers have documented grounds to renegotiate. Sellers who have been on the market for 60 days or more are frequently willing to accept revised offers rather than restart the process.

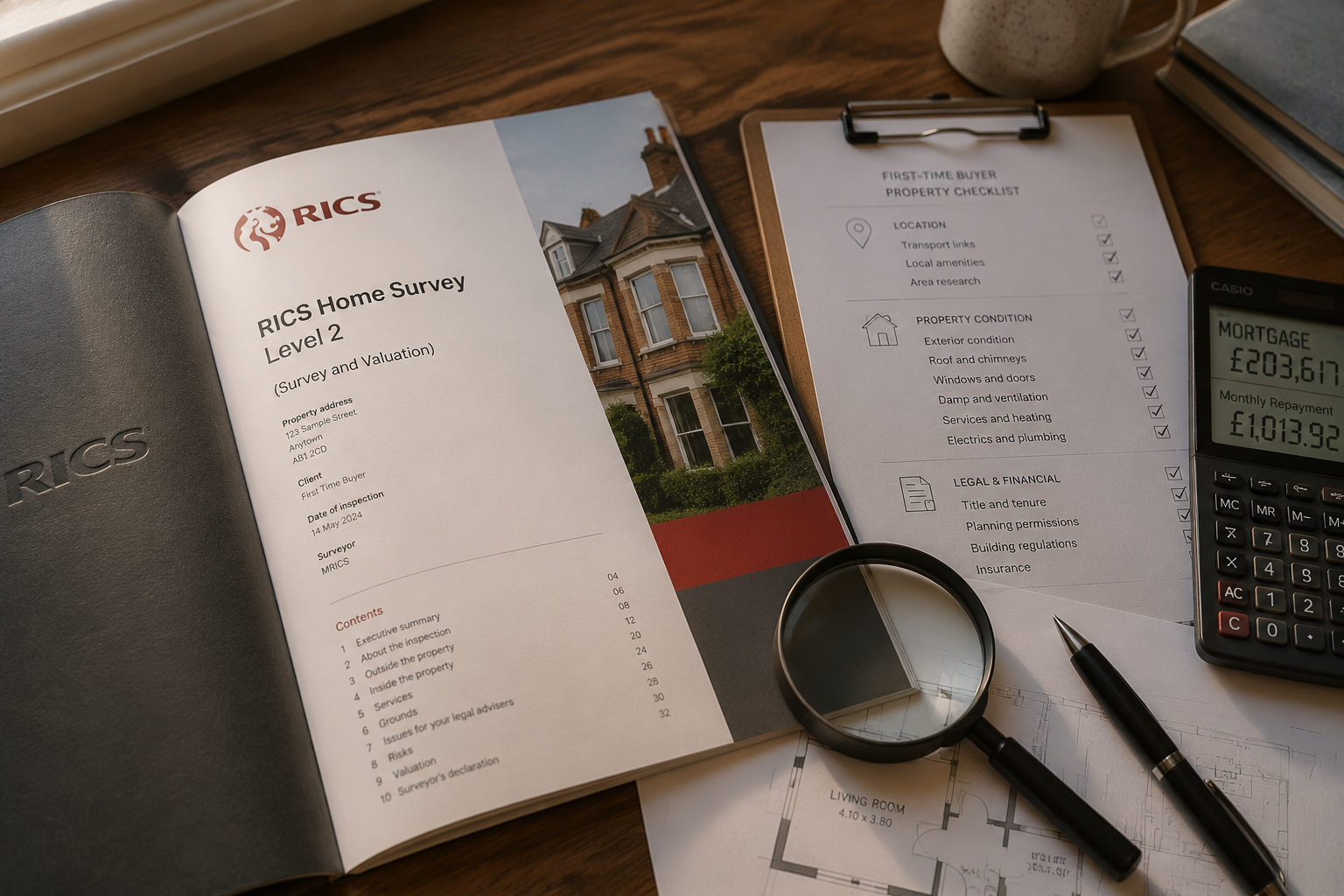

2. Condition-Based Adjustments

Market value alone does not capture the full picture. A property priced at £350,000 in a stabilizing market may carry £40,000 in remedial costs that a standard estate agent appraisal will never reveal. This is where a RICS building survey becomes a negotiation tool in its own right.

A Level 3 Building Survey — the most comprehensive option — covers:

| Survey Element | Why It Matters for Valuation |

|---|---|

| Structural integrity | Identifies subsidence, movement, or cracking |

| Roof condition | Flat roofs, tiles, and flashings carry significant repair costs |

| Damp and drainage | Hidden damp can cost thousands to remediate |

| Electrical and plumbing | Outdated systems may require full replacement |

| Windows and insulation | EPC ratings affect resale value and running costs |

Each defect identified is a line item in a post-survey renegotiation. Buyers who commission surveys before finalizing offers routinely achieve price reductions that far exceed the cost of the survey itself. For a detailed breakdown of what to look for, the ultimate house survey checklist is an essential reference.

3. Comparable Evidence

RICS surveyors use Land Registry transaction data, local comparable sales, and current market listings to benchmark value. In a market where prices are softening, recent comparables carry more weight than historical data. A surveyor who uses transactions from 18 months ago will produce an inflated valuation. Buyers should confirm that their surveyor is using evidence from the past three to six months.

Choosing the Right Survey Level

Not every property requires the same depth of investigation. The table below summarizes the options:

| Survey Type | Best For | Typical Cost Range |

|---|---|---|

| RICS Level 2 (HomeBuyer Report) | Standard properties in reasonable condition | £400 – £700 |

| RICS Level 3 (Building Survey) | Older, extended, or non-standard properties | £600 – £1,500+ |

| Specific Defect Survey | Known issue requiring focused investigation | £250 – £600 |

For most first-time buyers purchasing older stock — which dominates UK supply — a Level 3 survey is the more prudent choice. The comparison of Level 2 vs Level 3 surveys outlines the key differences in plain terms.

If a specific concern has already been flagged — such as a crack in a wall or suspected damp — a RICS specific defect survey can provide targeted analysis at a lower cost.

Negotiation Strategies Grounded in Professional Valuation

Valuing stabilizing house prices in a buyer's market: RICS tactics for first-time buyers in 2026 reaches its practical peak at the negotiation stage. A survey report is not just a risk document — it is a negotiating instrument.

Using Survey Findings to Reduce the Purchase Price

The process works as follows:

- Agree a purchase price in principle — subject to survey.

- Commission a RICS survey before exchanging contracts.

- Receive the survey report and identify material defects or valuation discrepancies.

- Obtain remedial cost estimates from qualified tradespeople.

- Submit a revised offer supported by documented evidence.

This approach is entirely standard and widely accepted by sellers and their solicitors. In a market where properties are taking longer to sell, most sellers will engage with a well-evidenced renegotiation rather than risk losing the buyer entirely [4].

Reading Market Signals: When to Push Harder

Not all properties offer the same negotiating room. The following signals indicate a seller who is more likely to accept a reduced offer:

- Property has been listed for more than 45 days without a price reduction.

- The seller has already purchased elsewhere (chain pressure).

- The property has previously fallen through (suggests prior issues).

- Asking price is above recent comparable sales in the same street or postcode.

- EPC rating is D or below (increasing buyer resistance due to energy costs).

In London specifically, where average prices are expected to flatline throughout 2026 [2], buyers in areas like Ealing, Chiswick, and Barnes are finding that sellers are more receptive to negotiation than at any point in the past decade.

Shared Ownership: A Structured Entry Point

For buyers whose budgets are stretched by elevated mortgage rates, Shared Ownership remains a viable route. Under this scheme, buyers purchase a share of a property (typically 25% to 75%) and pay rent on the remainder, with the option to "staircase" toward full ownership over time.

RICS valuations play a critical role here. A RICS shared ownership valuation establishes the full market value of the property, which determines the price of each share purchased. An accurate, independent valuation protects buyers from overpaying for their initial stake — a risk that is heightened when housing association asking prices are set without reference to current market conditions.

For a thorough overview of the Help to Buy process and its valuation requirements, the complete guide to Help to Buy valuations covers the key steps and common pitfalls.

Financial Readiness: Aligning Valuation with Affordability

A credible valuation strategy must sit within a realistic financial framework. RICS guidance consistently emphasizes that first-time buyers should assess their full cost position before committing to a purchase [4].

The True Cost of Buying in 2026

Beyond the purchase price, first-time buyers must budget for:

| Cost Item | Typical Range |

|---|---|

| Mortgage arrangement fee | £999 – £2,000 |

| RICS survey | £400 – £1,500+ |

| Solicitor / conveyancing fees | £1,200 – £2,500 |

| Stamp Duty Land Tax (SDLT) | 0% on first £425,000 (first-time buyers) |

| Removal costs | £500 – £2,000 |

| Initial repairs / redecoration | Variable |

With a two-year fixed mortgage rate at 5.68%, the monthly cost of a £250,000 mortgage over 25 years is approximately £1,640 — a figure that has forced many buyers to recalibrate their target price ranges [1].

Deposit Strategy in a Stabilizing Market

In a market where prices may soften further before recovering, a larger deposit serves two purposes: it reduces the loan-to-value ratio (improving mortgage rates) and provides a buffer against negative equity if prices dip before stabilizing.

RICS recommends that first-time buyers avoid stretching to the absolute maximum of their borrowing capacity in uncertain conditions [4]. A property purchased at a fair, survey-supported price with a 15% or 20% deposit is a far stronger financial position than one purchased at the asking price with a 5% deposit.

Long-Term Value Considerations

The 2026 market rewards buyers who think in five-to-ten-year horizons. While national annual growth has slowed to 1.7%, the underlying drivers of UK housing demand — population growth, undersupply of new homes, and structural constraints on development — remain intact [3]. Properties purchased at survey-supported prices in 2026 are well-positioned for the next growth cycle.

Buyers should also consider the reinstatement cost of a property — the cost to rebuild it from scratch — which is relevant for insurance purposes. A RICS reinstatement cost valuation ensures that buildings insurance is set at the correct level, protecting the investment from day one.

Practical Steps: Applying RICS Tactics Before Making an Offer

The following sequence consolidates the key RICS-informed tactics into a practical action plan for first-time buyers in 2026:

Step 1 — Establish your budget ceiling using current mortgage rates

Use a broker to confirm your maximum borrowing capacity at current rates (5.68% average for two-year fixed deals) and identify your comfortable monthly payment threshold.

Step 2 — Research comparable sales, not asking prices

Use Land Registry data and platforms like Rightmove's sold prices tool to identify what similar properties in the same area actually sold for in the past three to six months.

Step 3 — Commission a RICS valuation before finalizing your offer

An independent valuation provides documented evidence of market value and creates a defensible basis for negotiation. This is particularly important in London, where asking prices have lagged behind the correction in actual transaction values [2].

Step 4 — Commission a building survey appropriate to the property

For properties built before 1980, a Level 3 Building Survey is strongly recommended. The guide on whether a homebuyers survey is worth it provides a clear cost-benefit analysis.

Step 5 — Use survey findings to renegotiate

Present defect repair estimates alongside the survey report. A well-documented renegotiation is not aggressive — it is professional and expected in the current market.

Step 6 — Explore government schemes if affordability is tight

Shared Ownership, the Mortgage Guarantee Scheme, and First Homes are all active in 2026 and can materially improve purchasing power for eligible buyers.

Step 7 — Instruct a conveyancer early

Legal searches can reveal planning restrictions, flood risk, and ground stability issues that affect value. Instructing a conveyancer before the offer is accepted accelerates the process and reduces the risk of late-stage surprises.

Conclusion

The 2026 housing market presents a genuine window of opportunity for first-time buyers who approach it with the right tools. Slowing price growth, elevated mortgage rates, and increased supply have shifted negotiating power away from sellers — but that leverage only materializes when buyers are equipped with credible, professional valuations.

Valuing stabilizing house prices in a buyer's market: RICS tactics for first-time buyers in 2026 comes down to three core actions: commissioning an independent RICS valuation to establish true market value, ordering a building survey to quantify defect costs, and using both documents to negotiate a purchase price that reflects reality rather than aspiration.

Actionable next steps:

- Contact a RICS-qualified chartered surveyor to discuss the appropriate survey level for your target property.

- Use Land Registry sold prices data to benchmark asking prices against recent transactions.

- Speak to a whole-of-market mortgage broker to confirm your borrowing capacity at current rates.

- Review eligibility for Shared Ownership or other government schemes before ruling out properties at the upper end of your range.

- Read the complete guide on whether you need a survey when buying a house to understand your obligations and options.

The buyers who succeed in 2026 will not be those who move fastest — they will be those who move with the most reliable information.

References

[1] Could House Prices Fall – https://moneyweek.com/investments/house-prices/could-house-prices-fall?utm_source=openai

[2] London House Prices – https://moneyweek.com/investments/property/london-house-prices?utm_source=openai

[3] House Prices – https://moneyweek.com/investments/house-prices/house-prices?utm_source=openai

[4] Uk House Price Forecast 2026 – https://britishproperty.uk/guides/uk-house-price-forecast-2026?utm_source=openai